Concerns about the sustainability of U.S. fiscal policy have moved back into the investment spotlight. Over the past week, both multilateral institutions and prominent policymakers have raised warnings about the potential implications of America’s expanding debt burden for Treasury markets. While these concerns are directionally valid, we believe recent calls suggesting a structural loss of appeal for U.S. Treasuries are premature and risk overstating near-term risks.

Rising Debt Issuance and the IMF’s Warning

The International Monetary Fund (IMF) cautioned last week that the accelerating pace of U.S. Treasury issuance may be eroding the premium traditionally afforded to U.S. government securities. As evidence, the IMF pointed to a narrowing spread between yields on AAA-rated corporate bonds and U.S. Treasuries, implying diminished relative demand for sovereign debt.

Separately, former Treasury Secretary Hank Paulson echoed these concerns, suggesting U.S. authorities should prepare contingency plans to address a potential future collapse in Treasury demand driven by investor anxiety over the federal debt trajectory.

There is little debate that U.S. debt dynamics are troubling. Deficits remain large, interest costs are rising, and issuance is likely to continue at elevated levels. However, extrapolating these concerns into a near-term loss of Treasury market credibility or safe-haven status is, in our view, a step too far.

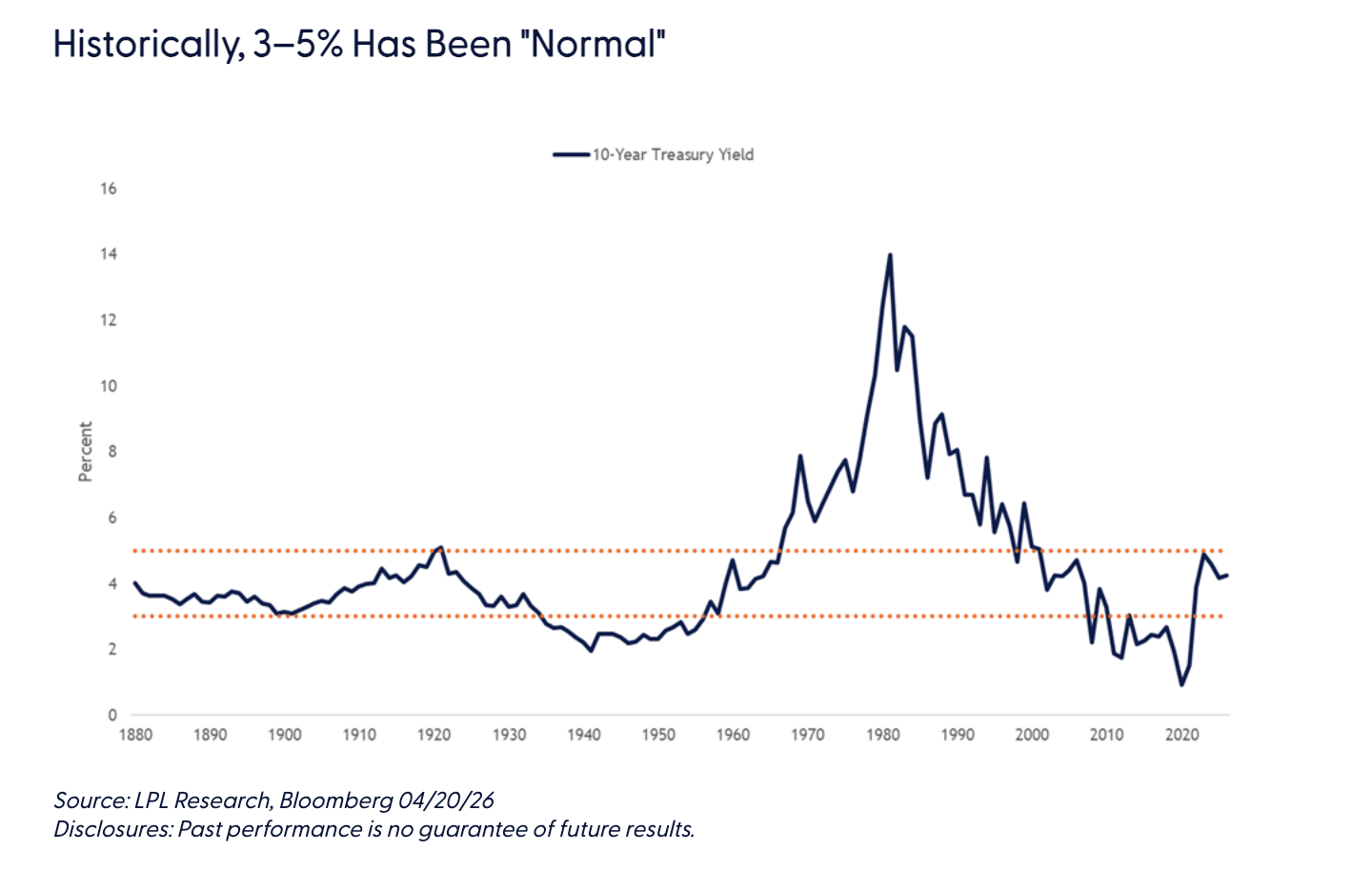

Treasury Yields: Elevated, But Not Abnormal

A basic starting point is the level of Treasury yields themselves. At roughly 4.25%, the 10-year Treasury yield sits close to its long-run historical norm. Since 1880, the 10-year yield has generally oscillated within a roughly 3–5% range, with notable deviations only during distinct monetary regimes: the inflationary excesses of the 1970s and early 1980s, followed by the structurally depressed yields of the post–Global Financial Crisis zero-interest-rate era.

Seen through this longer historical lens, today’s yield levels do not signal investor capitulation or an extraordinary risk premium tied to fiscal fears. Instead, they reflect normalization from an unusually suppressed rate environment.

Read more: Tactical Positioning Update: From Preparation to Action

Corporate Spreads and a Misleading Comparison

The IMF’s focus on the narrowing spread between AAA-rated corporates and Treasuries deserves closer scrutiny. As we discussed in our October 2025 Rate and Credit View, “Can Investment-Grade Corporate Bonds be the New Risk-Free Asset?,” tight investment-grade spreads are largely a function of elevated all-in yields and persistent institutional demand for income-producing assets. Many large buyers — insurance companies, pensions, and asset managers — are focused less on spread levels and more on total yield and balance sheet efficiency.

Moreover, the comparison itself is imperfect. There are currently only two AAA-rated corporate issuers remaining, making broad conclusions based on this cohort somewhat “apples to oranges.” The scarcity value of top-rated corporate paper, combined with structural demand from liability-driven investors, has compressed spreads independently of Treasury supply dynamics.

Auction Performance and Foreign Demand

It is also worth separating “less-than-stellar” Treasury auctions from outright dysfunction. Recent auctions have occasionally been soft at the margin, but coverage ratios and bid-to-cover metrics do not suggest a market that is failing to clear. Importantly, Treasury International Capital (TIC) data released last week showed that foreign demand for U.S. Treasury securities remains robust, undermining the argument that global investors are meaningfully turning away from U.S. government debt. In periods of genuine loss of confidence, foreign official and private-sector demand would be expected to decline sharply. That is not what the data currently shows.

Acknowledging the Long-Term Risk — Without Overreacting

None of this is meant to dismiss the broader concerns surrounding U.S. fiscal sustainability. The trajectory of deficit spending and debt accumulation is unsustainable over the long run, and higher issuance will continue to exert upward pressure on term premiums over time.

However, structural risk and imminent crisis are not the same thing. Treasuries continue to function as the global risk-free asset, anchoring pricing across capital markets and serving as the foundational collateral of the global financial system. That status does not disappear simply because supply is rising.

The Bottom Line: It’s About Price, Not Viability

Despite a growing mountain of debt and rising interest costs, the U.S. government is not on the brink of financial collapse, nor is the Treasury market at risk of losing its haven status in any fundamental sense. As long as Treasuries are treated as risk-free assets — legally, institutionally, and operationally — there will be buyers, and deficits will be financed.

The more relevant question is not whether Treasuries will be bought, but at what price. To date, the evidence suggests that investors have not balked at current prices. Concerns about U.S. debt are real, and deserve attention — but declarations of the end of Treasury exceptionalism remain, for now, exaggerated, in our view.

As well, despite the ongoing conflict in Iran, market-based indicators do not currently suggest rising stress in the Treasury market. Interest rate volatility, as measured by the MOVE index, spiked sharply at the onset of the conflict but has since retreated to levels below those observed prior to the war. Similarly, the Treasury term premium — the additional compensation investors demand to hold longer‑dated Treasury securities — is hovering near its average level over the past year and remains well below recent highs.

Historically, the combination of declining interest rate volatility and a subdued term premium is consistent with a market environment characterized by increasing confidence in central bank policy, diminished recession risks, and adequate market liquidity. Put differently, investors are currently requiring less compensation to hold long‑term Treasuries because they perceive a lower probability of extreme rate volatility or sustained inflation surprises.

All that said, given the considerable uncertainty surrounding the depth, duration, and potential spillover effects of the Iran conflict, markets may be underpricing upside risks to the 10‑year Treasury yield. As a result, while Treasuries continue to function as a core portfolio anchor, we remain neutral on duration relative to benchmarks.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1094468

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial