With 2025 behind us, it’s a good time to celebrate some of our better forecasts from last year while also reviewing some misses we can learn from. In our view, we got more right than wrong last year, but there were some misses among our tactical asset allocation recommendations. For the second straight year, as the bull market marched on, the most impactful decision we made was probably to recommend investors stay fully invested in equities at benchmark levels throughout the entire year despite elevated valuations.

Equities Predictions in 2025: Hits and Misses

Staying Fully Invested — Hit. Perhaps our most important tactical recommendation last year was to remain neutral equities. While staying neutral all year may seem like a miss in such a strong year, and of course, an overweight would’ve been better, a downgrade was tempting given the volatility last spring around tariffs. So, we’ll call maintaining full equity allocations a win. Tariffs weren’t the only concern, with market concentration, excessively bullish sentiment, high valuations, deficits, and inflation among the many concerns cited by the bears. The Russell 3000 returned 17.1% in 2025.

Despite widespread concerns about market concentration when 2025 began, with massive market caps of mega cap tech stocks, staying fully invested in U.S. equity markets was the correct call last year. Not only that, but Bloomberg’s Magnificent Seven Index returned 26.8% for the year, led by Alphabet’s (GOOG/L) 66% surge, strongly outperforming the market cap weighted S&P 500 (+17.9%) and its equal weighted counterpart (+11.4%).

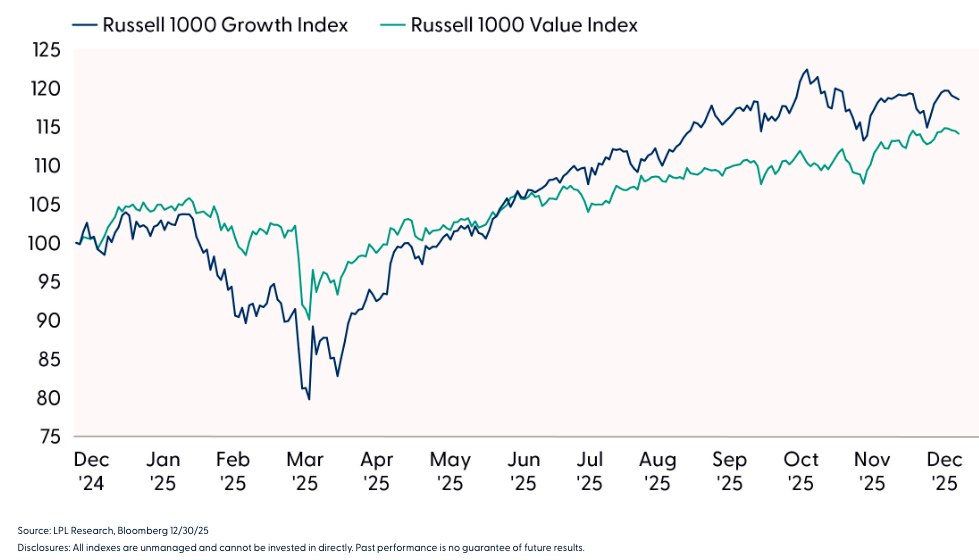

Large Growth Over Small and Mid Value — Hit. Continuing with the mega cap theme, our Strategic and Tactical Asset Allocation Committee (STAAC) maintained its preference for growth over value throughout all of 2025, with a large cap growth overweight and small and mid cap value underweight. The growth style paced large caps, with the Russell 1000 Growth Index outperforming its Value counterpart by 2.7% (18.6% to 15.9%) for the year. Meanwhile, small and mid cap value, measured by the Russell 2500 Value Index, underperformed large value and large growth with just a 12.7% return.

With prevalent calls for a rotation into value stocks throughout 2025, given significant optimism priced into stocks tied to the artificial intelligence (AI) theme, our focus on earnings and emphasis on technical analysis kept us in the growth trade throughout 2025 (as it did in 2024). Our expectations that the economy would slow down and confidence in growth stock earnings underpinned our preference for large caps over small last year.

Large Growth Outpaced Large Value in 2025

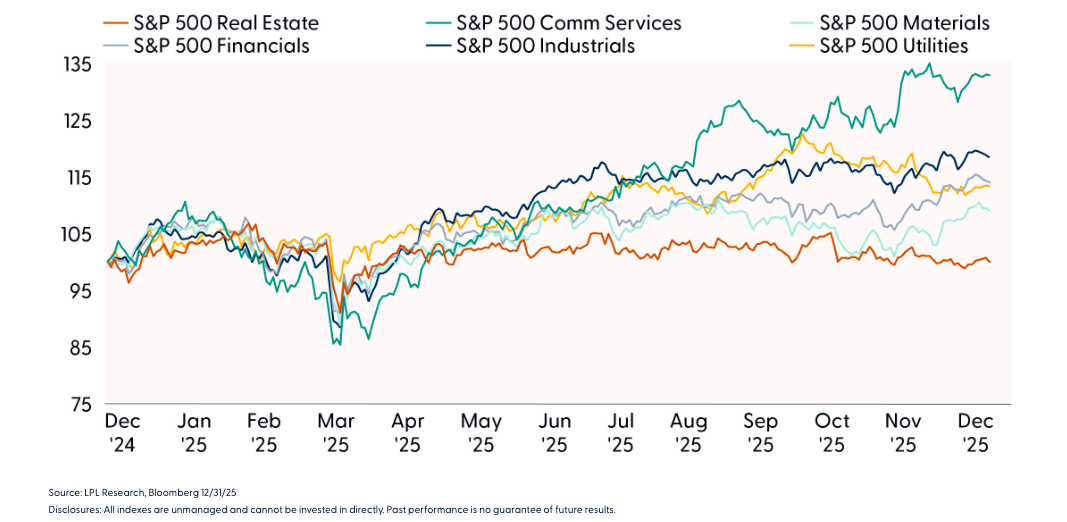

Overweighting Communication Services All Year — Big Hit. The only sector call we maintained throughout all of 2025 was a good one — overweighting communication (comm) services. The top-performing sector in 2025 for the second straight year (after gaining 55.8% to finish slightly behind tech in 2023), comm services returned 33.6% in 2025, more than 15% ahead of the S&P 500, and more than 9% ahead of the second-best sector, technology (+24.0%). A more reasonably valued play on AI with significant digital media exposure, the sector is tracking toward 19% earnings growth for 2025, and trades at a 17% discount to the technology sector. LPL’s STAAC maintained this recommendation as 2026 began.

Negative Real Estate Most of the Year — Hit. We started 2025 recommending an underweight to the real estate sector due mostly to our preference for more cyclical sectors with stronger earnings growth. We then turned neutral midyear before putting the underweight back on in November. Real estate slightly underperformed during both periods. STAAC maintained its underweight recommendation as 2026 began.

Positive on Industrials in the First Half — Hit. Industrials outperformed during the first half of the year, justifying our overweight that was based on infrastructure and defense spending, AI data center buildouts, and near-shoring. Taking the recommendation off midyear did not come with an opportunity cost because the sector underperformed in the second half. Industrials, still a neutral sector, is on our shopping list of potential opportunities for 2026.

Negative on Energy in the First Half — Hit. A global supply overhang dragged oil prices down and contributed to energy sector underperformance in the first half of 2025. The sector underperformed in the second half as well, so there was no opportunity cost for removing the underweight and going to neutral midyear. STAAC maintained its neutral stance as 2026 began.

Positive Financials Midyear — Miss. There were several reasons to like financials in 2025, including a normalizing yield curve, strength in capital markets, healthy credit markets, deregulation, and limited tariff risk. But our timing was off as the sector outperformed during the first half of the year, while we were neutral, and in the last two months of the year, when we were neutral again. STAAC maintained its neutral stance as 2026 began.

Negative Utilities Midyear — Miss. Our underweight recommendation on utilities from midyear until November was a miss as the sector outperformed during this time. We underestimated the benefit from AI power demand. STAAC maintained its neutral stance as 2026 began.

Communication Services Displayed Compelling Performance in 2025

Last, while not highlighted in the accompanying chart, technology and healthcare were two of the best-performing sectors last year and were rated neutral throughout 2025. So, while these asset allocation decisions did not necessarily detract from performance, they represent missed opportunities.

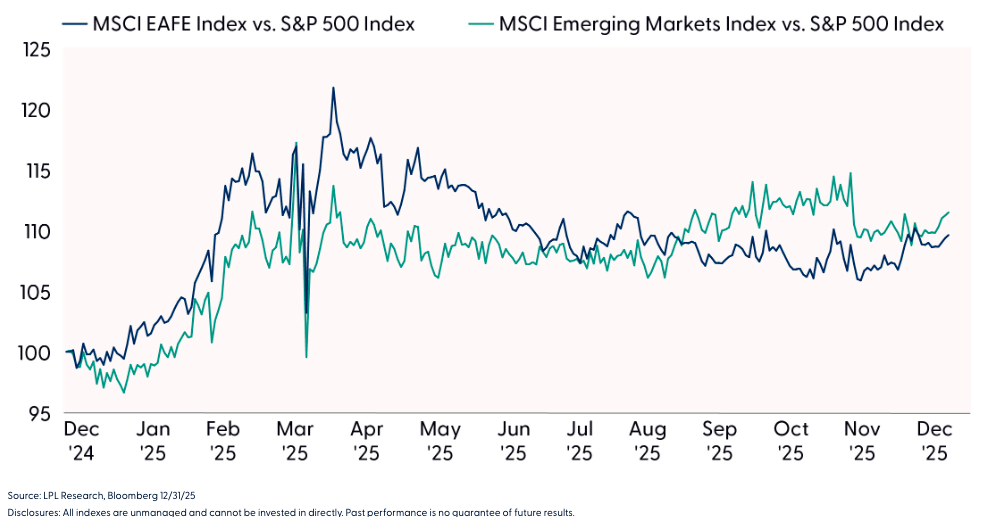

Favoring U.S. Over EM Early in 2025 — Miss. In perhaps our biggest miss of 2025, emerging market (EM) equities dramatically outperformed the S&P 500 during the first four months of 2025, a period when LPL Research recommended an underweight position. The STAAC’s cautious stance was driven primarily by U.S.-China trade tensions ahead of the Trump administration’s tariff announcements, but a weaker dollar, AI, and watered-down tariffs proved to be powerful drivers of EM stock performance. EM outperformed U.S. equities before and after our May upgrade, and the MSCI EM Index ended the year with an impressive 34.3% return, boosted by a 9% drop in the U.S. dollar based on the DXY U.S. Dollar Index. STAAC’s EM equity stance remained neutral as 2026 began.

EM and Developed International Equities Strongly Outperformed the U.S. in Early 2025

S&P 500 Fair Value Target — Miss. For the third straight year, all years of double-digit gains for the S&P 500, LPL Research’s year-end fair value target was too low. After starting the year with a range of 6,275 to 6,375, and a bull case of 6,700, tariff threats (so-called “Liberation Day”) sent the index down below 5,000 on April 8. Due to heightened tariff uncertainty and significant risk to earnings, on April 21 we lowered our year-end fair value target range to 5,650 to 5,800 — allowing for 10% upside at the time (as noted in our April 21 Weekly Market Commentary).

Then in early July, in LPL Research’s 2025 Midyear Outlook: Pragmatic Optimism, Measured Expectations, we raised our target to a range of 6,000 to 6,100, with a bull case scenario of 6,450. Not high enough, as the S&P 500 ended 2025 at 6,845, 1.2% below its record closing high on December 24.

Tariff uncertainty was the biggest challenge, while we also underestimated the earnings boost from AI. Our initial 2026 S&P 500 EPS forecast of $275, published in December 2024, along with our bull case scenario of $280, was raised to $290 last month in Outlook 2026: The Policy Engine.

We will give ourselves some credit for assigning a 23 forward price-to-earnings ratio (P/E) at the start of last year despite widespread calls from strategists for multiple compression.

Fixed Income Predictions: Hits and Misses

10-Year Treasury Yield Forecast — Hit. Several of our key calls in 2025 proved accurate. We anticipated that, despite the Federal Reserve (Fed) cutting rates, the 10-year Treasury yield would generally remain between 4% and 4.5%. That forecast mostly held true, with the 10-year trading between 4.79% and 3.95% before ending the year at 4.17%. The rangebound environment, as we noted in our 2025 Midyear Outlook, reflected a tug-of-war between easing monetary policy and ongoing concerns about U.S debt and deficits. As such, we expected the Treasury curve to steepen with short-maturity Treasury yields falling but longer-maturity yields remaining elevated, largely due to the return of the Treasury term premium, which is what happened.

The Treasury term premium represents the additional compensation investors demand to own longer maturity securities. After years of negative term premiums, investors finally received some compensation for holding longer maturities — though still below historical norms. Outside of a recession (not our base case), we think this dynamic holds, or potentially increases in 2026, which suggests a neutral duration to benchmarks is still prudent (a position we held in 2025 as well).

Return of the Treasury Term Premium

MBS Over Corporates — Hit. Another correct call was favoring mortgage-backed securities (MBS) over investment-grade corporate bonds. MBS returned over 8.5%, outperforming corporates at 7.77%. This was partly due to reduced MBS supply given ongoing housing affordability issues and relatively attractive spreads compared to corporates, which remained expensive throughout the year. Spreads for both asset classes are currently below historical averages, so while we think MBS can continue to outperform in 2026, our conviction level is lower this year.

Treasuries Remained a Safe Haven — Hit. Finally, we also pushed back against the narrative that U.S. exceptionalism was fading and that Treasury securities were losing their safe-haven status. In reality, U.S. fixed income markets outperformed most developed non-U.S. markets, with the Bloomberg Treasury Index marking its best year since 2020 — a year that saw Treasury yields fall due to a global pandemic. Moreover, inflation expectations stayed anchored, allowing the Fed to cut rates without sparking instability. This stability reinforced the resilience of U.S. bonds in global portfolios.

Avoiding EM Debt — Miss. Our biggest fixed income miss in 2025 was not allocating to emerging market debt (EMD). Our models flagged EMD as attractive, and we even brought in an outside EM expert to present to our Strategic and Tactical Asset Allocation Committee, but we hesitated due to the broad range of idiosyncratic risks of an index spanning nearly 70 different countries. We couldn’t get comfortable with that level of dispersion, as each country carries unique political and economic challenges. While caution is often prudent, in this case, it meant missing an opportunity for diversification and higher returns.

Economic Forecasts: Hits and Misses

Tariffs Do Not Automatically Translate Into Higher Inflation — Hit. As we stated in our November 18 Weekly Market Commentary and our November 13 LPL Research blog, several major factors would limit the broader inflationary impact from tariffs. China was weaker in 2025 than during President Trump’s first term; businesses do not always pass along higher input costs, post-pandemic trade realignments, and the likelihood of tariff exclusions would limit the inflationary impact. Perhaps giving markets something to cheer about, the core Personal Consumption Expenditures (PCE) price index was 2.8% in September, down from 3.0% in December of last year.

Fed Would Cut Several Times in 2025 — Hit. Despite some stronger job reports in early 2025, we believed the Fed would initiate rate cuts during 2025. The fed funds futures market was highly volatile in the first part of the year as inflation and labor markets did not support any easing of monetary policy, but we maintained the view that inflation was trending downward and labor markets were softer than some of the initial prints suggested. After the Bureau of Labor Statistics revealed its preliminary estimates of the upcoming benchmark revisions, our views were validated that a soft labor market allowed Fed officials to ease policy in 2025.

Growth Would Decelerate Later in the Year — Miss. Trade policy, seasonal factors, and a government shutdown all contributed to a messy economic backdrop. We anticipated economic growth would slow by the end of the year, but in actuality, the first quarter was the weakest, as the economy contracted by -0.6%. The fourth quarter report will be published on January 22 and will likely show weakness from the lapse in government appropriations. The average quarterly growth rate in personal spending over the first three quarters of 2025 was 0.54%, down from 0.83% the previous year. Despite a slowdown in consumer spending, business spending supported economic growth more than anticipated.

Conclusion

There you have it, our hits and misses from 2025. We’re pleased to report more hits than misses last year and we’re hard at work trying to deliver more of the same in 2026. On behalf of the entire LPL Research team, thank you for your trust in us as your investment partner and your interest in our content.

Asset Allocation Insights

LPL’s STAAC maintains its tactical neutral stance on equities as 2026 begins. Investors may be well served by bracing for occasional bouts of volatility given how much optimism is reflected in stock valuations, but fundamentals remain broadly supportive. Technically, the broad market’s long-term uptrend remains intact, leaving the Committee biased to buy potential dips that emerge.

STAAC’s regional preferences across the U.S., developed international, and EM are aligned with benchmarks. The Committee still favors the growth style over its value counterpart, large caps over small caps, and the communication services sector. The Committee is closely monitoring the healthcare, industrials, and technology sectors for opportunities to potentially add exposure on weakness.

Within fixed income, the STAAC holds a neutral weight in core bonds, with a slight preference for MBS over investment-grade corporates. The Committee believes the risk-reward for core bond sectors (U.S. Treasury, agency MBS, investment-grade corporates) is more attractive than plus sectors. The Committee does not believe adding duration (interest rate sensitivity) at current levels is attractive and remains neutral relative to benchmarks.

Jeffrey Buchbinder, Chief Equity Strategist, LPL Financial

Lawrence Gillum, Chief Fixed Income Strategist, LPL Financial

Jeffrey J. Roach, Chief Economist, LPL Financial

You may also be interested in:

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

The information presented is for educational and informational purposes only and is not intended as a recommendation or specific advice. Cryptocurrency and cryptocurrency-related products can be volatile, are highly speculative and involve significant risks including: liquidity, pricing, regulatory, cybersecurity risk, and loss of principal. A cryptocurrency fund may trade at a significant premium to Net Asset Value (NAV). Cryptocurrencies are not legal tender and are not government backed. Cryptocurrencies are non-traditional investments, resulting in a different tax treatment than currency. Federal, state or foreign governments may restrict the use and exchange of cryptocurrency. The use and exchange of cryptocurrency may also be restricted or halted permanently as regulatory developments continue, and regulations are subject to change at any time. Cryptocurrency exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers, malware, or bankruptcy.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

High yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

The Russell 1000 Index consists of the 1,000 largest securities in the Russell 3000 Index, which represents approximately 90% of the total market capitalization of the Russell 3000 Index. It is a large-cap, market-oriented index and is highly correlated with the S&P 500 Index.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Established in 1984, the Russell 3000 index measures the performance of the largest 3,000 U.S. companies representing approximately 96% of the investable U.S. equity market.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following developed country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

The MSCI EM (Emerging Markets) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the emerging market countries of the Americas, Europe, the Middle East, Africa and Asia. The MSCI EM Index consists of the following emerging market country indices: Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Egypt, Greece, Hungary, Poland, Qatar, Russia, South Africa. Turkey, United Arab Emirates, China, India, Indonesia, Korea, Malaysia, Philippines, Taiwan, and Thailand.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

Read more commentaries by LPL Financial