This bull market has been on quite a run. The S&P 500 is up 35% since its April 8, 2025 year-to-date low, and up over 92% since it began on October 12, 2022, excluding dividends (we wrote about the now three-year-old bull market in this LPL Research Weekly Market Commentary two weeks ago).

The rally, led by technology stocks riding the artificial intelligence (AI) wave, has caused many market-watchers to question whether the stock market is in a bubble and if dotcom crash 2.0 might be coming. We don’t think so for several reasons. One is that spending is being done by such cash-rich companies with pre-existing business models generating massive cash flow.

Another thing that makes this cycle different from the late 1990s is that so little capital has gone into tangential businesses lacking a strong business case. Clearly, Pets.com, for example, didn’t have a strong enough business case to support its peak valuation, nor did so many other internet companies that came along and attracted so much capital after the infrastructure was built. This cycle surely has some AI infrastructure players with excessive valuations that won’t deliver great long-term returns, and some of the hundreds of billions being spent on AI will eventually prove wasteful in hindsight. But we would argue that the infrastructure phase carries less risk than the application phase, and the AI cycle probably has several more innings left before we get there.

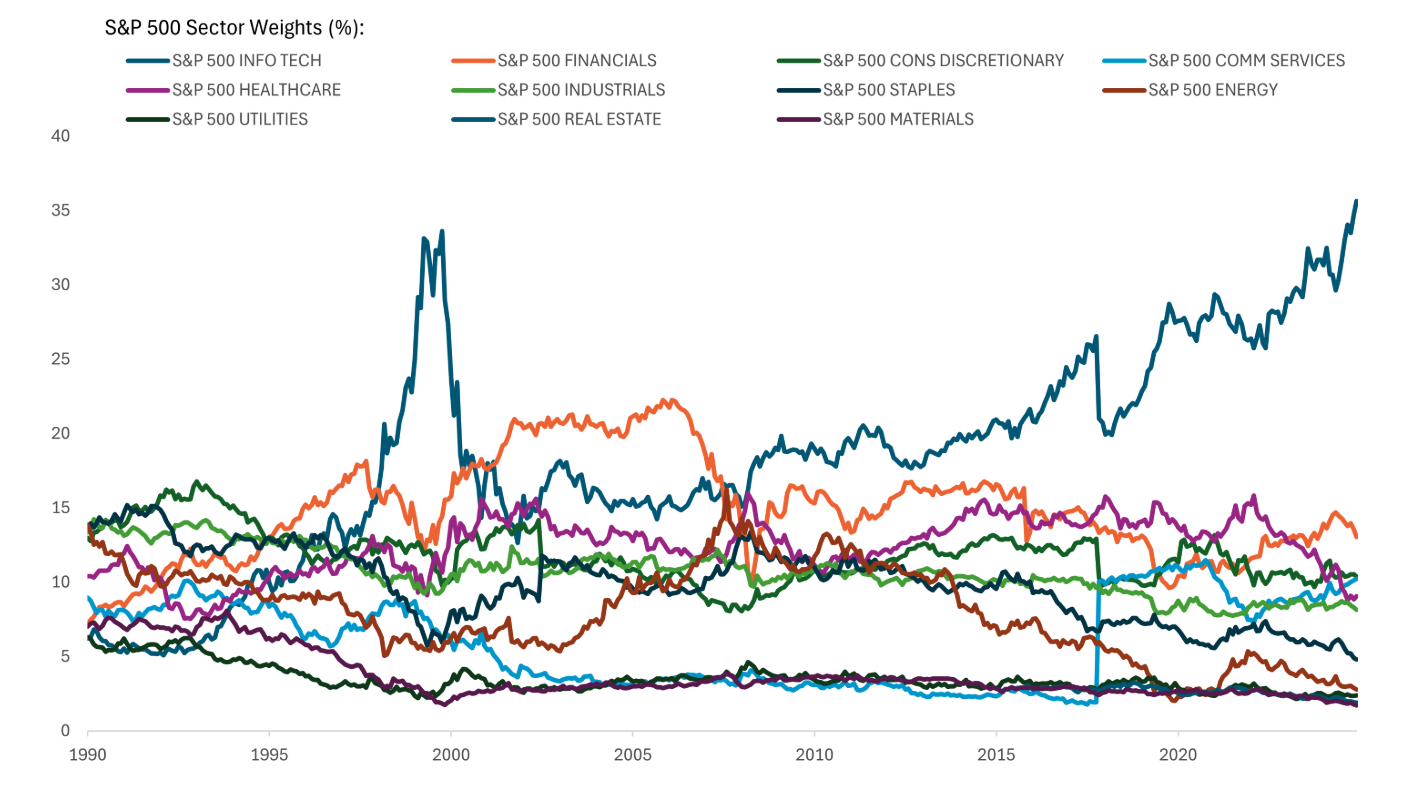

One striking similarity between this market environment and the late 1990s is that the weight in the S&P 500 technology sector, illustrated in the “Tech Record Sector Weighting Echoes Late 1990s” chart, just eclipsed its record high level from 25 years ago. This suggests the tech sector is overvalued, which it may be at a 34% premium to the forward price-to-earnings (P/E) ratio of the S&P 500. But consider the sector traded at double the S&P 500 valuation in March of 2000 at the peak of the dotcom bubble.

Finally, given strong fundamentals, including a 20% earnings growth rate that could be maintained through 2026 as capital investment in AI continues to ramp, and the best earnings revisions of all 11 S&P sectors over the last three and six months, we don’t think technology’s run is necessarily over.

Technology Sector Weight in the S&P 500 Reaches All-Time High

Source: LPL Research, Bloomberg 10/27/25Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

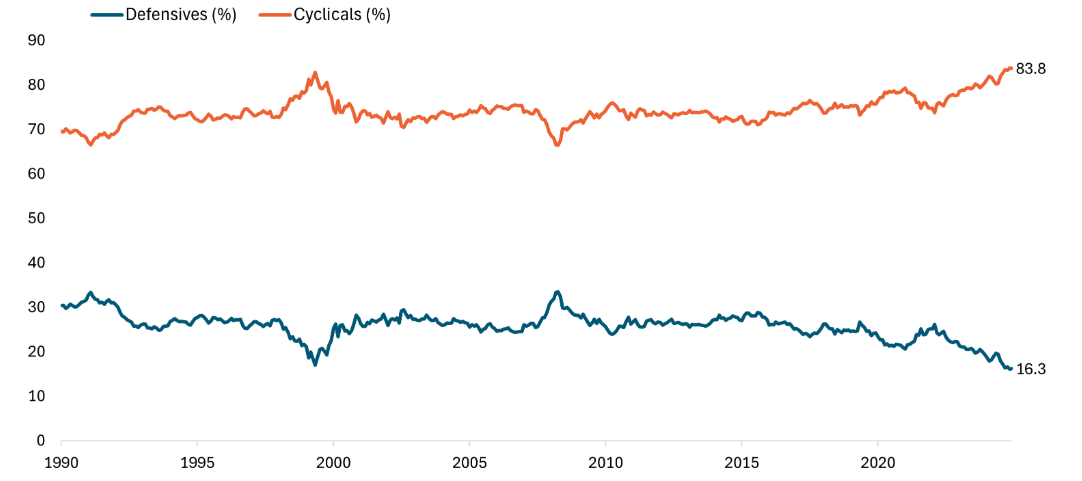

Another related and striking similarity between this market and the dotcom era is the small weight in defensive sectors. As shown in the “Record Low Exposure to Defensive Sectors” chart, the defensive sector allocation in the S&P 500 has fallen to an all-time low of 16.6% (since S&P GICS sector classifications began in 1990). For defensives, we include consumer staples, healthcare, and utilities. The previous all-time low came in March 2000, at the peak of the dotcom bubble, when defensive sectors composed 17.1% of the S&P 500. The common thread here is the technology sector, which sucked all the air out of the room. Remarkably, the index weight in technology bottomed out in December 1992 at 5.1% before starting its epic run that kicked into a higher gear when the Netscape browser came along in 1994.

The takeaway here is not that technology is in a bubble (we do not think it is), but rather that the equity market’s built-in hedge to help mitigate volatility is unusually small. That means investors must look elsewhere, e.g., alternative investments, select high-quality REITs and master limited partnerships (MLPs), precious metals, or high-quality bonds, for defensive exposure to balance the volatility profiles of their portfolios. This also means more stocks are at risk of being hurt by cyclical weakness, something to consider when the next recession arrives — though that may not be for a while.

Record Low Exposure to Defensive Sectors

Source: LPL Research, Bloomberg, 10/27/25

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Read more commentaries by LPL Financial