Perspectives on The Energy Sector and Underlying Sub-Sectors

Energy cycles have a way of rewarding investors who show up early, while punishing those who assume the next upturn will look exactly like the last one. Supply disruptions caused by the war in Iran that began just under a month ago have upended markets globally, with oil markets taking center stage. My colleagues Kristian Kerr and Adam Turnquist have each written pieces this month digging into the physical oil market, “Assessing the Impact of Developments in Iran: Watch Energy” and “Oil in the Driver’s Seat as Geopolitical Tensions Rise”, respectively. Our focus is on the equities that are in the oil and gas business (energy stocks), focusing on the individual sub-sectors within the broader energy sector. Energy was the best-performing sector in the S&P 500 before the war broke out, and investor interest has increased as they attempt to underwrite the new geopolitical environment.

Energy investing is rarely hard because the math is complicated, but because cycles mess with judgment. When oil is cheap and the sector is hated, it feels irresponsible to touch it. When oil is expensive and headlines are everywhere, it suddenly feels like the simplest trade in the world. That's typically when investors take the most risk for the least incremental reward.

As with most investing topics, we think the right way to approach energy equity analysis is as a mosaic, with the mind and machine working together to weigh the evidence. You don’t need one perfect indicator, but a set of clues that improve your odds of avoiding two classic mistakes in energy: showing up too late and leaning into the wrong subsector for the environment. What follows is a brief review of energy subsector performance and a framework for thinking about which sub-sectors tend to lead at the onset of an energy investment cycle, including a zoom in on energy sub-sector performance from December’s WTI crude oil closing low to date, with a focus on the before and after of the onset of the Iran War. Finally, we provide a brief overview of each of the main energy sub-sectors.

Energy Stocks Don’t Act the Same in Every Cycle

Many assume investing in energy stocks (oil and gas stocks, specifically) is simply one trade based on oil and gas prices. In reality, the energy complex is a collection of very different businesses that respond to different triggers. Some are in fact closely tied to commodity prices, while others are more closely tied to activity levels like exploratory drilling or producing refined energy products like diesel fuel and gasoline. Still others behave more like long duration cash flow machines where contract structure and capital allocation matter more than the spot price of oil.

That distinction matters because the market does not reward oil exposure the same in every cycle. Oil prices are typically the catalyst, but spending and activity are typically the factors that drive value-creation (and destruction) throughout the cycle, and therefore are key to uncovering equity leadership.

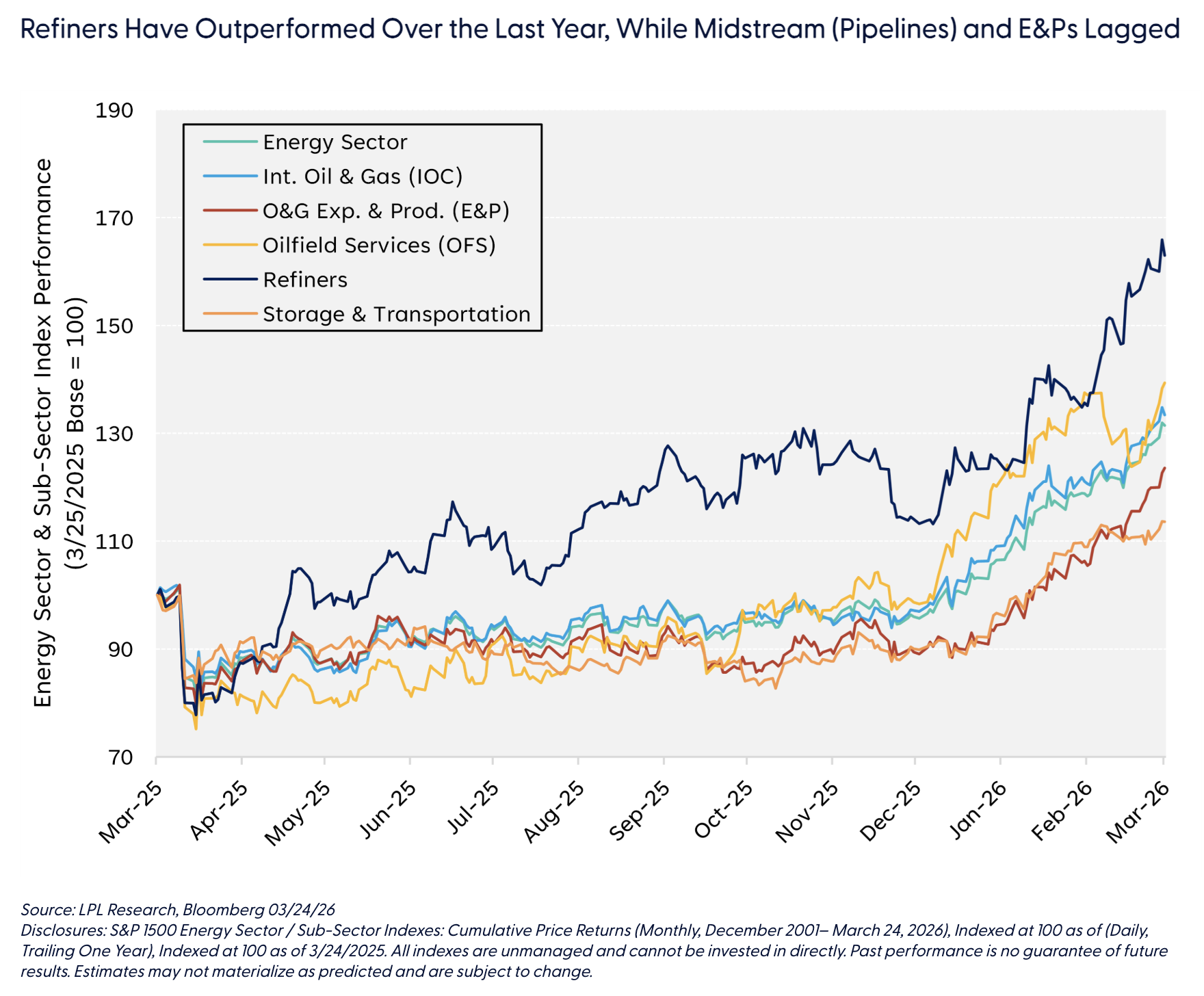

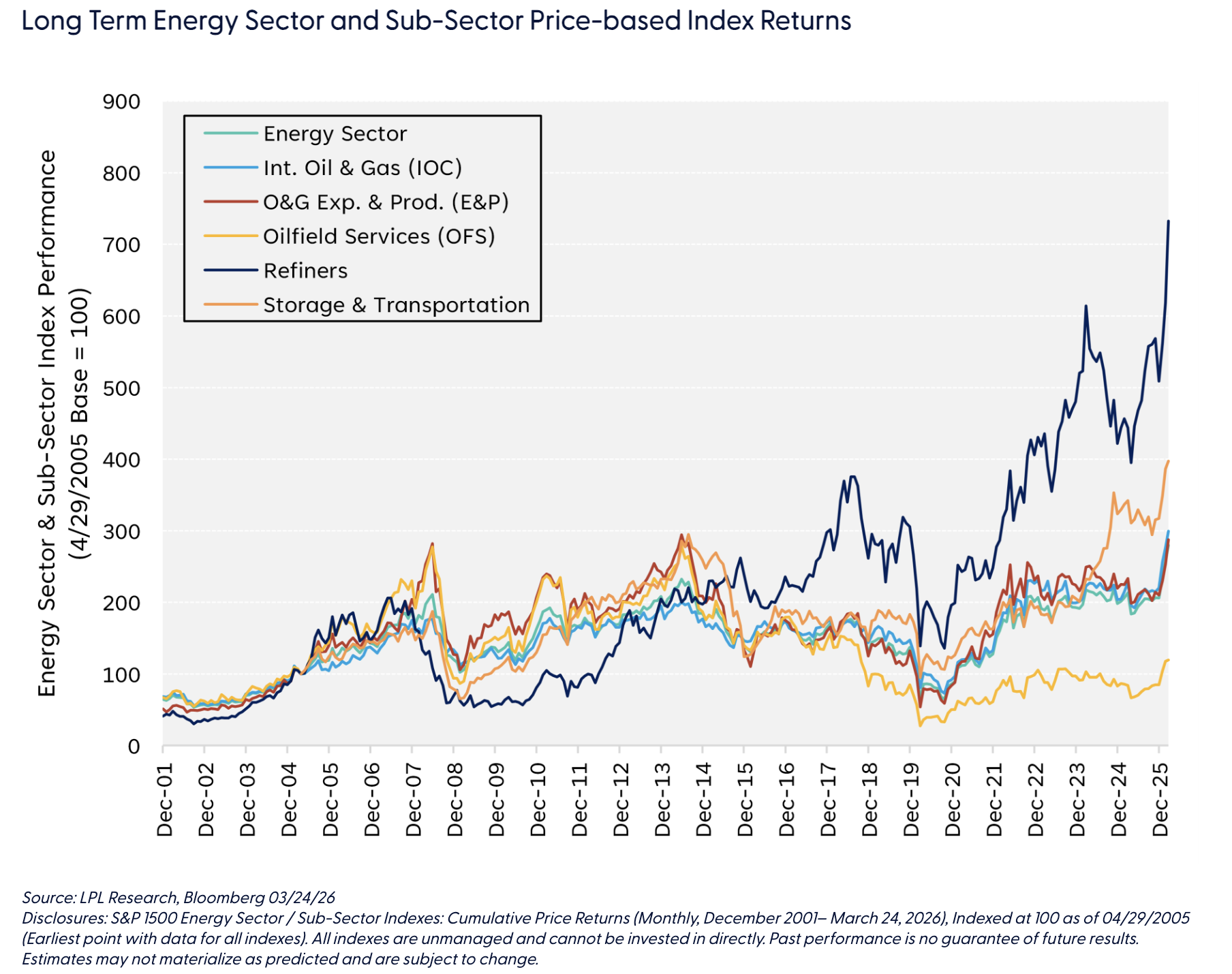

To provide a baseline on where we are today, in terms of leadership, we highlight the broad-based energy sector and individual sub-sector stock index performance on a near-term basis in the “Refiners Have Outperformed Over the Last Year, While Midstream (Pipelines) and E&Ps Lagged” chart and on a longer-term lookback in the “Long Term Energy Sector and Sub-Sector Price-based Index Returns” chart.

A Practical Road Map of What Tends to Lead Based on Cycle

The oilfield services (OFS) sector is often considered the “tip of the spear” in terms of an inflection in oil and gas activity. The sector generally leads out of the gates in an upcycle, followed by (or concurrently with) the E&Ps. While there is certainly truth in that, we prefer a more conditional way of describing leadership, depending on what the market believes about the duration of the move in oil prices. A helpful way to structure this thought process is based on how the sector reacts to three different views on the duration of the oil move, and how we characterize the returns generated by those views.

-

If oil rises but investors don’t trust it, the market often prefers short-cycle commodity exposure like certain exploration and production companies (E&Ps) and treats the move as a trade. These businesses move most with oil and gas prices and the forward curve. We characterize the returns here simply as “oil beta”.

-

If oil rises and the market starts believing it, leadership often shifts toward activity and pricing power. This is where OFS stocks will typically lead and outperform. These businesses benefit when industry spending rises and the service supply chain tightens. The equity upside historically has come not just when revenue climbs, but when utilization tightens and pricing power shows up via higher margins.

-

If the cycle persists and broadens into international/offshore, the market starts to focus on visibility and leadership can shift again toward backlog, project awards, and execution. In other words, the parts of the ecosystem that benefit from long lead-time investment. Large service platforms, offshore/subsea participants with backlog, many integrated majors, and midstream “toll-road” models often show up here.

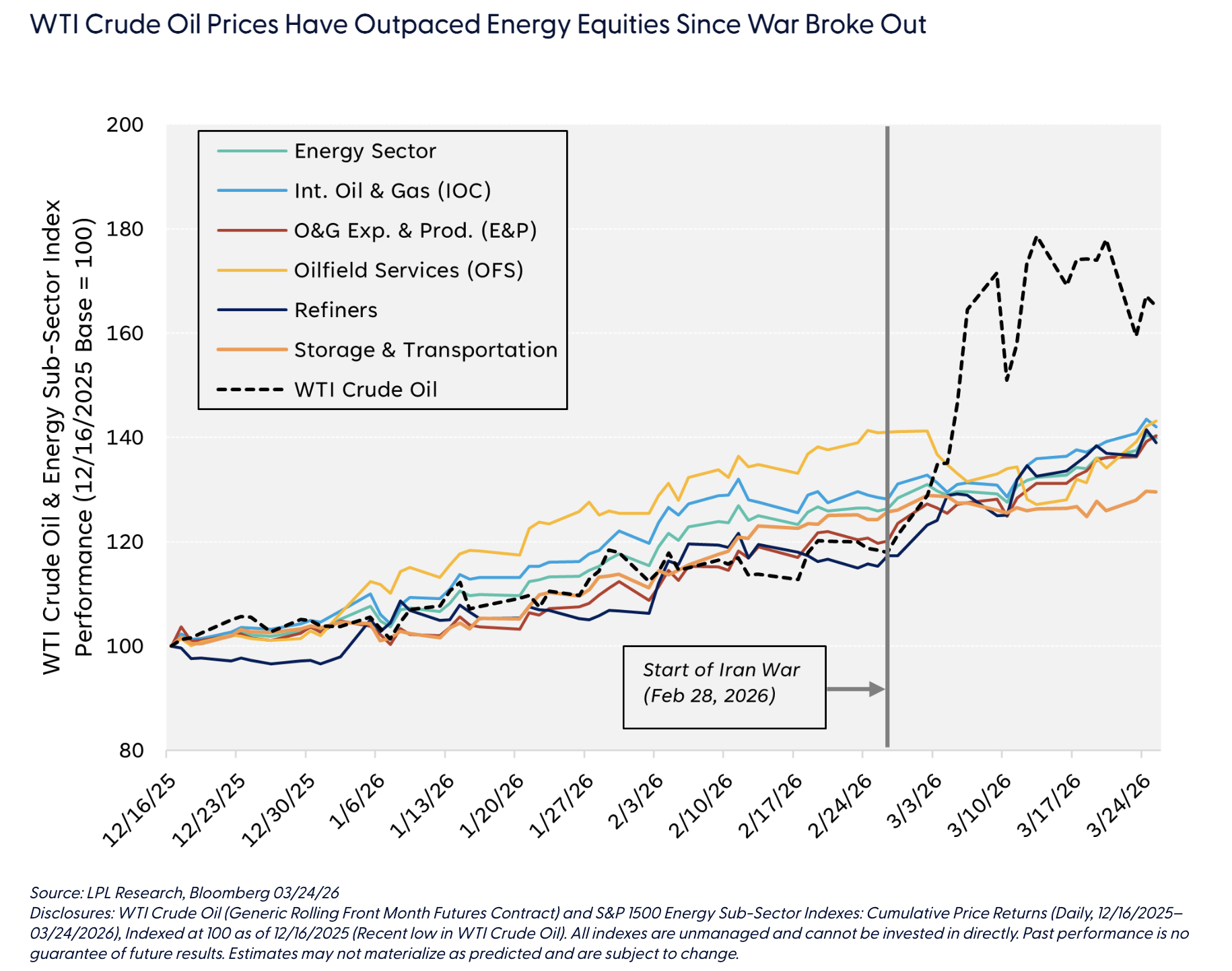

Since the recent pre-war lows in oil prices on December 16, 2025, energy equities have largely moved with oil. The notable standout was OFS, which tends to move with oil as a cycle develops, but moved well ahead of the commodity leading up to the war, though has underperformed since the war broke out due to disruptions in ongoing activity in the Middle East. The outperformance of the commodity relative to the stocks since the war broke out is not surprising given the physical nature of the supply disruption (highlighted in the “WTI Crude Oil Prices Have Outpaced Energy Equities Since War Broke Out” chart). However, we also believe this may point to the market not trusting the commodity move (scenario #1), and thus there is room for catch-up potential should oil prices sustain higher levels. In other words, we don’t think it’s too early to consider certain energy sub-sectors.

Energy Sub-Sector Cheat Sheet

In this brief closing section, we provide high-level definitions of the sub-sectors that make up the broader energy sector, important performance indicators to watch in each sub-industry, and what typically drives returns in the stocks. Think of this as a sort of CliffsNotes (do those still exist?) for the energy sector to help map the terrain and chart the course for a deeper-dive analysis.

Energy Equipment and Services (Oilfield Services, or OFS)

What they do: Provide the tools, equipment, technology, and labor that help producers drill wells, complete wells, and maintain or enhance production. This category ranges from drilling services to production chemicals to subsea systems.

What to watch:

- Customer, i.e., oil and gas companies’ capital expenditures (capex) plans and commitments (FIDs, or “Final Investment Decisions” for large, long-cycle mega projects)

- Rig and completion activity

- Service pricing commentary

- Increases (or decreases) in sequential operating margins (signs of pricing power, or lack thereof)

- Offshore rig day rates, contract awards, backlog and order intake for longer-cycle businesses (contract drillers, subsea equipment and surface capital equipment, project services)

What drives returns: Industry spending (capex), asset (rigs, equipment, etc.) and crew (labor) utilization, and pricing power. OFS companies have historically driven strong operating leverage when demand tightens.

Exploration and Production (Upstream Oil and Gas, or E&Ps)

What they do: Simplistically, find and produce oil and gas. Their revenue is tied directly to commodity prices and production volumes, while cost structures are largely driven by service costs (revenue for OFS companies), labor, and land acquisition/leases and royalties to land owners/partners.

What to watch:

- Reinvestment rate, i.e., how much cash flow goes back into drilling

- Balance sheet leverage (debt)

- Breakevens (cash or accounting-based operating costs, capex, and sometimes dividends). Typically stated in dollars per barrel of oil or per million British Thermal Units of natural gas (MMBtu).

- Decline rates, or the percentage annual reduction in production from an oil or gas field from its peak

- Payout framework (dividends/buybacks) and whether it holds through commodity volatility

What drives returns: Commodity prices, the hedge book (how much production revenue is “locked in” at a pre-determined price), reinvestment discipline, and capital returns.

Storage and Transportation (Midstream Oil and Gas)

What they do: Move, process, and store oil and gas. Many midstream businesses resemble toll roads in that they are paid for volumes moved and contracted services, often with less direct commodity exposure.

What to watch:

- Contract structure and duration

- Customer concentration (who pays them)

- Leverage and refinancing risk

- Volume outlook by basin and product (oil vs gas vs natural gas liquids (NGLs))

What drives returns: Contract quality, volume stability, counterparty health, and balance sheet management.

Marketing and Refining (Downstream Oil and Gas)

What they do: Turn crude oil into products like gasoline, diesel, and jet fuel. Refiners are not a pure bet on oil prices, but typically a bet on product margins (i.e., crack spreads, or the difference between crude input costs and product selling prices).

What to watch:

- Product inventory levels (gasoline/diesel)

- Unplanned outages and maintenance cycles

- Demand seasonality

- Regulatory changes that affect blending or capacity

What drives returns: Crack spreads, inventories, outages, regulations, and global refining capacity utilization.

Integrated Oil and Gas Companies (IOCs)

What they do: Operate across the value chain, including upstream production, midstream logistics, and downstream refining/marketing (and sometimes chemicals). The integrated model can smooth earnings across cycles.

What to watch:

- Project pipeline and cost discipline

- Dividend and stock buyback sustainability through the cycle

- Downstream margin sensitivity (refining can help or hurt depending on conditions)

- Geopolitical exposure and fiscal terms in key regions (jurisdiction matters in a global industry)

What drives returns: Upstream prices, downstream margins, project execution, and capital allocation.

Additional disclosure: The S&P Composite 1500® Energy comprises those companies included in the S&P Composite 1500 that are classified as members of the GICS® Energy sector.

Thomas Shipp leads the Equity Research team at LPL Financial, which provides insights driven from quantitative and fundamental equity research

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1084398

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial