Late last Friday, the Court of Appeals for the Federal Circuit (CAFC) largely affirmed the Court of International Trade’s (CIT) May ruling blocking President Trump’s tariffs imposed under the International Economic Emergency Powers Act (IEEPA). We expect the decision to land at the Supreme Court and for a ruling to come early in 2026, so it’s not clear if any tariffs must be removed just yet. Based on what we’ve heard from the various courts that have heard this case so far, and the policy strategists we follow, we believe it’s more likely than not that the Supreme Court upholds the CAFC decision, but that is a very low conviction call.

What’s at Stake

The IEEPA tariffs are the bulk of the tariffs the administration has put on far so this legal decision matters (though maybe not as much as you might think, as we explain below). According to Goldman Sachs, these tariffs account for eight percentage points of the roughly 11 percentage point increase in the effective tariff rate to date (from 2–3% under the Biden administration). Bloomberg’s calculations indicate a drop in the overall U.S. tariff run rate from 16% to less than 7% if all IEEPA tariffs go away.

A Backup Plan Is in Place

Our most important takeaway from this latest development is that the Trump administration has a backup plan. That plan could take a couple of different forms, but we believe most of these tariffs can be put back into place even if the Supreme Court rules they are illegal. Delays would occur, and rebates back to the companies that paid them could be required (though unlikely, in our view). But in the end, we expect most of these tariffs to stick in the long term.

Most Likely Path

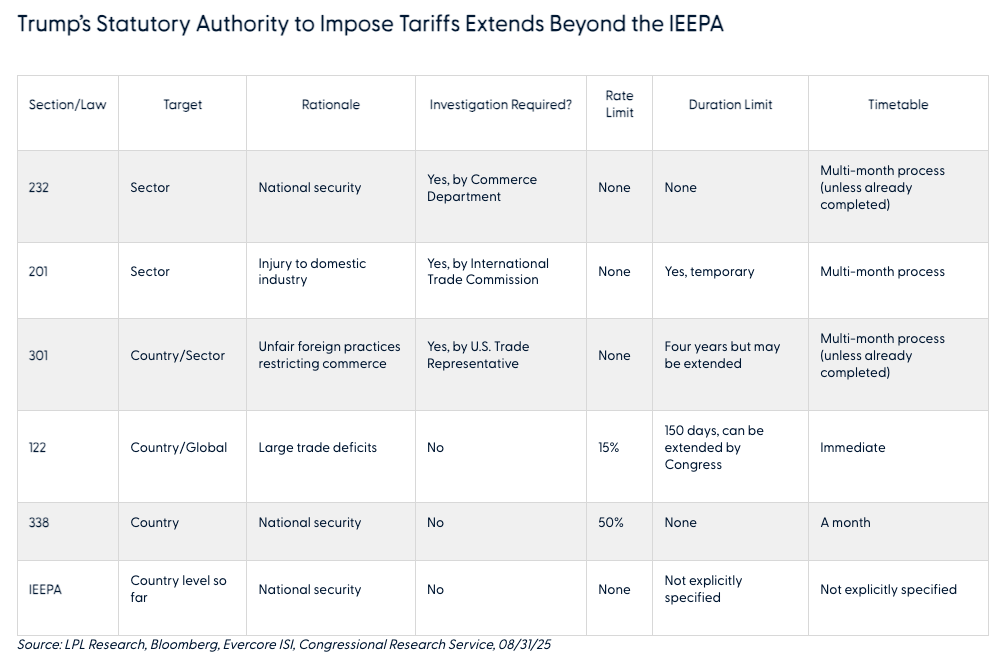

We believe the most likely backup plan is for the administration to use Section 122 to put the tariffs back on temporarily while an investigation takes place to enable use of Section 301. Section 122 requires large trade deficits (easy hurdle) but can only be employed for 150 days. That would allow the U.S. Trade Representative to conduct the required multi-month investigation to put on Section 301 tariffs that require proof of unfair trade practices by countries. While that has not been difficult to prove in the case of China 301 tariffs, it won’t be as easy for broader tariffs across dozens of countries. That will take more time, and bring more near-term uncertainty, but 301 tariffs can be extended after four years, making them a long-term strategy.

Another potential path that would bring more legal uncertainty is to go straight to Section 338. Tariffs under 338 could be employed within a month at current rates (the maximum rate is 50%) and remain in place long term based on discrimination against U.S. trade. The problem is this law has never been used, creating more legal uncertainty. The Trump administration may have to go to plan B, but it doesn’t want to go to plan C.

Market Implications

The market implications of this news are tough to parse through because we don’t know where the courts will take us. Tariff revenue helps contain increases in the deficit, as we wrote about in “Are Tariffs the Solution to America’s Debt Problem?” If tariffs are halted/rebated, the deficit widens because the Treasury would take in less revenue. The current tariff revenue run rate is roughly $200 billion annualized — and it’s headed higher if these tariffs stay in place. Essentially, corporate America would get a stimulus boost. Lower costs mean more earnings.

Fewer tariffs also reduce the upward pressure on inflation, on the margin. Not long ago, Federal Reserve (Fed) Chair Jerome Powell indicated that if it weren’t for tariffs, the Fed would have probably cut rates early this year. If tariffs come and go and come again, neither the Fed nor the markets will have a good handle on inflation effects. At the same time, tariffs haven’t lifted inflation much to date, so maybe the market shouldn’t worry so much about it anyway.

Conclusion

After Friday’s federal court ruling Trump’s IEEPA tariffs illegal, the decision will land at the Supreme Court. Regardless of how the highest U.S. court rules, expect most of the current tariffs to remain in place. The administration has at least one legal path to restore tariffs that we, and several policy strategists we follow, believe would stick. So, while deficit concerns may pick up in the short term while this legal morass gets sorted out, and it’s possible that not all tariffs are restored, the Trump administration’s long-term strategy to offset deficit spending from the One Big Beautiful Bill Act (OBBBA) with tariff revenue remains intact. Any boost to corporate America from reduced/rebated tariffs will likely be short-lived, and Friday’s ruling does not eliminate near-term inflation risk from tariffs.

LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) remains neutral toward equities overall, slightly favors the growth style over value, large caps over small caps, and remains neutral on a regional basis. The Committee continues to look for opportunities to add equities on potential pullbacks.

Jeff Buchbinder, CFA, provides the top-down view of the stock market for LPL Financial Research. He has over 25 years of experience in equities.

A message from Advisor Perspectives and VettaFi: Thinking about starting your own RIA, making a move to a different firm, or specializing in a new area? Read our latest articles on financial advisor transitions.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #791305

Read more commentaries by LPL Financial