First Cut of the Year

At its September meeting, the Federal Open Market Committee (FOMC) cut the federal funds target range by 25 basis points to 4.00%–4.25%, marking the first rate reduction of the year after eight months of holding steady.

Policymakers framed the move as a risk management step, citing a combination of slowing job gains, a rising unemployment rate, and inflation that remains “somewhat elevated.” The Fed emphasized that while inflation has moderated from its peak, progress toward the 2% target has been uneven, and recent labor market data signaled cooling momentum. Updated projections indicated the possibility of two additional cuts by year-end and one more in 2026, suggesting a gradual easing cycle rather than an aggressive pivot.

The decision came against a backdrop of mixed economic signals. GDP growth forecasts were revised slightly higher, reflecting resilient consumer spending, but payroll revisions and a rising unemployment rate raised concerns about underlying labor market strength. Inflation, while trending lower, remains above target, keeping the Fed cautious about cutting too quickly. This balancing act could be described as an insurance cut.

Financial market reactions were mixed. Treasury yields fell across the curve, with the 2-year yield dropping nearly 10 basis points but only temporarily. By the end of the day, 2-year yields were slightly higher than just before the announcement. Over the next day or so, equity markets rallied, led by rate-sensitive sectors such as technology (due to its long-duration cash flows) and real estate, while the U.S. dollar initially weakened modestly against major currencies before quickly bouncing back. Investors expect the Fed to move faster next year than its own projections suggest. Volatility remains elevated as traders weigh incoming data against the Fed’s conflicting tone.

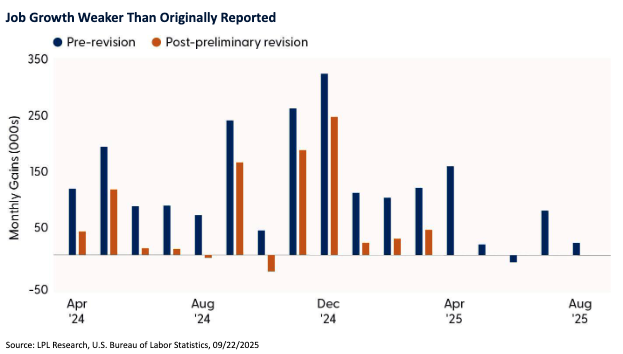

Softer Labor Market Nudged the Committee

The Fed was concerned about the preliminary benchmark revisions to payroll growth because they suggested that job creation over the prior year was significantly weaker than previously reported. The Bureau of Labor Statistics estimated an 818,000-job downward revision for the 12 months ending in March 2024, equivalent to about 68,000 fewer jobs per month than initially thought. This raised questions about the true strength of the labor market, a critical input for monetary policy decisions. A softer employment backdrop could imply less wage pressure and slower economic momentum, potentially accelerating the case for rate cuts. The revisions also introduced uncertainty into the Fed’s assessment of economic resilience, making it harder to gauge whether restrictive policy was still appropriate.

An Act of Solidarity?

The Federal Open Market Committee’s 11-1 vote at its latest meeting signals strong alignment among policymakers on the decision to deliver a 25-basis-point rate cut, but the lone dissent underscores an important internal debate. Newly appointed Governor Stephen Miran voted for a 50-basis-point cut, citing concerns about emerging labor market weakness and the risk of a sharper economic slowdown. In contrast, the majority favored a more measured approach, emphasizing the need to balance downside risks with the ongoing challenge of bringing inflation sustainably back to target. In an act of solidarity, both committee members Waller and Bowman joined the majority with last week’s decision despite being in the running to be the next Fed chair.

Dissenting votes are relatively rare but not unprecedented. Historically, they tend to cluster during periods of economic transitions such as the early 1980s disinflation, the 2008 financial crisis, and the 2020 pandemic response when uncertainty about the appropriate policy stance is high. In recent years, dissents have often reflected differences in risk tolerance rather than fundamental disagreements about the Fed’s dual mandate. The current dissent was not a surprise because of the vocal calls to cut aggressively from the President. Stephen Miran was previously chairman of President Trump’s Council of Economic Advisors and is (controversially) on leave from that position.

While a single dissent does not alter the policy path, it can influence market perceptions of the Fed’s ability to stay outside of political pressure. Investors may interpret the vote split as an early sign of increasing pressure as the FOMC will have a new chair after Jerome Powell’s term expires in May of next year. For markets, this means heightened risk to the central bank’s independence in the coming year.

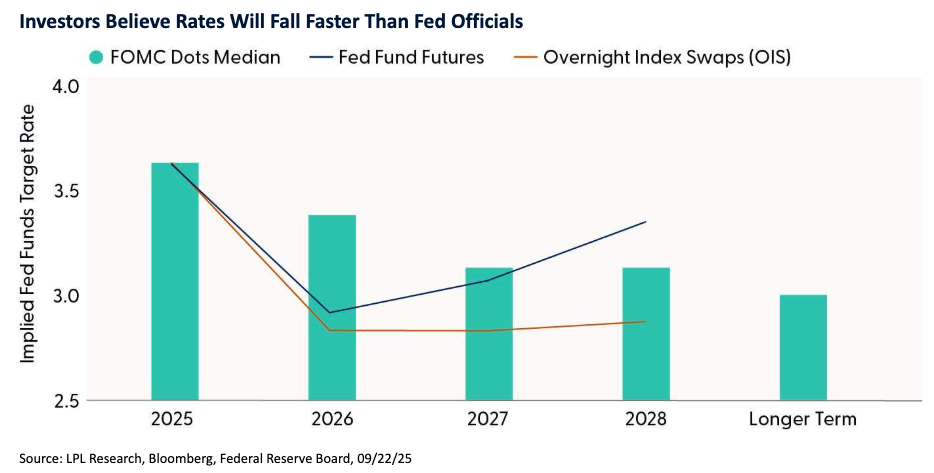

Market Expectations Diverge from the Fed’s Outlook

While the Federal Reserve’s latest dot plot signals only a modest pace of easing in 2026, markets are betting on a much steeper path of rate cuts. The September projections place the federal funds rate near 3.4% by year-end 2026, implying just one additional cut beyond 2025 levels. Futures markets, however, are pricing in multiple cuts, reflecting expectations that slowing growth and a softer labor market will compel the Fed to act more aggressively. This divergence underscores a fundamental debate: will inflation remain sticky or will disinflation and weaker demand dominate as markets seem to anticipate? The answer will shape the trajectory of monetary policy over the next two years. The gap between official guidance and market pricing underscores the uncertainty surrounding monetary policy in the coming years and highlights the risk of volatility if either side is proven wrong.

This disconnect carries significant implications for financial markets. If the Fed sticks to its slower pace of cuts, long-term yields could remain higher than markets expect, pressuring equity valuations and rate-sensitive sectors like housing and technology. Conversely, if the Fed ultimately aligns with market expectations and cuts more aggressively, risk assets might rally on easier financial conditions. The wider the gap between the dot plot and market pricing, the greater the potential for volatility as traders recalibrate positions based on incoming data and Fed communications.

More About Congress, Less About Fed

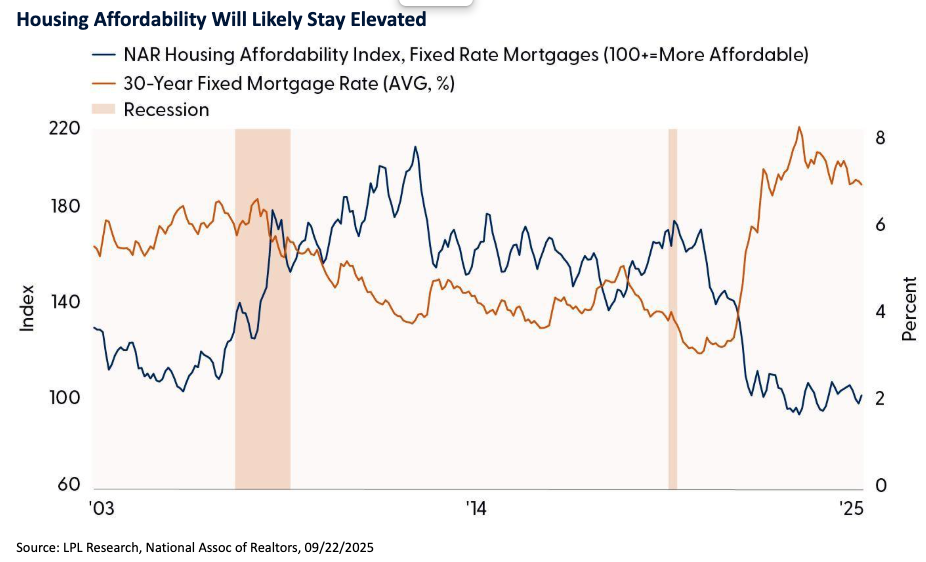

A common question we get is where we think mortgage rates will head in the near term. We expect mortgage rates to continue to come down from recent highs, but it’s important to set expectations. A cut in the fed funds rate does not necessarily mean mortgage rates will fall. The relationship between these two rates is complex. Mortgage rates are primarily influenced by long-term interest rate dynamics, which are shaped by the fiscal outlook and the 10-year U.S. Treasury yield rather than the Fed’s short-term policy rate. That’s why it’s more about Congress and less about the Fed. The 10-year Treasury acts as the benchmark for mortgage-backed securities, and lenders price mortgages partially based on the yields investors demand for holding long-term debt. When fiscal policy results in large deficits and heavy Treasury issuance, investors often require higher yields to compensate for increased supply and inflation risk, pushing mortgage rates higher. For example, in 2024, even as the Fed began cutting the federal funds rate, mortgage rates remained elevated because Treasury yields stayed high amid concerns about persistent deficits and strong issuance. However, this year was different. Mortgage rates fell in anticipation of a dovish tilt from the FOMC. This illustrates that while the Fed can influence short-term borrowing costs, mortgage rates are anchored to long-term expectations about inflation, growth, and government borrowing needs.

The persistent lack of housing supply is a key factor keeping median home prices elevated, even in the face of higher mortgage rates and affordability challenges. Inventory remains constrained for several reasons: many homeowners are “rate-locked,” unwilling to sell and give up historically low mortgage rates, new construction has lagged household formation for over a decade, and zoning restrictions and labor shortages continue to limit building activity. The lack of supply could be a growth opportunity for homebuilders as they bring more inventory to market. This structural shortage means that even modest demand creates competitive bidding, keeping upward pressure on prices. For example, in 2024, active listings were still well below pre-pandemic norms, and months of supply hovered near historically low levels, signaling a seller’s market. As a result, while higher borrowing costs have cooled transaction volumes, they have not produced broad price declines because the imbalance between supply and demand remains severe. Until inventory meaningfully increases through new construction or more existing homes coming to market, median prices are likely to stay elevated, acting as a floor under the housing market and keeping affordability near the all-time lows.

The Call to Action

Prepare for volatility as investors assess the risks of leadership changes at the Fed. Expect lower fed funds rates in the coming quarters. And yes, consumer borrowing rates should eventually follow that lower path as productivity enhancements propel growth with less cost pressures.

The first year of this rate-cutting cycle has been excellent for stocks, and history offers a reason for optimism as the cycle continues. Year two of rate-cutting cycles has historically delivered solid gains for stocks — provided the economy avoids recession. Markets like rate cuts that are a luxury, not an emergency. With the Fed likely to signal more easing ahead, and near-term recession risk seemingly low, the backdrop for stocks remains constructive.

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities. Investors may be well served by bracing for occasional bouts of volatility given how much optimism is reflected in stock valuations, lingering tariff and inflation risks. STAAC’s regional preferences across the U.S., developed international, and emerging markets (EM) are aligned with benchmarks. The Committee still favors growth over value, large caps over small caps, and the communication services and financials sectors.

Within fixed income, the STAAC holds a neutral weight in core bonds, with a slight preference for mortgage-backed securities (MBS) over investment-grade corporates. The Committee believes the risk-reward for core bond sectors (U.S. Treasury, agency MBS, investment-grade corporates) is more attractive than plus sectors. The Committee does not believe adding duration (interest rate sensitivity) at current levels is attractive and remains neutral relative to benchmarks.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or

services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy. All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet or Bloomberg.

Read more commentaries by LPL Financial