The decision to hold the federal funds rate steady was in line with expectations, but the accompanying statement and projections indicate a shift toward easing in 2024.

As expected, the Federal Reserve kept the target range for its policy rate—the federal funds rate —unchanged at 5.25% to 5.5% at its latest meeting. The decision was unanimous. While the decision to hold the fed funds rate steady was in line with expectations, the accompanying statement and projections point to a shift toward easing in 2024. In addition, Fed Chair Jerome Powell's comments in his press conference confirmed that most members of the committee believe that the hiking cycle is over, and they discussed the path to lower rates.

Inflation is the key to the policy pivot

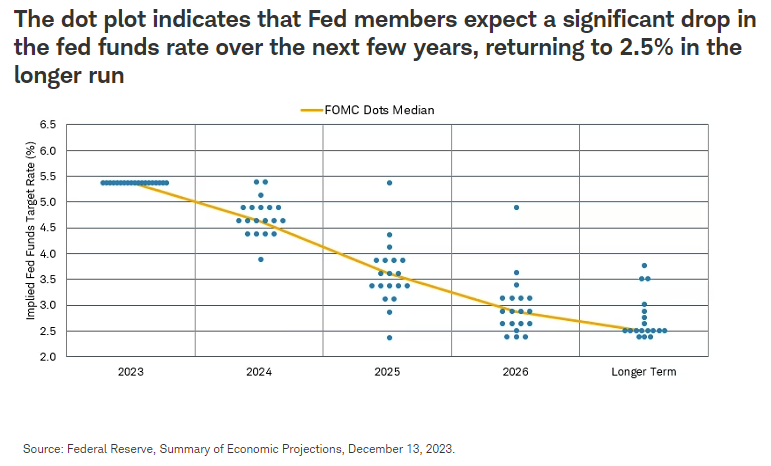

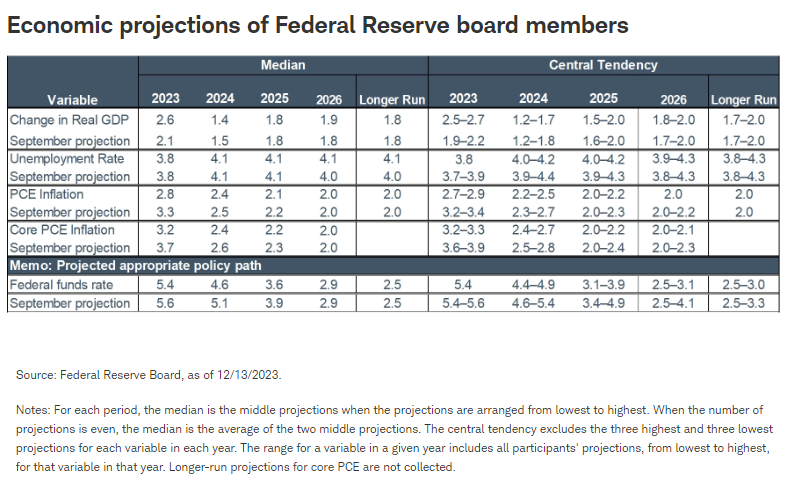

Encouraged by declining inflation, the Federal Reserve's Open Market Committee (FOMC) signaled that more rate hikes are unlikely in this cycle and that there could be 75 basis points in rate cuts in 2024. The statement that accompanied the Fed's decision indicated that "growth of economic activity has slowed since the third quarter" and "inflation has eased over the past year." In the accompanying Summary of Economic Projections (SEP), the median estimate of Fed officials suggests three rate cuts of 25 basis points each in 2024, bringing the fed funds rate to 4.6%. That compares to an estimate of 5.1% as recently as last September.

The shift in the Fed's projections brings them much closer to what the markets had been expecting compared to its previous projections. The "dot plot," which shows each member's estimates for the fed funds rate going forward for the next several years, indicates much more optimism about inflation heading back to target in the next few years. For a Fed that has been cautious about presenting an aggressive inflation-fighting stance, the change in tone was notable and was reflected in a strong rally in the bond market.

The Fed's quarterly economic projections suggest declining inflation.

The Fed appears on a track to "normalizing" interest rates—moving from a tightening stance to a more neutral stance. At neutral, the Fed hopes to have rates at a level consistent with slowing growth and inflation at 2%.

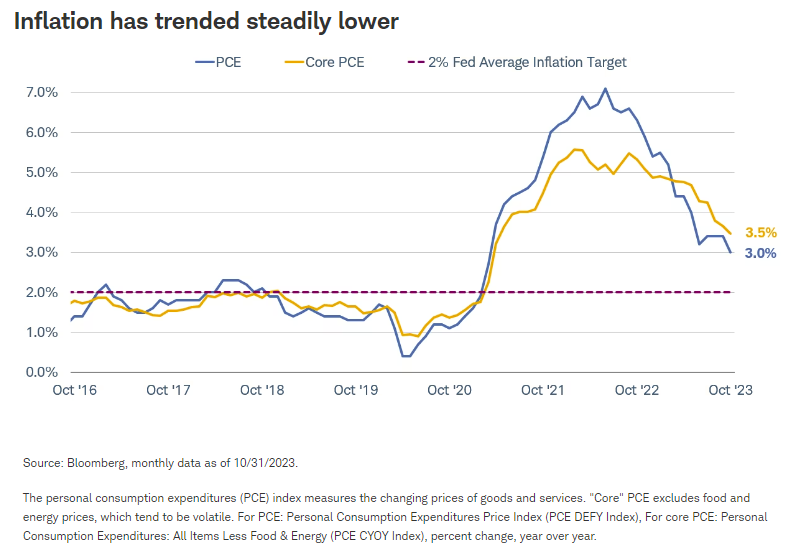

Since the last FOMC meeting, the benchmark inflation measure that the Fed uses—the deflator for personal consumption expenditures excluding food and energy (core PCE) has declined. It has trended steadily lower over the past year and now stands at just 3.5% compared to a peak level of 5.6% in this cycle. That progress appears to be encouraging the Fed to begin rate cuts sooner rather than later.

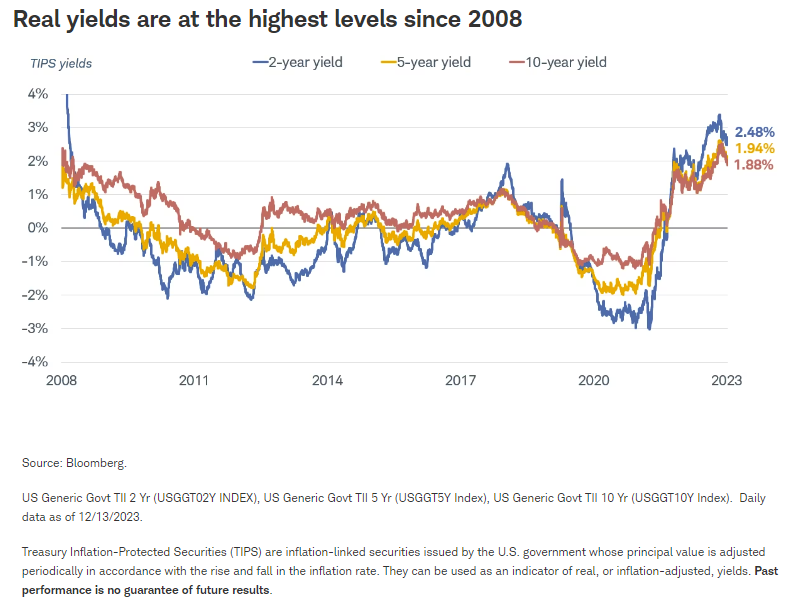

If the Fed left policy unchanged for a long time period as inflation declined, then real interest rates—adjusted for inflation—would continue to climb, exerting more pressure on economic growth. Real interest rates are already at the highest levels since 2008. Therefore, to some extent, Fed rate cuts are just aimed at preventing real interest rates from rising to even higher levels, risking a recession.

The Fed's economic projections indicate that the committee expects a modest rise in the unemployment rate, but not in the range that would suggest a recession forecast. Fed Chair Powell suggested in his press conference that the labor market is "coming back into balance." Given the Fed's mandate to aim for full employment along with low inflation, this is the "soft landing" scenario that the central bank has been seeking.

Quantitative tightening continues

The prospect of lower short-term interest rates is positive for the economic outlook and financial markets. However, the Fed does plan to continue to reduce the size of its balance sheet by allowing bonds it holds to mature without reinvesting the principal. The balance sheet has already fallen by more than $1 trillion from its peak. Continuing with quantitative tightening "in the background" may prove more difficult long-term if the economy slows down more than anticipated. However, for now, the reduction plan seems to be working without disrupting financial markets.

Financial markets responded positively to the surprisingly "dovish" projections from the Fed. Markets often make big moves at turning points. With rate cuts now on the horizon, yields of all maturities should continue to trend lower as the Fed looks to get to a more "neutral" interest rate. Two-year Treasury yields are nearly 80 basis points off the cyclical highs while 10-year treasury yields are nearing 4% after having touched 5% in late October. In the near term, the market reaction may be somewhat overdone, and we do expect volatility ahead, but we continue to be optimistic about the prospects for returns to fixed income investors in 2024.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation. Treasury Inflation-Protected Securities are guaranteed by the US Government, but inflation-protected bond funds do not provide such a guarantee.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab