The Bond Market in 2026: What Could Go Wrong?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- We expect another generally good year for bonds in 2026, although returns might not be as robust as they were last year.

- We expect the yield curve to continue to steepen with only one or two more rate cuts this year by the Federal Reserve.

- Starting yields are lower and we see less room for bond yields to fall (and bond prices to rise) as an expected resilient economy likely will limit the scope for Fed rate cuts.

- Risks to our outlook include inflation surprises (to the upside or downside), a weaker-than-expected economy, changes at the Federal Reserve and geopolitical events.

- Our "base case" calls for steady economic growth and persistent inflation, but it's always important to consider alternative scenarios and how they may impact investments.

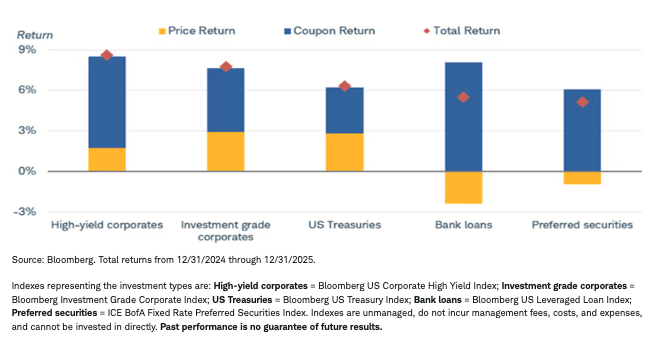

It was a good year for most bond investments in 2025. High starting yields, price appreciation for high-quality bonds, and a downtrend in yields led by Federal Reserve rate cuts combined to produce strong returns.

Coupon income was the key driver of total returns for many bond

investments in 2025

We expect another good year in 2026, although returns might not be as robust as they were last year. Starting yields are lower, and we see less room for yields to fall (and prices to rise) as an expected resilient economy likely will limit the scope for Fed rate cuts.

We expect the yield curve to continue to steepen. The Federal Reserve lowered interest rates three times in 2025 but is expected to cut only one or two more times this year. That should pull short- and intermediate-term Treasury yields lower, but the 10-year Treasury yield should hold near 4% given sticky inflation, an expected increase in Treasury supply to finance federal deficits and rising global bond yields.

But even the best-laid plans can go awry when circumstances change. The year has already started off with a bout of volatility and there are plenty of potential catalysts for more. Consequently, we have compiled a list of what could go wrong and what it would mean for bond markets.

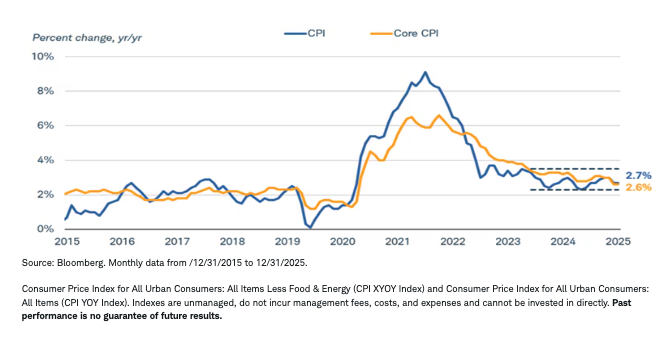

1. Upside or downside surprises to inflation. After peaking in 2022, inflation has been trending lower, but the downward progress has stalled a bit lately. The 12-month change in the headline Consumer Price Index (CPI) has held between 2.3% and 3.5% since the beginning of 2024; the 12-month change in core CPI, which excludes volatile food and energy prices, held at 2.6% in December after moderating in November, but prior to that had held between 2.8% and 3.4% for 17 straight months.

Inflation has generally held in a range since coming off the 2022 peak

We expect inflation to remain a bit sticky, holding above the Fed's 2% target, for the near term given the resilient economy, but there appear to be both risks to the upside and the downside.

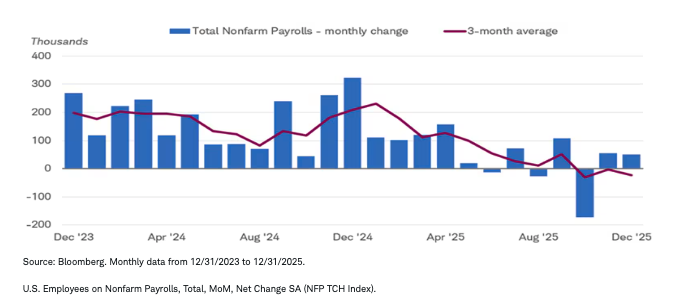

A significant weakening of the labor market could pull inflation lower if it slows down consumer spending. The labor market picture has been a bit mixed lately, with the December unemployment rate falling to 4.4% to reverse some of the recent rise, but job growth remains tepid. On a three-month-average basis, nonfarm payroll gains have been negative since October. Lower inflation could result in more rate cuts, a flatter yield curve, and more potential price appreciation for Treasuries.

Nonfarm payroll gains have slowed

There are risks to the upside as well. Fed easing has kept financial conditions easy, and fiscal stimulus from last year's "One Big Beautiful Bill Act" could support a pickup in consumer spending. Tariffs appear here to stay, even if the outlook for the legality of the International Emergency Economic Powers Act (IEEPA) is uncertain. While tariffs haven't necessarily driven headline inflation rates much higher, they have generally lifted the prices of imported consumer goods by varying degrees.

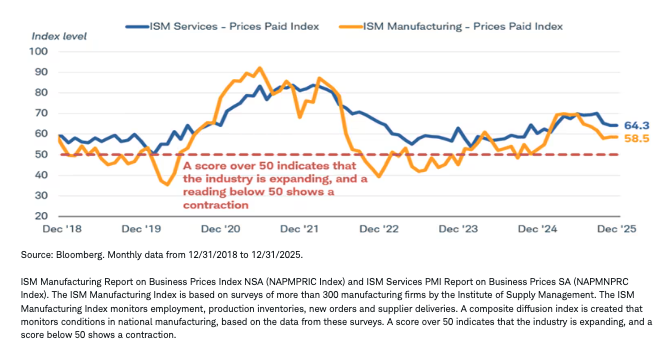

Meanwhile, consumer and business surveys suggest that price increases are still a concern. The prices-paid components in both the Institute for Supply Management (ISM) Manufacturing and Services surveys highlight this risk, as both indexes have increased from the recent lows. Treasury yields would likely rise if inflation were to reaccelerate, with long-term Treasury prices falling the most given their high interest-rate risk.

The prices paid indexes from the ISM Manufacturing and Services Surveys

are both above their lows of the last few years

2. A weaker economy. The recession that many feared when the Fed aggressively hiked rates in 2022-2023 never arrived, but risks are still present. Despite the strong headline growth, it's generally a bifurcated economy, often referenced as the "K-shaped" economy. Not everyone has benefitted from the above-trend growth over the last few years.

Slower growth would likely result in more Fed rate cuts and lower Treasury yields all across the curve. High-quality bond investments would likely benefit in this environment as lower yields would result in more price appreciation.

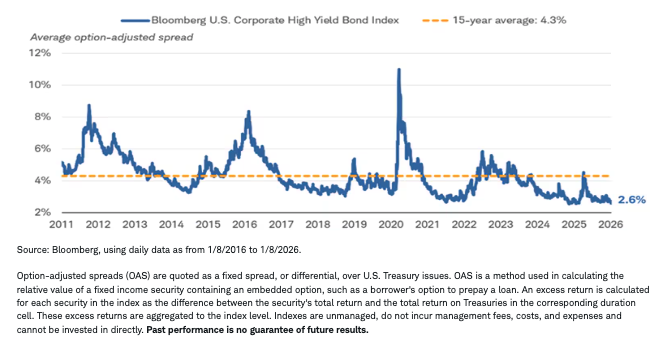

Riskier investments, like high-yield bonds and bank loans, would likely underperform in a slowing economy. Corporate profit growth would likely stall or turn negative, making it more difficult for highly indebted companies to remain current on their bond obligations. High-yield bond defaults have held near their long-term averages for the last two years, and they would likely edge higher.

The corporate bond markets aren't priced for slower growth ahead. Credit spreads—the extra yields that corporate bonds offer above comparable Treasuries—remain near their all-time lows, suggesting very little investor concern about the health of the economy or corporate balance sheets. If the outlook deteriorates, investors tend to demand higher relative yields to compensate for the potential credit losses if defaults do pick up. That pulls corporate bond prices lower relative to Treasuries.

High-yield spreads are close to the all-time lows

We have a neutral outlook on high-yield bonds even if growth holds near its trend given the low relative yields. If economic growth were to slow, or worse, a recession arrived, high-yield bond and bank loans would likely underperform U.S. Treasuries.

3. Changes at the Fed. The beginning of each year brings the annual rotation of voters on the Federal Open Market Committee (FOMC). Governors are permanent voters, as is the president of the Federal Reserve Bank of New York who serves as the committee's vice chair, but district bank presidents vote on a rotating basis. While the two district presidents who dissented at the December FOMC meeting in favor of holding rates steady will rotate out of voting, two incoming voters appear to lean on the more hawkish side—Cleveland Fed President Beth Hammack and Dallas Fed President Lori Logan.

Potential changes to the Board of Governors may have more implications, however. Governor Stephen Miran's term ends at the end of January, and whoever fills that may become the Fed Chair once Jerome Powell's term ends at the end of May. President Donald Trump has made it clear he prefers a chair that shares his views on lower interest rates, so it's reasonable to assume that Miran's replacement will be more dovish than Powell.

While Powell's term as chair ends in May, his term as governor runs until January 2028. He hasn't disclosed his post-chair plans yet, and it's possible he will vacate his governor position later this year. Meanwhile, Governor Lisa Cook's future is in question as administration is attempting to remove her from her position.

The reported threat of a criminal investigation into the Federal Reserve muddies the outlook even more as it raises questions around both Federal Reserve independence and the outlook for new potential governor appointments. Following the announcement, Senator Thom Tillis stated that he will "oppose the confirmation of any nominee for the Fed—including the upcoming Fed Chair vacancy—until this legal matter is fully resolved." 1

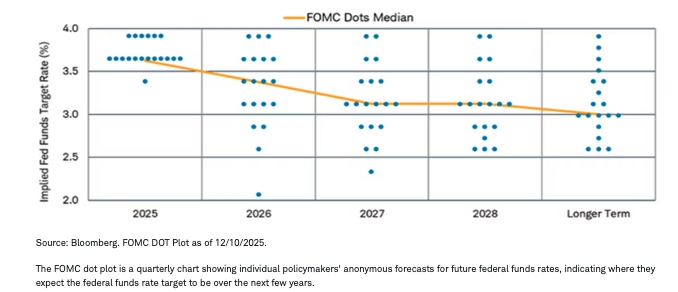

There's plenty of uncertainty around the path of monetary policy as the dot plot below illustrates. There's a wide range of views among committee members, and it may be difficult to build consensus this year. But if we see turnover at the Board of Governors and the members are dovish, then the Fed would likely cut rates more than we and the markets currently expect.

There is a wide dispersion of views among Fed officials about the path of

monetary policy

4. Geopolitical risks. The political outlook is unstable amid a number of policy changes. Domestically, the loss of subsidies for the Affordable Care Act and their impact on the government shutdown has been a source of dispute, along with immigration policies. In the global economy, the U.S. move to remove Venezuela's president has raised questions about future foreign policy moves.

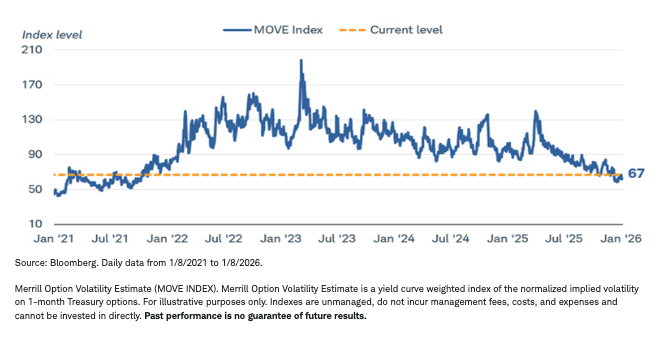

While markets have handled the various international conflicts easily, the implications for oil prices, the U.S. dollar, economic growth, and the budget are a bit unknown. It would not be surprising to see future bouts of volatility due to the instability. Treasury market volatility, measured by the ICE BofA MOVE Index shown below, is near its four-year lows. Treasury yields could move up or down more than expected if volatility picks up this year.

Bond market volatility is near its four-year low

What investors can consider now

Our base case—what we believe to be the most realistic expected scenario—calls for steady growth and sticky inflation, but it's always important to consider alternative scenarios and how they may impact investments.

We suggest investors consider intermediate-term maturities—those with average yields in the four- to 10-year range—given our outlook for a steeper yield curve. Focusing too much on short-term investments introduces reinvestment risk as the Fed cuts rates, but focusing too much on long-term investments means high interest rate risk if yields rise due to sticky inflation or the increase in supply.

We continue to suggest an "up in quality" investment theme mainly due to valuations. Treasuries, agency mortgage-backed securities, and investment grade municipal and corporate bonds would fall under that umbrella. Investors can consider riskier investments in moderation, but their low relative yields mean there's little margin for error if the economy slows.

1 Source: https://www.tillis.senate.gov/2026/1/tillis-statement-on-federal-reserve-nominations

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The securities and investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

Individual situations will vary. Not intended to be reflective of results you can expect to achieve and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk. High-yield securities and unrated securities of similar credit quality (junk bonds) are subject to greater levels of credit and liquidity risks and may be more volatile than higher-rated securities. High-yield securities are considered predominately speculative with respect to the issuer's continuing ability to make principal and interest payments.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Preferred securities are a type of hybrid investment that share characteristics of both stock and bonds. They are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features, and the timing of a call, may affect the security's yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so their prices may fall during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Bank loans typically have below investment-grade credit ratings and may be subject to more credit risk, including the risk of nonpayment of principal or interest. Most bank loans have floating coupon rates that are tied to short-term reference rates like the Secured Overnight Financing Rate (SOFR), so substantial increases in interest rates may make it more difficult for issuers to service their debt and cause an increase in loan defaults. A rise in short-term references rates typically result in higher income payments for investors, however. Bank loans are typically secured by collateral posted by the issuer, or guarantees of its affiliates, the value of which may decline and be insufficient to cover repayment of the loan. Many loans are relatively illiquid or are subject to restrictions on resales, have delayed settlement periods, and may be difficult to value. Bank loans are also subject to maturity extension risk and prepayment risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Currency trading is speculative, very volatile and not suitable for all investors.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2026 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits