Picture yourself in charge of the government of a rich country. You discovered soon after taking office that you are unable to pass structural reforms, so you have relied on easy monetary policy for growth. This worked well while there was spare capacity, but now the economy is nearing full employment and slowing and monetary policy is clearly losing effectiveness. How to keep growth going? The best strategy is to reform, but most developed countries are more likely to return to deficit spending – Big Fiscal – than to reform. This presents a dilemma, because fiscal spending is costly in already heavily indebted countries.

We set out what a return to Big Fiscal means for developed countries and why Emerging Markets (EM) countries for the most part are unlikely to pursue a similar approach.

Introduction

Demand stimulus has been in fashion in developed countries since the 2008/2009 financial crisis. Monetary policy in particular has been popular with zero interest rate policies and Quantitative Easing (QE) forming the backbone of macroeconomic policies in the UK, Japan, Europe and the United States. This may now be changing.

Financial markets have recently signalled growing concern about the declining marginal effectiveness of monetary policy as a means of sustaining growth and asset price appreciation. This reflects the fact that economies are nearing full capacity and asset prices have become very expensive.

The only sustainable remedy to the diminishing effectiveness of demand stimulus is to re-engage in supply-side reform, but this is generally outside the remit of central banks.

Unfortunately, governments have generally been loath to reform. It is more likely that developed countries will return to fiscal stimulus as their economies slow, i.e. Big Fiscal looks set to stage a return. Experts are lining up to furnish arguments for greater public spending. While many of these arguments are dubious, this may not deter politicians keen to deliver strong growth.

In our view a return to Big Fiscal will increase already high debt levels, reduce trend growth rates and possibly pave the way for higher inflation, especially in countries with low domestic savings rates.

EM countries are generally wary of relying heavily on deficit spending. While self-imposed fiscal discipline in EM can seem irrational to outsiders, it is in fact entirely rational within the EM political context, because poor populations in EM countries are generally intolerant of macroeconomic instability. From the perspective of an investor, of course, fiscal prudence is a good thing. In EM, investors learned the lesson long ago to go underweight when governments go overweight. As developed countries return to Big Fiscal, investors in those developed countries may soon have to learn the same lesson.

Diminishing effectiveness of monetary stimulus

Demand stimulus has been the mainstay of macroeconomic policies in developed countries since the 2008/2009 financial crisis. The reliance on demand stimulus made sense in the context of large output gaps. Most governments ignored the structural causes of crisis, such as excess debt.

Monetary stimulus has been the preferred method of demand stimulus even though many have also relied heavily on fiscal policy. Quantitative Easing (QE) was a genuine revelation. The ability to push real yields below zero all the way out to thirty years and beyond was entirely novel. The prospect of unprecedented low yields as far as the eye could see boosted hopes of a strong economic recovery, especially in the US, where banks had also been recapitalized .1 Given the starting point of deep recession and rock bottom asset prices, both the economy and stocks were able to stage strong improvement and monetary policy was hailed as saviour.

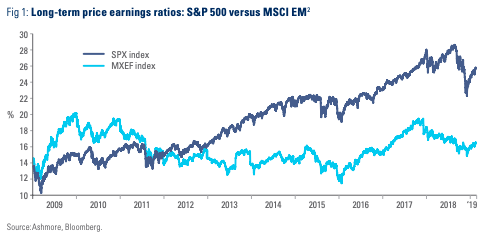

Sadly, it is the nature of economic reality that all good things come to an end. By now, the long-term price earnings ratio for US stocks has moved way out of line with price earnings in non-QE sponsored markets, including EM. Additional asset purchases at this point would merely inflate a bubble.

Monetary policy has also become less effective in terms of stimulating growth as most Western economies now operate near to their full potential. This means that, barring significant slowing, central banks face big macroeconomic trade-offs if they continue to ease.

Markets have acknowledged the emerging limitation to monetary stimulus. The reaction to ECB’s recent announcement of a third wave of Targeted Longer Term Refinancing Operations (TLTROs) was tepid. The reaction of the US stock market to the Fed’s recent, quite material dovish tilt was also disappointing: US stocks are down since 21 March.

Growth will slow absent reform

The problem of diminishing returns to monetary easing is fundamental. When economies reach full employment, the only way to maintain growth sustainably is to shift from demand stimulus to supply-side reforms, i.e. to raise productivity. While there is no doubt that theoretically developed countries could grow faster, this would require willingness to reform. Sadly, governments are unwilling to reform, while reforms are entirely outside the remit of central banks. The reluctance to reform is partly a reflection of political realities: Donald Trump is a lame duck. Theresa May is a lame duck. Emmanuel Macron is a lame duck. Shinzo Abe never shot his third arrow. Italy is run by populists. The jury is out on Angela Kramp-Karrenbauer in Germany, but early indications do not point to a big shift in German economic policy as Chancellor Angela Merkel hands over the reins of power.

Indeed, it would be more accurate to say that governments in developed countries are leaning more towards populism rather than reform. The US has taken the lead with pro-cyclical fiscal spending and restrictions on immigration and trade. These policies provide short-term political benefits, but they are unambiguously negative for trend growth. US growth has decelerated from 4.2% qoq saar in Q2 2018 to 3.4% in Q3 2018, 2.2% in Q4 2018 and now tracks less than 1% in Q1 2019.

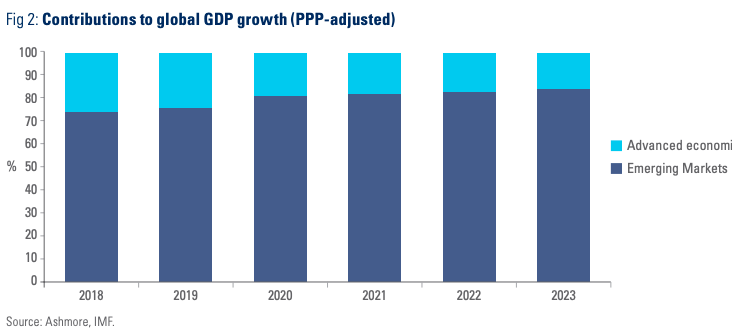

The IMF has recognized the problem and downgraded its growth forecast for developed economies meaningfully. Under IMF’s new projections, developed economies will contribute less to global growth every year for the next five years until, by 2023, they only contribute a mere 16% to global growth, down from 24% in 2018.3

Academic lip service

Slow growth poses a major political problem. Discontented electorates in developed countries have already voted populists into power, but slower growth means that pressure on politicians to do something only gets stronger. Populists are far more likely to double down on fiscal stimulus in this environment than to reform, especially if they can get political cover for a return to Big Fiscal. Enter the economic intelligentsia.

Some academic economists would sell their mothers to be taken seriously in policy circles. Perceiving a growing political bid for Big Fiscal, many economic experts are already presenting arguments in favour of major spending increases. Luminaries, such as Larry Summers, Joseph Stiglitz and Paul Krugman have for some time waxed lyrical about fiscal stimulus, usually with reference to low borrowing costs.

More recently, Big Fiscal has received fresh impetus from the Modern Monetary Theory (MMT) crowd. MMT argues that low inflation is a symptom of inadequate aggregate demand, which the government can address with greater deficit spending. US Representative Alexandria Ocasio-Cortez’s Green New Deal, a modern day version of Roosevelt’s New Deal, is a prominent example of a recent specific policy proposal based on MMT.

Dubious arguments

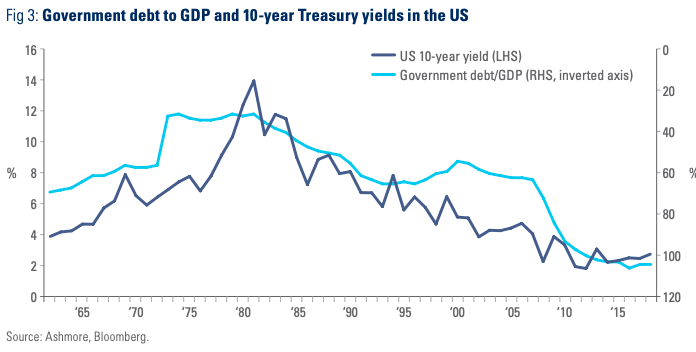

Unfortunately, the arguments in favour of more debt-financed government spending in developed countries are dubious. First, take the argument that low interest rates somehow justify greater indebtedness. The US and other developed countries have only been able to borrow so heavily at low yields, because of enormous central bank bond buying programmes and regulatory forbearance, while credit worthiness has worsened due to a lack of reform and worsening debt dynamics. This can be seen in Figure 3. The US government has already massively increased its borrowing as rates have declined. This means that bonds have become more risky and that investors are compensated less for the risk. In a recent report, the IMF stated that “the US public debt-to-GDP ratio is on an unsustainable path”.4

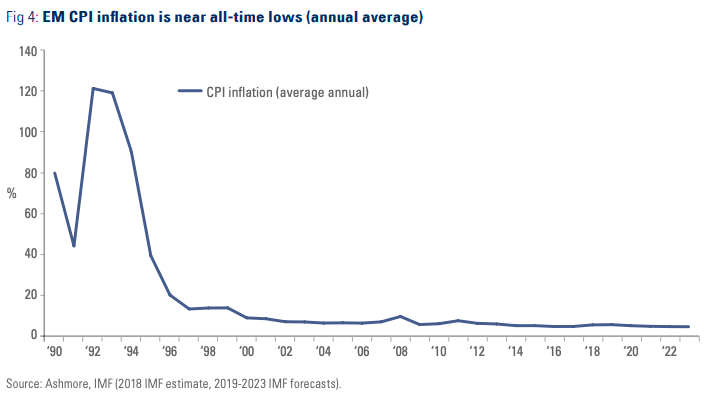

Second, the MMT argument that low inflation is somehow indicative of inadequate government spending is even more problematic. For one, such arguments are not universally applicable. For example, the typical EM country is currently running inflation below 3% (Figure 4).5 On this basis, EM governments should be able to jack up government spending significantly. Yet, as every EM investor knows, if an EM country actually tried to do so, it would immediately find itself engulfed in a financial crisis! Beware of economic theories, which lack universal applicability, because they are likely to be weak. It is far more likely that low inflation in developed markets is due to excessive government spending in the past than inadequate current spending. High levels of debt reflect heavy spending in the past, which depresses the propensities to invest and consume today (because high debt implies higher future defaults, tax hikes, inflation and/or currency debasement).

Sacrificing long-term economic performance on the altar of short term political performance

Despite the dubious quality of the arguments in favour of higher public spending in developed countries, it is very likely that politicians will begin to sing along with the siren songs of the pro-debt lobby. Fiscal policy is simply the only thing left if monetary policy is becoming ineffective and if reforms are too difficult. In fact, Big Fiscal has already begun. The US Congress approved tax cuts to the tune of 7% of GDP in December 2017, when the US economy was just approaching the point of full employment. In Europe, governments are also spending more. This year, for example, national governments in Europe will engage in the largest fiscal boost in ten years, while EU-level fiscal deficits may also increase further in the coming years.6 Of course, if growth slows in line with IMF projections fiscal deficits will also increase due to the operations of automatic stabilizers.

In the following, we outline the three most likely consequences of greater deficit spending in the three main developed market regions of US, UK and the Eurozone. Unless specified otherwise, ‘US-UK-Eurozone’ refers to the average across the three regional entities.

1. Even more indebtedness

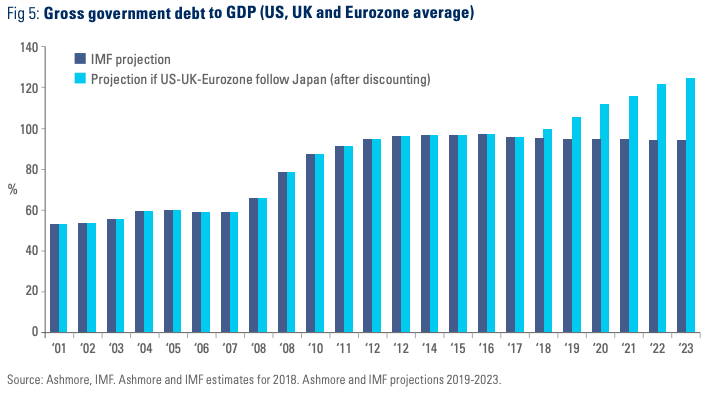

The starting point for re-engaging in Big Fiscal is not great, because governments in developed economies have already become heavily indebted over the last decade or so on the back of fiscal stimulus in the aftermath of 2008/2009. The gross government debt-to-GDP ratio in US-UKEurozone ended 2018 at 93%, up from 57% in 2007.7 What about debt trajectories going forward?

Japan’s experience with public indebtedness in the decades after its 1989 crisis provides a useful guide to how debt in US-UK-Eurozone may evolve during the phase, which US-UK-Eurozone is now entering. Japan’s government debt-to-GDP increased by 58% of GDP to 131% of GDP in the first decade after 1989 and then went up by a further 70% of GDP to 201% in the second decade after crisis. In other words, the experience in Japan was the debt went up even more in the second decade after crisis than in the first.

However, Japan’s experience cannot be translated directly to the US-UK-Eurozone, because the private sector in Japan saves far more than the private sector in the US-UK-Eurozone, which means that Japan can tap into a larger reservoir of domestic funding. To adjust for the difference in local financing, we have adjusted our estimate for the likely trajectory of the US-UK-Eurozone debt burden by the difference in the pace of indebtedness between Japan and US-UK-Eurozone in the first decade after crisis, which is 38%. In other words, we assume that US-UK-Eurozone debts rise by 38% less than in Japan.

Figure 5 shows the resulting debt trajectory for the US-UK-Eurozone rising to 121% of GDP by 2023. This stands in very sharp contrast to IMF’s current projection of an outright decline in the US-UK-Eurozone debt to 92% debt-to-GDP by 2023. Clearly, the enormous difference in trajectories implies a large potential surprise for investors to the extent they place their faith in IMF’s debt trajectories.

2. Even slower growth

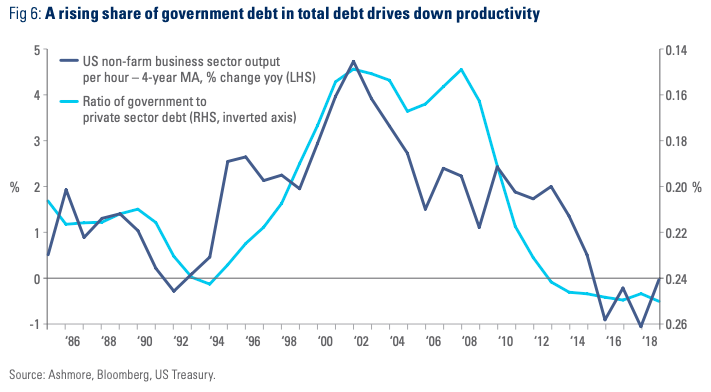

Fiscal deficits can temporarily boost growth, but excess public debt will undermine trend growth by undermining productivity. Trend growth is already impeded by high levels of debt, so piling yet more debt on top of old debt only worsens things. Figure 6 illustrates this point by charting the relationship between the ratio of government to private debt on the inverted right axis and productivity growth on the left for the United States since 1984. The relationship is unmistakable: Productivity growth tends to decline as the ratio of government to private debt rises. This relationship exists, because more government debt starves the private sector of money (‘crowding out’) and because government spending is simply less productive than private investment. If, as we expect, government debt burdens rise in the coming years it follows that productivity growth – and hence trend growth – will also decline further.

3. Higher prices

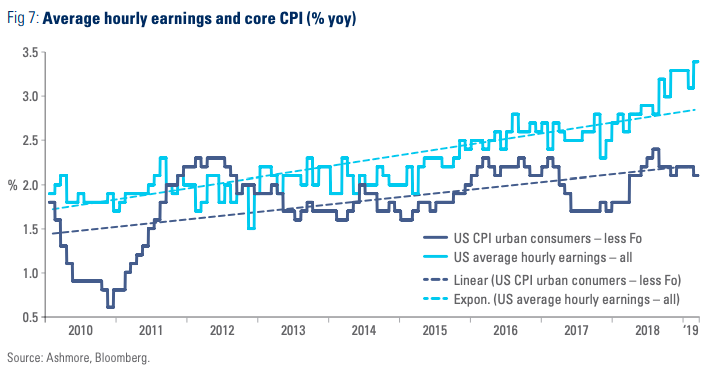

Slower trend growth does not mean that inflation cannot rise. Inflation depends on imbalances between current demand and supply, regardless of what happens with trend growth, although, of course, if trend growth slows then inflation sets in at smaller increments to demand than at higher trend growth rates. Worryingly, inflation is already rising. Figure 7 shows that US wages have been rising steadily for several years despite stagnant productivity growth. Wages are going up because the US economy is at full employment and Trump’s tariffs have reduced the scope for American businesses to outsource production to other countries, where labour is cheaper. A return to Big Fiscal will boost aggregate demand, but reduce productivity, so, barring recession, Big Fiscal will increase inflation risks

The horns of a dilemma

If inflation becomes a serious problem, the Fed will be impaled on the horns of a dilemma: whether to fight for price stability by raising rates or protect growth by keeping rates low? This trade-off is necessitated by the low growth environment. The Fed’s recent actions, particularly the massive U-turn since April last year, suggest that the Fed is extremely sensitive to slower growth (and weaker stock markets). So far, the Fed appears quite relaxed about the rise in wage inflation. If this reflects the Fed’s true preference then the Dollar becomes vulnerable in an environment of slower growth and rising inflation. The Dollar rallied precipitously in recent years on expectations of stronger US growth and higher rates than in other countries, so slower growth and lower rates means that much of this money would be in the wrong place. If the Dollar falls, the US government will find it more difficult to finance the deficit, precisely at a time when deficits are going up under a Big Fiscal push. The Dollar lost 50% of its value against the Deutsch Mark and 46% of its value against the Japenese Yen in the 1970s. This experienced showed that even US government bonds are not truly safe investments in P&L terms when the Dollar falls.8

Where does EM fit into this picture?

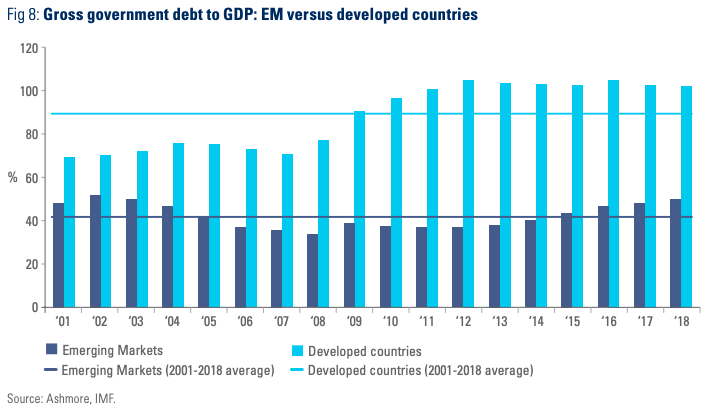

EM governments are far less inclined to run counter-cyclical fiscal policies than developed countries. This is why they have approximately half the debt burden of governments in developed economies (Figure 8). The common perception is that EM countries borrow less due to unwillingness on the part of foreign investors to finance counter-cyclical spending in EM. However, this argument lacks credibility at a time, when EM countries source about 90% of their financing at home. The real reason why EM governments borrow less is political. EM government want to minimise the risk of macroeconomic shocks, which can be politically (and sometimes literally) lethal, because the vast majority of voters cannot ameliorate the effects of shocks due to lack of unemployment benefit, inflation hedges or social security. The best way for EM governments to ensure stability and sustained growth is therefore to pursue prudent fiscal policies and to undertake reforms.

What will happen to EM if developed economies embark upon Big Fiscal? Initially, EM markets may underperform in response to a burst in fiscal spending as investors get bullish about the short term growth outlook and return prospects in developed economies.9 However, pullbacks tend to be temporary and should be exploited ruthlessly to build positions at attractive entry levels. Beyond the initial knee-jerk reaction, we would expect EM bonds to perform well, especially local markets. As growth slows in developed economies relative to EM, EM FX performance tends to pick up.

Conclusion

Drug addicts move on to harder drugs when their favourite drugs stop working. The same is true for dysfunctional governments, which are unable or unwilling to put in the hard work required to keep their economies fit.

As governments in developed countries revert to fiscal stimulus, having run out of room for monetary easing, without paying attention to supply-side reforms, debts will rise, growth will slow and inflationary pressures will mount. The case for investing diminishes. As all EM investors know, the golden rule is to go underweight when governments go overweight. Developed market investors may soon have to familiarise themselves with this rule too.

1 Bank recapitalization was a crucial difference between US and Europe. Europe’s continuing failure to fix its banks lies at the heart of the region’s weaker economic performance relative to that of the US.

2 Long-term price to earnings ratio using the company’s last share price and 10-year average real earnings per share. 10-year average real earnings per share is computed using 40 quarters, or 20 semi-annual periods or 10 annual figures.

3 See ‘EM versus DM growth (2019-2023): How global is ‘global’ growth really?’, The Emerging View, 26 February 2019.

4 See IMF 2018 Article IV report, page 41: https://www.imf.org/en/Publications/CR/Issues/2018/07/03/United-States-2018-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-46048

5 Based on the JP Morgan GBI EM GD.

6 Morgan Stanley, “The Fiscal Boost In Now”, March 19, 2019.

7 From here onwards, US-UK-Eurozone refers to the average for these three regions.

8 The experience of the 1970s showed that a sustained period of high inflation and low rates is detrimental to the Dollar, which declined about 50% over ten years. When the Dollar falls, the purchasing power of any pool of capital denominated in Dollars declines with respect to a basket of imported goods. The loss of purchasing power is not immediately obvious due to the absence of an instant P&L impact. However, when clients sell their assets in order to consume they will discover the loss of purchasing power.

9 As we have noted elsewhere, periods of extra-ordinary US government policy support, such as the Quantitative Easing (QE) period (2010-2015) and the recent fiscal splurge (2018) are associated with clear underperformance in EM local bond markets relative to US stocks. The underperformance is also evident in sovereign bonds and EM corporate high yield bonds, only less so – see ‘US late cycle dynamics and EM bonds’, The Emerging View, 8 November 2018.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2019.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.