All That Glitters…Could Actually Be Gold

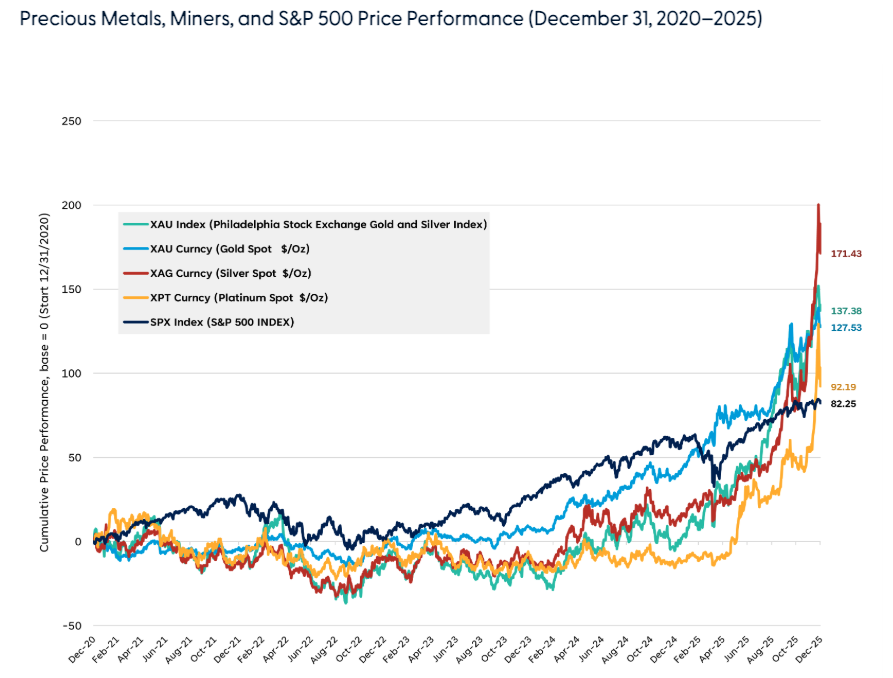

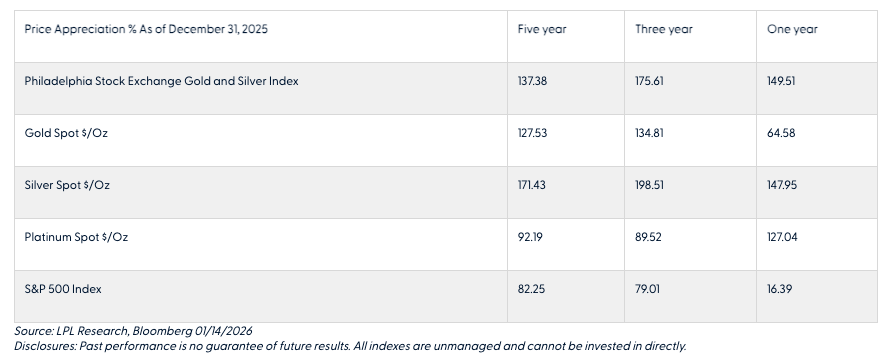

Precious metals surged out of the gate to begin 2026, not dissimilar to how they closed out 2025. Gold has already made two record highs this year alone, is currently trading above $4,600 per ounce, and is up over 6% in 2026. Silver is also breaking new records regularly, and more than doubled gold’s gain in 2025 after slightly lagging in 2024. Platinum joined the party in 2025, also doubling the performance of gold, after having done next to nothing in the previous four years. Precious metals mining stocks, measured by the Philadelphia Stock Exchange Gold and Silver Index1, outperformed gold, silver, and platinum last year. All three precious metals, as well as the Philadelphia Stock Exchange Gold and Silver Index, have outperformed the price return of the S&P 500 on a trailing one-, three-, and five-year basis2. Investors can choose their own adventure when it comes to the potential macroeconomic drivers of this outperformance: geopolitical tensions exposing foreign governments to the risks of relying solely on the dollar as the reserve currency (leading to U.S. dollar diversification, e.g., de-dollarization); a lack of trust in fiscal and monetary policies that lead to inflation; and concerns over Federal Reserve independence.

Whatever the reason, investors seeking exposure to precious metals will ultimately face a critical choice: invest in the commodity itself or invest in the companies that extract it. The LPL Strategic and Tactical Asset Allocation Committee (STAAC) continues to hold a constructive view of the precious metal commodity complex. However, in today’s blog, we will analyze the fundamentals and the technicals of the mining stocks and determine whether they have the potential to keep up the strong relative performance.

We’ll refer to companies in the business of discovering, mining, extracting, and ultimately selling metals and other physical materials as “miners” and their publicly traded shares of common equity we’ll call “mining stocks”. Our focus is on the precious metals mining group, but note there is typically overlap with broader mining indexes and large diversified miners may mine precious metals like gold and silver in addition to industrial metals like copper and aluminum. We will continue to leverage the Philadelphia Stock Exchange Gold and Silver Index as a proxy for this group of miners given its coverage (30 stocks) and history (incepted January 1979).

Fundamentals

We analyzed the performance of precious metals and the mining stocks in the prior section, so we know performance has been strong. The immediate questions for fundamental analysis are 1) do the underlying fundamentals of the mining stocks support the recent performance, 2) does the outlook support future outperformance, and 3) what expectations are discounted into current valuations? The answers to some of these questions are, of course, specific to individual circumstances and risk tolerance, while others are unknowable. We will break it down as best we can, in order.

- Recent fundamentals, namely revenue growth, profit margin expansion, and returns on equity, have all followed commodity prices higher as expected and superficially support the recent stock performance. On a trailing 12-month basis, current year-over-year revenue growth for the mining stock index is ~26%; operating margins are at ~37%, which expanded from 16% in the prior-year period; and returns on equity are currently at ~13.5%, up from ~2.5% in the year ago period (please note past performance does not guarantee future results). Growing sales and margin expansion drove earnings growth to ~91% in the current trailing 12-month period, up from 28% in the prior-year period, and highlight the operating leverage inherent in the mining business.

- However, we know that equities are forward-looking securities that discount future expectations, so the outlook is at times even more important than recent historical business performance. The outlook for 2026 is also supportive of the recent stock performance. Revenue is expected to grow 30% in fiscal 2025 once Q4 2025 earnings season wraps up, and then is expected to grow 24% in fiscal 2026. Similarly, earnings are expected to grow 99% and 61% in fiscal 2025/26. As a reference point, the so-called “Magnificent 7”, represented by the Bloomberg Magnificent 7 Total Return Index, is expected to grow earnings 21% and 19% in 2025 and 2026, respectively. All expectations and estimates are consensus estimates aggregated and sourced from Bloomberg.

- As for the current expectations discounted into the stocks, this is a bit more nuanced than prior calculations. We sampled the largest six miners in the index, which represents 67% of gold produced by the entire index; we used gold production to get a better representation of gold miners and to adjust for diversified miners and royalty companies. We then sourced consensus estimates for two primary key performance indicators — expected production, i.e., gold and silver mined, and realized prices, i.e., what analysts are modeling the sales price of said gold and silver. We focused on the 2026 and 2027 year-over-year change in each of these metrics. We then took a weighted average of expectations and found that consensus revenue expectations for 2026 are driven primarily by price, as realized prices are expected to grow ~21% while production is expected to decline slightly at -0.6%. In 2027, however, which at an index level shows revenue growth decelerating to just over 8%, our sampled companies show expectations for realized prices to decline by 1%, while production slightly ticks up by 2.6%. Now we just threw a lot of numbers out there, but the bottom line is this — the underlying consensus estimates for gold and silver prices discounted into the mining stocks begin to decline in 2027.

We have covered the fundamental performance that is baked into the mining stocks at the index level, as well as some sampling of underlying stocks in the index. As for valuations, the index is currently trading at a price-to-earnings ratio (P/E) of ~14.3x on consensus 2027 EPS; for reference, this is about five turns below the broad S&P 500’s P/E of 19.5x on 2027 consensus EPS. Despite much higher growth expectations in 2026 for the miners, and only slightly lower growth expectations for 2027, the group still trades at a sizable discount to the market.

Technicals

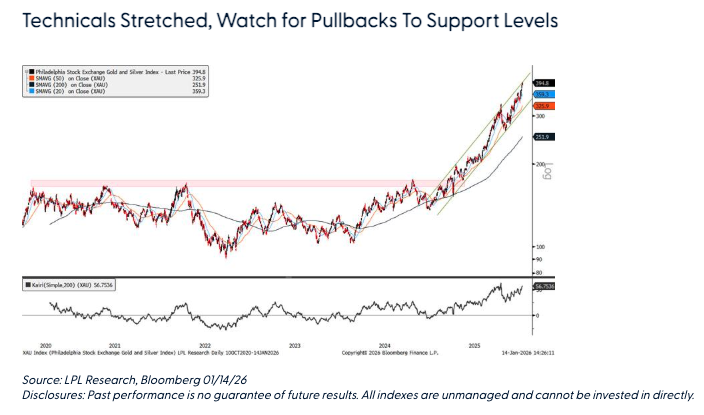

Looking at price-based technicals, the mining index continues to climb within a steep rising price channel after breaking out above major resistance in April 2025. Buying pressure has been widespread, but overbought conditions have resurfaced. Nearly half of the index constituents now show a Relative Strength Index (RSI) of 70 or higher, and the index itself is testing the upper boundary of the channel in an overbought state. The index is trading at a 57% premium to its 200-day moving average (dma) — just shy of the 62% premium seen in October before a sharp pullback ensued. Given this backdrop and the elevated risk of a potential pullback from these levels, we favor a tactical approach: using pullbacks within the channel as buying opportunities rather than chasing the current rally. Key support levels to watch include $370, the 20-dma near $359, and $333.

Risks

We must note the risks inherent in investing in mining stocks. First, volatility can be pretty extreme, so potential investors must be prepared for wild swings, on the upside and the downside. Second, as with all mining and natural resource operations, precious metals mining is conducted all over the world, many times in jurisdictions with immature or rapidly changing laws around ownership, taxes, and royalty rates. In certain emerging markets, it’s not unheard of for a newly installed government to completely nationalize mining operations — effectively killing the opportunity foreign mining companies had invested time and shareholder capital developing. Finally, as with all commodity based businesses, they are very cyclical. The current high prices of gold and silver will undoubtedly attract more capital to the industry, which will drive increased production (i.e., greater supply), which will drive prices lower. As the saying goes, the cure for low oil prices is low oil prices. The supply and demand of the commodities themselves is a topic for another note, but our research suggests we aren’t yet to a point where capital cycle theory would begin to come into play.

Conclusion

Our analysis suggests that the recent outperformance is supported by a strong fundamental backdrop of the business of mining gold, silver, and platinum group metals. The outlook for the next 12 or so months remains positive, yet is already reflected in the stock prices of the mining companies. From a fundamental perspective, investors need to expect either more price appreciation of the underlying precious metals this year, e.g., greater than ~20% baked into the mining stocks estimates or, must see sustained precious metal price appreciation into 2027. From a technical perspective, the group is clearly in a sustained uptrend but is exhibiting overbought conditions, and technical-based buyers may want to wait for pullbacks for entry points, while technical-based existing owners of mining stocks have no reason to look for the exits.

For investors seeking exposure to precious metals in an era of geopolitical uncertainty and monetary policy concerns, mining stocks offer a compelling alternative to physical commodities. They provide leveraged upside to accelerating gold and silver demand while delivering the cash flows, earnings, and shareholder returns that only operating businesses can generate. With the index demonstrating strong momentum and many constituents trading at reasonable valuations relative to their cash-generation potential, the sector warrants serious consideration in diversified portfolios.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) recommends neutral weighting to the materials sector and maintains a positive view on both precious and industrial metals.

Thomas Shipp leads the Equity Research team at LPL Financial, which provides insights driven from quantitative and fundamental equity research.

1 The Philadelphia Gold and Silver Index is an index of thirty precious metal mining companies that is traded on the Philadelphia Stock Exchange.

2

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #849529

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial