Municipal bonds enter 2026 as a compelling option for investors: attractive yields, strong fundamentals, and structural changes that continue to reshape the market. After a volatile 2025, marked by Treasury market dislocations and record muni issuance, the outlook for this year suggests more stability — and opportunity.

Return Expectations

We think a 4%-5% return is a reasonable return expectation for the national municipal market in 2026, supported by a stable Treasury rate environment and attractive tax-equivalent yields. While last year’s returns fell slightly short of the 5% target, current valuations and curve dynamics make a repeat performance plausible.

Supply and Demand Dynamics

Issuance remains a key theme. After hitting $600 billion in 2025, supply is projected to stay near record levels again this year. Drivers include infrastructure financing, refunding activity, and capital projects — plus ripple effects from the artificial intelligence-driven data center boom. These facilities consume vast water resources, prompting municipalities to invest heavily in water and sewer infrastructure, estimated at $1.2 trillion over 20 years.

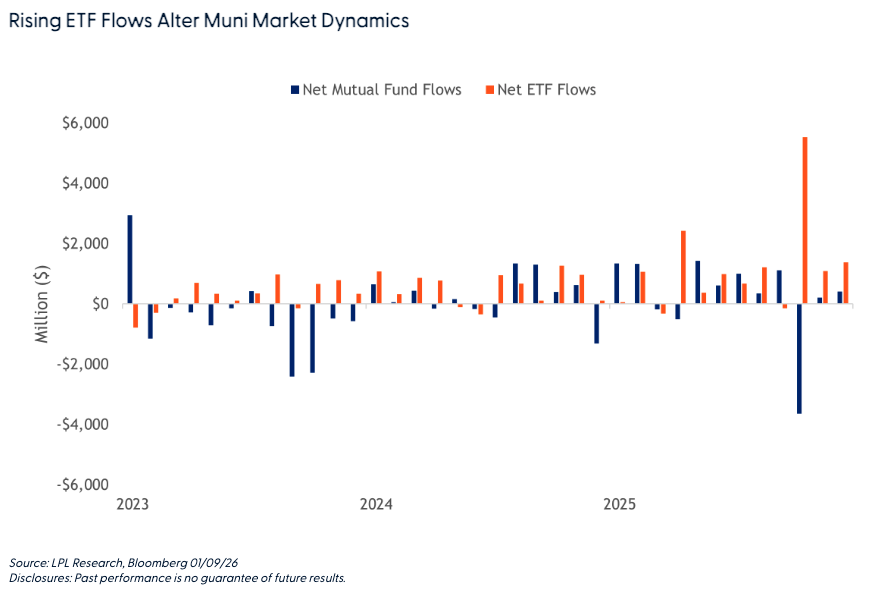

Despite heavy supply, demand has proven resilient. ETFs absorbed nearly $40 billion in flows last year, outpacing mutual funds and signaling a structural shift toward more liquid, transparent investment vehicles. Historically, mutual funds were the dominant vehicle for municipal bond investment. But that changed last year and is expected to continue to change in 2026. The number of municipal mutual funds has fallen below 500, while ETF offerings have surged. This migration introduces greater intraday liquidity and price transparency, but it also alters demand dynamics — particularly for bonds beyond 20-year maturities.

ETFs typically concentrate on shorter and intermediate maturities, leaving the longest tenors dependent on a shrinking pool of mutual funds. As a result, long-duration muni yields may remain elevated, even as shorter maturity yields fall. For investors, this means intermediate maturities (10–20 years) look compelling, offering strong carry and roll-down potential.

Curve Opportunities

The muni curve steepened significantly in 2025, making intermediate maturities (10–20 years) particularly attractive. Investors willing to extend duration selectively can capture additional carry and roll-down potential, enhancing total returns.

Fundamentals Remain Strong

Municipal credit quality looks solid. Tax revenues hit a record $2.1 trillion, and public pension funding has improved dramatically, with nearly half of plans at or near full funding. These factors reduce downgrade risks and support market stability.

Investor Takeaways

Valuations remain compelling, especially versus investment-grade corporates. For investors in higher tax brackets, munis may offer compelling after-tax yields. While supply pressures persist, strong demand and healthy fundamentals suggest another year of positive returns (no guarantees of course).

Bottom Line: Attractive yields, a steep curve, and robust credit fundamentals position municipal bonds as a strong candidate for portfolios in 2026. Expect structural shifts — like ETF growth — to continue shaping the market, but the math still favors munis in our view.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #848695

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial