If U.S. Housing Inflection Is Near, Look for More Than Just Homebuilders

Over the last three months, the housing conversation has warmed up again. Markets seem to be saying the next chapter could be “more activity”; i.e., more housing starts, more remodeling, more jobs coming off the sidelines as confidence improves. However, homebuilding is not a simple business. It’s an industry where politics, regulation, and public scrutiny can swing sentiment just as much as mortgage rates and household formation. Recently, two storylines have competed for attention. One is a “pro-building” narrative based on recent Bloomberg reporting that two large homebuilders were developing “Trump Homes,” a pathway-to-ownership program to address affordability concerns for first-time homebuyers (Builders Push ‘Trump Homes’ in Pitch for a Million Houses). Such a program implies a friendlier environment for construction and development. The other storyline is the kind of headline that can drive equity investors toward the exits: reports that the Department of Justice may be looking at anti-competitive practices in parts of the homebuilding ecosystem. (White House considers antitrust probe into homebuilders, Bloomberg News reports | Reuters)

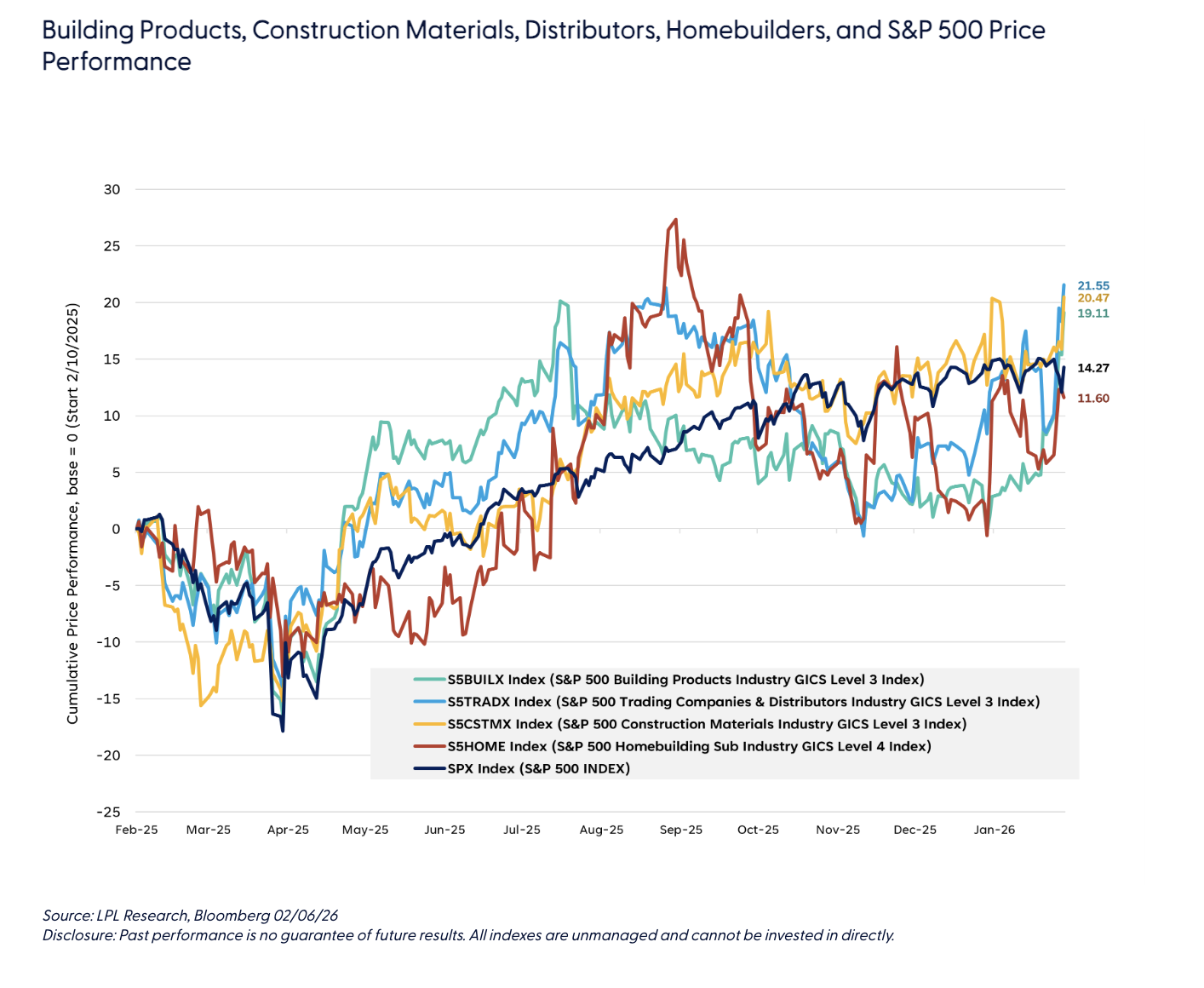

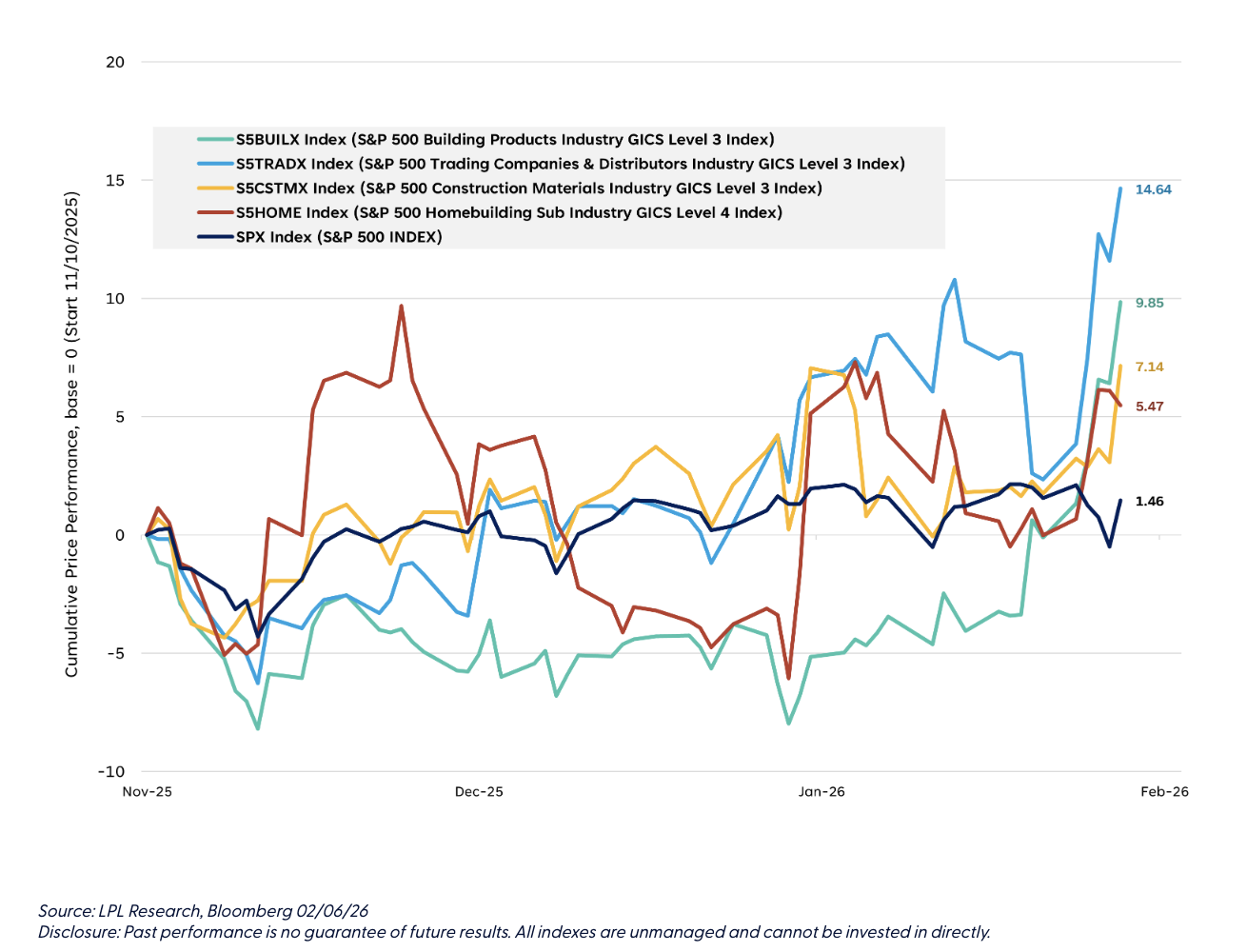

Whether either headline has legs in a legal or economic sense is almost beside the point. The market takeaway is that builders can carry non-obvious headline risk, especially when an industry is concentrated and profitability is visible. Therefore, if your core view is “residential construction activity will increase,” take a page from the AI capital expenditures (capex) boom and buy the picks-and-shovels businesses (i.e., building materials, product manufacturers, and distributors), rather than the homebuilders themselves. These are the companies that make and move the products that show up on every job site, regardless of which builder wins the subdivision. Performance of relevant S&P 500 industry indexes suggests the market agrees, as construction materials, building products, and distributors have outperformed homebuilders and the S&P 500 over the last three and 12 months.

Builders Have Baggage — Land, Incentives, Politics

Homebuilders can be great businesses in the right part of the cycle, and we appreciate the fact that most homebuilders are better businesses than they were in the last big housing upcycle pre-Global Financial Crisis (GFC). However, results remain influenced by several drivers beyond just “housing demand,” including:

-

Land economics: Lot costs, option structures, and entitlement timing can matter as much as sales volume.

-

Incentives and affordability: The builder can keep headline pricing stable while quietly giving up margin via mortgage buydowns, upgrades, and concessions.

-

Cycle timing: A builder’s profits can be extraordinarily sensitive to small changes in cancellation rates and closing schedules.

-

Regulatory optics: If regulators decide an industry looks “too concentrated” or “too profitable,” valuations can re-rate quickly, regardless of near-term demand.

In other words, buying homebuilders is often a bet on how housing demand expresses itself (pricing vs. incentives, regional mix, land bank strategy), not just whether demand exists. Acknowledging that homebuilding equities will generally benefit from increased housing demand, we suggest expanding your watchlist to include additional businesses that stand to benefit.

More Building Activity = More Materials and More Distribution Throughput

If you dig deeper beyond headlines and typical investment playbooks, the most reliable beneficiaries of increased housing activity are often the companies that supply the job site, either by making building materials and products or moving them efficiently to contractors and builders. Building materials manufacturers and distributors sit in a different part of the value chain. Their economics are typically more tied to unit volume and turnover, repair and remodel activity levels, and content/product mix. These drivers of sales growth and profit margins matter because housing can improve without turning into a new build-led housing boom. These businesses don’t need every macro variable to line up perfectly, they just need incrementally better activity, and the volume and mix can start to work.

Building materials and product manufacturers:

Manufacturers produce the core components that physically go into a home, such as roofing systems, insulation, siding, flooring, exterior cladding, sealants, etc. When activity improves, they can benefit in three broad ways:

-

Volume leverage: Many manufacturing operations have meaningfully fixed costs. As utilization rises, incremental sales can carry attractive profit contributions.

-

Mix and “content per home”: Even without a huge surge in starts, codes and preferences can increase the dollars of material per house.

-

Performance-driven pricing: In categories where labor-saving installation, durability, and energy efficiency are important, pricing can be based on “value added,” not just commodity costs. The better product portfolios can defend price and attach more components per project by selling integrated systems.

Different types of building materials and product manufacturers include those supplying: (a) the building envelope (i.e., roofing/insulation/weatherproofing) such as Carlisle Cos. (CSL), Owens Corning (OC), and Amrize Ltd. (AMRZ); (b) heating, ventilation, and air conditioning (HVAC) and climate control systems such as Trane Technologies (TT), Carrier Global (CARR), and Lennox (LII); © water heating and treatment systems, such as A.O. Smith Corp. (AOS); and (d) other diversified building product manufacturers such as Masco Corp (MAS).

Building products distributors:

Distributors connect manufacturers to contractors and builders by stocking inventory, delivering to job sites, bundling SKUs, and often extending trade credit. In a housing upcycle, distribution can be seen as a direct “activity proxy” because it captures:

-

Throughput growth: More jobs lead to more orders, whether new build or repair/remodel.

-

Share-of-wallet expansion: Distributors increasingly try to become one-stop shops across complementary categories.

-

Operational leverage: Consolidated networks can spread branch, warehouse, and delivery costs across more volumes.

Examples of distributors include QXO Inc. (QXO), privately held ABC Supply, Builders FirstSource (BLDR), TopBuild (BLD), and traditional “big box” retailers like Home Depot (HD) and Lowe’s (LOW), which have expanded their professional distribution businesses in recent years via acquisitions.

As with any supplier/wholesaler relationship, channel consolidation can drive efficiencies but also be detrimental to manufacturers, as distributors may gain bargaining power, pressuring manufacturers’ margins even when end demand improves. That’s why within these “picks and shovels” plays, it is important to focus on quality, which often shows up as product differentiation on the manufacturing side, and supply reliability and service on the distribution side.

Conclusion

The housing investment theme doesn’t have to be a binary decision based on a boom-or-bust homebuilding environment. If activity is simply trending upward, we believe there’s a compelling case for adding exposure to the companies that supply the job site, especially when political and/or regulatory noise make the homebuilders harder to underwrite. Roofing, HVAC, plumbing, and insulation aren’t glamorous. But they are necessary, and they scale with activity. Additionally, as building codes push for energy efficiency and durability, building materials and products can quietly become more valuable per home over time. If the next leg of housing demand is higher, the cleanest beneficiaries may not be the names buying land and managing incentives, but instead the businesses selling the materials, shipping the products, and helping solve the job site’s daily problems.

Thomas Shipp leads the Equity Research team at LPL Financial, which provides insights driven from quantitative and fundamental equity research.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1063041

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial