Divergent Data

GDP Growth Seems to Be Slowing

What’s Driving the Stock Market?

Iran and Oil

Final Call for SIC 2026 (Almost)

Boston, Miami And Maybe Europe?

I’ve been traveling for a week, reading and talking to a lot of readers and friends. It seems to me there is a great deal of angst in the media and newsletters and podcasts. And the more bearish you are, the greater your audience and clicks. There are so many analysts taking one or two data points and projecting a dismal outcome. Yes, there are a few that are more bullish, but they don’t get the publicity.

Today we're going to look at the underlying data and find that while the world is not ending anytime soon, there are actually good reasons for the disparity in forecasts. So, it’s okay if you’re confused. The stock market just hit an all-time high, energy is volatile and will be a negative on global growth, to say the least. GDP growth is much lower than we would like, the geopolitical issues are problematic (to say the least), plus a dozen other data points. Let’s see if I can help you understand how to deal with all this.

In the 26 years of writing this letter, two themes stand out. The first is that in the early 2000’s I said that the decade ending in 2010 would be a Muddle Through Economy. You must understand that US GDP had grown by over 3% for decades. There were three decades in a row last century where growth averaged almost 5%, so talking about a 2% decade was decidedly not consensus. I was constantly told that I was too negative and bearish.

We were coming off the 2002 low, but when I looked at how we were accumulating debt and organizing our country, I said that the US economy would only grow at 2% for the decade ending in 2010. That was what the research and economic data suggested to me. As it turns out, I was slightly optimistic - the economy grew 1.9%.

At the beginning of the last decade, I said essentially the same thing: we are in for another decade of a Muddle Through Economy. All the dreams of returning to a 3% GDP growth (which for an economy our size is incredibly strong) was not going to happen. And sure enough, GDP growth 2010-19 was 2.4%. Which, given the challenges, was pretty solid.

GDP seems to be slowing down again, and I think for the rest of this decade we will be lucky to see 2% overall growth. That is not bad. There are a lot of opportunities out there. But it is my belief that the opportunities are not going to be where they were in the past decades, where you can simply find an index and just ride the wave. I think this will be a very rifle shot, long-term investor market. You (or your advisor) are going to have to do homework rather than just simply choosing an index.

The second theme is that I believe we are going to see a crisis, a Great Reset or Great Restart, towards the end of the decade that will be quite disruptive. But it is also something that will pass, so the key is to make sure your portfolio and your life are anti-fragile enough that while the world may be disrupted, you are not.

Read more: The Global Restructuring

Divergent Data

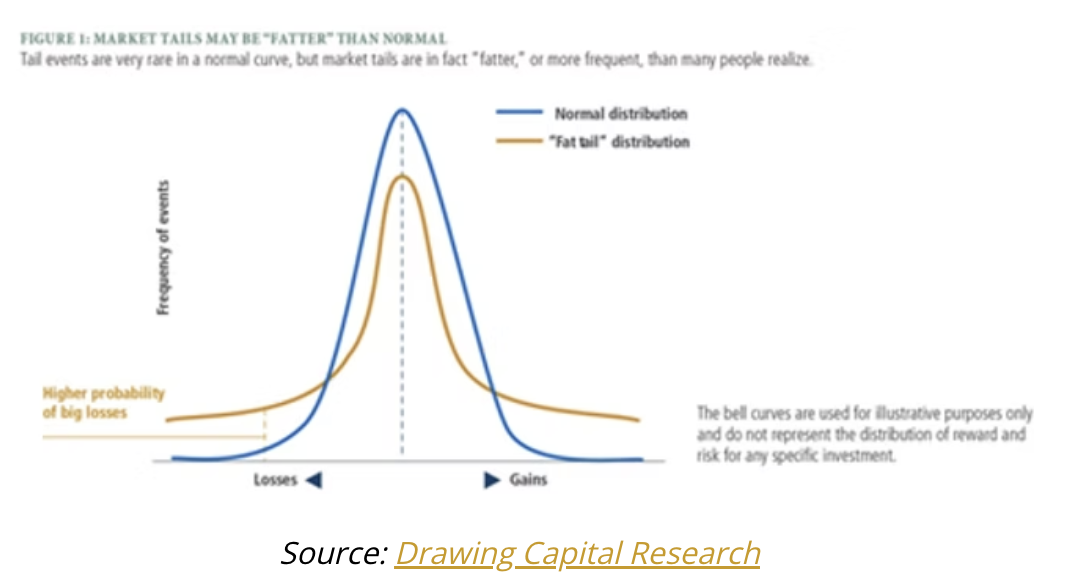

For most of the last century, economic data was pretty much evenly distributed across a normal bell curve. The chart below is a simple illustration of normal distribution, which I think represents the last century, and the “fat tails” distribution which has been the norm for the last 25 years and I think is going to be increasingly what we are looking at.

The distribution of economic data is more divergent, both good and bad, and that gives the opportunity for analysts to make far more divergent claims. These become click bait. And in our world today the negative ones get far more attention. It is good to pay attention to potential negative problems, but you need to balance that with the upside views.

Below, we are going to look at the projections for first quarter GDP. They are not robust. A lot of analysts take that one data point and make some pretty distressing predictions. But there are other equally compelling data points suggesting the opposite is happening. The goal is to find balance. So let’s jump into some of the data.

GDP Growth Seems to Be Slowing

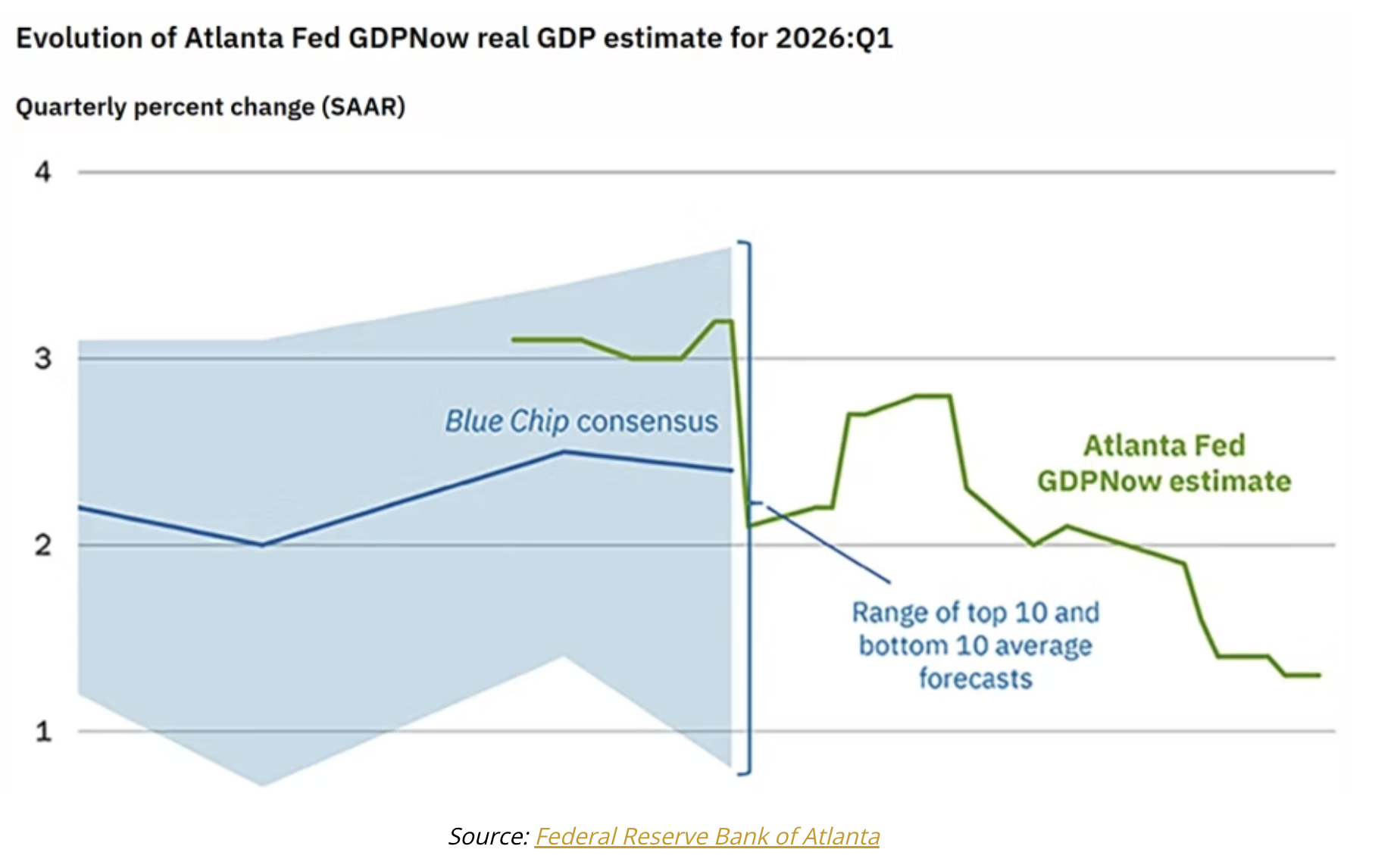

Projections for first quarter 2026 GDP are generally uniformly lower, some are more optimistic than others. The Atlanta Fed GDPNow says that the first quarter GDP growth will be 1.3%. This would be coming off of a 0.5% fourth quarter of 2025. To be balanced by a very robust 4.4% third quarter of 2025. For the entire year 2025 was up 2.2%, so a very Muddle Through year.

Projections for 2026 are generally higher for the year. The IMF projects 2.1% for the US. The Fed is at 2.4%. J.P. Morgan projects real GDP growth of 2% year-over-year by the fourth quarter of 2026. They come to this number where growth is expected to start at 1% in the first quarter, increase to 3% in the middle quarters, and then slow down again to 1% in the fourth quarter.

I should point out that obviously 2% GDP growth on average is not an end of the world moment. That has basically been our average GDP growth since the beginning of the millennium. Yes, there were some serious negative episodes, but they passed. They always do. And the stock market hit an all-time high this week.

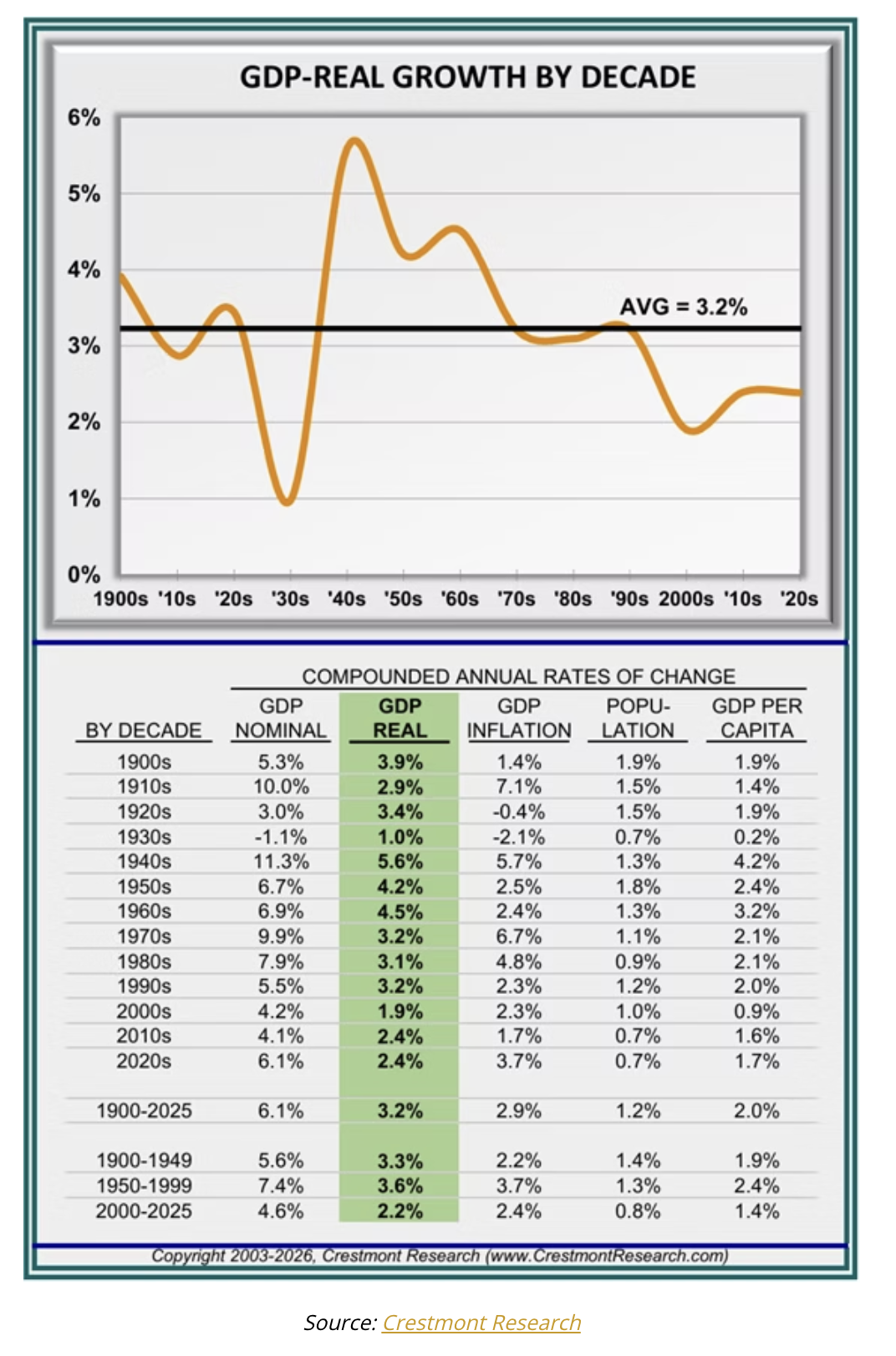

To give us historical perspective, let’s look at this table from Crestmont Research (run by my good friend Ed Easterling). Take some time to look through these numbers. And in particular notice the numbers on the far right of the table. This is the growth in GDP per capita. Even though GDP has grown 2.2% since 2000, on a per capita basis it has only grown 1.4%.

GDP is essentially the number of workers times their level of productivity. Because the US has seen a number of workers increase, largely due to immigration, we have more workers and the capital we employ make those workers more productive.

Therefore, by definition GDP per capita will always be less than national GDP. While 1.4% per capita GDP growth doesn’t sound like much, and historically it isn’t, it has increased the well-being of our nation. The distribution may not be even, and that is another real problem, but the entire country as a whole is improving. And that sets the foundation for continued growth.

What’s Driving the Stock Market?

There is a quote attributed to Benjamin Graham but has been repeated by Warren Buffett. “In the short run, the market is a voting machine. But in the long run, the market is a weighing machine.”

What Graham was trying to tell us is that emotions drive stock prices in the short term. And just like voters in any political election can change from month to month or week to week, so can prices in the stock market.

But in the long run, stock prices are a reflection of their earnings. Earnings are the weight, if you will. And earnings have been unusually strong for the last 6 quarters.

The earnings projections from Standard & Poor's for the S&P 500 for the first quarter of 2026 and for the whole year are as follows:

They expect year-over-year earnings growth rate in the first quarter to be 13.2%. This growth rate is expected to mark the six-story quarter of double-digit year-over-year earnings growth reported by the index. That is just spectacular.

Looking at the actual figures, they project earnings of $308.52 per share.

You can find numerous projections, but almost all are robust. J.P. Morgan projects that the S&P 500 will see earnings growth of between 13% and 15% over the next two years, with a year-end price target for 2026 initially set at 7,500 but later revised down to 7,200 due to market volatility and external risks.

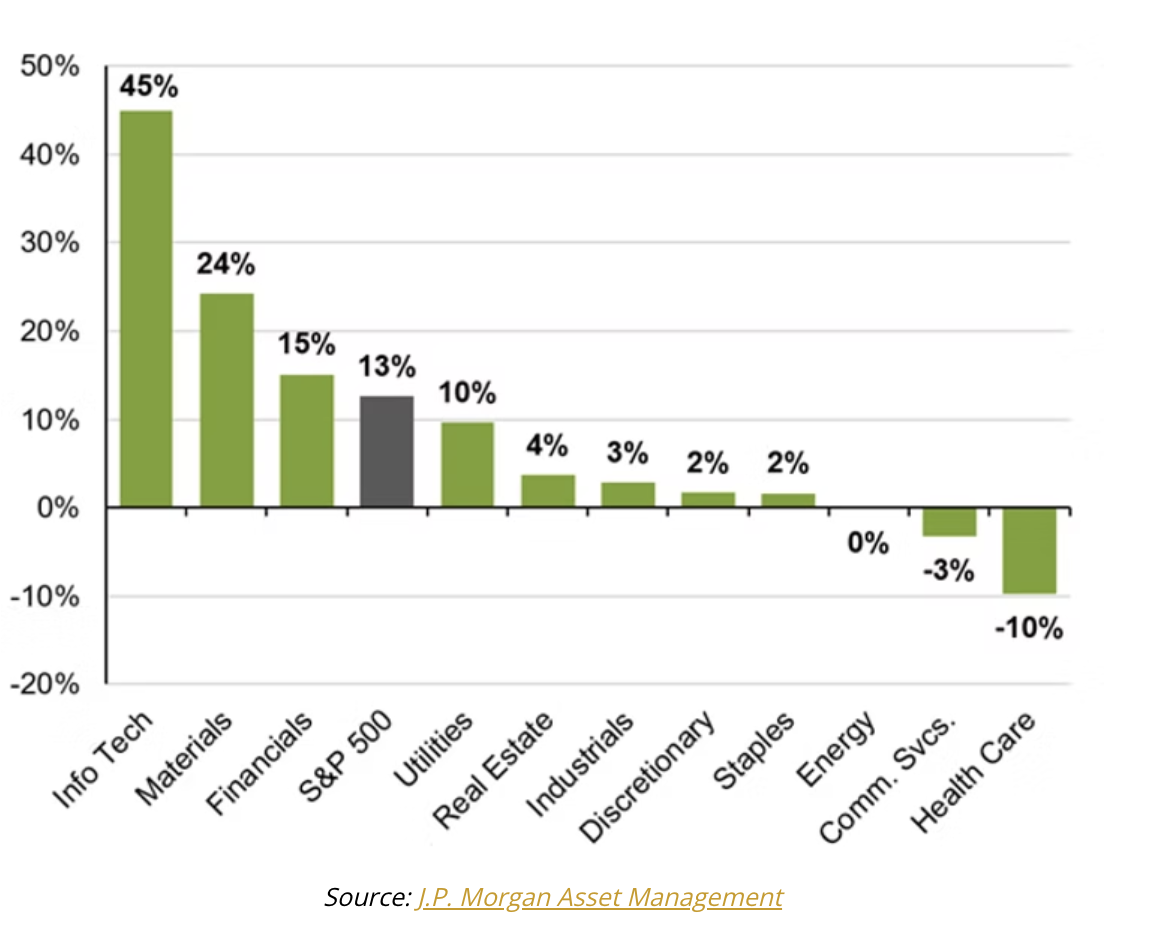

And yes, earnings are not evenly distributed by company and sector.

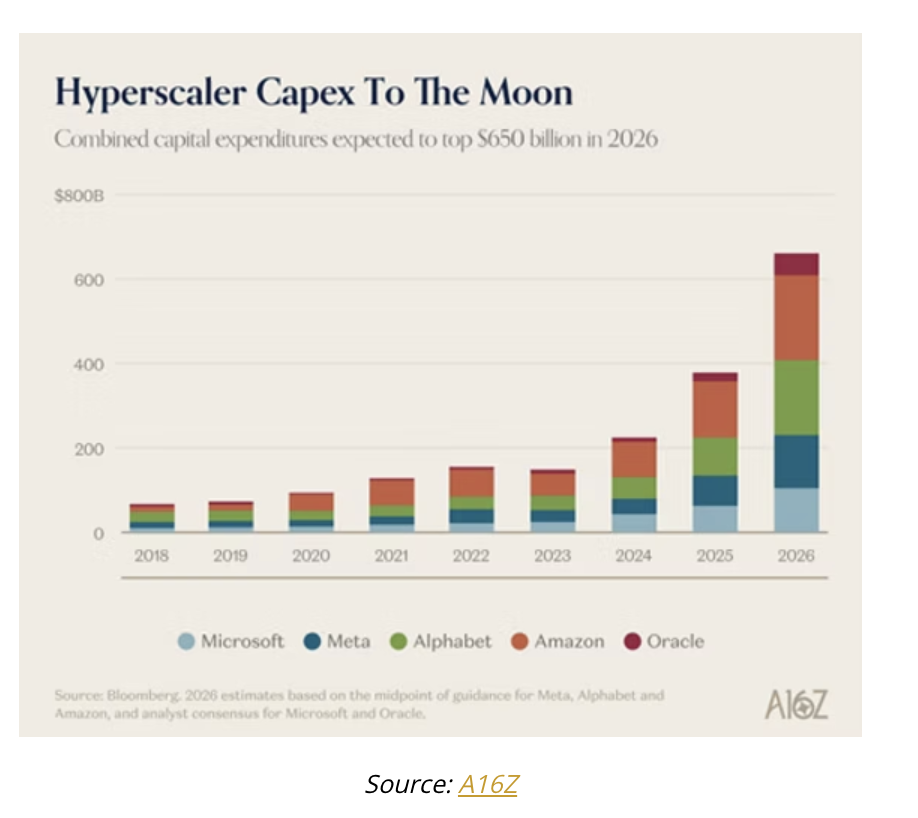

Yes, technology, materials and financials are driving the robust earnings. But in every period there are certain sectors driving the growth of the economy and earnings. And they change and rotate. Right now a lot of people are skeptical about AI and earnings, but the simple fact is that demand for AI and data is rising exponentially, which means that the tech sector which services that demand is growing rapidly. The “hyper-scalers” are seeing their Cap-ex needs grow just as exponentially.

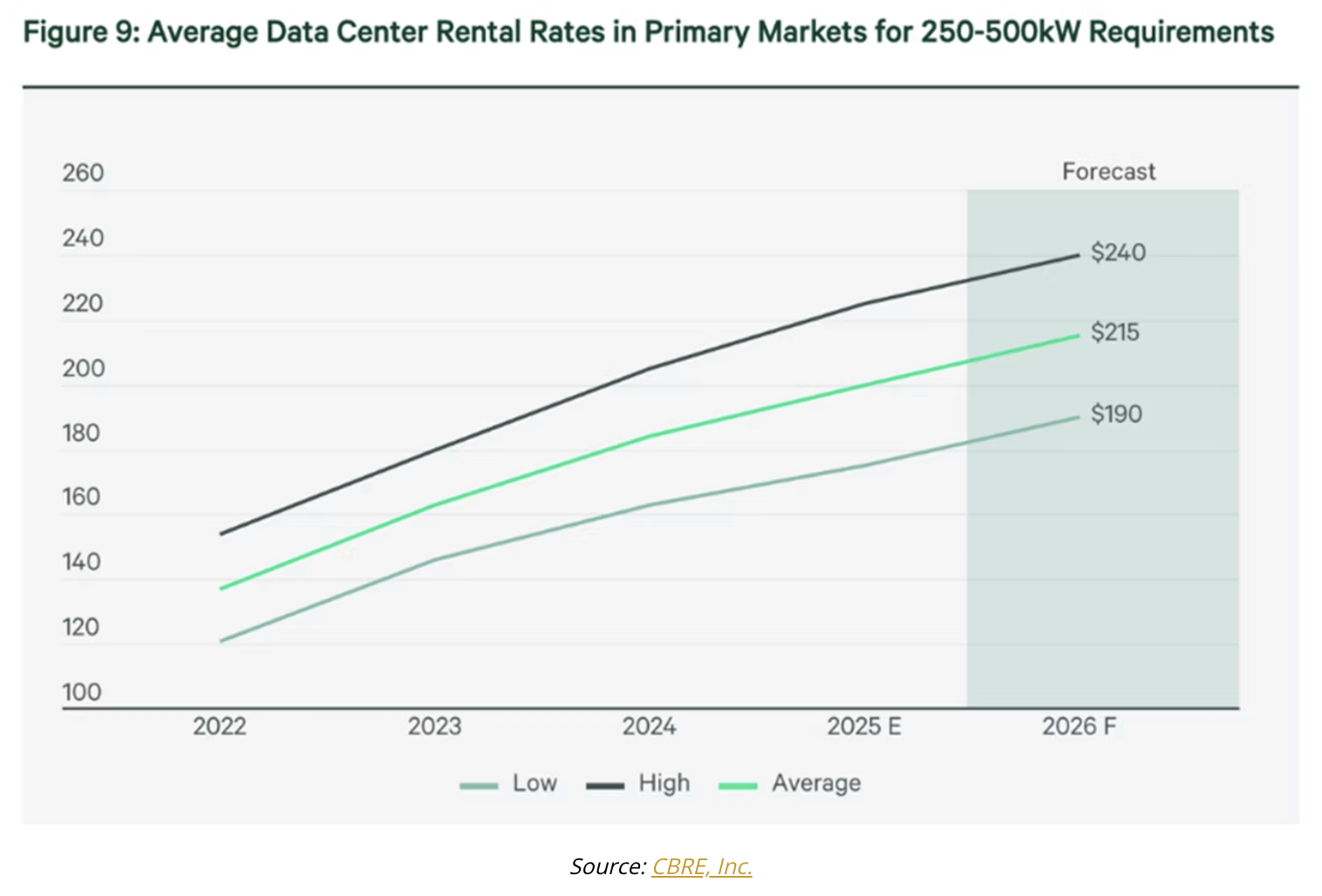

Rents are also rising for the data centers and have been for the last four years. I question whether all of these companies can be the final winners, but certainly management and their boards are all-in on AI and the need to build infrastructure. For them, it is existential. And that increases earnings up and down the line.

By the way, forward earnings multiples for Walmart and Costco are higher than the big tech companies of Microsoft, Google, Meta and Amazon. And the earnings infact are growing faster. You could make the argument that tech is undervalued, although I won’t.

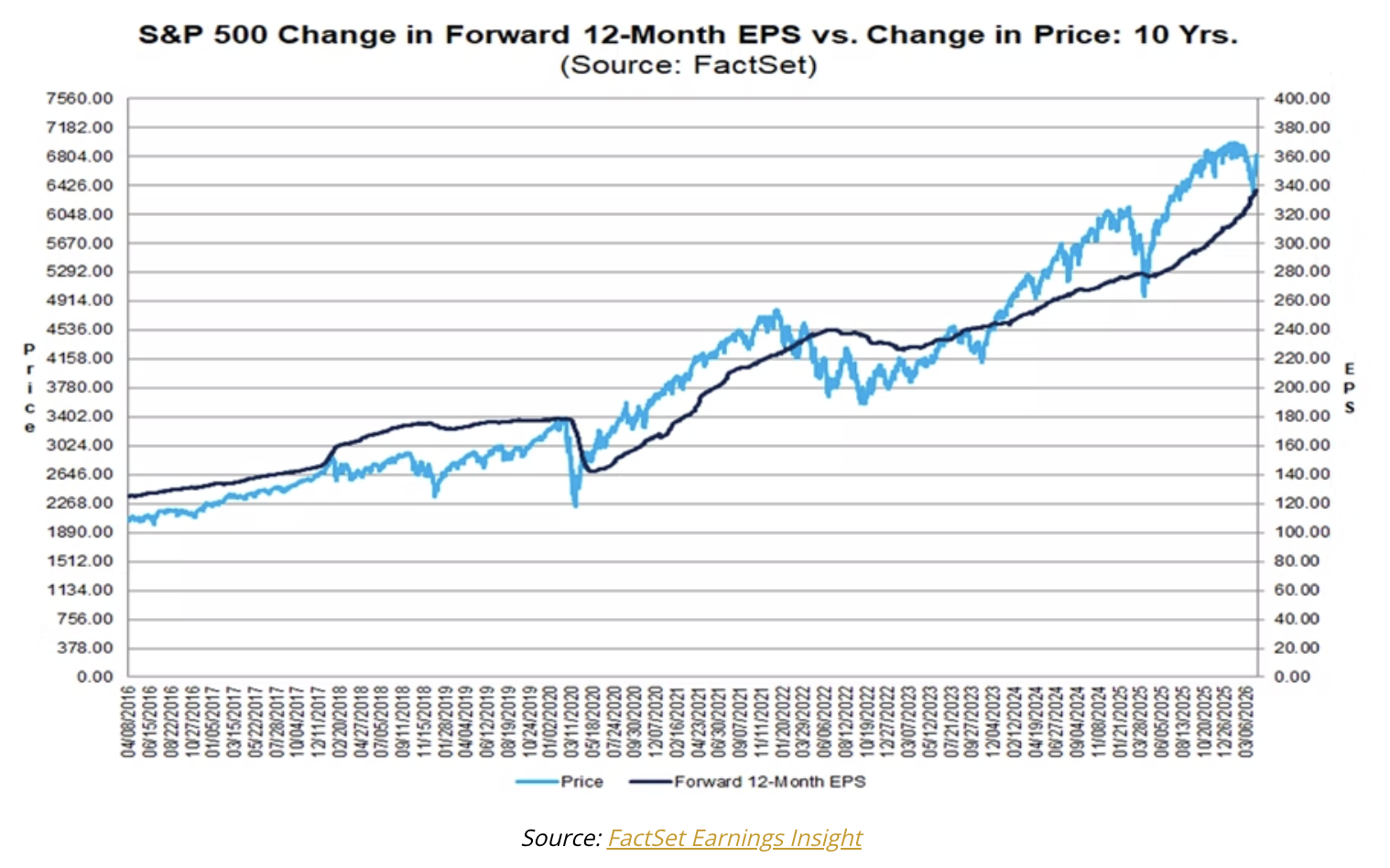

Let’s look at the relationship between earnings and the change in prices for the last 10 years. You could argue that stocks are overvalued, but earnings just keep rising and giving justification to those prices.

As I read the data, the actual forecasted earnings by the companies which show earnings growth for the first quarter of 12.6%. Given that most S&P 500 companies report actual earnings above estimates, what is the likelihood the index will report earnings growth of 12.6% for the quarter? Based on the average improvement in the earnings growth rate during the earnings season, the index could report earnings growth of 19% for Q1. This would be the highest earnings growth rate reported by the index since Q4 2021 (32.0%).

“Over the past five years, actual earnings reported by S&P 500 companies have exceeded estimated earnings by 7.3% on average. During this same period, 78% of companies in the S&P 500 have reported actual EPS above the mean EPS estimate on average. As a result, from the end of the quarter through the end of the earnings season, the earnings growth rate has increased by 7.0 percentage points on average (over the past five years) due to the number and magnitude of positive earnings surprises. If this average increase is applied to the estimated earnings growth rate at the end of Q1 (March 31) of 13.2%, the actual earnings growth rate for the quarter would be 20.2% (13.2% + 7.0% = 20.2%). (FactSet)

There was some moaning about the 9% drawdown of the S&P 500 this past quarter, and more bearish predictions. But that reversed, obviously. The simple fact of the matter is there have only been a few years, even in serious bull markets, where there was not at least one 9% drawdown in a year. It’s that voting versus weighing thing. And right now the continued earnings growth is spurring the markets to increase their “vote.”

Iran and Oil

The controversy around Iran and economic projections are stark. Based on the president’s latest social media posts or something happening in the meetings, oil prices are volatile. As I write, Iran announced that the Strait of Hormuz will be opened. The price of light crude dropped to $82 a barrel in a matter of seconds. If the Strait is actually open, it can drop a lot more. If something happens to derail the negotiations they can rise a lot. We just don’t know.

And that’s okay. If you look at the historical price of energy in inflation-adjusted numbers, the price of energy has been much higher at times and the economy did just fine. Yes, like I said last week, oil prices are effectively a tax on the economy, but it’s not a big one. It might affect GDP by ½ point here and there, but lots of things can do that.

Let’s look at the worst case, at least from my standpoint. Trump and the military significantly underestimate the ability of Iran to survive, the Strait is not opened and Iran gets to keep their nuclear weapons. That would pretty much be a defeat for the US. But that will not kill the US economy. It will certainly weaken the US and much of the world.

But what really happens? Iran gets to charge a toll which will increase oil prices. All of the countries in the Middle East will figure out how to build pipelines and other ways to deliver oil that will offset that. It takes time to build pipelines and alternatives, but it happens and the price of oil goes back down. That is what always happens in every market. Businesses figure out how to reduce their costs and deliver better prices.

The best case? Iran takes the fact that there are boots on the ground in the neighborhood seriously, that they are losing revenue because of Trump’s blockade, and they figure out how to settle. The price of oil will drop back to the $70 range over time.

A middle case, we put boots on the ground and there are military losses which will not be helpful to the mood of the country, but after a longer period, Iran has to come to terms. The price of energy remains high for the next quarter or two before finally turning down. That will be a serious hit to global GDP.

A large portion of your investment portfolio should be focused on how to get in front of earnings growth and predictability. Not on day-to-day price action or geopolitics. Hitting walk-off home runs is something to talk (brag) about, but it is not something that is predictable.

If you can’t relax over the ups and down of data and markets, then you should change your portfolio until you sleep easy at night.

Relax. We are in a Muddle Through world. And that has been good for us for the last 25 years. There are fabulous opportunities out there and our team is working on helping you find them. And to that point…

Final Call for SIC 2026 (Almost)

This is it, our next-to-final call for this year’s Strategic Investment Conference. Well, not for you, of course; surely you’ve already secured your Virtual Pass. I’m talking to those other readers who always wait until the last minute (you know who you are!). You’ve trained us to market right up to the deadline.

This year’s theme, The Global Restructuring, couldn’t be more timely. The era of predictable trade, shared incentives, and borderless capital is ending. Nations are turning inward. Alliances are shifting. Entire industries are being disrupted. Some by policy, others by AI, many by both at once. It demands new thinking. New positioning.

Seriously, look at our lineup. The best ever: Louis Gave, Tyler Cowen, Mark Halperin, George Friedman, Ben Hunt, Joe Lonsdale, Liz Ann Sonders, Danielle DiMartino Booth and 30+ others in their league. No one does conferences like I do. Watch it live or at your leisure. Audio podcasts. Transcripts. It’s all there. Click and see the All-Star faculty. Then sign up here at the discounted rate while it’s still available. Be part of the conversation on how to navigate and invest through, The Global Restructuring.

Boston, Miami And Maybe Europe?

This has been a whirlwind week for me. I started last Friday at a large longevity conference in Palm Beach which was wall-to-wall meetings and conversations. We are making progress. We also opened our Lifespan Edge clinic this past week in West Palm Beach. We will have one in Columbia, Maryland (DC) opened within a few weeks, joining Dallas and Dorado. We literally have dozens of doctors and clinical practices calling us wanting to partner with us. A new powerhouse CEO will help give me some time to focus on my book.

This week has been sensational for me, as I got to be with really good friends like Neil Howe, Mark Mills, Bill Walton and Bruce Mehlman. Then in New York it is always a sensational time when I can be with David Bahnsen, Renè Aninao and Brian Syztel. The next night I got to spend time with Peter Boockvar and friends. Lots of great conversations.

Shane and I are talking about taking a vacation this year which we haven’t done for a while. I am thinking somewhere in Europe but I want to get my book done first.

I may end up going to Miami for a day or two to meet with another company in the longevity space. They really have made some breakthroughs and the data is just powerful. This is happening across the globe. Dr. Mike Roizen in his presentations thinks there is an 80% chance that we will be reversing aging within 10 years. That means that you and I want to try to make it at least another 15. With some of the technology coming along and maintaining a proper lifestyle, you may be living longer than you think.

And with that, I will hit the send button. You have a great week. And click the link to the SIC registration page before you close this letter. You really want to join me.

Your tired but enjoying life analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Mauldin Economics

Read more commentaries by Mauldin Economics