A new year can bring a renewed focus for a financial advisor who decided to take the leap of faith into starting their own independent practice. After all the initial groundwork has been completed to get the practice started, it's now time to be productive and build the business. Of course, this is much easier said than done.

Financial advisors transitioning from working for an employer to starting their own practice will ultimately need to increase their productivity levels. This is vital, as independents advisors need to build a sustainable business that's capable of attracting as well as retaining clients in a competitive financial services marketplace. Not only are they competing with other independent financial advisors, but also the very firms they left to go solo.

On top of day-to-day operations, independent advisors also need to complete tasks beyond their typical work scope, such as building their brand, creating budgets, and other administrative tasks they weren't accustomed to handling as an employee of another firm. With that said, here are three ways advisors can be more productive in the new year.

Embrace Artificial Intelligence (AI)

It was difficult to get away from artificial intelligence in 2025, but AI is more than just a trendy investment theme. Independent advisors can actually add AI into their practices to foster automation that could help streamline their business operations.

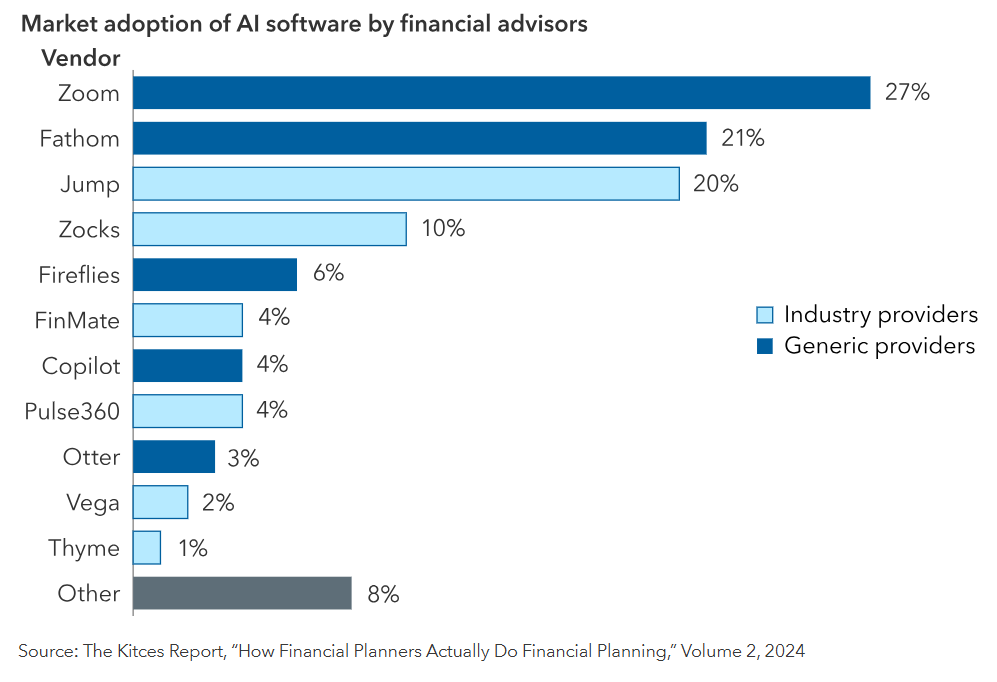

Advisors can leverage the capabilities of AI platforms to help with generating reports, creating meeting transcriptions, performing research, and other tasks. Note-taking in particular is an important task, especially when it comes to client meetings where advisors can extrapolate valuable information to create tailored financial plans that suit their clients. A 2024 survey from The Kitces Report revealed some of the applications most widely used by financial advisors for note-taking.

Ultimately, using tools like notetakers can help advisors reduce time spent on time-consuming administrative tasks. The time saved could be used for advisors to focus on activities related to revenue generation and more importantly, deepening client relationships through expert financial planning and personal engagement.

"Successful application of AI depends on tuning out the hype and staying focused on solving real-world problems for clients and your business," Capital Group said in an article identifying different ways advisors can use AI.

Have a Niche Client Focus

An independent financial advisor can't be everything to everyone. While a large firm can handle a heavy client load with a workforce flush with advising talent, an independent firm should have a niche focus and thus, a targeted marketing plan. This allows an advisor to focus on the clients within their niche area rather than chasing every possible lead — thereby enhancing productivity and laser-focusing on the clients that matter.

"While it might seem advantageous to appeal to everyone, advisors who specialize in the needs of specific audiences can build more effective marketing efforts," noted Gordy Abel, the chief marketing officer at Dynasty Financial Partners, who gave reasons as to why independent advisors should have a niche focus.

In addition to efficient productivity, focusing on a niche will open up opportunities for advisors to become an authority figure for their specific client base. This will also help create a pathway for referrals from other advisors who aren't privy to a specific type of client.

"When you focus on a specific niche, whether it’s veterans from a certain branch of the military, small business owners within a category like real estate, or senior healthcare professionals at local hospitals, you have the opportunity to tailor your planning approach to address the distinct financial concerns that matter most to them," Abel added.

Build a Support Team

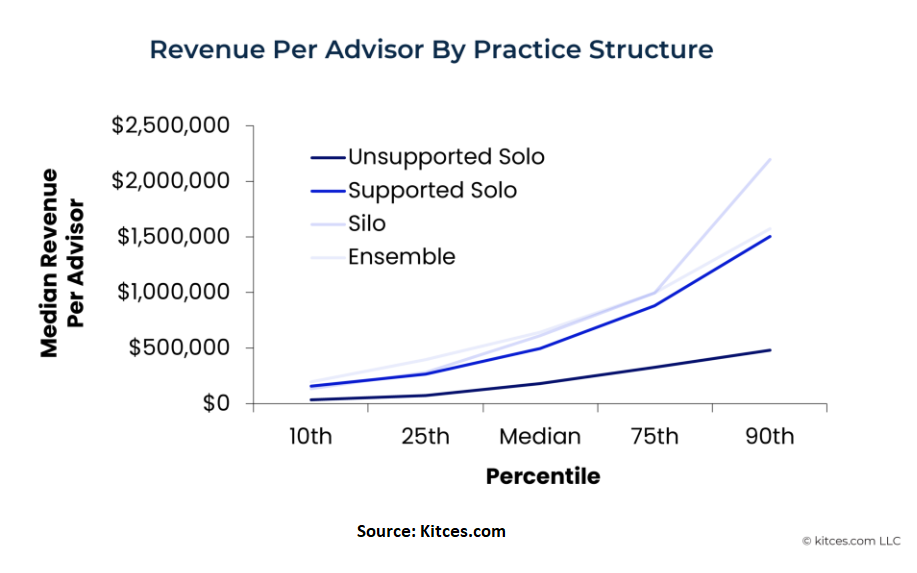

While technology such as AI can be beneficial, building the right support team is imperative. Kitces research data noted that this is one of the most important ways to enhance productivity, as it serves as the foundation for other productivity drivers they identified.

As mentioned, newly minted independent advisors should maintain their focus on tasks such as client-facing work that drives revenue generation, while delegating tasks beyond their expertise. This includes billing, creating budgets, developing market plans, handling compliance, and other tasks.

And how does hiring a support team translate into increased revenue? Kitces research data also shows that independent practices with a support team "to leverage and support them is preferable to having no team at all–even a single CSA supporting a solo advisor makes a meaningful difference!"

"The gap between unsupported solo advisors and everyone else is astounding," Kitces.com noted further, highlighting the revenue gap between unsupported and supported practices in the graph below. "While the median unsupported solo advisor brings in $182,500 in revenue, this is $317,500 (or 64%) less than the $500,000+ median for supported solo advisors."

These are just a few of the many ways advisors can tackle the new year in an efficient, productive manner.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by VettaFi | Advisor Perspectives