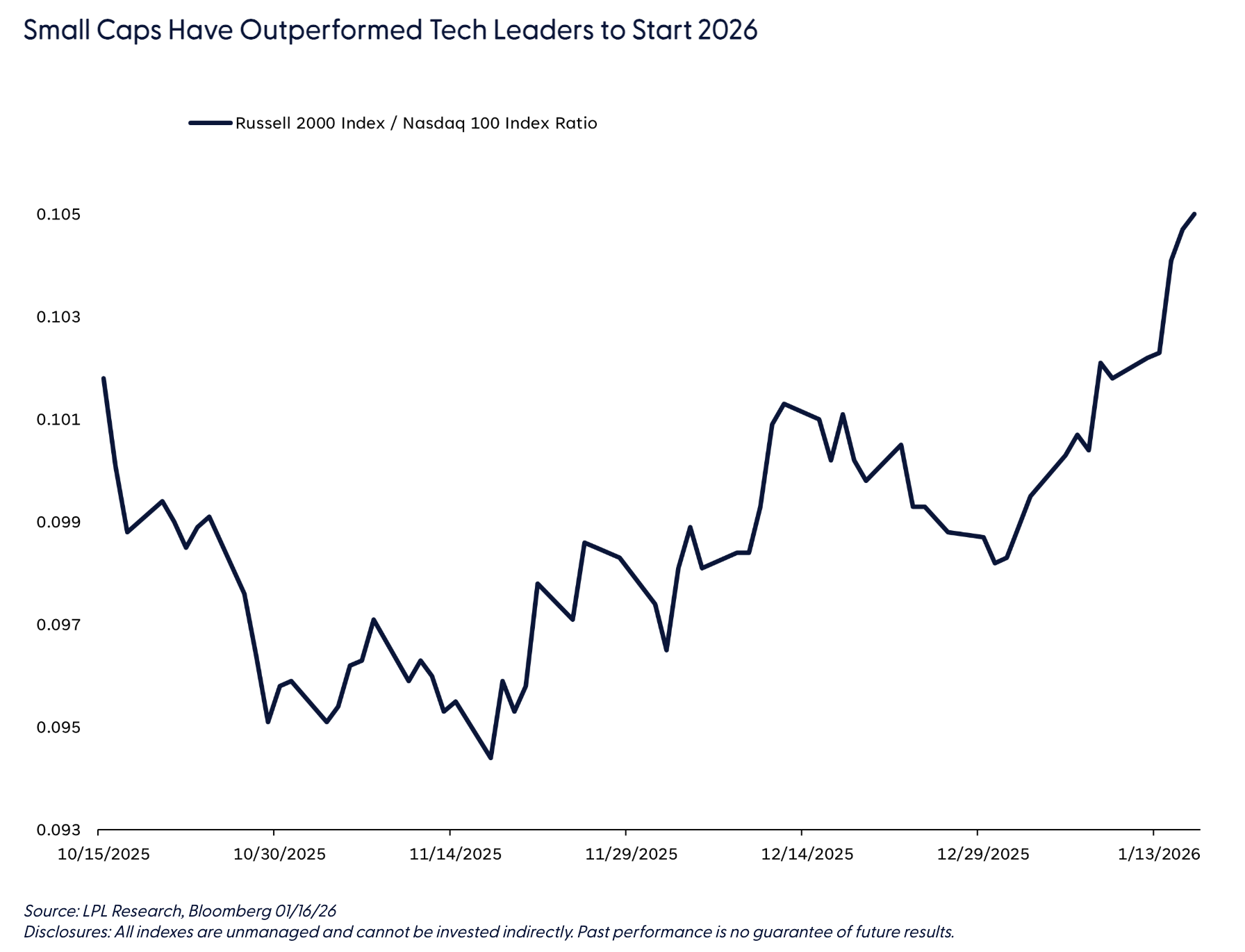

As the new year begins, one market theme is already attracting plenty of attention, and that is the dispersion and broadening out in the stock market that has occurred during the first two weeks of trading. After several years in which a small group of mega cap technology stocks dominated index performance, the first stretch of 2026 has looked surprisingly different. As of last Friday, the so-called Magnificent Seven is down on the year, while the Russell 2000 Index is outperforming the Nasdaq 100 Index by mid-single digits. At the same time, the Equal Weight S&P 500 is ahead of the traditional market capitalization weighted index by over two percent. This represents a real departure from the patterns investors have grown accustomed to throughout the last few years, in which leadership at the top of the index has largely overshadowed everything happening underneath.

Part of this shift seems to be driven by a growing belief that the economy is settling into something resembling a so-called “goldilocks” environment. Economic growth is near its long-run trend; inflation remains contained while the Federal Reserve (Fed) continues to ease. This is all perceived as particularly supportive of the broader S&P 493 and small cap companies, which are more sensitive to both interest rate expectations and cyclical momentum. What's unusual and worth noting is that even as the market embraces the reacceleration narrative, consumer staples — a sector that normally behaves defensively — has climbed almost 6% to start the year.

However, there are other additional factors that could be contributing to the broadening out in the market. Investors are becoming more hopeful that the Fed will turn meaningfully more accommodative after May. There is also speculation that lower-income consumers may benefit from targeted stimulus, which would help a wide range of domestically focused companies. On top of that, enthusiasm is building around the idea that productivity gains from artificial intelligence may finally start spreading beyond the mega caps into the real economy, which would be a genuine support for earnings across a much broader swath of the market.

While many market participants are celebrating the possibility of a more inclusive advance this year, we are approaching the early action with some caution. The first few weeks of any new year are notoriously tricky as every institutional manager has seen their P&L reset to zero with the turn of the calendar year. This reset often triggers a period of repositioning, tactical jockeying, and a lot of dispersion. Historically, the themes that work immediately out of the gate often give back some of their gains as the initial burst of activity settles down. In most years, it is not until mid-February or early March that the genuinely sustainable trends begin to really reveal themselves.

We shall see if this year is any different. The latter part of January will be especially important as the market will be entering into the real heart of earnings season. Microsoft (MSFT), Meta (META), and Tesla (TSLA) all report on the 28th, and that will probably be the first test for assessing whether the rotation away from the mega caps has real staying power. If the market continues to reward smaller names and equal weight indices even after the mega caps report, then the probability of a meaningful and durable broadening rises in a significant way. Until we see how the market reacts to these earnings, there remains a real risk of mean reversion in the themes that have worked so far in the new year.

In short, the early signs of broadening out are interesting, refreshing, and potentially important. But January is known for false starts and sharp rotations that do not always last. The next few weeks will be critical in determining whether this is the beginning of a new market regime or simply another early year head fake. For now, the best approach is to stay engaged, stay flexible, and watch closely how the market responds once results from the major tech companies begin to roll in.

Kristian Kerr drives the broad, house investment strategy for LPL Financial Research. His career includes over 25 years of industry experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #851235

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial