Alternative Candidate(s) for Data During Shutdown

Membership required

Membership is now required to use this feature. To learn more:

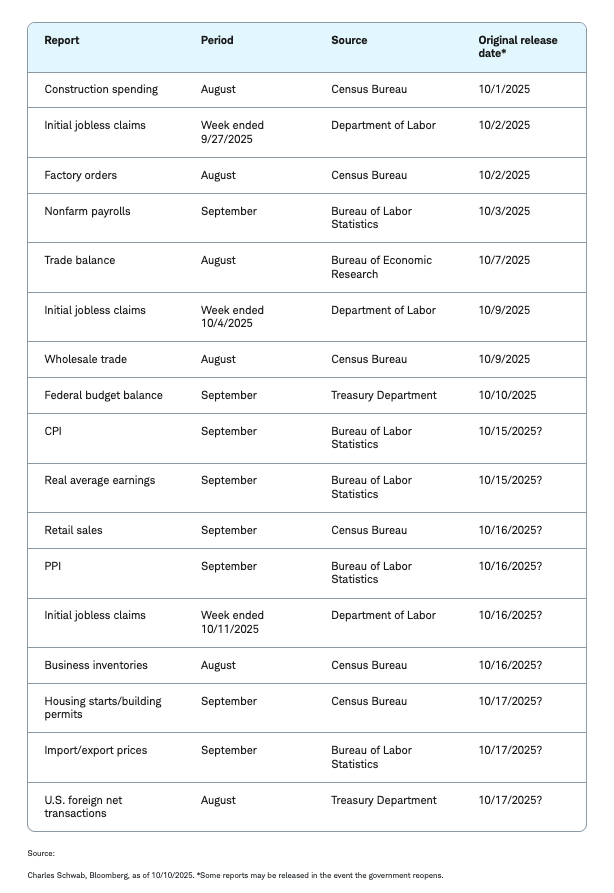

View Membership BenefitsWith key federal government agencies shuttered and official data releases suspended, investors have been turning to alternative private sector data sources to track real-time economic conditions during the shutdown. We are highlighting key sources in this week's report which are helping to fill the informational void left by delayed reports such as the Employment Situation (monthly jobs report), construction spending, the trade balance, and retail sales.

Below, we show how much longer that list might be if the shutdown lasts through the end of this week. Worth noting is that the Bureau of Labor Statistics (BLS) is calling back employees to put out the September Consumer Price Index (CPI) report, which is now slated for release on October 24th.

Economic reports delayed by government shutdown

U.S. government data are the gold standard in terms of depth and breadth. The collection efforts and capabilities of the Bureau of Economic Analysis (BEA), BLS, and others are second to none, so it's understandable that with these agencies closed, markets and investors are presumably flying blind. While we wait in the (federal) dark, the best we can do is sift through data from the private sector—many of which we'll go over briefly in this report.

What say you, labor data?

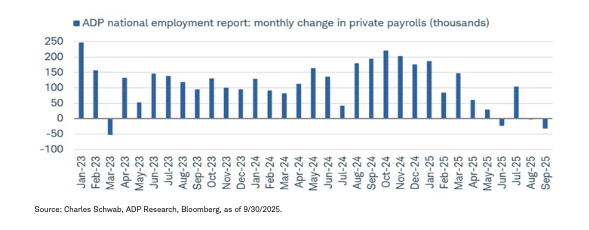

Catching most investors' attention in the past couple weeks was the employment report put out by ADP, which tracks private sector job growth. As shown in the chart below, ADP reported a decline of 32,000 jobs in September, which was much worse than August's decline of 3,000. That drop was revised from an initially reported gain of 54,000–meaning the labor picture was much worse than expected heading into September.

ADP payrolls contracting

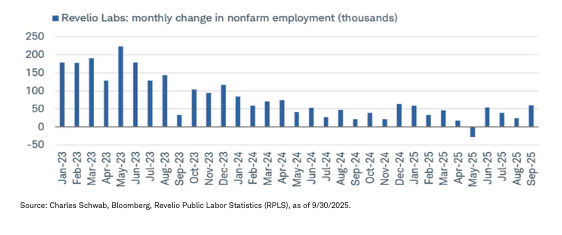

Conversely, however, a report from Revelio Labs—which uses data from 100+ million U.S. job profiles and follows a similar format to the BLS in tracking labor data—showed that the economy added 60,000 jobs in September. That's in stark contrast to ADP's report, but keep in mind that both sources' trends were also quite different last year, with Revelio understating the degree of strength in both ADP jobs as well as payrolls reported by the BLS.

Revelio says no pain, strong gains

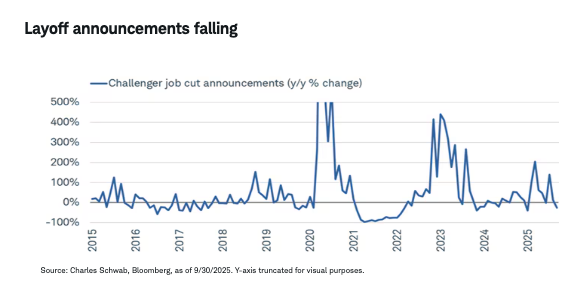

In keeping with the labor theme of low layoff activity, job cut announcements tracked by Challenger, Gray, and Christmas have rolled back over; the year-over-year change fell further into negative territory in September.

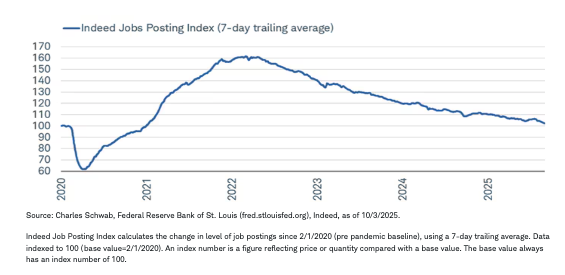

In keeping with the other labor theme of low hiring activity, Indeed's Job Posting Index has also continued to decline, suggesting a continued downtrend for the BLS' Job Opening and Labor Turnover Survey (JOLTS).

Indeed, there is less labor demand

At the small business level, however, there is a different trend in place. Per the National Federation of Independent Businesses (NFIB), hiring plans have picked up over the past few months. Worth noting is that the level is not particularly strong, so the recent rebound isn't suggestive of a major hiring boom on the horizon.

Small business hiring plans improving

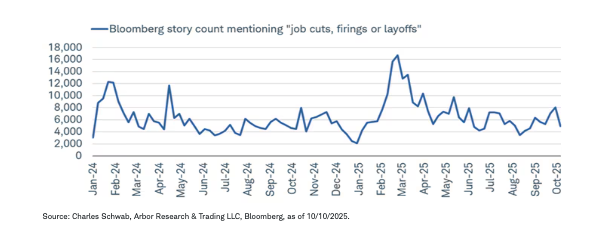

That provides a bit of a contrast to the recent pickup in news stories mentioning job cuts, firings, or layoffs per Bloomberg news. The uptick wasn't as aggressive as what was seen in the first quarter of this year, and as shown below, it has rolled over again; although if federal layoffs persist, this could hook higher again.

An improving "story"

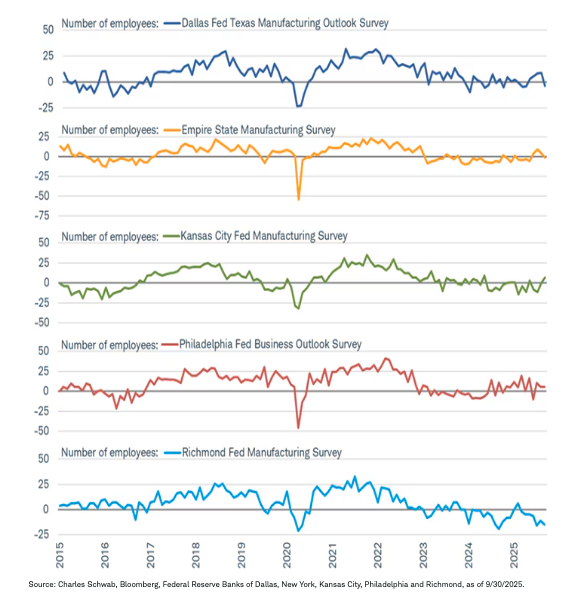

One benefit of the Federal Reserve banks being separate from the federal government is that they don't cease operations during shutdowns. As such, we have employment statistics from the five key regional Fed banks, which provide their own manufacturing reports each month. As shown below, three of the five show employment being in contraction in September, with Richmond in the weakest spot.

Fed banks reporting labor weakness

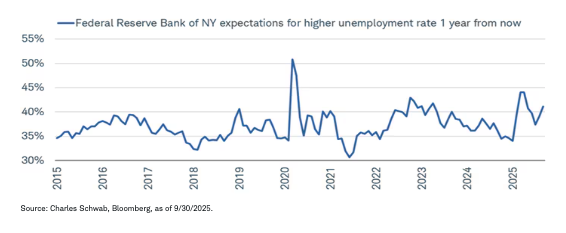

In a separate report put out by the New York Fed, consumers' expectations for higher unemployment a year from now has started to pick up rather sharply. As shown below, there was a nice rolling over earlier this year, but that has started to reverse.

NY Fed says labor concerns rising…

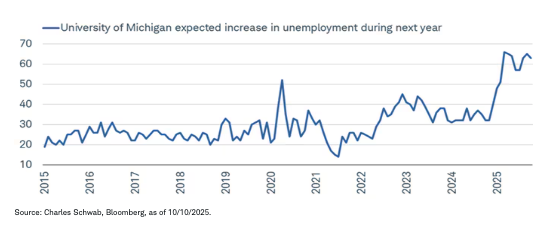

That is consistent with, but not as bad as, a similar datapoint put out by the University of Michigan (UMich) in its Consumer Sentiment Index. Expectations for higher unemployment are near a cycle high, shown below.

…and so does UMich

Inflation and growth concerns justified?

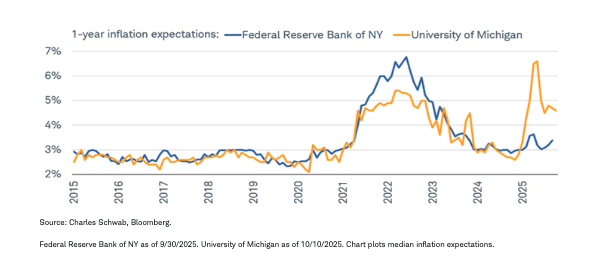

As mentioned, we are expecting to see a CPI report toward the end of the month, but for now, we can take a look at a few supplemental datapoints that show still-sticky inflation expectations. For September, the New York Fed's consumer survey showed an uptick in year-ahead inflation expectations. UMich's series ticked down a little but remains considerably high.

Price concerns still elevated

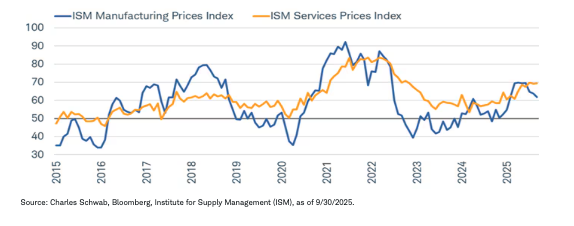

On the business side, the picture is a bit mixed when splitting the economy into manufacturing and services. As shown below, the Purchasing Manager Indexes (PMIs) from the Institute for Supply Management (ISM) underscore stickier price pressures for services, but some easing for manufacturing.

Stickier services prices per ISM

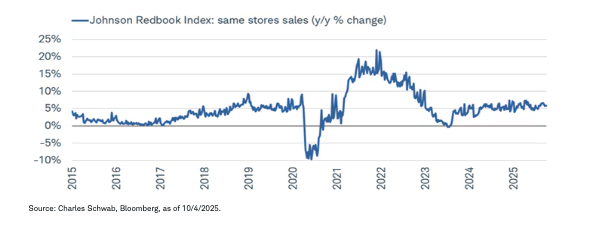

None of those inflation concerns have derailed consumer spending, however. The Johnson Redbook Index, which tracks same-store retail sales on a weekly basis, has been firmly in positive year-over-year territory for the better part of the past two years.

Redbook sales not in the red

In sum

While less standardized and occasionally more volatile, the datasets above, among others, can offer valuable high-frequency insights into labor demand, inflation, and consumer behavior. While we wait for the government to re-open, these alternate data sources can serve as an essential bridge for economic monitoring until normal statistical reporting resumes. Beyond that, it would not surprise us if these alternative data sources remain popular monitors alongside government-issued releases, given recently elevated concerns about government data efficacy and low response rates to a wide number of survey-based data points.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

Investment and Insurance Products: Not a Deposit • Not FDIC Insured • Not Insured by any Federal Government Agency • No Bank Guarantee • May Lose Value

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All