Key takeaways

- The war in Iran has evolved from a geopolitical event to a global energy supply shock. The disruption to energy and commodity supplies is likely to have an increasingly negative impact on economic and financial conditions the longer it goes on.

- Even if military activity ends soon, the impacts to growth, inflation, and commodity prices could linger. And the longer energy and commodity supplies remain disrupted, the greater the potential economic damage. Asia appears most vulnerable, with Europe also facing meaningful exposure.

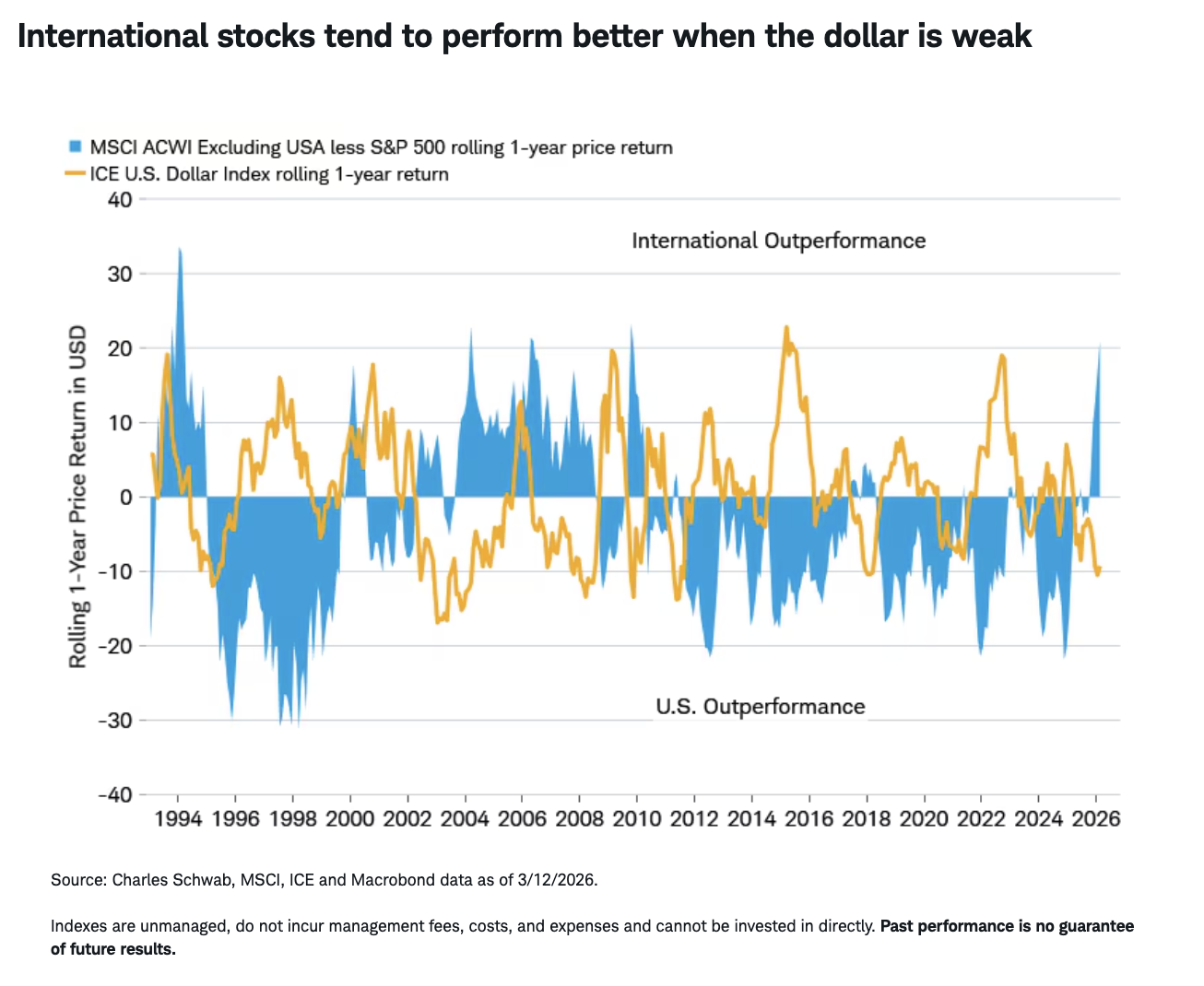

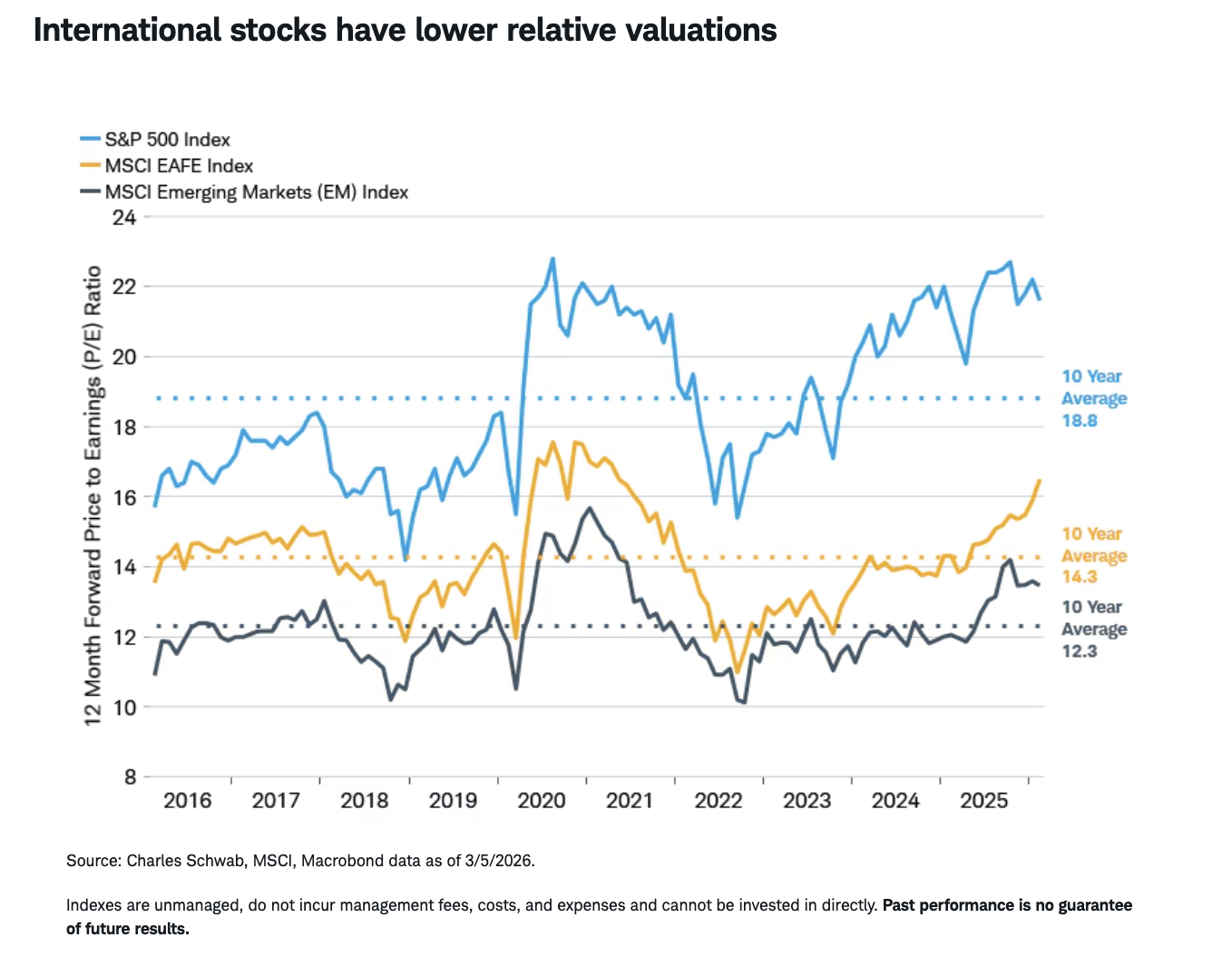

- While markets would likely rebound in the case of an end to military operations, international developed and emerging-market stocks may not resume their outperformance. Our base-case outlook is consistent with the Moderate scenario we lay out below, and implies greater downside risks for international markets in the near term and lingering economic and financial pressures that could persist over the next six to 12 months even with a quick end to the conflict. Said differently, we are less convinced international stocks can resume their outperformance in a Moderate case scenario.

Scenario framework: Three potential outcomes

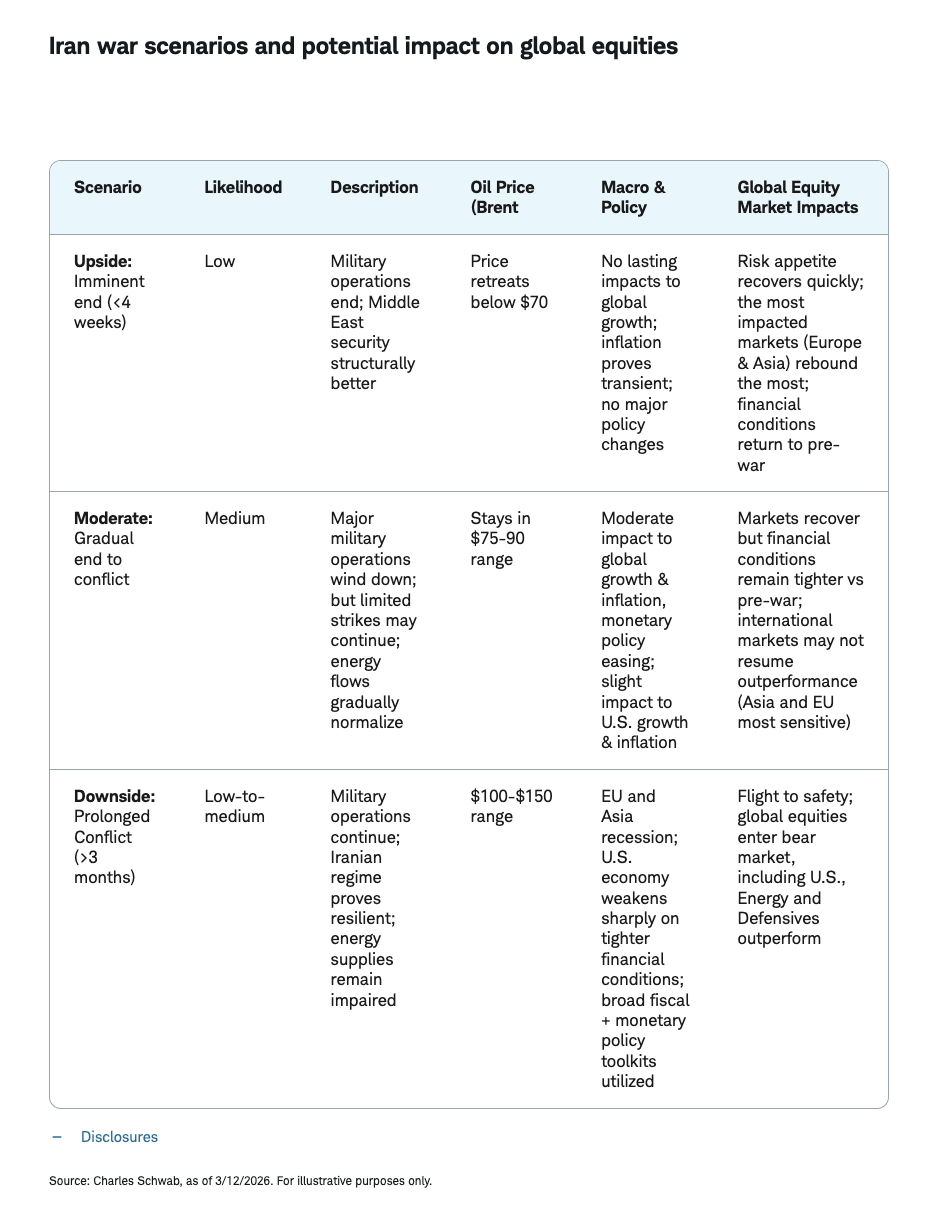

We are tracking the Iran war and potential economic and market outcomes via a scenario analysis that has three potential outcomes—an upside case, a moderate case and a downside case. The scenario table below provides an assessment of the likelihood of each case, including details on the potential impact to equity markets. The upside case is defined by a quick end to military operations, with energy production and shipments normalizing and market pricing returning toward pre-conflict levels. We see the likelihood of this case as reduced given the worsening conflict and disruptions to energy and commodity supplies.

The probability of the moderate case has increased and is now consistent with our baseline view. In this scenario, military operations may continue for several weeks before winding down. Oil prices may remain elevated due to lingering supply impacts and general uncertainty. The disruption to energy supplies has already increased in both intensity and duration since the start of the war. The longer energy and commodity supplies remain disrupted, the greater the economic damage. In this environment, financial conditions can remain tighter than normal and risk aversion can stay higher for longer, and market leadership may not revert to international markets as had been the case leading up to the war.

The downside case presents more severe risks to portfolios with a prolonged conflict leading to energy and commodity shortages, sharply higher commodity prices and rapidly tightening financial conditions. Such an outcome would raise recession risk while also possibly lifting inflation, which is a particularly difficult mix for policymakers to respond to. In this scenario, the potential for deeper and more persistent drawdowns across global equities increases. The risk of this scenario has increased but remains less likely than the moderate case, in our opinion.

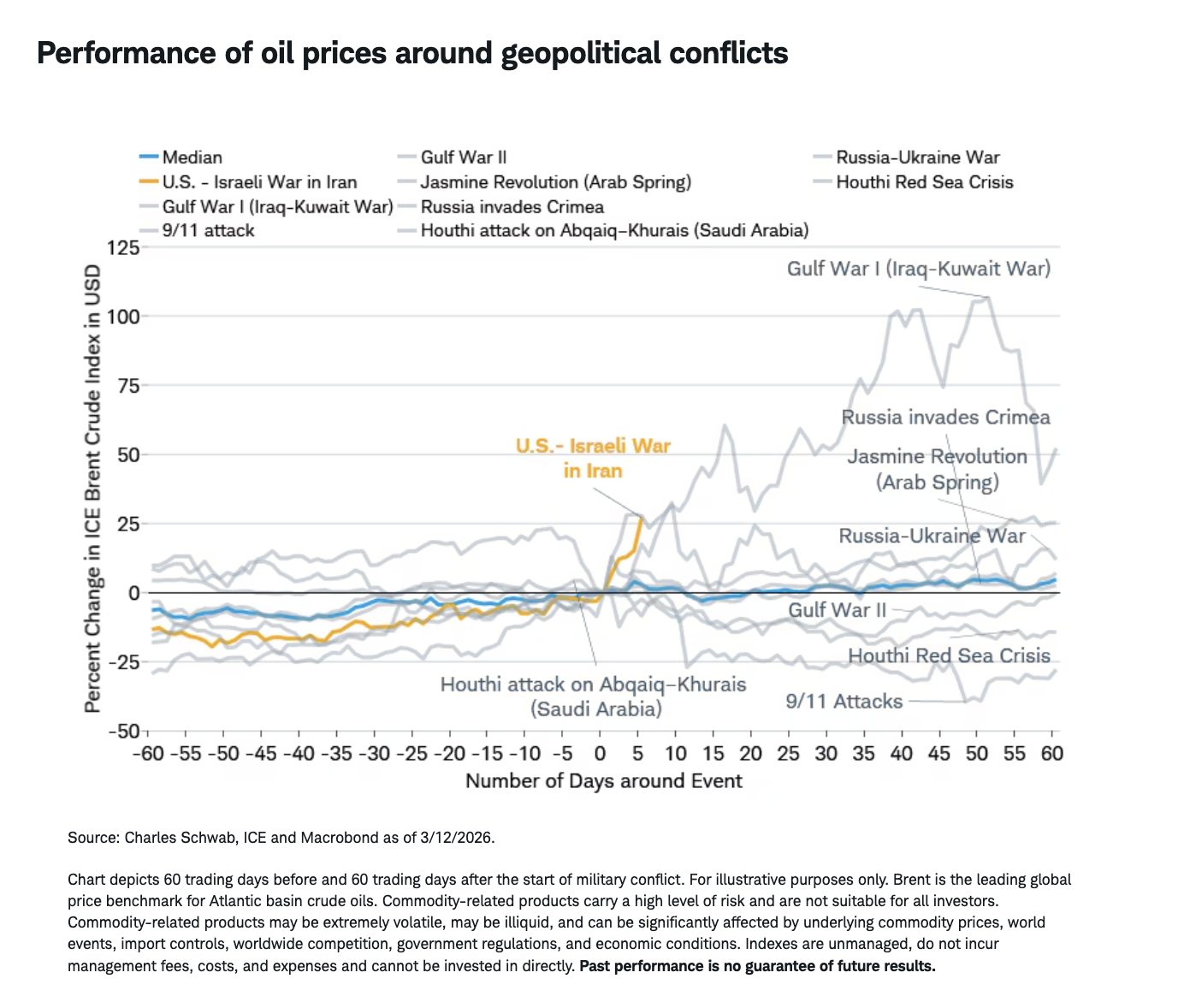

The current environment represents a geopolitical event that has evolved into a supply shock. History shows relatively mild impacts to equity markets after geopolitical crises. By contrast, major energy supply shocks have had more severe economic and financial market impacts. This conflict has effectively stopped all traffic from moving through the Strait of Hormuz, an event that has not occurred since the 1970s. Energy producers in the Middle East are running short of storage, which threatens to halt production altogether and raises the possibility of severe supply constraints. The worsening risk changes our outlook for international developed and emerging-market stocks.