Want to read more by Ashmore Group? Visit their Featured Firm page here

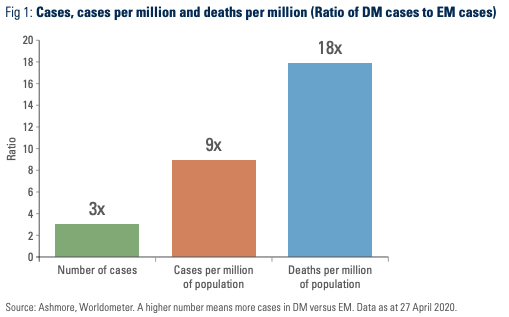

As of 27 April 2020, eighteen times more people have died from coronavirus per million of population in developed countries (DMs) than in Emerging Markets (EM). This is partly due to measurement problems, but there may also be genuine structural reasons for expecting slower spread, less overall incidence, and lower mortality rates in EM countries than in DMs.

Meanwhile, the economic impact of lockdowns should prove transitory and the latest estimates from the International Monetary Fund (IMF) give some grounds for optimism about EM growth relative to growth in DMs. EM’s growth advantage becomes even stronger in the years after coronavirus. Yet, bond market valuations do not reflect this at all, which means that serious money can be made in EM bonds, particularly compared to bonds in DMs.

Many EM countries are now able to meet all their financing requirements at home – and the coronavirus crisis has enabled them to showcase a raft of policy instruments typically associated only with developed economies. This still leaves a vulnerable fringe of countries, which tend to get cut off from overseas financing during bouts of risk aversion. No one should call for blanket debt moratoria in these countries many of which have worked very hard to gain a toehold in global capital markets, which they rightly see as vital to their economic futures. Instead, international financial institutions (IFIs) should begin to address the obvious markets failures, which clearly jeopardise the economic futures of millions at every bout of risk aversion.

Meanwhile, coronavirus is likely to pave the way for recession in the US and therefore a significantly lower Dollar once the panic phase is over. On the other hand, we do not see coronavirus changing the broad direction of travel in China, which views the populism on display in the West as a way to enhance its own reputation en route to global economic and financial hegemony.

Coronavirus

As of Monday 27 April, there were just shy of 3.0 million recorded cases of coronavirus worldwide. There were 3 times as many coronavirus cases in developed markets (DM) than in Emerging Markets (EM) (Figure 1). Within EM, Asia accounted for 6% of cases, Eastern Europe for 8%, Latin America for 5%, the Middle East for 5% and Sub-Saharan Africa for 2% of all recorded cases. It can be misleading to compare absolute numbers of cases across regions due to large differences in population sizes. Controlling for population sizes, there were 8 times more cases in DMs than in EM.

The lower number of cases in EM countries is undoubtedly partly due to lack of testing facilities. One way to reduce this source of error is to look at deaths per million instead of cases per million. After all, health workers are more likely to get involved when someone dies than when they are alive and going about their daily business. Comparing deaths per million, DMs have even more cases per million than EMs: 18 times more. One would expect this ratio to decline as EM countries become better able to test.

However, testing deficiencies notwithstanding, there may also be structural reasons to expect a slower spread, lower overall incidence, and lower mortality rates in EM countries than in DMs. These structural reasons may include:

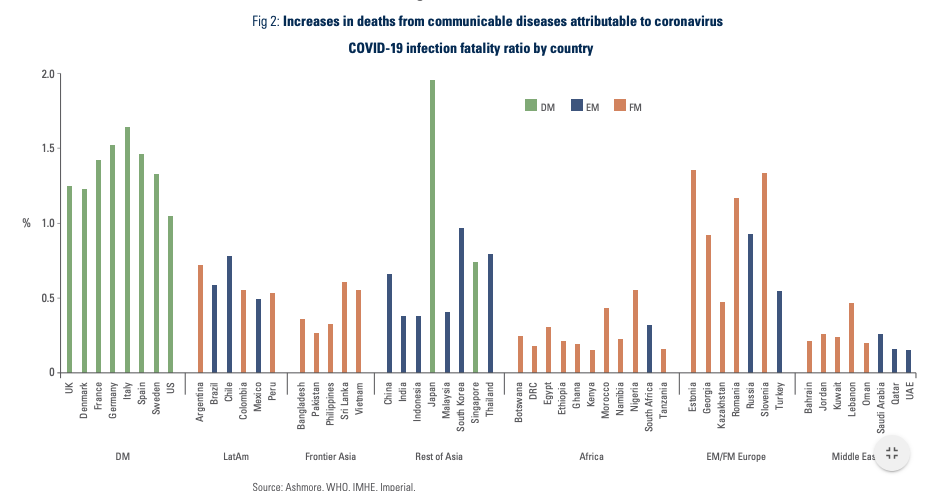

- Younger populations: EM populations are generally far younger than populations in DMs. This means mortality rates should be lower, since young people are less likely to be seriously affected by coronavirus than the elderly, let alone die. This also means that health care costs should be lower in EM countries. Indeed, if one applies the infection fatality ratio (IFR) for coronavirus found in Wuhan to the individual age demographic profiles of individual countries then the disease can be expected to be 50% less severe in the main EM countries and more like 75% less severe in Frontier Economies (Figure 2).

• Climatic differences: Last week, officials from the US government announced that a link may exist between transmission of coronavirus and temperature and humidity.1 While the US government may not be the go-to authority on coronavirus, this observation is nevertheless consistent with evidence in medical journals, which shows that viruses can be sensitive to temperature and transmission can be impeded in humid climates (since large viruses get caught in airborne water molecules, reducing spread). Of course, climate-related barriers to transmission are neutralised by air conditioning, but many people in EM countries cannot afford air conditioning.

• Smaller service sectors: Many service sector jobs involve direct person to person contact in contrast to manufacturing jobs and jobs in the primary industries, such as farming, mining, etc., which tend to be person-to-machine and person-to-earth jobs, respectively. The latter two naturally imply greater social distancing.

• Larger rural populations: Some 67% of Indians live in rural areas compared to just 17% of British people. In general, EM populations tend to be far more rural-based than DM populations. This also ensures far greater natural social distancing and therefore lower transmission rates.

• Ubiquitous BCG vaccinations: Countries with widespread tuberculosis vaccination programmes (BCG vaccine) appear to have fewer cases and the seriousness of cases may be less.2 BCG vaccines are extremely widely dispensed in EM countries, but the US never had a mass vaccination programme. The UK introduced the BCG programme in 1953, which means that people over 67 years of age have generally not been vaccinated. The UK ended the BCG vaccination programme in 2005.

Clearly, the observation of sharply lower case numbers in EM could be consistent with both inadequate case measurement and the structural differences outlined above. It is not possible to draw a firm conclusion as to contribution of each explanation yet, but a balanced view should certainly assign a non-zero probability to the possibility that EM countries continue to see slower spread, lower overall incidence, and lower mortality rates than DMs.

The economic shock from coronavirus in EM

The primary source of economic weakness in EM arising from the coronavirus outbreak is lockdowns, both at home and in DMs. The same political debate over lockdowns versus achieving herd immunity, which rages in DMs, also exists in EM countries, although, like most DMs, the majority of EM countries have opted in favour of lockdowns.

Yet, the case for lockdown is weaker in EM countries, because they are likely to be less effective and hence may prove less economically damaging and more likely to be lifted sooner too and less likely to be repeated. EM countries have large informal sectors in which people are totally out of reach of government services, oversight, enforcement, etc. Besides, many people in EM live hand to mouth and simply cannot survive for very long if they ‘lock down’.

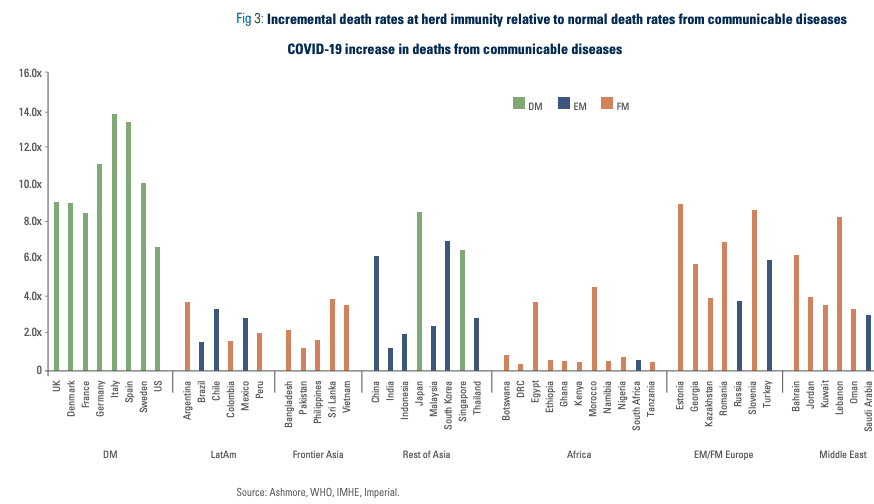

Another tragic consequence of poverty is that the marginal economic impact of coronavirus in many countries may be rather small, because EM populations already struggle with high levels of mortality from other communicable diseases. For example, if one applies Wuhan IFRs to EM and Frontier Economies and assume, for argument’s sake, that herd immunity sets in at 80% penetration rate then the increment in deaths from communicable diseases due to coronavirus specifically compared to a non- coronavirus counter-factual is just 1.0-6.0x in EMs and 0.3-4.0x in Frontier Asia and Africa. In fact, the coronavirus shock is almost undetectable in African countries, given their already high mortality rates due to other causes. By contrast, the incremental death rate is very high in DMs at 8-14x (Figure 3).

The mounting evidence of a lower impact from coronavirus itself on EM countries should, all else even, translate into better relative economic performance than in DMs. Indeed, this is what the latest forecasts for economic growth from the IMF suggest (Figure 4).

In its April 2020 World Economic Outlook, the IMF clearly recognises that coronavirus is likely to be a transitory shock to growth and expects EM countries to perform far better than DMs not just in 2020, but also beyond. Specifically, IMF sees world real GDP contract by 3% in 2020 followed by a 5.8% rebound in 2021. IMF expects DM growth to collapse by 7.8% in 2020 relative to last year, while EM growth drops a more modest 4.8% relative to 2019. Hence, EM real GDP growth should be negative 1.1% in 2020 compared to -6.1% for DMs. In the 2021 rebound, IMF sees EM growth surging to a higher rate of 6.6% than the 4.5% growth rate expected from DMs.

In other words, DMs will contribute the vast majority of the contraction in global growth this year and China will be one of the few countries to positively contribute to global GDP growth in 2020.

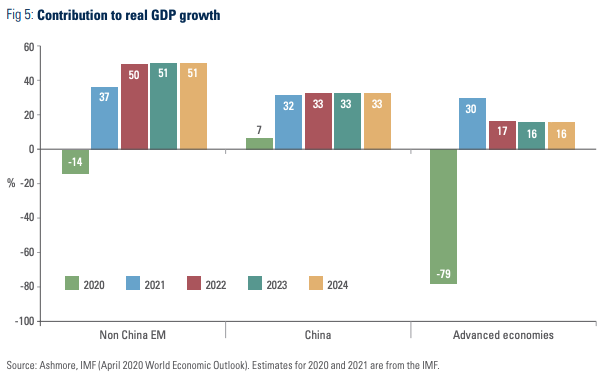

Looking beyond 2020/2021, the world economy is likely to gradually revert to pre-shock growth drivers. This should ensure that EM’s growth contribution increases structurally towards 84% by 2024 with the contribution of DMs to global growth slipping to just 16% (Figure 5). We expect China’s contribution to global growth to stabilise to around one third after the coronavirus shock, which means that non-China EM’s contribution to global growth steadily picks up towards 52% by 2024. Still, the overall rate of growth in the global economy as a whole should remain relatively subdued compared to the pre-2008/09 period, so commodity prices should remain subdued.

Commodities

Lockdowns have pushed down demand for commodities. Oil has been particularly affected due to a concurrent price war between Russia and Saudi Arabia. EM countries are very differently affected by lower commodity prices, including oil. Across EM as a whole, commodity exports make up 5% of GDP and oil exports make up 2% of GDP. However, the majority of EM countries are net commodity importers, so they benefit from lower commodity prices.

As for fuel, the average EM country imports fuel to the tune of 5% of GDP. The smaller group of specialised fuel exporters nevertheless tends to depend rather heavily on this single commodity due to Dutch Disease and other issues typically associated with heavy dependence on oil production and exports.3 As a group, the specialised energy exporters generate about 7% of their GDP from exporting oil. However, even this group of countries is varied. It includes countries like Russia with very strong public finances and excellent macroeconomic management as well as Middle East economies of great wealth and some of which also have good track records of handling shocks. On the other hand, there are dysfunctional economies in this group, such as Venezuela and then a long list of countries with varied track records, including Ecuador, Angola, Nigeria, Ghana, Gabon, Iraq, Kazakhstan, and Azerbaijan. Clearly, the duration of the collapse in oil prices is critical to these countries as their short-term economic fate largely depends on the duration of the weakness in oil prices.

Fortunately, very extreme moves in oil prices in recent weeks are mainly technical in nature and therefore unlikely to be sustained. We expect demand for oil to begin to reduce stocks of oil in storage to facilitate a rebound in prices once lockdowns are lifted.

Financing and policy responses

Upwards of 90 EM countries are reported to have asked the IMF for financial assistance in recent months. This is a large number, but should be placed into context. There are around 165 EMs in the world of which only 74 are represented in benchmark indices. Roughly one third of countries in the index have ongoing programmes with IMF, while almost all the non-index countries have permanent relationships with the IMF, since they need IMF sign-off in order to tap into World Bank and bilateral money. What financing challenges now face EM countries due to coronavirus? To answer this question, it is useful to split EM countries into two broad groups, those with own markets and those without.

1. Established EM countries (with local markets)

This group comprises the established EM countries, such as Brazil, Mexico, Indonesia, Poland, Russia, Turkey, China, Thailand, Hungary, Colombia, etc. These countries have large domestic bond markets, which provide about 90% of their total financing requirements.

There are very interesting and novel things happening in this group as far as financing is concerned. In fact, when the coronavirus shock is behind us many will look back and focus not on the temporary market stresses or the odd default, but on the fact that EM local bond markets came of age. First, there has been surprisingly little stress in EM local markets. Second, EM central banks have been able to roll out an unprecedented range of conventional and unconventional easing measures that one would ordinarily associate with DMs, with the notable difference that EM bonds still offer much higher yield.

EM currencies have moved sharply lower in this crisis, but so have EUR, GBP, AUD, CAD and other non-Dollar currencies. This sell-off in EM FX has not destabilised local bond markets nor triggered a burst in inflation. Besides, EMs jointly sit on 75% of the world’s FX reserves, so they can intervene, should they wish to do so. EM currencies were already cheap prior to the coronavirus sell-off.

The new reliance on local bond markets means that the stock of local debt will go up in line with the roll out of fiscal measures. The rise in local debt stock is preferable to a rise in external debt, because external shocks in countries with large local currency (as opposed to USD) debt tend to be deflationary. This forces central banks to cut policy rates, lowering the cost of the debt as the debt stock increases. The scale of fiscal spending must always be monitored closely, but so far EM countries have not splurged nearly as much as DMs. EM countries are also setting out with much lower debt levels, roughly half in fact. Since the debt is mainly local if debt stocks get too large the main effect will be to slow growth just as happens in DMs and then central banks can cut rates. A few established EM countries have cleverly exploited the low oil price environment to cut fuel subsidies, which help to reduce the fiscal burden.

2. The rest of EM

The other group of EM countries either have no local bond markets or their local markets are not large enough to meet all their financing needs in full. This group includes some of the least developed and poorest countries in the world. They tend to get cut off from global capital markets during major bouts of risk aversion and without local markets they can be plunged into serious difficulty. To avoid disaster, they turn to IFIs, like IMF, but this is no free ride. IMF money is typically subject to conditionality, that is, interference in domestic affairs. Due to the associated stigma, IMF support can be costly in terms of political capital and therefore undermine a government’s ability to meet the conditions for IMF credit, thereby setting in motion a negative dynamic of growing economic, political and financial weakness.

Be that as it may for EM countries with poor macroeconomic management. Unfortunately these destructive dynamics happen even in countries with good economic performance, because all it takes to trigger them is for international investors to get cold feet about allocating to EM. And this happens at every bout of risk aversion. This is a massive market failure. In fact, such behaviour would never be tolerated in domestic markets, where governments would step in to prevent unnecessary and unjustified economic harm.

IFIs do not intervene, however. They do not have the tools. They should design new programmes – call them global macro-prudential polices – to address gratuitous market failures, such as the tendency for whole classes of countries to be cut off from access to finance in a wholesale and indiscriminate manner at every bout of risk aversion. Such programs could involve credit lines to enable EM countries to buy back their own debt during periods of extreme market mispricing, or bond purchases undertaken by the IFIs themselves.4

It is also imperative that IFIs refrain from their current practice of immediately calling for debt moratoria for EM countries at every sign of market stress, which is deeply counter-productive. EM countries have often fought very hard to gain a toehold in global markets, which is a giant step forward in any country’s economic development. To then be cut off from markets at the first sign of stress is a huge setback. Maintaining access to global markets is not the problem, rather it is part of the solution, assuming, of course, that policies are good and debt is sustainable, which is the case in the vast majority of cases.

Price action

EM markets have reacted as one would expect in the middle of a major risk aversion episode. In next to no time, investors have dumbed down the world to the conventional binary distinction between ‘risky EM’ and ‘safe DM’, leading to significant mispricing of many EM assets. EM sovereign debt spreads topped out at 725bps on 23 March and have since tightened to 630bps, but this is still extremely dislocated (Figures 6).5 The spread on EM investment grade bonds is 336bps, which is the widest since 2009.

We estimate that the fair spread for external debt should be around 300bps over Treasuries. External debt traded at spreads of 180bps and 220bps over Treasuries in 2007 and 2010, respectively, when there were only half the number of countries in the index and the index names had lower average credit ratings than today.

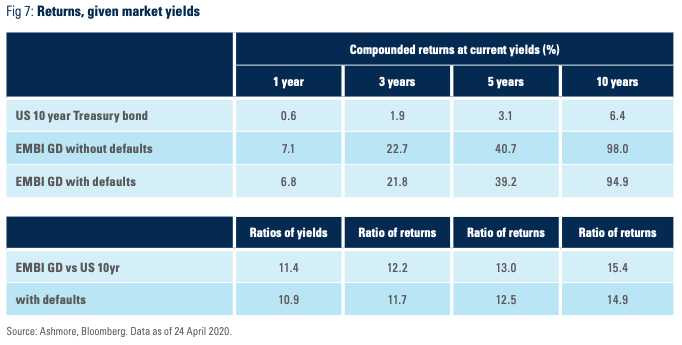

Another way to illustrate what current spreads imply for return, external debt currently pays 12 times more than an equivalent-duration US government bond (Figure 7). Even factoring in the long-term default rates in external debt, the asset class still pays 11 times more than US bonds. If yields remain at these levels for five years, compounding of yield alone ensures that investors in external debt are paid 13 times more in USD terms than if they own equivalent duration US government bond. This means 40% return versus 3% for the US 10 year government bond. On the other hand, if risk sentiment gradually normalises from current panic-stricken levels – which seems overwhelmingly likely – then capital gains will be realised, which points to a return closer to 70% over 5 years, or about 65% factoring in defaults. Presumably, US Treasury yields would then rise a bit, which implies ever lower returns for US bonds.

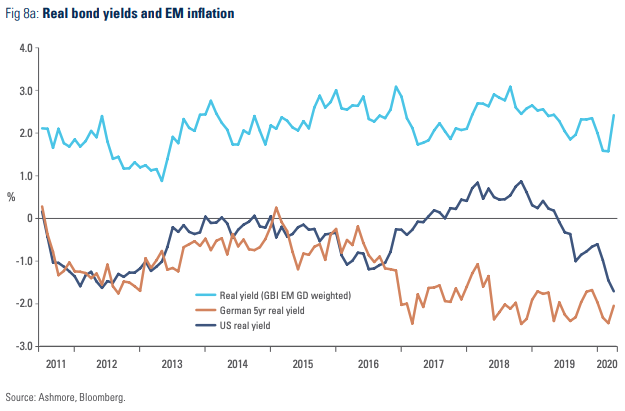

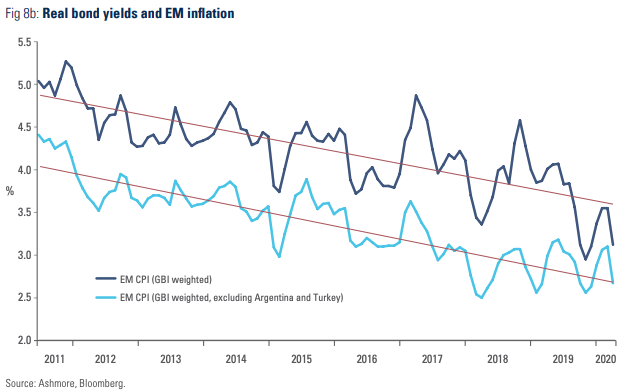

Turning to local currency bonds, the yield is 5.0%, which is remarkably low given the scale of the global dislocation. The lack of stress in local markets reflects partly the growing set of tools available to central bankers in EM, but also the fact that positioning is light in the asset class after ten years of a strong Dollar. Yields, though unusually stable compared to past shocks, are attractive in real terms given near record low EM inflation of just 3.1%. In other words, bonds pay about 200bps positive real yield for 5-year investment grade sovereign credit with a differential to US 5-year bonds of close to 400bps (Figures 8a and 8b).

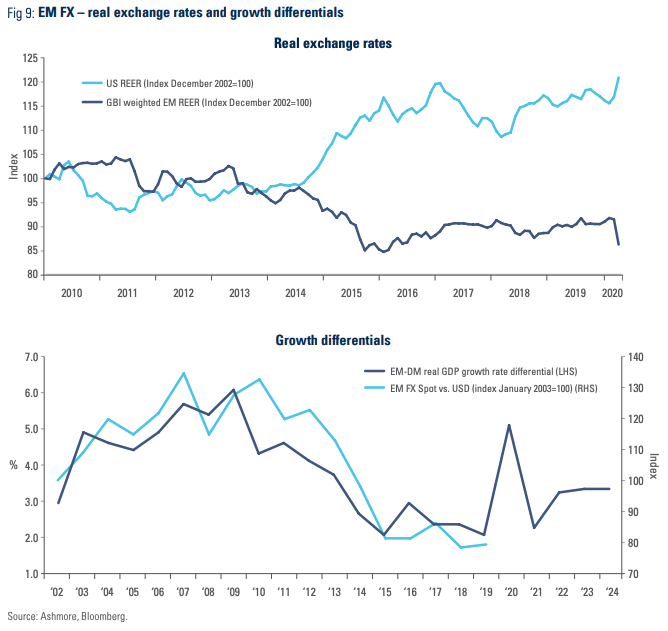

Meanwhile, EM currencies have dropped sharply as one would expect due to flight to Dollars in risk aversion, but EM currencies were already 20% cheaper to the Dollar prior to the coronavirus shock, based on real exchange rates and growth differentials (Figure 9). Now is simply a better entry point, especially if, as we expect, the Dollar slumps in a post-coronavirus recession environment. Yield and FX combined, if EM local bonds do not rally at all and EM currencies merely make up their fundamental cheapness to the Dollar then EM local bonds should deliver about 48% return in Dollar over the next five years.

US outlook

US markets are special to EM investors, because many EM bonds trade as a spread over the US Treasury curve and most EM currencies trade against the Dollar. Besides, the Dollar is the main global reserve currency that investors buy when they get scared. Europe may be a larger economy than the US, but EUR does not have the same clout. One important reason is that Europe does not have a large centralised government bond market due to Europe’s inability to establish fiscal union.

The outbreak of recession in the US has scared many investors and ironically made them buy Dollars and US Treasuries. These are classic panic trades, but they do not form a sound basis for strong long-term returns, particularly since the Dollar tends to fall in US recessions (for the obvious reasons that the investment environment is not particularly attractive, with earnings declining, defaults increasing, and the economy slowing). This is also likely to happen in the recession getting underway now, only possibly more so, since the Federal Reserve has already used up most of its policy tools fighting coronavirus, which leaves little ammunition for tackling the recession itself.

Besides, US government debt levels are already very high, which puts a serious dampener on productivity growth.6 Add to that a not so great technical position after some USD 10trn (half of US GDP) of foreign money poured into US bull market trades, such as stocks, high yield credit, and leveraged loans over the past decade. In a recessionary environment, much of this money will be in the wrong place. Normally, investors can hide in the Treasury market at the onset of recession, when yields are typically as high as 5-6%, but today 10-year yields sit around 0.6%, so there is not enough capital gain potential in Treasuries to offset losses in stocks and other bull market trades. Foreigners, unable to hedge onshore, will likely aim to hedge offshore, meaning they sell Dollars. This means that the Dollar may right about now be in the middle of a classic whiplash, which sees it move higher with risk aversion only to come down with the subsequent recession.

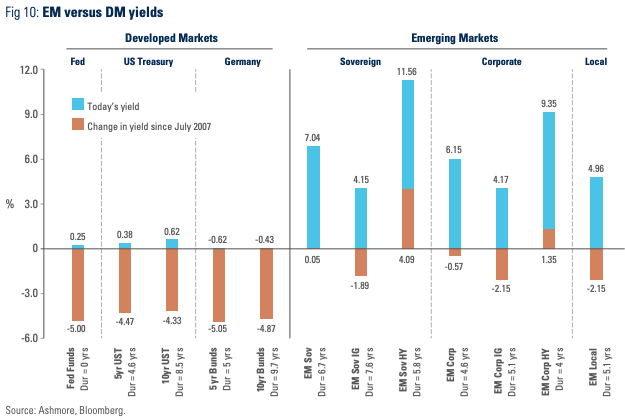

A lower Dollar would open the door to the entire non-Dollar universe of investment opportunities for the first time since 2010. Some 70% of the world’s investments opportunities reside in this universe, but many do not offer much in the way of yield, such as Japanese or German bond. However, EM bonds stand out with their much higher yields (Figure 10). So they should attract flows.

An approaching lower Dollar environment would also be critically important for EM fundamentals. Inflows strengthen EM economies, which are severely finance constrained. If you add up all the bonds and stocks in EM and divide them by EM GDP on a purchasing power parity basis you get a ratio of just 0.9, meaning that EM countries have less finance than output. By contrast, in DMs this ratio of 3.6 (which is why US stocks are expensive and German bond yields are low). When flows come back into the local currency asset class then financial conditions ease, which means that banks can suddenly make consumer and business loans again. This pushes up domestic demand, which should result in higher EM growth than that which the IMF is expecting, starting as soon as the current bout of risk aversion and the inevitable associated flow disruptions begin to dissipate in earnest.

China

There is currently a vicious blame game underway with China in the cross hairs. Some Western government are accusing China of being less than 100% forthcoming about its coronavirus outbreak. If so, it would of course not be the first time that countries tried to manage bad news. In our view, the attacks on China are almost 100% politically motivated. Enormous policy failures in the handling of coronavirus have taken place in the US and UK and politicians are searching for scape goats; as usual they pick on China.

It would be a serious mistake for investors to jump on the anti-China band wagon. China is going to win. Due to its very high savings rate and four times more people than the US, it is very likely that China will be between 2 and 3 times larger than the US by 2050, that is, within the investment horizon of most pension funds. China’s markets will therefore also be multiple times larger than US markets and due to their greater liquidity everyone will therefore adopt them as benchmarks for stocks, bonds and FX in exactly the same way that global benchmarks moved from UK to the US in the inter-war years. None of what is happening now with coronavirus or the petty political blame games changes any of that.

Nor will the general direction of economic policy in China change. President Xi Jinping wants to go down in history as the leader, who put China on its path towards global economic and financial hegemony. To this end, he will continue to veer China’s economy away from its erstwhile reliance on exporting to the West towards domestic consumption-led growth. This means that within a couple of decades, China’s economy will look very much like the United States economy today: Consumption led, a current account deficit, a global reserve currency, financing from other countries, deep open financial markets, and a very powerful central bank.

This economic rotation towards more consumption led growth requires three broad sets of reforms, which will also continue for the next decade at least:

• Freeing up interest rates and liberalising local capital markets to enable conventional monetary policy tolls to be used to control consumption, investment, and inflation.

• Liberalising prices and increasing the size of the private sector to increase productivity, so that domestic demand – mainly consumption – can be stepped up without jeopardising price stability and the external balance.

• Opening up the capital account to enable China to finance its inevitable current account deficit due to rising consumption. This involves promoting CNY as a reserve currency and joining benchmark indices for bonds and stocks. This year China joined GBI EM GD, for example, and Chinese bonds have already displayed excellent qualities as a safe haven asset within the EM asset class.7 These qualities will gradually become more apparent to and appreciated by investors, thereby slowly eroding the Dollar’s erstwhile monopoly position as the sole safe haven.

While China’s growth strategy and policy choices are under its own control, China’s reputation is not. China is still viewed by many as source of risk, despite the country’s enormous positive contribution to the world economy. China’s greatest challenge will be to overcome the intense prejudices against and fear of her in the West. However, crises, such as coronavirus, speed up the process. Every time the populist governments in the West take decisions that are clearly negative for the world, China makes sure it does everything possible to seem sensible, mature, reasonable, multilateral, basically acting like the adult in the room. This is why China expresses support for WHO when the US government pulls out, touts free trade when Trump declares trade war, calls for climate accords, when the US pulls out, etc. This is how China gradually builds its reputation as a reliable international player.

The European Union is in many ways the more natural successor to the US as global leader. However, Europe is the most tribalistic region in the world and cannot speak with one voice. Unfortunately, since Europeans and Americans are not yet ready to place their trust in China the world has now entered a darker period, where “the best lack all conviction and the worst are full of passionate intensity”.8 Rogue states can reign more freely in this world. There will be more bully tactics in the global school yard. And until China has overcome the misgiving against her there will be an elevated level of global risk, which poses headwinds to everyone, including EM investors.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2020.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.

4 See: “The case for a global macro-prudential policy”, Market Commentary, 20 April 2020.

5 Markets bottomed out within a month of the spike in the VIX index, confirming with the pattern of previous risk off episodes. See: “It is here again – the VIX spike!”, Market Commentary, 28 February 2020.

6 For a very detailed explanation of the important relationship between US fiscal policy and productivity growth see: “What goes around comes around: a short note on Dollar risk”, Market Commentary, 17 January 2020.

7 See: “Chinese bonds challenge Treasuries as ‘safe haven’ destination”, Market Commentary, 2 April 2020.

8 ‘The Second Coming’, William Butler Yeats.