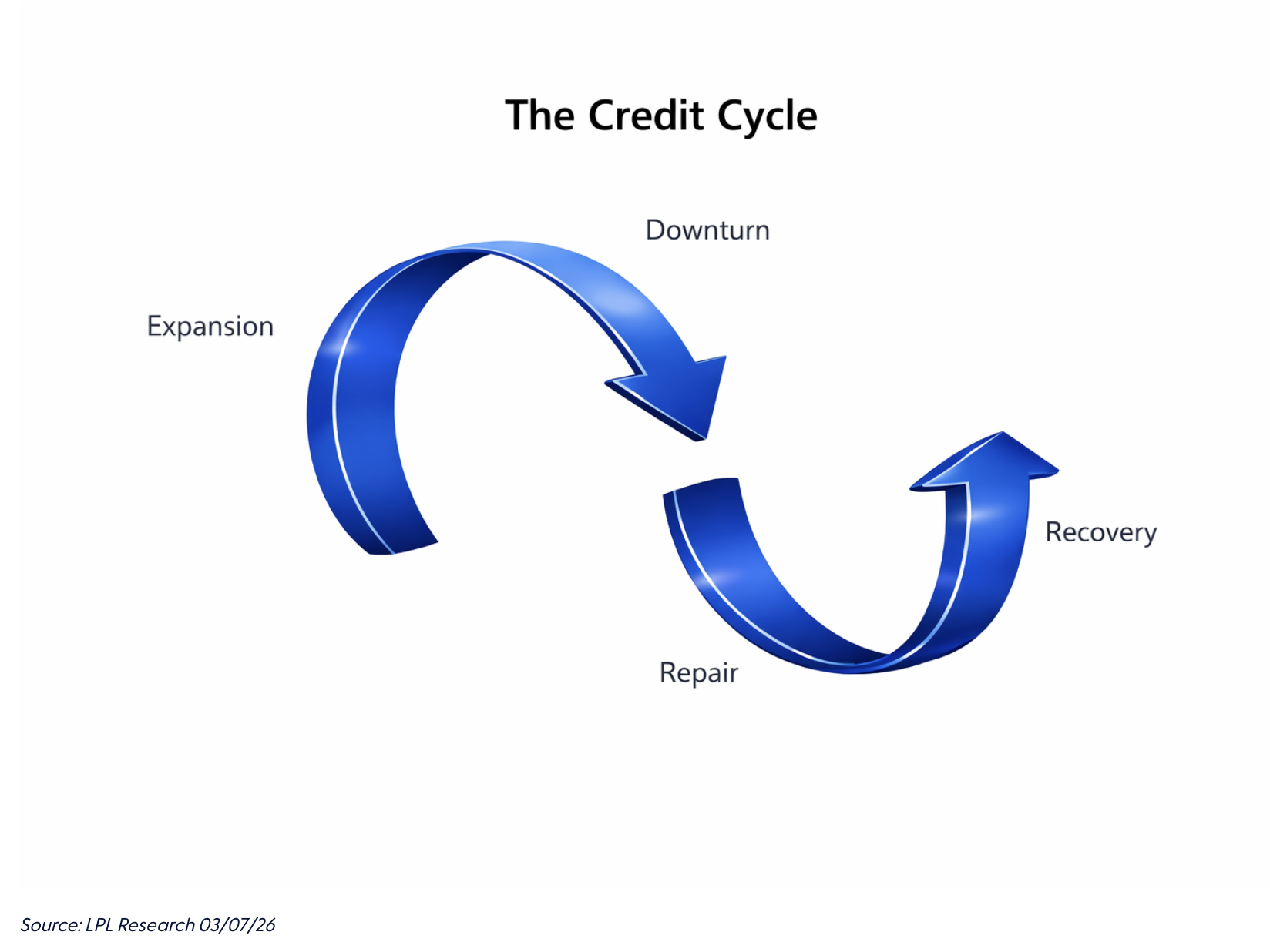

Private markets benefited enormously from the post-Great Financial Crisis era of ultralow interest rates that stretched through much of the 2010s and into the early 2020s. Amid regulatory change and muted returns in traditional fixed income during this time, investors were increasingly pushed into alternative areas of capital markets in search of yield. Private credit, in particular, emerged as a favored destination for institutional capital, including pensions, endowments, and insurers. The sheer volume of capital entering the space created competitive pressures that, in hindsight, were distinctly late cycle. Spreads compressed, underwriting standards loosened in some segments, leverage crept higher, and growth at any cost became a dominant objective for many managers. In many cases, deals were structured under assumptions that financing would remain cheap, and refinancing would be readily available. As liquidity ebbs and rates normalize at higher levels, those assumptions will undoubtedly be tested.

It is important to note, however, that acknowledging excesses and the existence of a credit cycle does not mean the private market asset class is structurally impaired. Credit cycles are not a flaw of the system; they are a feature of it. Periods of easy money tend to inflate asset prices and encourage excess risk-taking, while tighter financial conditions reassert discipline, reset valuations, and reward selectivity. We are clearly in that phase today. While additional adjustment and some degree of further pain appear likely, overall loss rates in private credit remain low by historical standards. Even if defaults were to triple from current levels, they would still represent a relatively small portion of total assets under management. What is changing is not the viability of the asset class, but the degree of differentiation between truly skilled managers and mediocre ones.

Every cyclical credit downturn acts as a stress test. Managers who prioritized asset growth, overly concentrated in specific sectors, stretched covenants, or relied on optimistic refinancing assumptions will find the current environment less forgiving. By contrast, firms that maintain conservative leverage, disciplined underwriting, and robust downside protections are entering this phase from a position of strength. This will be especially relevant for vintages that originated in 2020 and 2021. Many of those loans are now approaching refinancing windows in a materially higher-rate world, compressing interest coverage ratios and exposing weaker capital structures. Yet this is precisely how cycles are supposed to work. Capital becomes scarcer, pricing power returns to lenders, and prudent risk management is rewarded.

Private credit is unquestionably facing a more challenging operating environment than it has in years. But difficulty does not equate to dysfunction. In fact, the current backdrop is restoring many of the conditions long term investors should consider, including wider spreads, stronger lender protections, and fewer undisciplined competitors. In our view, opportunities will eventually emerge and disciplined managers will be there to take advantage of them in the repair and recovery stages. As financial history repeatedly demonstrates, cycles do not eliminate asset classes; they reset them, though past performance does not guarantee future results. For investors willing to be selective, patient, and cycle aware, private credit will be an asset class that is not defined by its recent stress, but by the managers who actually put processes in place that were built to perform across the full length of the credit cycle, not just the expansion.

Kristian Kerr drives the broad, house investment strategy for LPL Financial Research. His career includes over 25 years of industry experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1090486

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial