When it comes to assembling a well-rounded investment portfolio, the makeup and placement of U.S. equity allocations are key considerations. Tony DeSpirito, Global CIO of BlackRock Fundamental Equities, challenges conventional thinking to suggest that alpha-seeking strategies in U.S. large-cap stocks are deserving of a core position in portfolios.

Elections have been anything but easy for investors. What has been easy is financial conditions in the US relative to the level of policy rates, fostering the debate over the degree of policy restrictiveness as global monetary easing begins.

In this article, Russ Koesterich discusses why bonds are still not a reliable hedge for equities in an environment where inflation remains elevated and volatile.

Municipal bonds posted their strongest June performance since 2019. The asset class outperformed amid improving seasonal supply-and-demand dynamics. Looking ahead, July has historically been the strongest performing month of the year.

The world could be undergoing a transformation akin to past technological revolutions. But the speed, size and impact of that investment is highly uncertain. We think leaning into the transformation and adapting as the outlook changes will be key.

Rick Rieder and team argue that the economy is making further progress towards normalization and continues to offer a once-in-a-generation investing opportunity, which isn’t adequately represented by the benchmarks.

Macro worries meet AI wonderwall. Stocks have managed to climb a wall of macro worries, thanks to largely solid earnings that we believe can expand beyond AI beneficiaries and continue to support prices. As Q3 begins, we look for:

Market indexes can be a useful barometer of long-term performance. But the investment opportunity set need not start and end there. Fundamental Equities investor Alister Hibbert uses an unconstrained approach in seeking to identify those rare companies that stand out from the pack.

Municipal bonds deviated from U.S. fixed income assets and posted negative performance in May.

The Federal Reserve’s balance sheet is one of the world’s most important security portfolios. Yet, its ongoing importance for markets and financial conditions is often underappreciated.

In this article, Russ Koesterich discusses the YTD strength of energy stocks and why it could continue.

A defining feature of the post-COVID investment regime has been the persistence of elevated market uncertainty and volatility. The below visual highlights how this has led to a wider range of market performance outcomes, focusing in on the vast difference between the last two calendar years.

Strong Q1 earnings were a bright spot as sticky inflation and dimmed expectations for rate cuts cast some shade on U.S. equity markets. Fundamental Equities investor Carrie King looks beyond the headlines to offer four takeaways from the most recent earnings season.

Artificial intelligence (AI) and its unparalleled potential have powered stock market returns over the past year. Yet the market has more to offer, particularly as leadership may be poised to broaden beyond AI beneficiaries.

In this article, Russ Koesterich discusses why stocks are proving to be resilient in the face of higher rates and muted expectations for monetary easing.

How momentum and election cycles may shift the impact and timing of seasonal trends.

With yields at current levels, bond funds can lock in longer term yields, offer price appreciation potential and overall serve as a hedge against a possible hard landing. Though elevated cash balances worked during the Fed’s hiking cycle, we believe now is an opportunity for clients to consider adding duration given the potential for a Fed pause.

Elevated all-in yields in high yield credit present an attractive opportunity for income-seeking investors to lock in higher levels of income. Of course, that comes with a much higher degree of risk as compared to sitting in cash.

After a strong start to the year, equity investors are assessing whether a range of escalating risks will lead to continued volatility ahead. In this quarter’s Systematic Equity Outlook, we’ll explore macro and micro risks through a systematic lens, and how we’re positioning portfolios to harness alpha opportunities ahead.

In this article, Russ Koesterich discusses why a higher rate environment may still allow stocks to end the year higher.

Improve your income potential with a tactical, unconstrained strategy that sources opportunities across geographies and asset classes. BlackRock Multi-Asset Income Fund takes a risk-first approach while seeking to deliver a consistently attractive yield.

Why the current momentum trade, despite stretched valuations, could continue.

Market update from BlackRock's municipal bond team.

A favorite Mark Twain aphorism states, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

What next for stocks after a strong start to 2024? While a near-term pullback wouldn’t be surprising, we see fuel for the positive momentum to continue throughout the year ― but with selection growing more important.

After a career in design that included restoring furniture and textiles for nine presidents, Iris Apfel became a fashion icon in her 80s. This isn’t a commentary on how to live out one’s retired years (some may air-quote that term). It’s to drive home the point that she lived – really lived – to 102.

Russ Koesterich discusses the reason that bonds are not providing the same diversification benefit to equities as in prior decades.

Gargi Pal Chaudhuri, Head of iShares Investment Strategy and Markets Coverage at BlackRock, and Anne Ackerley, Head of BlackRock’s Retirement Group, sat down for a conversation about women and investing – the good, the bad, and the diversified.

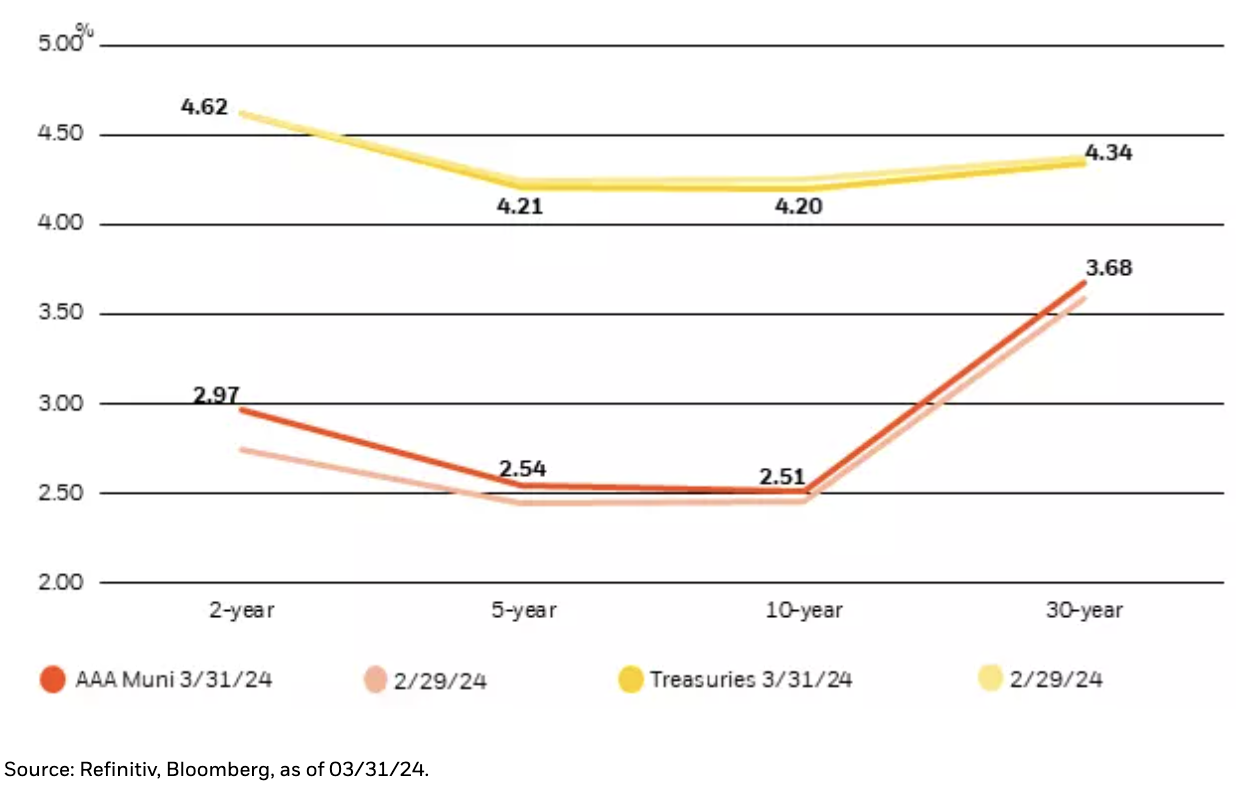

Municipals posted positive performance and outperformed comparable Treasuries in February. We expect supply-and-demand dynamics to turn less supportive in the coming months. After patience to start the year, we would view any material backup as an opportunity to buy.

We monitor battery prices, elections and market attention on climate resilience for their impact on transition-related investment opportunities and risks. U.S. stocks were mostly flat last week, while 10-year U.S. Treasury yields fell further. Markets still expect the first Federal Reserve rate cut around mid-2024.

Q4 earnings revealed a tale of two markets in the U.S., with tech and internet players hitting home runs as other sectors and industries played small ball in comparison.

We get granular as the environment for risk-taking is supportive for now. That’s why we like euro area high yield credit, emerging market debt and U.S. stocks.

The shift from a regime of secular stagnation to one of reflation is contributing to both a broadening of global earnings growth and significantly higher dispersion in company results and performance.

22%. That is the average increase in potential retirement spending that individual savers in defined contribution plans can achieve when they embed guaranteed retirement income solutions into a target date fund. For lower-income workers, it’s a 25% increase.

In this article, Russ Koesterich discusses the reason behind the recent resiliency of stocks, despite rising rates.

We see Japan stocks climbing higher on robust earnings, corporate reforms and a Bank of Japan likely worried about returning to a chronic deflationary mindset.

We think market optimism can persist for now but stay nimble. We get more active in our long-term portfolios given a greater dispersion of returns.

The deceleration of the core PCE (Personal Consumption Expenditures) inflation rate in the second half of 2023 catalyzed a pivot in monetary policy messaging and shifted market pricing for the path of policy rates in 2024.

Japanese stocks were standout performers in 2023 after years of stagnation and deflation left Japan an unloved investment destination. Can the positive momentum continue in 2024? BlackRock’s Belinda Boa believes it can and sees the makings of a rags-to-riches story with staying power ― and abundant investment potential.

Municipal bonds posted negative total returns as the market reassessed macro expectations. Seasonal supply-and-demand dynamics were supportive, albeit less so than in prior years.

In this article, Russ Koesterich discusses why a different approach to portfolio construction within equities is warranted in 2024.

After initial optimism at the start of 2023 spurred strong performance, munis subsequently struggled as the Fed continued its tightening policy, raising fed fund rates to 5.25%−5.50%, before pausing in September.

What’s in store for stocks after they climbed a wall of worry to exceed expectations in 2023? Fundamental Equities Global CIO Tony DeSpirito sees a rich hunting ground for stock pickers and offers four insights for 2024 ― from sector likes to international opportunities.

Factors are long run drivers of portfolio risk and returns. Having strategic allocations to factors may increase a portfolio’s expected return.

Markets in 2023 kept investors on the edge of their seats. Groundbreaking technological advancements, mega-popstars being blamed for summertime inflation, and a December Fed pivot were just a few of the plot twists.

Risk assets surged to end 2023 as the Federal Reserve blessed market hopes for rate cuts. That momentum could persist for some time as inflation cools.

In this article, Russ Koesterich discusses why equity performance in 2024 may be more muted and warrant more focused positioning across segments of the market.

20 years into retirement, most retirees have spent only 20% of their savings. We talked to retired participants to understand why–and what it means for the next generation of retirees.

We think 2023 stressed the value of adapting to a new volatile macro regime and leveraging investment insight and structural forces to find opportunities.