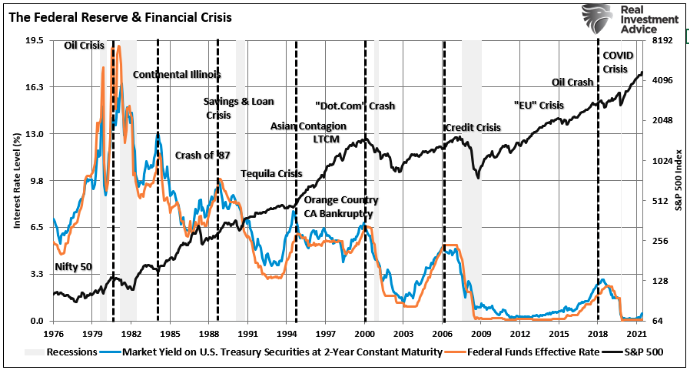

Could the Fed trigger the next “financial crisis” as they begin to hike interest rates? Such is certainly a question worth asking as we look back at the Fed’s history of previous monetary actions.

Do rising interest rates matter to the stock market? Many in the financial media and advisory community are scrambling to locate periods where rates rose along with stocks. Has it happened? Absolutely. However, it was only a function of timing until it mattered.

While the Fed notes valuations are elevated, the crucial message to investors gets obfuscated. From current valuation levels, the expected rate of return for investors over the next decade will be low.

“Is cash a good hedge?” It’s a focus of a recent article discussing “fast” versus “slow” risk which examined the financial impact on equities and cash over long-term periods.

Charting the stock market “melt-up” in prices, and the Fed’s naivety of the laws of physics may be of benefit to younger investors. After more than a decade of rising prices, accelerating markets seem entirely normal, detached from underlying fundamentals. As a result, new acronyms like “TINA” and “BTFD” get developed to rationalize surging prices.

Fundamentally speaking, there are more than a few indications that 2022 earnings estimates are still overly exuberant. However, the bullish optimism currently supports rising stock prices.

What If I told you that 40% of the bull market rally over the last decade was from buybacks alone? That may not be as crazy as it sounds.

While the promise of a continued bull market is very enticing, it is essential to remember that all markets ultimately complete a “full cycle.” Therefore, if your portfolio, and eventually your retirement, depends on the thesis of an indefinite bull market, you should at least consider the following charts.

Like all rules on Wall Street, Bob Farrell’s rules are not hard and fast. There are always exceptions to every rule, and while history never repeats exactly, it often “rhymes” closely.

We dig into the bullish and bearish case for the market as we head into the end of the year. Currently, investors face a conundrum between year-end seasonality and the Fed starting to taper its bond-buying program.

Is the risk of a more significant correction over now that the expected 5% decline is complete? That was a hotly debated question after this past weekend’s newsletter supporting the idea of a reflexive rally into year-end.

No. We are not repeating the “Roaring 20’s” analog. Ben Carlson had a recent post asking if the “Roaring 20’s” are already here?

The fact we have the lowest interest rates in 5000-years is indicative of the economic challenges we face.

On Monday, stocks solidly cracked below the 50-dma, but the bounce off the lows has investors asking if it’s “time to buy?”

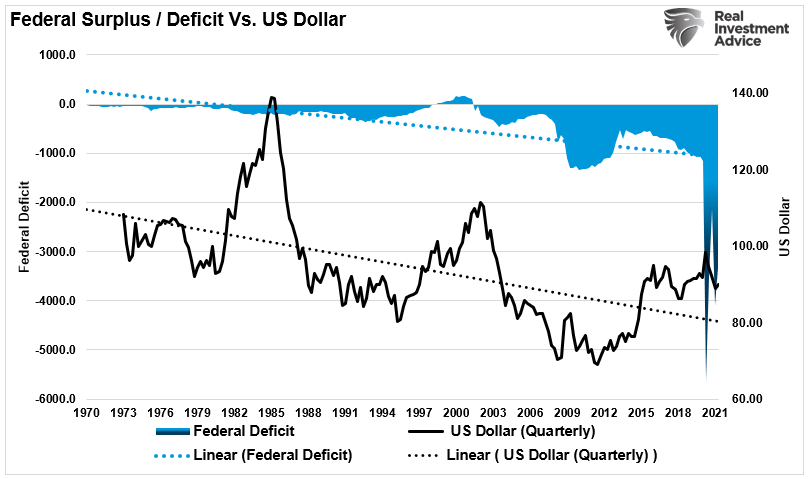

After 40-years of economic erosion, there are still deficit deniers.

We don’t disagree the S&P 500 could well hit a target of 5000. But, let us be honest about the reasons why...

Gold. What’s wrong with it? From spiking inflation, falling real interest rates, and massive money printing, it seems logical that gold, a touted inflation hedge, should be rising. Yet, so far this year, gold has done little.

As the Fed started to talk about “taper,” the “bulls” sent a stern warning with a 2% “crash” they shouldn’t. After a couple of weeks of several Fed speakers discussing the need to reduce monetary accommodation, a quick sell-off brought had Powell singing a “dovish” tone at the recent Jackson Hole summit.

The question of Japanization in the U.S. continues as the S&P 500 tracks the Nikkei of 1980.

Young investors are taking on personal debt to invest in stocks.

“Pet Rocks” first appeared in the mid-70s as a novelty item. Just recently, digital NFT’s of “pet rocks” sold for over $100,000.

In the fastest bull market in history, the S&P 500 doubled from its pandemic lows.

Did the Fed’s “monetary policy experiment” fail?

The question I get most often is “when is the next bear market?” There are three specific items that tend to predict bear markets and recessions with some accuracy.

The data shows the Fed is behind the surging wealth gap.

Was the second quarter the peak of economic growth and earnings?

“Past Performance Is no guarantee of future of results.” Such is the disclaimer below every performance chart produce by the financial marketplace.

A few years ago, Paul Wallace penned an article entitled: “GDP Is A Grossly Defective Product.” The recent release of the Q2-2020 report reminded me of it as the media fawned over the 7.6% print.

In this past weekend’s newsletter, I discussed the issue of the markets next “Minsky Moment.”

It’s now official that the recession of 2020 was the shortest in history.

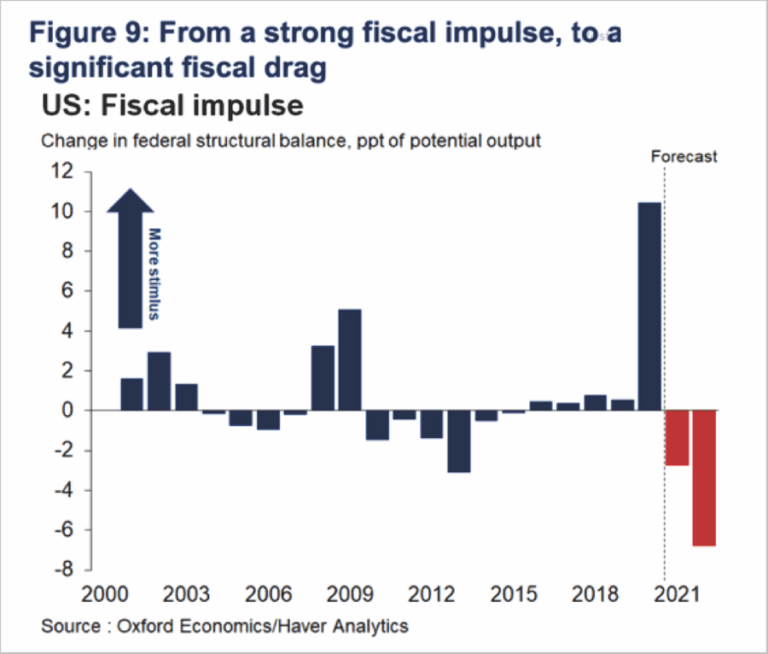

Monetary policy is not expansionary despite widespread belief otherwise.

Knowledge vs. experience. When it comes to investing, such is what separates long-term success from failure.

Is the retail investor rampage over?

Bond yields are sending an economic warning as this past week 10-year Treasury yields dropped back to 1.3%.

“Warnings From Behind The Curtain” almost sounds like the title of a good “Cold War” fiction novel.

In Part-2 of “Capitalism” does not equal “Corporatism,” we delve into why bailouts support corporatism and how to fix the system.

Wall Street is once again in the midst of a “money heist” from naive investors.

A couple of weeks ago, in “Warning Signs A Correction Is Ahead,” we said quite a few indicators set the stage for a pick-up in volatility.

Bull markets always seem to end the same – slowly at first, then all at once.

Much like “Humpty Dumpty,” despite the Fed’s best efforts, you can’t create permanent inflation from artificial growth.

Over the last couple of months, the Fed started its campaign to prepare markets for a “taper” of its asset purchases.

After a decent rally from the recent lows, there are multiple warning signs a correction approaches.

The media is buzzing with claims of an “Economic Boom” in 2021.

Bear markets matter, and they matter much more than you think.

I can understand the confusion when this past week I discussed the issue of “If everyone sees it, is it still a bubble?”

“The strong economic recovery will not get interrupted by inflation or a credit crunch, and the market will soon reach 4,500.” – Ed Yardeni via Advisor Perspectives

Over the long term, confusing market crashes and bear markets can be detrimental to investor outcomes.

“If everyone sees it, is it still a bubble?” That was a great question I got over the weekend.

The recent NFIB survey suggests we are only in an economic recovery, not an expansion.

One of the interesting aspects of “bull markets” is the further they go, the lower forward returns fall.