Last week, the U.S. labor market took center stage, delivering conflicting signals, all while the S&P 500 reached multiple record highs during the shortened trading week. While the official U.S. employment report for June showed stronger-than-expected job additions and a surprising drop in the unemployment rate, underlying details suggested a more nuanced story. In contrast, the ADP Employment Report indicated an unexpected private sector job loss for the month, while Job Openings (JOLTS) unexpectedly jumped to a six-month high in May. Amidst these divergent signals from the labor market, the S&P 500 responded positively, hitting new record highs on three out of the four trading days, with its strongest surge occurring on Thursday following the stronger-than-expected jobs report.

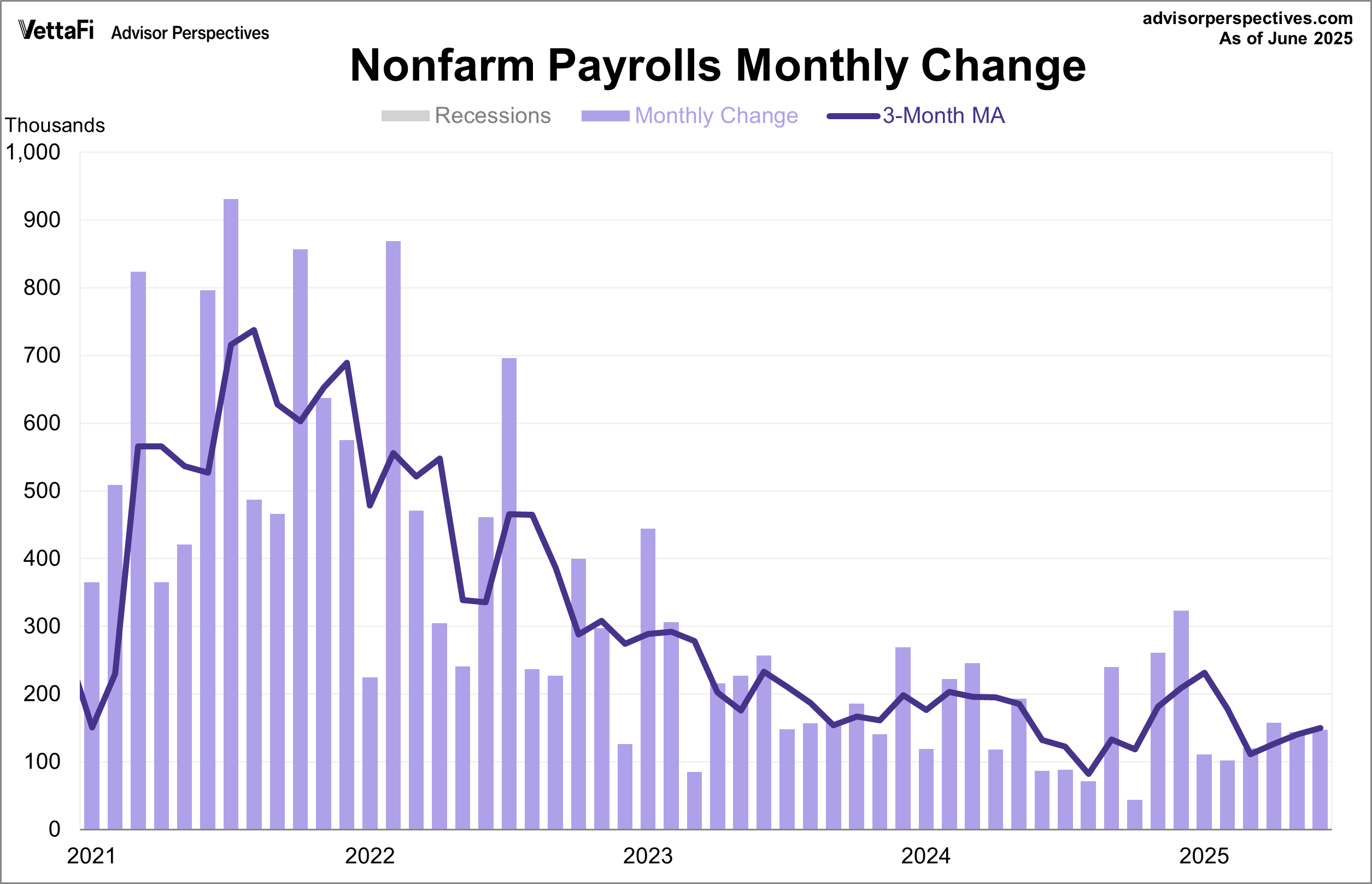

Employment Report

The U.S. labor market continued its resiliency in June, adding more jobs than anticipated for a fourth straight month. The latest employment report showed that 147,000 jobs were added last month, exceeding the expected 111,000 addition. Additionally, May’s number was revised higher to 144,000 new jobs. Meanwhile, the unemployment rate remained near historically low levels at 4.1%. This was an unexpected decline as the rate was projected to inch higher to 4.3%. Wage growth was softer than expected last month with average hourly earnings up 0.2% compared to the previous month and up 3.7% from one year ago.

While June’s headline data looks strong on the surface, underlying details of the report point to a slowing labor market. For instance, only 74,000 jobs came from the private sector. This is the lowest private job growth since October. The remaining 73,000 jobs were largely attributable to government employment, particularly in education, which is influenced by summer seasonality. Additionally, the labor force participation rate came in at 62.3%, its lowest level since 2022. Combining this with the unexpected drop in the unemployment rate, suggests fewer people are seeking work.

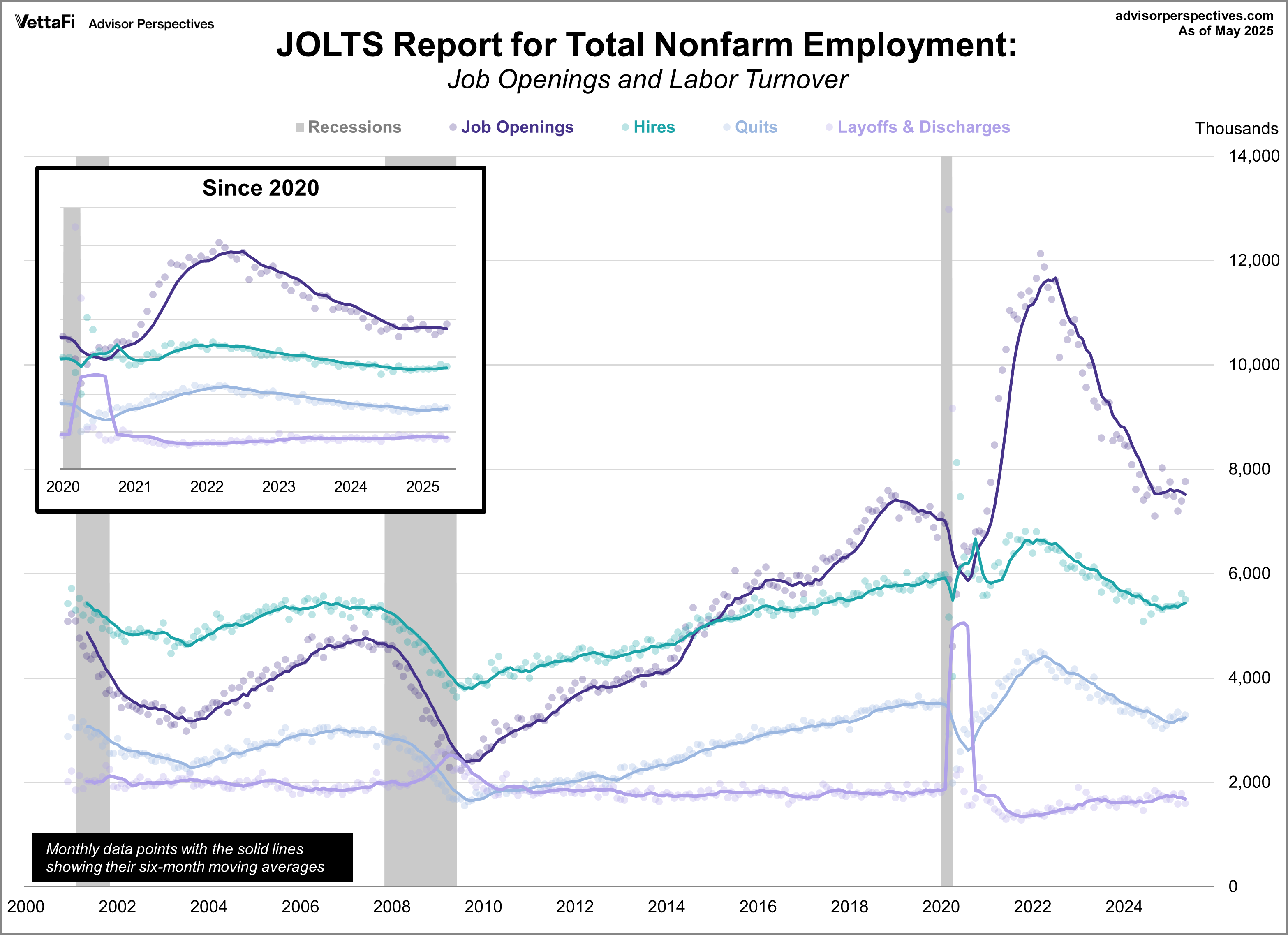

Job Openings and Labor Turnover Summary (JOLTS)

Job openings unexpectedly jumped to a six-month high in May. The latest JOLTS report revealed vacancies increased by 374,000 to 7.769 million, exceeding the predicted 7.320 million. Job openings have steadily declined over the past three years and are finally starting to touch pre-pandemic levels.

The report also showed that hires and layoffs decreased, while quits rose. The hiring rate remains near its lowest levels over the past decade, at 3.4%. The quit rate, which indicates worker confidence, inched up to 2.1%, well below pre-pandemic norms. Lastly, the layoffs rate edged lower to 1.0%. The ratio of job openings to unemployed workers was at 1.07, well below the peak from a few years ago when there were two jobs available for every one unemployed worker.

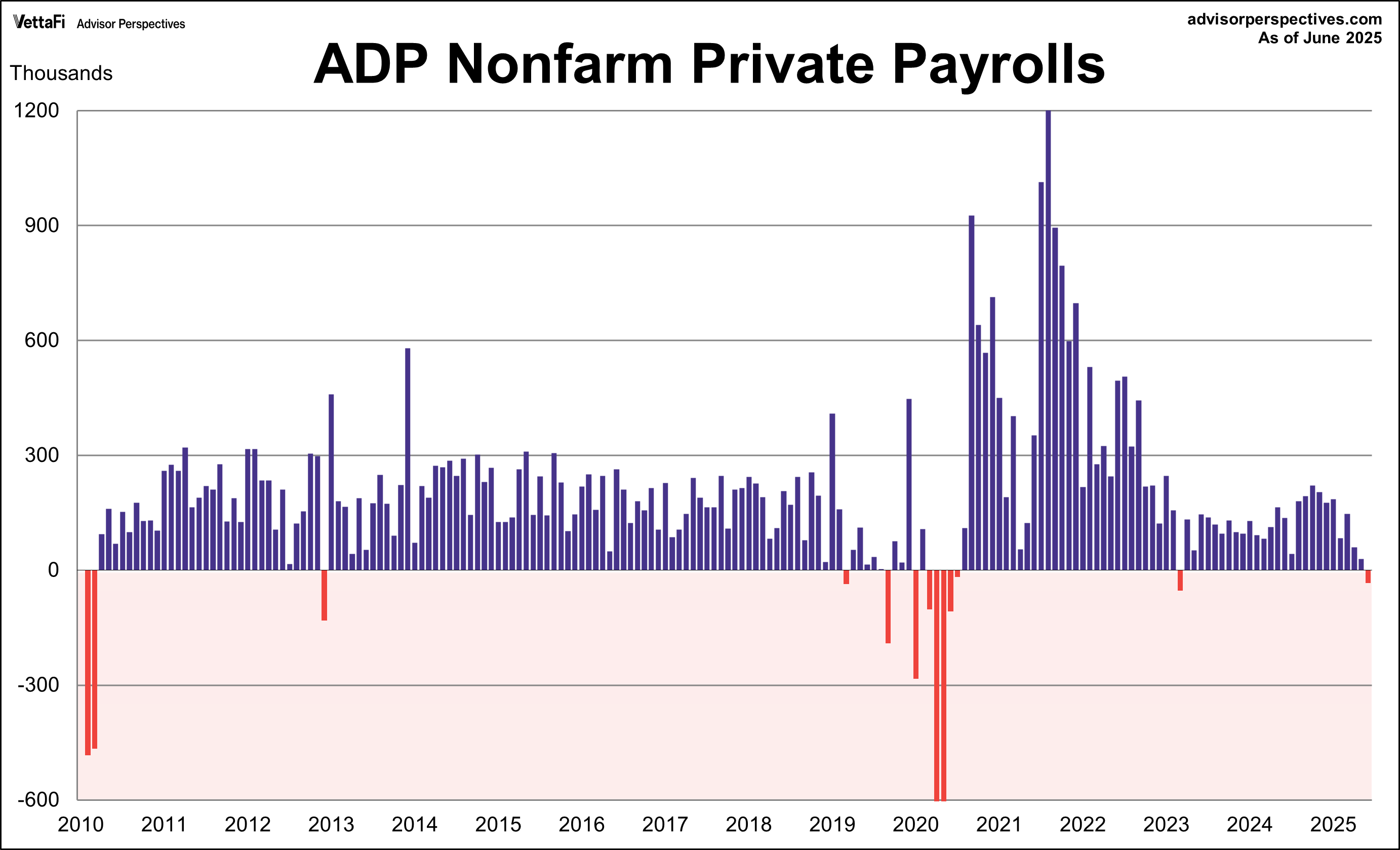

ADP Employment Report

In contrast to the BLS employment report and May’s JOLTs data, the ADP employment report pointed to a cooling labor market. According to the latest data, the private sector unexpectedly lost 33,000 jobs in June. This marked the first monthly reduction since March 2023 when there was a decline of 53,000 jobs. It was anticipated that 99,000 private sector jobs were added last month.

The job loss last month was due to declines in service-providing industries which lost 66,000 jobs whereas goods-producing industries gained 32,000 jobs. Additionally, small size companies (1-19 employees or 20-49 employees) lost a combined 47,000 jobs in May while large companies (500+ employees) gained 30,000 jobs.

Market Reactions

The S&P 500 closed out the shortened-trading week at a new record high, its third in the past four trading days and the seventh of the year. The index posted a 1.7% weekly gain, its second consecutive week in the green. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.7% last week. Meanwhile, the S&P Equal Weight Index was up 2.4% from the previous week and the Invesco S&P 500 Equal Weight ETF (RSP) rose 2.4%.

The 10-year Treasury yield finished the week at 4.35%, while the 2-year note finished at 3.88%.

The CME FedWatch Tool currently shows a 95% likelihood that the Fed will hold rates steady at their next meeting this month. Markets are pricing in two 25 basis point cuts for later this year coming at the September and October meetings. Additionally, three 25 basis point cuts are projected in 2026.

Economic Data in the Week Ahead

The economic data this week will be relatively muted with only a few releases during the week. On Tuesday, the National Federation of Independent Business (NFIB) will release their Small Business Optimism Index. Then on Thursday, weekly unemployment claims will give another glimpse into the overall health of the labor market.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi