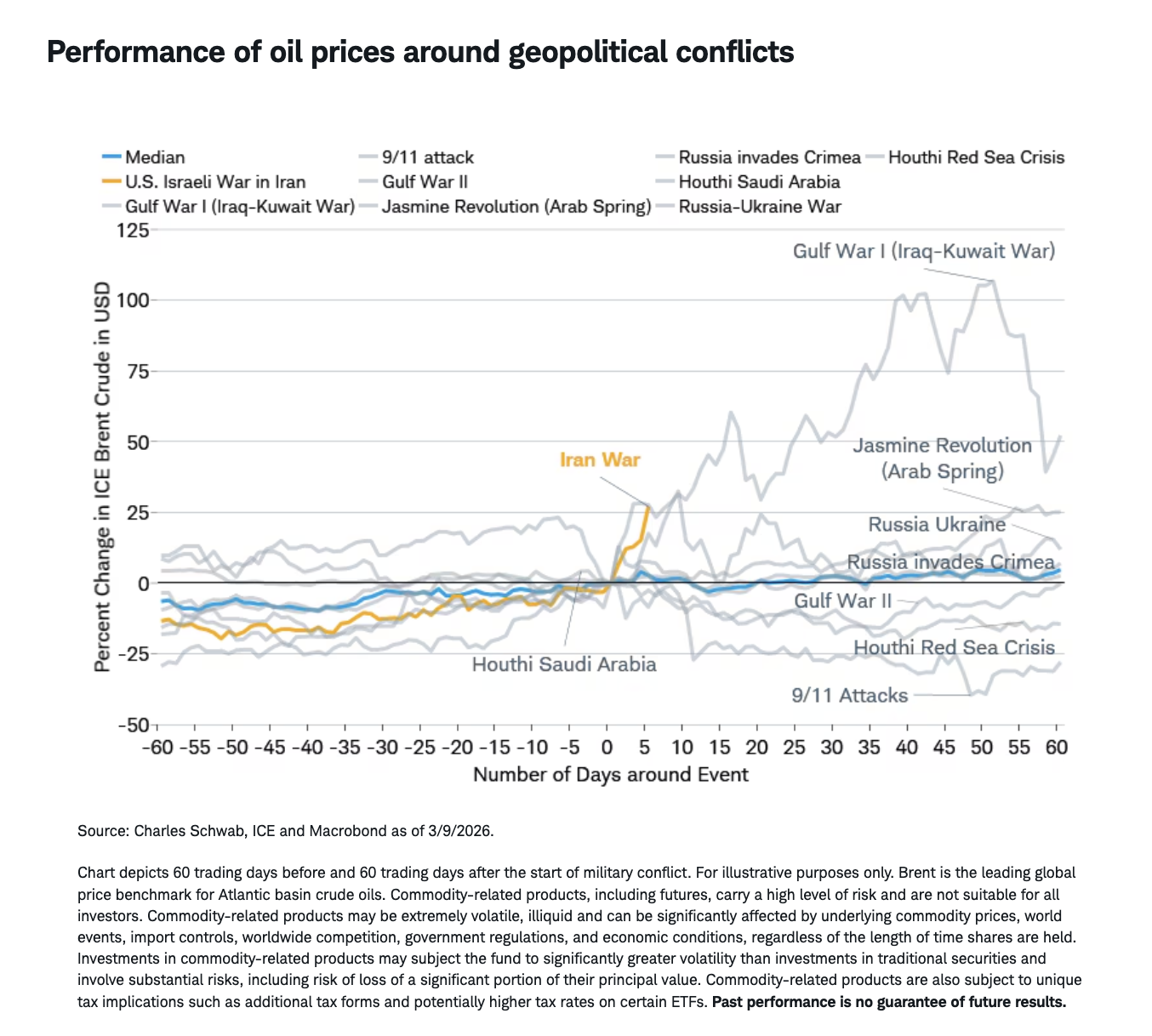

Iran War: Potential Impact on Global Equities

Key takeaways

- In the week since the U.S. and Israel launched military operations against Iran, we've seen global market volatility increase sharply. Energy prices have spiked and risk assets have sold off to varying degrees. Uncertainty remains very high and we continue to track a range of scenarios for how this conflict may be resolved and how it may impact economic conditions and financial markets.

- We see the most likely outcomes as either a relatively quick transition from major military operations to negotiations or a gradual de-escalation. However, downside risks rise meaningfully in scenarios where global energy supplies face a prolonged disruption with potential spillovers to global growth, inflation, tightening financial conditions, with international markets (especially Europe and Asia) most exposed.

- Currently, we are not changing our views regarding the constructive backdrop for risk assets and continue to see international equities as offering strategic appeal due to attractive valuations and sector composition. History suggests equity markets could rapidly rebound if a ceasefire occurs. That said, this conflict presents meaningful downside risks, and we don't believe now is the time to aggressively add risk; it's too early to call the "all clear."

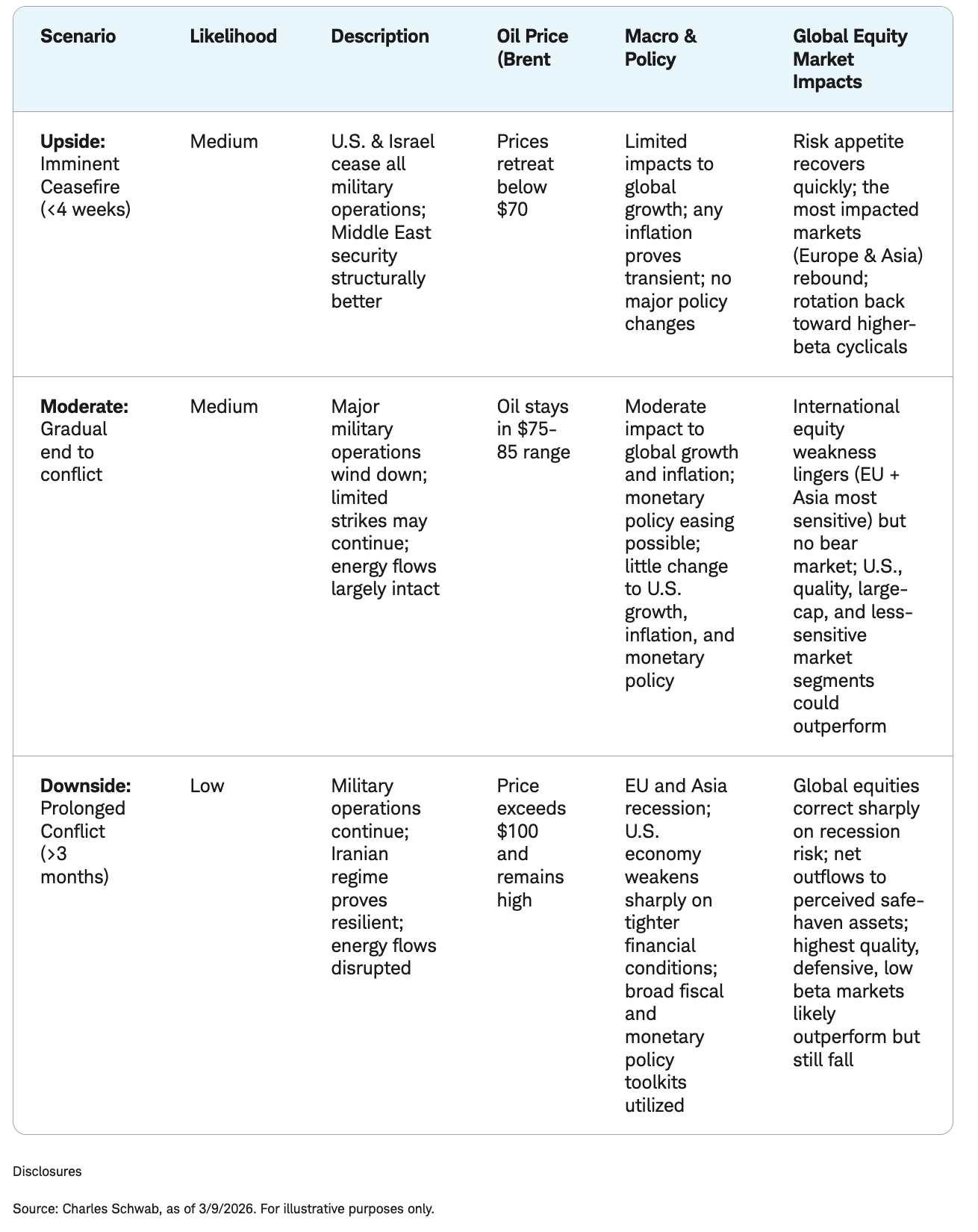

Last week we outlined three potential outcomes for the Iran conflict—an upside case, a moderate case, and a downside case. We are providing an updated scenario table below to provide more details on the impact to stocks. The upside case is defined by a quick end to military operations, with energy production and shipments normalizing and market pricing returning toward pre-conflict levels.

In the moderate case, military operations continue for several weeks at reduced intensity before winding down. Oil prices may remain elevated, but there is no major disruption to global supplies. In that environment, risk aversion can stay higher for longer, and market leadership could remain with relative "safe-haven" assets and sectors with less exposure to energy costs. U.S. equities may outperform Europe and Asia-Pacific on a relative basis, while energy and defense-related areas tend to hold up better than energy-sensitive industries such as airlines and transportation. We view the upside and moderate scenarios as the most likely scenarios.

The downside case presents risk to portfolios with a prolonged conflict disrupting global energy supplies and pushing oil prices sharply higher for a sustained period. That would raise recession risk by squeezing household purchasing power and corporate margins while also lifting inflation, which is a particularly difficult mix for policymakers to respond to. In this scenario, the potential for deeper and more persistent drawdowns in global equities increases, more so for international stocks than U.S. stocks.

Risks for emerging-market (EM) stocks are greater than for developed markets due to the impact a weaker currency has on inflation and capital outflows. The 18% two-day decline in the South Korean KOSPI Index last week highlights the risk. Speculative stock trading, limited liquified natural gas (LNG) inventory and a weaker Korean won resulted in forced sales by speculators, causing stock market selling to snowball. Additionally, the MSCI Korea Index has over 50% exposure to two memory chip companies. The longer the conflict in Iran and energy supply disruptions last, the bigger the chance the memory chip shortage intensifies either due to restrictions on access to energy or higher energy prices.

Iran war scenarios and potential impact on global equities

Episodes like the current one can be uncomfortable for investors given the uncertainty and volatility that accompany them. Indeed, headlines over the last week have been spectacular—and often focused on worst-case outcomes. But we reiterate the point that making reactive changes to portfolio allocations can lead to adverse impacts. Strategically constructed, diversified portfolios are built to weather periodic geopolitical shocks like this one. History suggests equity markets would rapidly rebound when a ceasefire occurs. That said, this conflict presents meaningful downside risks, and we don't believe now is the time to aggressively add risk.