Global growth is decelerating. Policy-makers in developed economies are gearing up for yet more fiscal spending. While fiscal spending may support growth for a short time, and for longer if very carefully applied, it will not change the growth outlook fundamentally. This is because the main reason for slower growth lies elsewhere, namely in gross misallocation of capital on a global scale.

A decade of hyper-easy monetary policies has pushed so much capital into developed markets that the marginal ‘growth effectiveness’ of another Dollar in these markets is at or even below zero. Meanwhile, too little capital is available in Emerging Markets (EM), which have room to absorb inflows and much greater growth potential due to binding financial constraints. The opportunity cost of shifting capital from developed markets to EM would be small due to the low marginal growth effectiveness of capital in the former.

The simplest way to encourage a re-allocation of capital and therefore faster global growth is to weaken the Dollar. Dollar weakness will eventually happen by itself, or, alternatively, the US government may choose to weaken the Dollar unilaterally as a matter of policy. Intriguingly, it is also entirely within the power of EM governments to weaken the Dollar if they wish to claw back their fair share of global capital. All it takes is a bit of coordination on the part of their central banks.

Global growth is slowing

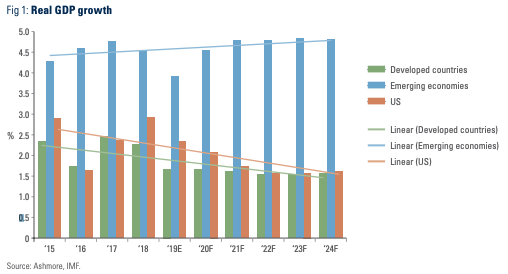

Global growth has slowed for the last three years. The world economy expanded at a rate of 3.8% in real terms in 2017, then 3.6% in 2018 and 2019 is only expected to deliver about 3.0% growth, according to the IMF. The slowdown in economic activity is particularly acute in developed countries, where growth has slowed from 2.5% in 2017 to just 1.7% this year, but EM growth has also decelerated, albeit by a smaller amount in percentage terms from 4.8% in 2017 to 3.9% this year.

Looking forward, developed economies are expected to continue to slow to just 1.6% per annum by 2024, while EM growth is expected to re-accelerate to about 4.8% by 2024 (Figure 1). Lifted by the recovery in EM growth, global growth will recover a bit in the next few years, but only to about 3.6% by 2024. This is a far cry from the pre-crisis years, when the global economy expanded at a rate of more than 5% per year. Even EM growth rates are expected to be well below the growth rates recorded prior to the 2008/2009 financial crisis.1

Inefficient allocation of global capital

In our opinion, the most important, yet least recognised, reason why global growth is slowing is that capital is no longer allocated to where it gives the biggest bang for each buck. Global capital has become grossly misallocated as a result of powerful incentives designed by Western central banks to encourage investors to deploy more capital in financial markets in developed countries in the aftermath of the 2008/2009 financial crisis. In the worst economic crisis since the Great Depression, capital was required urgently to prevent developed countries from falling into depression.

The main instrument employed by central banks to encourage capital to flow into financial markets in developed economies was interest rate subsidies, also known as Quantitative Easing (QE). It was hoped that trillions of Dollars of interest rate subsidies would buy time for governments to reform and deleverage, and give companies confidence to once again invest in the real economy.

While interest rate subsidies were the right policy for the time and the circumstances, the law of unintended consequences soon intervened. Loving the easy monetary conditions provided by central banks, governments felt no inclination to reform and instead engaged in significant fiscal stimulus, which took, say, the US government debt to GDP ratio to more than 105% from 60% prior to the crisis. The private sector never got comfortable enough to invest in the real economy either, opting instead to take advantage of record low interest rates and corporate tax cuts to borrow copiously to buy back shares.

The result was that financial asset prices surged, but productivity growth failed spectacularly to recover and debt burdens gradually began to mount again. Investors, largely oblivious to fundamentals, only had eyes to the enormous capital gains generated in developed markets, including 425% return in US stocks and 150% return in long German bonds. The Dollar surged ahead of all other currencies for the simple reason that US stocks produced higher returns than other markets and investors bought Dollars to participate.

Meanwhile, in the rest of the world, that is the world whose bonds were not bought by central banks, including EM, bonds only offered yield, which was not enough to compete with the unprecedented capital gains in developed markets. Investors reduced exposure to EM in order to chase returns in developed economies and EM became collateral damage. As outflows from EM mounted, performance suffered, but so did growth because EM economies were severely finance-constrained to begin with and outflows only tightened the finance constraints further.

No longer fit for purpose

The big four QE trades – buying US stocks, Dollars, European bonds and selling everything in EM – have now been taken to such extremes that they threaten further global growth stagnation, in our opinion. The trades, which were designed as a response to an emergency, are no longer fit for purpose. Far too much money is now sitting in financial markets in developed economies, where its marginal ‘growth effectiveness’ has declined to or even below zero, while far too little money is available to the rest of the world – Emerging Markets (EM) – where the marginal growth impact of a Dollar is far higher.

It is difficult to see how another Dollar invested in US stocks will materially increase US growth. Similarly, it is difficult to see how investing another euro in Germany’s already negative-yielding long bonds will do anything to increase German or European growth. Indeed, one might argue with some justification that investing more money into these markets could pose a risk to future growth. US stock markets and European bond markets are already trading near or at bubble levels relative to rather unspectacular economic fundamentals, so these markets could crash with potentially serious negative ramifications for the underlying economy.

A relatively simple solution

The good news is that misallocation problems are relatively easy to solve, conceptually at least. Global growth rates can be raised simply by allocating more capital towards destinations where capital has a greater marginal growth effectiveness and away from destinations where growth effectiveness is low. In practice, this requires the original QE trades to be put into reverse now that they have served their purpose. By shifting funds away from overbought markets in developed economies back towards EM, i.e. more into line with global asset allocation patterns that prevail in normal economic circumstances, the marginal growth effectiveness of a Dollar of investment can be increased significantly.

Greater allocations to EM enhance growth for two reasons. First, EM economies have room to absorb a lot of capital due to market valuations and fundamentals. EM currencies are 50% lower than in 2011, inflation is below 3% and current account balances have improved by an average of nearly 4% of GDP, based on the thirty most traded EM economies. Sovereign bond spreads are twice as wide as they were in 2006 and in local markets real bond yields have not come down at all in ten years. EM equities are also spectacularly cheap relative to US equities and availability of additional capital would enable companies in EM to ramp up investments significantly.

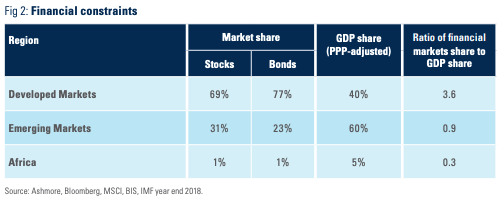

The second reason why the marginal growth effectiveness of allocating to EM is higher than in developed economies is because EM economies are severely capital constrained. Inflows to EM therefore directly enhance growth. The extent of finance constraints in EM can easily be illustrated by comparing shares of global capital to shares of GDP in EM and developed economies. In EM, this ratio is only 0.9 compared to a whopping 3.6 in developed economies. In the poorest regions in EM, such as Africa, the ratio is shockingly low at just 0.3. In other words, the very countries with the largest growth potential in the world have the least amount of financing, while the countries with the lowest growth potential are drowning in money (Figure 2).

Meanwhile, the opportunity cost of allocating funds away from developed economies is low, because the marginal growth effectiveness of a unit of capital in these markets is already so low. That is not to say that the US economy would not fall into recession if such a re-allocation were to occur, but outflows would not be the cause. Rather, a US recession would be the consequence of either ongoing policy mistakes, such as the trade war, or the cumulative effect of so many years of real effective exchange overvaluation. Indeed, seen in this light, outflows from the US could actually help the US economy by lowering the Dollar, which in turn would support beleaguered US exporters to regain some competitiveness. It is important that this happens because exports will have to play a much bigger role in future US growth, while the country deals with declining productivity and rising debts.

Barking up the wrong fiscal tree

Sadly, despite the obvious economic merits of allocating global capital more efficiently, there is not as of yet, as far as we are aware, any clear thinking about this issue in policy circles. Instead, our wise leaders are calling for yet more fiscal stimulus. Last month, Christine Lagarde, newly appointed President of the European Central Bank, urged European governments to increase fiscal spending. Loose fiscal policy is already a central pillar of US macroeconomic policy, while the UK looks likely to become seriously profligate on the fiscal front to offset the negative effects of Brexit over the coming years. Japan is also considering more fiscal stimulus.

Yet, fiscal stimulus may not solve the global growth problem and could, in fact, make it worse. For one, the types of fiscal stimulus favoured by developed governments at the moment – consumption subsidies and corporate tax cuts – have not had lasting effects on growth, while the types of spending that are known to boost trend growth, such as infrastructure investment have been neglected.

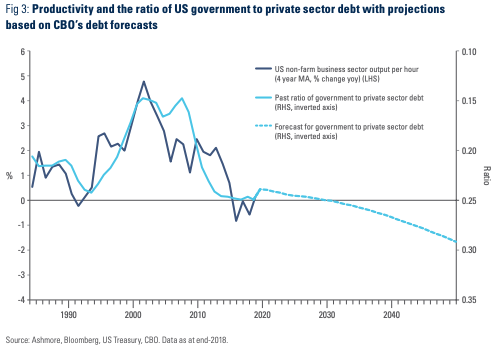

The problem of inefficient government spending is further compounded by an already dangerous imbalance between fiscal spending and productivity-enhancing reforms. Consider Figure 3, which shows a simple ratio of government debt to private sector debt in the US. This ratio is negatively correlated with US productivity growth because government spending in its present form is vastly less productive than private sector spending. Therefore, the more the government spends the lower the productivity of the economy as a whole.

In theory, fiscal stimulus can of course contribute to trend growth, but only if every penny is allocated hyper-efficiently to ensure that it generates more growth than its deterrent effect on productivity growth. This is simply not the case at the moment. The Congressional Budget Office’s projections for US government debt points to a continuing erosion of US productivity growth as shown in Figure 3.

Inching ever closer to currency manipulation

Barring miraculous policy shifts that rectify the imbalance between fiscal policy and reform and raise the productivity of government investment, it is therefore likely that additional fiscal stimulus will only depress trend growth further. This would be unfortunate because the effectiveness of monetary policy is also diminishing. The ECB ran out of conventional and most unconventional policy tools this summer and a mere 175bps of rate cuts in the US would put the Fed into a similar quandary.

Prudent investors must therefore expect policy-makers soon to resort to entirely new policy instruments to try to shore up growth. The obvious place to focus is global asset allocation, but since this option is not even on the radar screen of most policy-makers, the likely direction of travel is towards currency manipulation and possibly even helicopter money. Both these policy tools would have significant effects on exchange rates.

For example, the US government could decide to unilaterally weaken the Dollar as a matter of policy, especially in the context of a recession. President Donald Trump has frequently called for a lower Dollar. The US Treasury can weaken the Dollar using a facility specially designed for that purpose, while the Fed can intervene in unlimited size. All it takes is a word from Trump himself.

The Dollar may also simply start to weaken by itself. So much bull-market money from foreigners is sitting in US stock markets that a simple downturn in US growth would trigger significant repatriation of capital. An orderly policy-driven adjustment would clearly be preferable, given the heavy positioning in US assets by foreign investors, including EM central banks. An uncontrolled disorderly adjustment would likely be more destabilising and costlier in terms of growth.

A lower Dollar boosts EM growth

Ironically, if policy makers move towards greater reliance on exchange rate policies as they run out of other means of stimulating growth they will inadvertently take a huge step towards re-balancing global capital with broad market participation. This is because currencies are hugely effective ways to shift large volumes of global capital. In EM, for example, many investors do not even consider allocations to EM local markets – bonds or stocks – unless they have a neutral to bearish view on the Dollar.

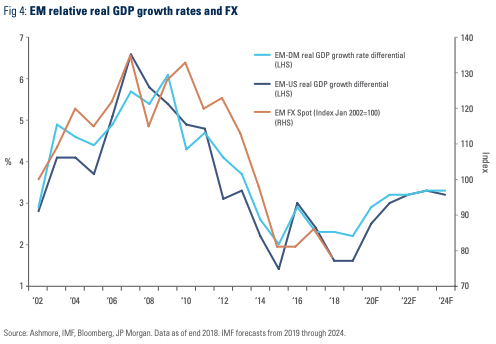

Once they get bullish on EM currencies, however, the case for allocating even more to EM quickly mounts. This is because stronger EM currencies are closely associated with higher EM relative growth rates (Figure 4). In other words, the more capital gets allocated the stronger the fundamentals. This odd relationship is a direct consequence of EM’s financial constraints. We estimate that EM growth rates could rise by a least a fifth simply from the additional domestic demand that results from the volume of inflows required to return EM currencies to fair value, i.e. a 20% recovery after the 50% decline against the Dollar since 2011.

EM power

Intriguingly, it is entirely within the power of EM governments to secure a larger share of the global financial pie, thereby improving their own and global growth prospects. This power stems from the fact that EM central banks jointly control three quarters of all the FX reserves in the world of which the vast majority is denominated in Dollars. An agreement by EM’s major central banks to sell, say, 20% of their Dollar holdings over a period of a few years and replace them with bonds from each other’s domestic bond markets would achieve the objective. Private capital would soon follow. There would be obvious benefits beyond diversification away from the Dollar, especially a massive increase in liquidity in EM’s own domestic bond markets.

EM local markets are large enough to support such a program. The EM local currency government bond market today measures about USD 11trn and grows by approximately 10% each year. If EM central banks were to replace 20% of their current Dollar holdings of about USD 6.5trn with EM bonds they in effect have to buy approximately 12% of outstanding EM local currency government bonds. Phased in over, say, five years, however, the demand from central banks could be accommodated entirely through net new supply arising from the natural growth of markets.

Conclusion

“Everything he knows is wrong!” exclaimed Brock Lovett, a minor character in James Cameron’s blockbuster movie ‘Titanic’, when he described Captain Edward Smith’s misguided belief that he could spot icebergs in advance and turn the ship in time to avoid collisions. In our opinion, Lovett may as well have been talking about policy-makers in developed economies today as they pin their hopes for a recovery in growth on yet another round of fiscal stimulus.

While fiscal stimulus can assist growth under a narrow set of circumstances, if global growth is to stage a proper comeback it is crucial to get the diagnosis right. The primary impediment to global growth today is not inadequate fiscal spending. Rather, it is the gross misallocation of risk-willing capital. Too much money has been chasing financial investments with zero to negative growth effect in rich countries, while obvious lucrative and seriously growth-enhancing investment opportunities in EM lie fallow.

The policies that led to this skewed allocation of global capital were justified in the immediate aftermath of 2008/2009 by the need to avoid depression, but today this allocation of global capital is deeply inefficient and stunts growth.

Policy-makers should evaluate the effectiveness of asset allocation not from the narrow perspective of past financial performance, which was mostly delinked from underlying economic performance during the QE era. Instead, the focus needs to shift to the growth effectiveness of financial allocations. Here, the best option is not to put yet more money into developed economies. Putting money into EM unlocks far more growth due to the general state of underfinancing and the existence of binding finance constraints.

It would be ideal if policy-makers realised the potential to stimulate global growth by tilting incentives such that every marginal unit of capital goes to where it has the absolute largest growth effect. If they fail in this task, however, markets will almost certainly do the job for them. That is why investors might as well get ahead of the curve by allocating more money to EM right away.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2019.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.