Bond markets expect more cuts than the Fed is signaling, and this expectation largely reflects a return to pre-COVID dynamics of low inflation, massive central bank support, and suppressed term premia.

The use of “factors,” or broad and persistent drivers of investment returns, has grown rapidly in equity markets, but with less adoption in fixed income.

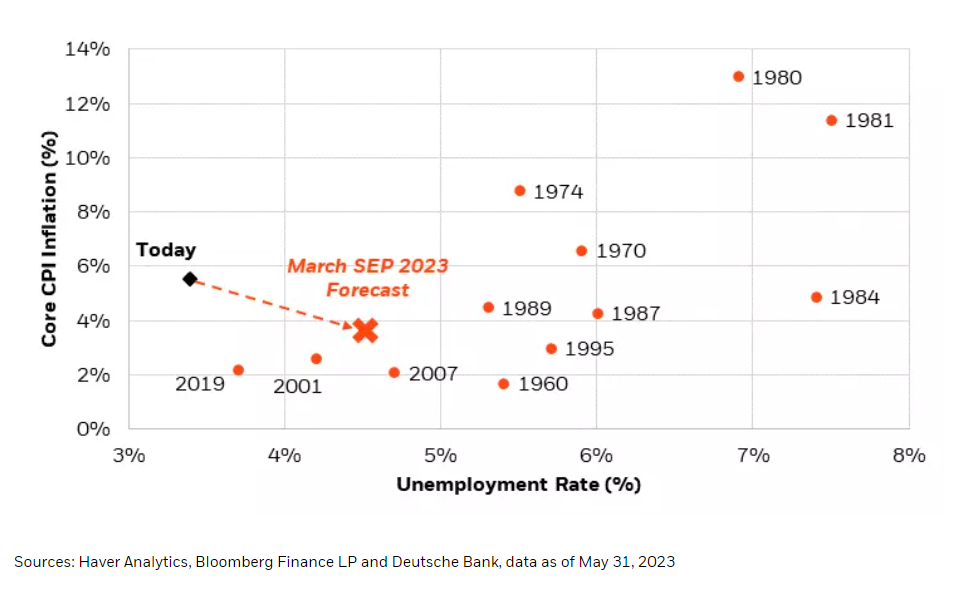

In the same way that a swimmer can make the biggest splash by jumping off of a higher diving board, so too fixed income asset returns can appear prospectively most attractive after a prolonged back up in rates.

Municipal bonds posted historic total returns of 5.90% in November. Rallying interest rates led the way, while strong demand aided outperformance versus Treasuries.

Insurance is making national headlines in 2023 as major providers retreat from writing new policies in large parts of the country and renewal premium prices skyrocket.

Q3 earnings season had many familiar refrains relative to the year’s first two quarters. One difference was a return to positive earnings growth for the first time since Q3 2022. Still, the market wasn’t unanimously cheering the results.

Generative artificial intelligence (AI) is firmly on the scene and set to change the way we live and work. NVIDIA CEO Jensen Huang, an AI pioneer and visionary, is optimistic and energized.

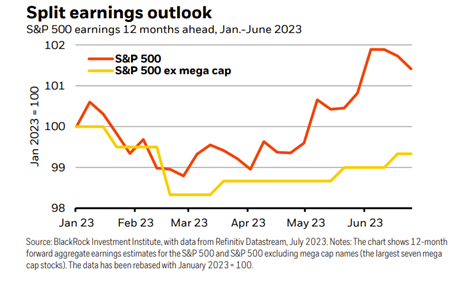

Year-to-date, technology has outperformed the broader market largely given the prevalence of low leverage, high profitability and consistent earnings across many names in the mega-cap tech space.

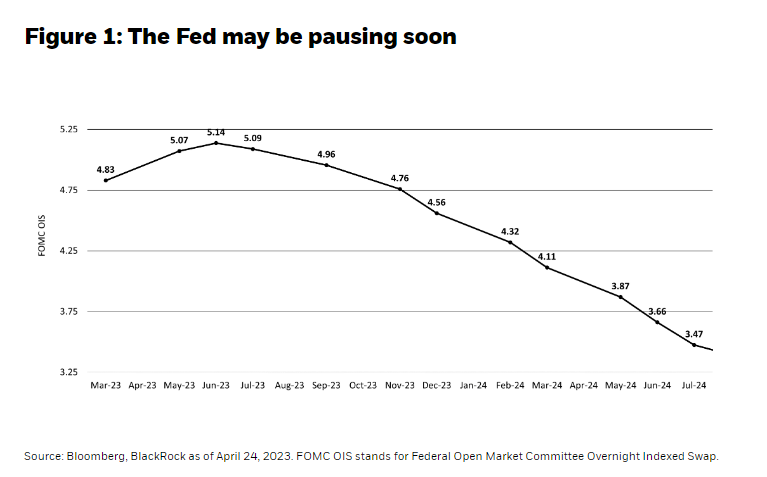

The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios. In this market regime, we believe duration serves well as hedge and equity diversifier.

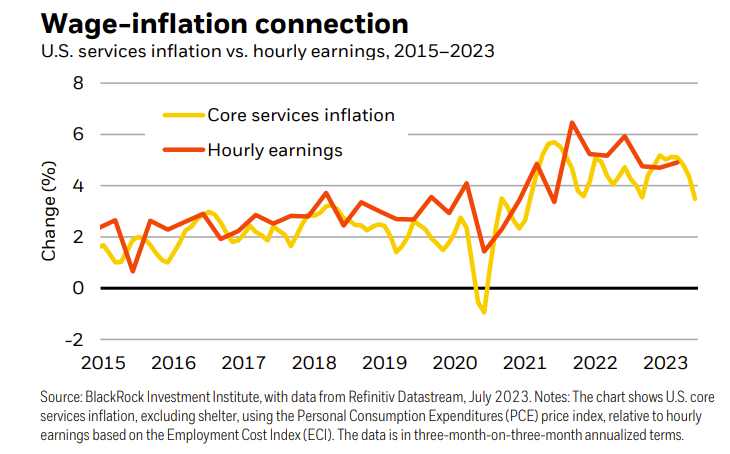

Despite progress on bringing down inflation from mid-2022 highs, data from online job postings suggests that wage pressures may be reaccelerating. Beneath the surface, growing divergence in wage gains across occupation categories may be adding a layer of complexity to the outlook for labor markets.

As investors face continued macroeconomic and market uncertainty, evolving the 60/40 portfolio of stocks and bonds to include alternative investments may help build portfolio resiliency.

Municipal bonds sold off considerably in September alongside vastly rising interest rates.

With all eyes on generative AI (genAI) and its transformative potential, individual investors’ interest has been piqued. The market-moving innovation certainly has generated a lot of hype ― and questions. Equity CIO Tony DeSpirito parses three reasons for excitement and three areas for awareness.

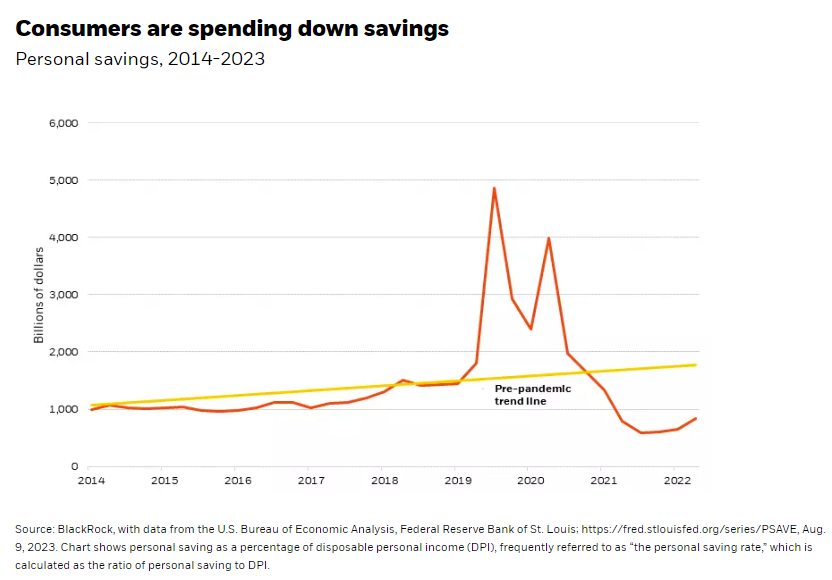

Global central bank hiking cycles have dominated financial market headlines for the last 18 months, keeping many investors on the sidelines, hiding out in cash as inflation and the resulting rate hikes were serious headwinds to returns.

Rising rates in the second half of the year have brought year-to-date returns for the US Aggregate (“Agg”) benchmark index negative.

U.S. stocks typically post their best returns in the final quarter of the year. Our review of S&P 500 performance since the index’s inception in 1957 found an average Q4 uptick of 4%. (Q1 was next best at an average of 2%.)

The prevailing narrative about the U.S. economy is that it’s ‘resilient’: despite rapid rate hikes, economic growth has held up and may even be accelerating.

In many ways, 2023 continues to be the mirror image of 2022, with the most volatile assets being some of the best performers for much of the year.

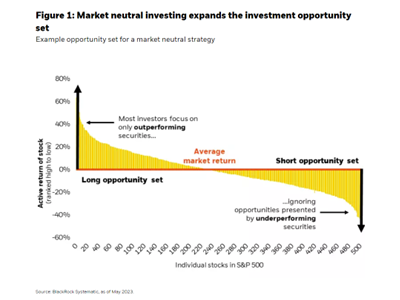

When markets are in a rising tide, all boats (aka stocks) can benefit. When the waters are choppier, active equity selection aims to identify the sounder vessels. Tony DeSpirito reviews five reasons why he believes the new environment is setting up to favor an active approach.

BlackRock and Human Interest have found that American workers earning less than the national average are not saving due to lack of access to saving tools. Broadening access requires an intuitive and automated approach to retirement savings.

Municipals posted negative total returns amid rising interest rates. Issuance exceeded tempered expectations, while demand waned as performance struggled.

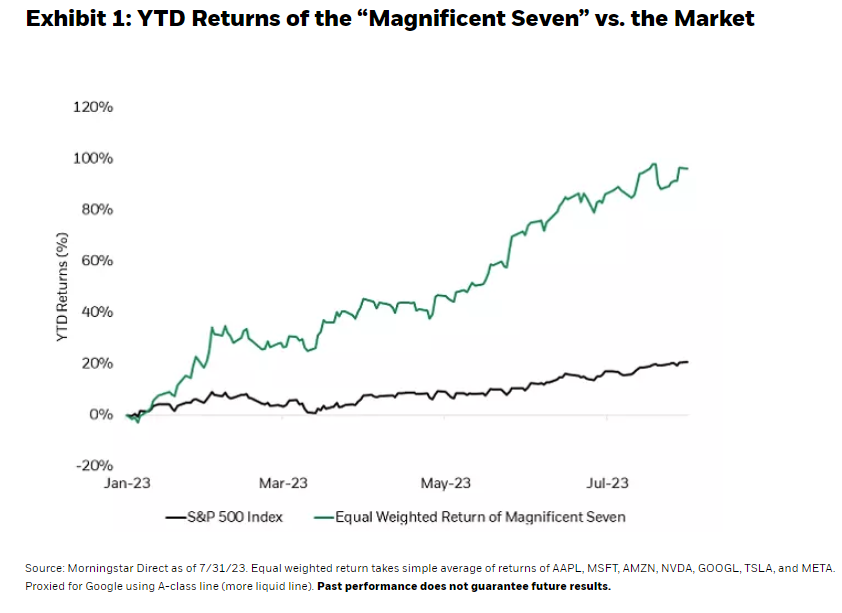

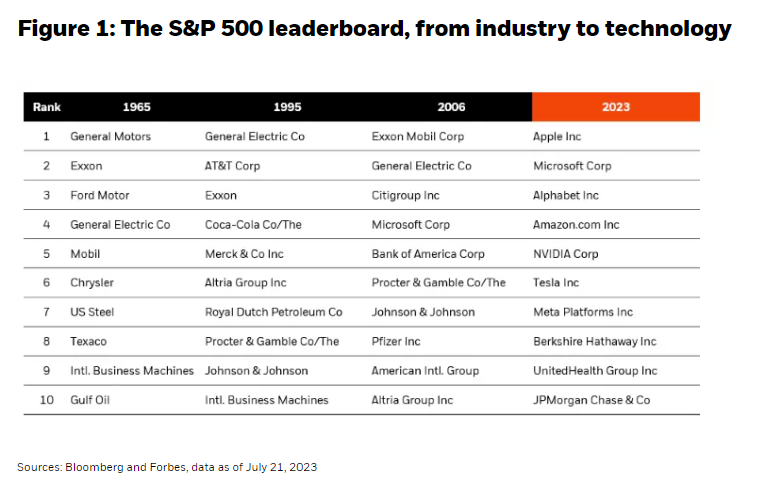

Seven mega-cap US-based companies – Apple, Microsoft, Amazon, Google, Nvidia, Tesla, and Meta (Facebook) – have stayed top of mind for many investors this year.

As multi-asset income investors, we seek to help a wide range of clients meet their income needs. The benefits of an income-centric approach are especially relevant for investors as they enter retirement – and that’s especially true today. We bring that to life with two case studies.

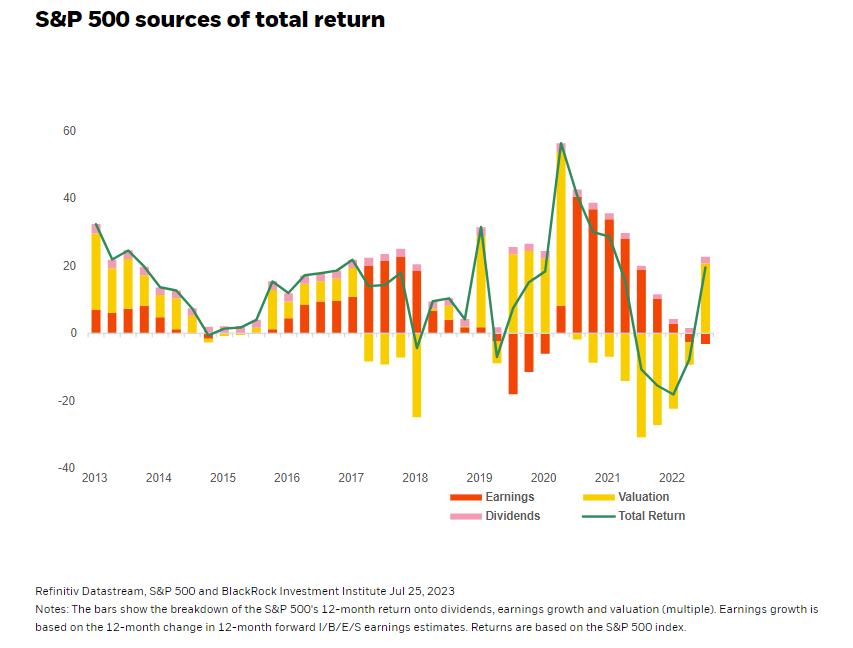

U.S. companies broadly notched better-than-expected results in the second quarter, even as overall earnings growth for the S&P 500 saw a decline. Equity investor Carrie King sees more interesting developments beyond the numbers and posits one area that may be getting tired as another readies for a reawakening.

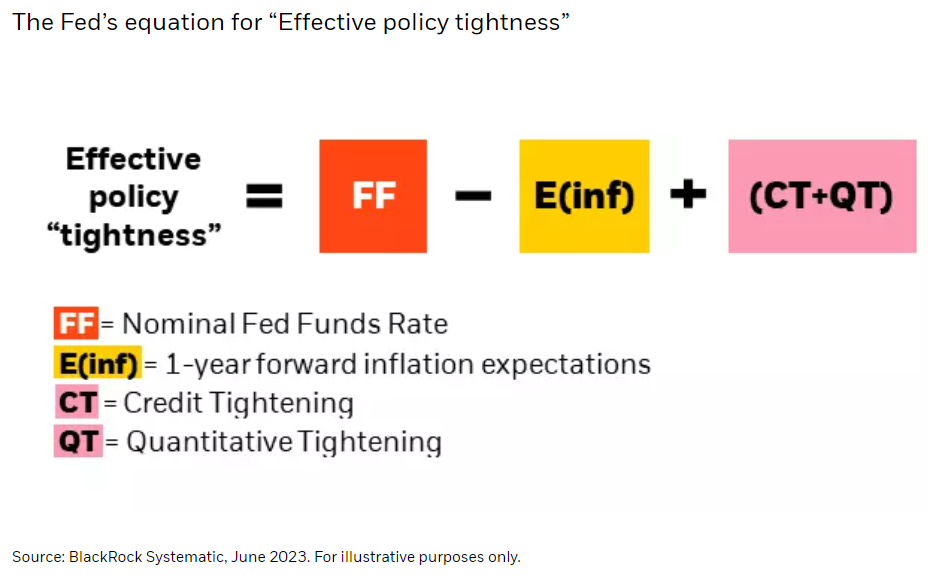

Monetary and fiscal policy are typically thought of as independent tools that central banks and governments use to manage the economy.

U.S. corporate earnings have stagnated for a year, but Q2 beat a low bar. Expectations of improving margins look rosy. We stay selective in equities.

Following the YTD strength in equity markets, Russ Koesterich discusses how a combination of cyclical, and a growth bias may serve investors well in today’s market.

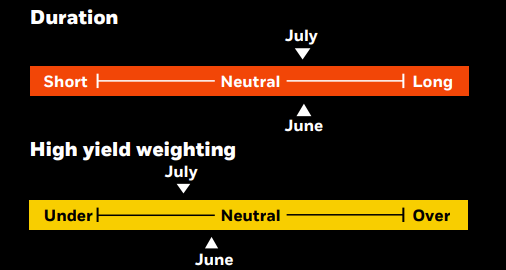

We maintain a neutral-duration posture overall. We prefer an up-in-quality bias and have become increasingly selective in non-investment grades.

For the better part of the last century, the largest companies in the world were those that produced physical property – traditional transportation machines, the energy that powered them, or the capital that financed them.

The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios.

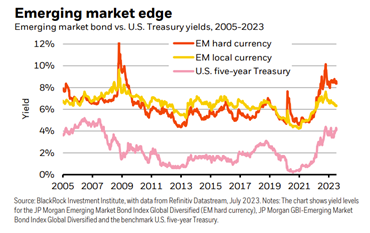

We see emerging markets better withstanding volatility and benefiting as supply chains rewire. We switch our EM debt preference to hard currency from local.

The economy and markets that have emerged from the pandemic fundamentally changed. For equity investors, we believe this means a different opportunity set than the one that prevailed over the past decade and a half ― and one that favors alpha (excess return) over beta (market return).

Russ Koesterich CFA, JD, Managing Director, and Portfolio Manager discusses how improving economic expectations may suggest adding to cyclical areas of the market.

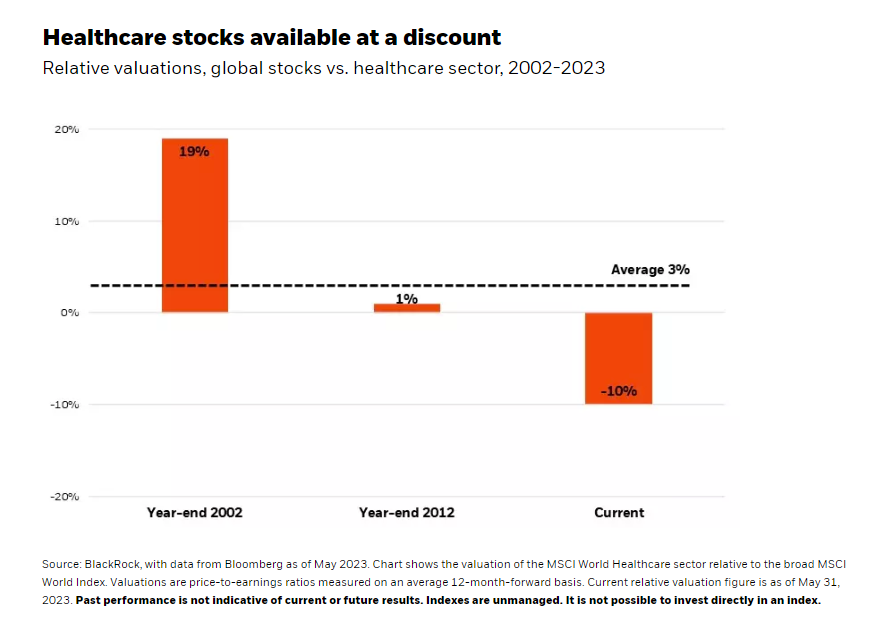

Healthcare stocks rank high on our like list, boasting a history of resilience amid both inflation and recession as well as attractive growth prospects thanks to potent innovation. Dr. Erin Xie examines the opportunity.

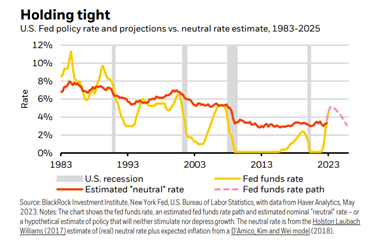

Central banks are set to hike policy rates this week. Markets expect rate cuts to soon follow due to cooling inflation, whereas we see central banks holding tight.

So far in 2023, equity markets have shrugged off banking stress, recession risk, and monetary tightening in favor of a more optimistic view. While risks remain, alternative data suggests that inflation may fall faster than expected as the economy remains relatively healthy.

We favor emerging market (EM) to developed market (DM) assets on a brighter macro backdrop. We get granular and harness mega forces, per our playbook.

Municipal bonds posted positive absolute and relative performance in June. Modest primary and secondary supply was outpaced by improved demand. While July has historically been a top-performing month, we maintain some near-term caution.

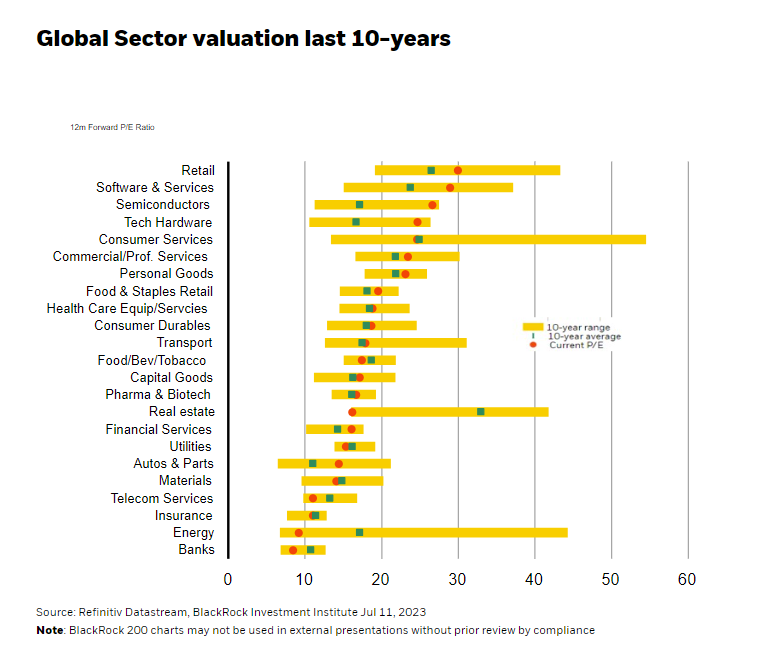

Factor investing can help drill through broad sector labels to help investors better understand past performance and expected returns.

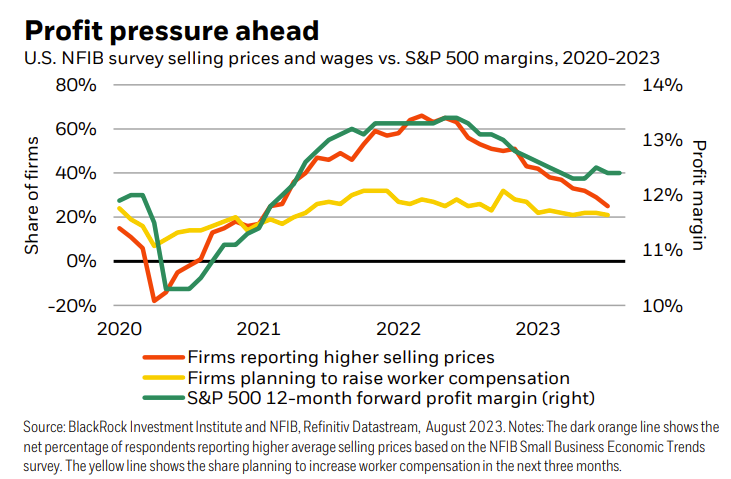

Higher expected corporate earnings mask broad pressure under the surface. We see more earnings pain ahead and look for opportunities at the sector level.

We see different and abundant opportunities in the new macro regime. We go granular within asset classes, regions, and sectors – and harness mega forces.

Financial advice often focuses on boosting personal savings rates and maximizing return on investment during a worker’s accumulation years. Equally important, however, is the decumulation process, when people spend those savings in the form of income.

The US Federal Reserve (“Fed”) paused rate hikes in June, but signaled it expects to deliver 50 basis points of additional hikes this year.

An ounce of optimism, a pound of prudence. It’s still a good time to be measured about taking risks in equities, but we believe the longer-term horizon holds particular promise for active stock pickers.

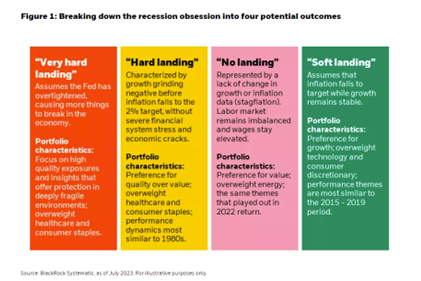

Macroeconomic uncertainty has remained front and center in 2023 as the new investment regime continues to play out. Inflation remains above central bank targets and some signs of economic weakness have started to surface in the wake of rapid monetary tightening.

Since the March trough the S&P 500 Index has gained around 14% and ten-year Treasury yields have risen roughly 0.50%. As market conditions have improved, inter-asset correlations have also shifted.

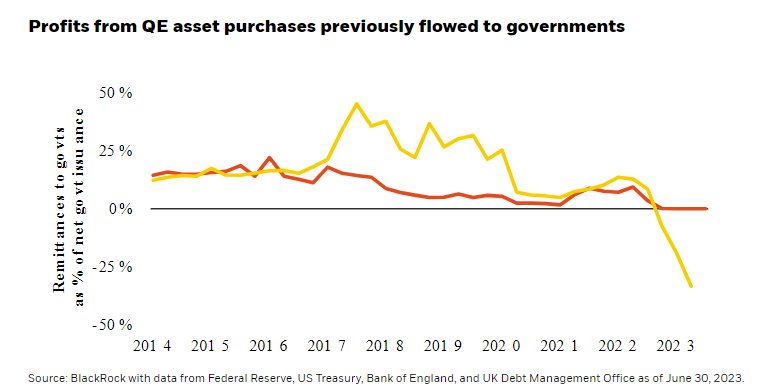

The exit from a decade of very low interest rates, via the most aggressive hiking cycle since 1980 has laid bare the distorted financing incentives that became entrenched in the years between the Global Financial Crisis in 2008 and the end of pandemic-era monetary policies in 2022.

Sticky inflation looks to compel developed markets (DM) central banks to crank policy rates higher – and keep policy tight for longer. The Federal Reserve paused last week but pointed to more hikes on the way.

Artificial Intelligence (AI) has garnered widespread attention with the public launch of ChatGPT. Learn how these same technologies can be used in investing.

With the passage of SECURE 2.0, new in-plan emergency savings solutions are on the horizon. What have the past five years of research taught us about the connection between short-term and long-term financial security? And how can 401(k) plans benefit from lessons learned?