Fixed income securities have been buffeted this year by events including rising federal debt, a resumption of Federal Reserve rate cuts, a lack of data given the government shutdown, and some headline-grabbing corporate defaults. Fixed income investors wary of continued volatility have asked us many questions. Here we address a few of the currently most frequently asked questions (FAQs) about fixed income investments, including market conditions, credit quality and other issues that can affect debt securities.

1. Federal Reserve Chair Jerome Powell has said that the federal debt is "on an unsustainable path." What does that mean for the U.S. Treasury market?

An unsustainable path refers to a case when debt grows faster than the economy, and our debt and deficit data don't paint a rosy picture. The U.S. is running a deficit of 5.8% of gross domestic product (GDP) and our ratio of debt to GDP has hit 124%.

Historically there has been no correlation between the size of the deficit or its growth rate and bond yields. It's counterintuitive—because when deficits run large, the Treasury issues more bonds, increasing the supply. It would seem logical that yields would rise to attract buyers. However, that hasn't been the case in the past. With the U.S. dollar as the world's reserve currency, demand for U.S. Treasuries is quite strong and issuance has been absorbed without a discernible rise in yields. Moreover, the U.S. is a large economy and a wealthy country capable of servicing the debt.

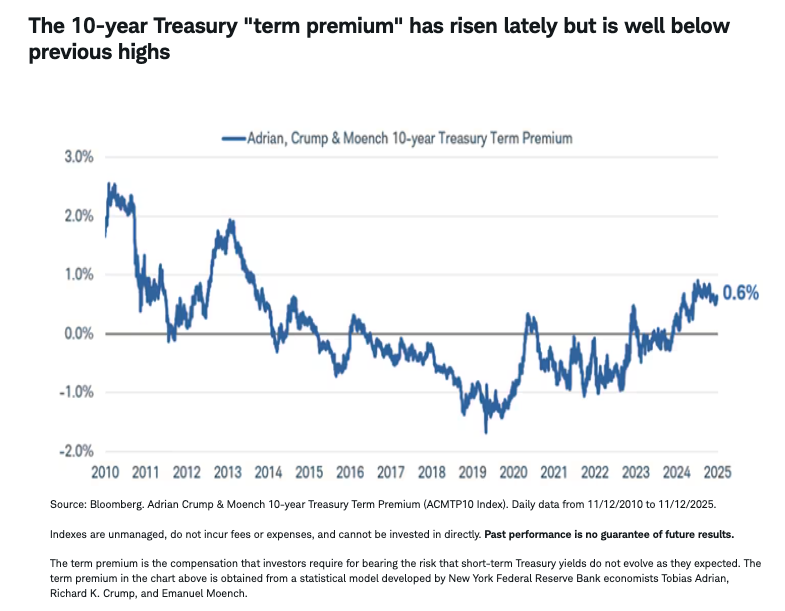

Nonetheless, we are concerned that the size of the debt load is reaching a point that might cause investors to pause—or demand more yield in order to invest in long-term Treasuries. The dysfunction in Washington and signals that Congress is not willing to address deficit spending could mean that demand for long-term Treasuries softens. The result would likely be a rise in the term premium—the extra yield that investors demand to hold long-term bonds versus a series of short-term bonds.

The term premium for 10-year Treasuries has been rising over the past few years after falling into negative territory in the years leading up to the pandemic. At about 60 basis points (or 0.60%) it is not as high as it was in the past. Consequently, it wouldn't be surprising to see 10-year Treasury yields rise due to an increase in the term premium, even if the Fed cuts short-term interest rates. All else being equal, a rising term premium could add 40-50 basis points to 10-year yields from current levels, as its average since 1990 is just over 100 basis points.

2. What is the outlook for the Federal Reserve?

We expect the Fed to keep the federal funds rate steady at the December meeting due to ongoing concerns about inflation and uncertainty about the economy due to lack of data. The fed funds futures market is discounting a significant drop in the fed funds rate into 2026, but we see a slower and shallower path for rates to move lower.

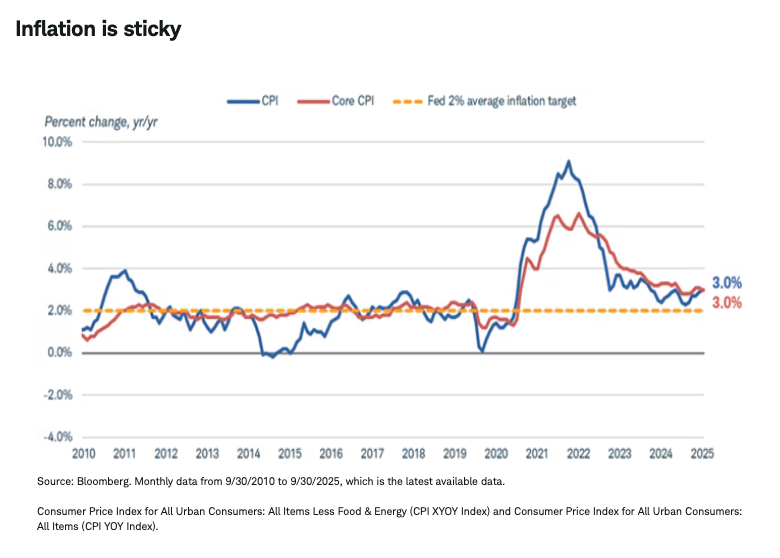

At the last Federal Reserve Open Market Committee (FOMC) meeting, Powell indicated that a rate cut in December was "far from certain." Since then at least four members of the committee have indicated that they are not on board with another rate cut this year due to concerns about inflation. Using the consumer price index (CPI) as a measure, inflation has been holding near 3% for several months and has recently started to move up.

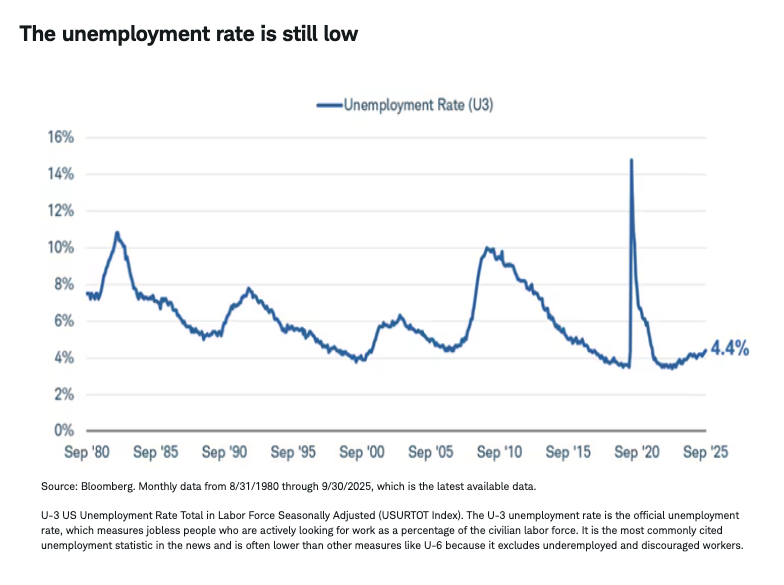

Meanwhile, the labor market has shown signs of softening with job growth slowing, which led to the Fed's recent rate cuts. However, the unemployment rate remains low at under 4.5%, which is still consistent with "full employment."

Lack of hard economic data due to the government shutdown from October 1st to November 12th is another reason for the Fed to move slowly on rate cuts. It will take a month or two for the labor market and inflation statistics to get updated. The data void could add to the Fed's caution. Moreover, the Fed has only a limited amount of room to cut rates until there is evidence that inflation is headed lower. The lower bound of the target range for the fed funds rate is 3.75% which is only 75 basis points above the current inflation rate. If the Fed moved quickly to slash short-term rates, it would risk pushing real short-term interest rates into negative territory, which would be stimulative.

As we look into 2026, we expect that growth and inflation will likely slow, allowing the Fed to cut rates modestly. However, the path is likely to be slow and cautious.

3. What's the outlook for the dollar?

Over time we expect the dollar to resume its decline. After falling more than 10% from its January 2025 high, the Bloomberg Dollar Spot Index has generally held in a tight range since July. That decline was likely driven by weaker U.S. growth prospects in light of the tariff announcements, but the recent resiliency of the U.S. economy appears to have stalled that decline.

The dollar often follows the path of U.S. interest rates. When U.S. yields rise relative to other government bond yields, the dollar tends to follow, and vice versa. The gap between the average yield of the Bloomberg US Aggregate Index and the Bloomberg Global Aggregate ex-USD Index has declined lately, and monetary policies appear to be diverging. The Federal Reserve lowered its benchmark interest rate again at its October meeting, and although the outlook around the timing and number of rate cuts is uncertain, it seems likely that the Fed will cut rates a couple more times over the next few quarters. The European Central Bank is likely done cutting rates for the time being, however, after lowering its policy rate by 200 basis points from June 2024 through June 2025. Meanwhile, the Bank of Japan has gradually raised rates after holding its policy rate below zero from 2016 through early 2024. As the Fed gradually cuts rates, interest differentials should continue to decline.

The dollar moves in many directions at once, depending on which exchange rate you're referencing, but the euro and the yen make up 42% of the Bloomberg Dollar Spot Index.

As the advantage that U.S. yields currently offer above other developed market bonds offer declines, the dollar looks likely to continue trending lower over the course of the next few quarters, and we expect volatility to remain elevated.

4. What's the outlook for the muni market?

Usually municipal bonds make sense only for fixed income investors in higher tax brackets but that's not the case today—they also can make sense in some lower tax brackets.

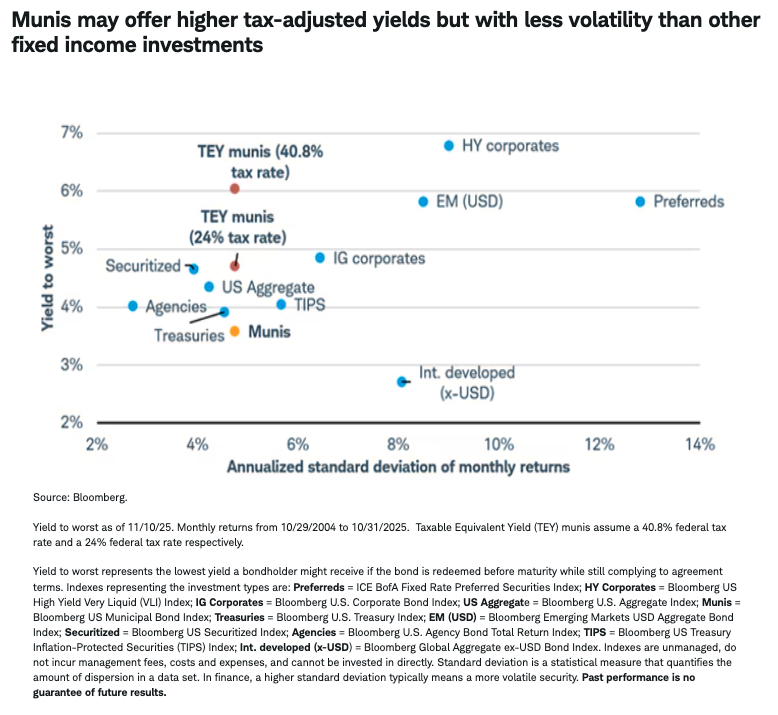

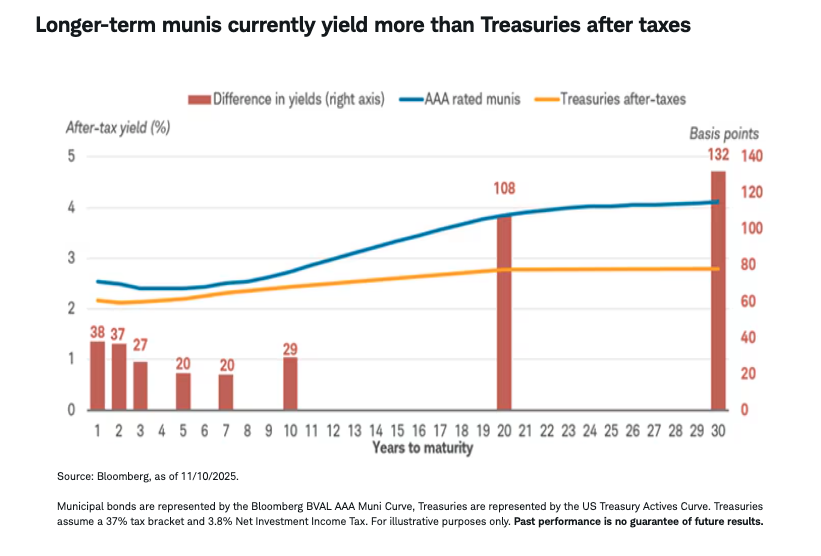

Munis offer an attractive combination of high tax-adjusted yields and strong credit quality in our view. Municipal bonds generally pay interest income that's exempt from federal and potentially state income taxes and partly as a result, their yields are usually less than most other fixed income investments. One method to compare municipal bond yields to other fixed income investments is to look at the tax-equivalent yield. This is essentially the yield on a muni if it were fully taxable. For an investor in the top federal tax bracket of 37% or even a moderate tax bracket of 24%, tax-equivalent yields are very comparable, and even higher, than many other fixed income investments. For example, the yield-to-worst for the Bloomberg Municipal Bond Index is currently about 3.6%. This is the equivalent of a 6% yield for an investor in the top tax bracket (37% plus a 3.8% Net Investment Income Tax) or 4.7% currently for an investor in the 24% tax bracket. Additionally, munis tend to be less volatile than other fixed income investments. Relative to their risk, as measured by standard deviation, we think munis stack up well against other fixed income investments.

Within the muni market, we believe there are opportunities with longer-term munis for investors who are comfortable with duration risk. As illustrated in the chart below, relative to Treasuries, the difference in yields is much higher for longer-term munis than shorter-term munis after adjusting for the impact of taxes. We don't believe that most investors should focus the bulk of their fixed income portfolio in longer-term munis because they are more sensitive to interest rates; if rates rise, prices of longer-term bonds will likely fall more than short-term bonds. However, given the differences in yields, we think they can be worth a second look.

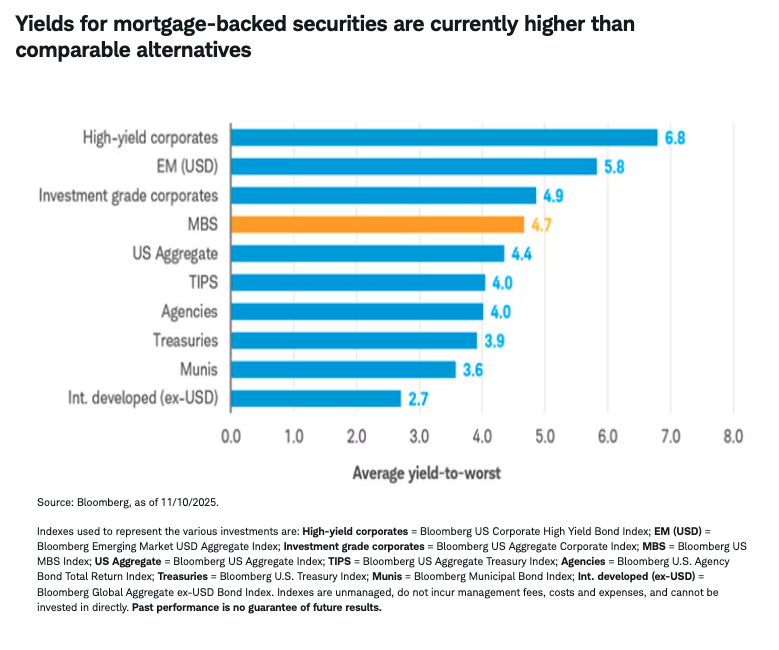

5. Should investors consider mortgage-backed securities?

We believe that mortgage-backed securities (MBS) can have a place as part of a diversified fixed income portfolio. Mortgage-backed securities are investments that are comprised of pools of mortgages. They generally make regular interest payments that are comprised of both principal and interest. As a result, the principal is slowly paid back to the investor. Like most other fixed income investments, they have a stated maturity date, but unlike most other fixed income investments, the principal is often paid off prior to that date in small increments rather than one lump sum. Partly because of this risk, they often pay a higher rate of interest than comparable investments of similar credit quality. For example, the average yield on an index of Treasury securities is 3.9% compared to 4.7% for an index of mortgage-backed securities.

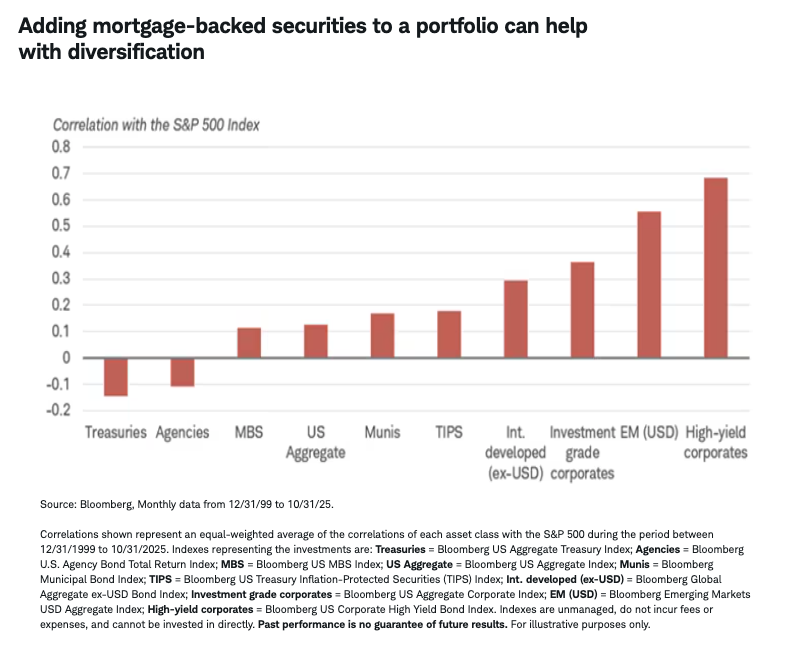

Beyond the potential for higher yields, mortgage-backed securities can also help diversify a portfolio. The correlation between mortgage-backed securities and riskier investments, like the S&P 500 in this example, is low. Correlation is a measure of how closely returns move together. A correlation of +1 means the two securities move perfectly with one another while a correlation of -1 means the two securities move in exactly the opposite direction. A lower correlation means greater diversification benefits.

Although mortgage-backed securities have potential benefits, they're not without risks. Two unique risks with MBS are prepayment risk and extension risk, or the risks that an investor will receive their principal payments earlier (prepayment) or later (extension) than expected. For example, if interest rates fall, mortgage-backed securities generally pay principal sooner than expected and the investor is faced with the prospect of investing the proceeds in a lower yielding environment. The opposite is true if rates rise. In this instance, generally mortgage-backed securities pay principal later than expected and investors miss out on the opportunity to invest in a higher yielding environment.

We believe that agency mortgage-backed securities should be considered as part of a fixed income portfolio's "core holdings." We generally suggest no more than 20% of the fixed income allocation be dedicated to mortgage-backed securities but that can vary based on investor preferences and risk tolerance. Additionally, investors may want to consider using a fund, like a mutual fund or ETF, because reinvesting principal and interest payments with individual mortgage-backed securities can be difficult. You should consult the fund's prospectus to understand its investment objectives, risks, charges, and expenses.

6. Should I be concerned about some of the recent headline-grabbing corporate bankruptcies?

Corporate bond risks appear to have risen lately, but we don't think the recent bankruptcies necessarily pose a systemic risk to the financial markets.

Corporate defaults had already begun to pick up a few years ago after the Federal Reserve aggressively raised interest rates, boosting the borrowing costs for many issuers. A bond default is when an issuer fails to meet its contractual obligations to its bondholders, for example, by failing to make an interest payment or repaying a debt at maturity. We think the default rate may remain somewhat elevated, but here are two key factors that may prevent them from surging higher: credit quality and relatively supportive corporate fundamentals.

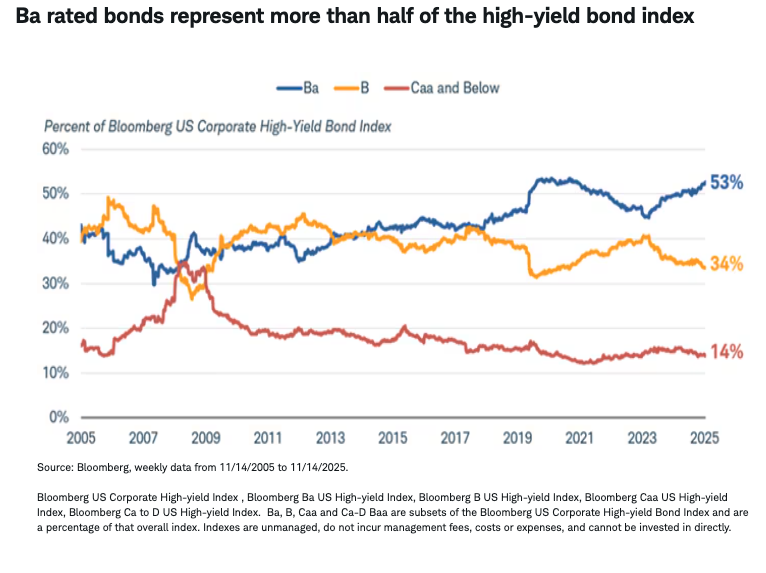

Not all high-yield bonds (or "junk" bonds) are equal, with those rated Caa or below1 generally having the greatest risk of default. Bonds with those ratings make up a relatively small share of the Bloomberg US Corporate High-Yield Bond Index, with the share of Ba rated bonds near its 20-year high.

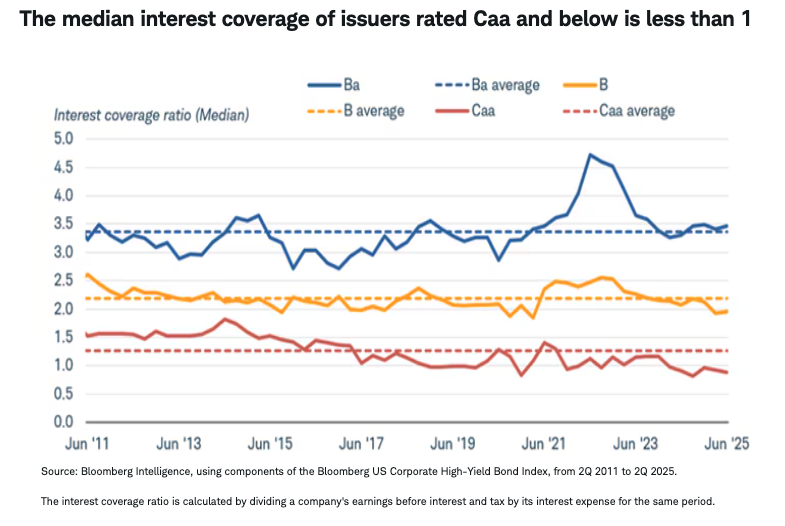

Corporate fundamentals are mostly strong, except for the lowest rated issuers. And those issues represent a small share of the market, as the chart above highlights. A key metric for corporations is the interest coverage ratio—the ratio of a company's annual earnings (usually earnings before interest and taxes) to its annual interest expense. It's also called the "times interest earned." For Ba rated issuers in the Bloomberg US Corporate High-Yield Bond Index, the interest coverage ratio of 3.5 is above its 15-year average. The ratio for Caa issuers is a bit more troubling—a ratio of 0.9 means that the median Caa rated issuer is not generating enough annual earnings to pay its annual interest expense. This suggests that some lower-rated issuers may continue to default, but their low share of the market may prevent the overall default from surging much higher.

Even if the default rate doesn't surge much higher, our outlook for high-yield bonds is neutral with a touch of caution. For high-yield bond investors, what matters is how much extra yield they can expect in exchange for the potentially heightened credit risk, and today that extra yield is very low.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The securities and investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

Preferred securities are a type of hybrid investment that share characteristics of both stock and bonds. They are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features, and the timing of a call, may affect the security's yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so their prices may fall during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation. Treasury Inflation-Protected Securities are guaranteed by the US Government, but inflation-protected bond funds do not provide such a guarantee.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes than other fixed income investments.

This information is not a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager, Estate Attorney) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Currency trading is speculative, volatile and not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

© Charles Schwab

Read more commentaries by Charles Schwab