Additional content provided by Brian Booe, Associate Analyst, Research.

With the proverbial ceasefire negotiation can kicked down the road for the second time in a week, the U.S. and Iran remain in a stalemate over the Strait of Hormuz. While equity markets have bounced back this month, seemingly moving on to the more upbeat fundamental and macro backdrop, and crude oil futures have dropped off their March highs, the physical supply squeeze for oil may be somewhat underappreciated by investors. Entering 2026, crude oil over supply was expected to be a headwind for energy prices, but damage to the energy infrastructure and production cuts in the Middle East have accelerated uncertainty around the supply crunch sparked by the Strait of Hormuz closure. For perspective, one-fifth of global supply typically traverses the Strait, but roughly 23,000 outbound kilobarrels of crude oil have passed the waterway since March 1 (just under 1.5 days’ worth, based on the one-year average before the conflict). Early-year oversupply has helped absorb the immediate shock better than feared, while markets still face normalization that could take months.

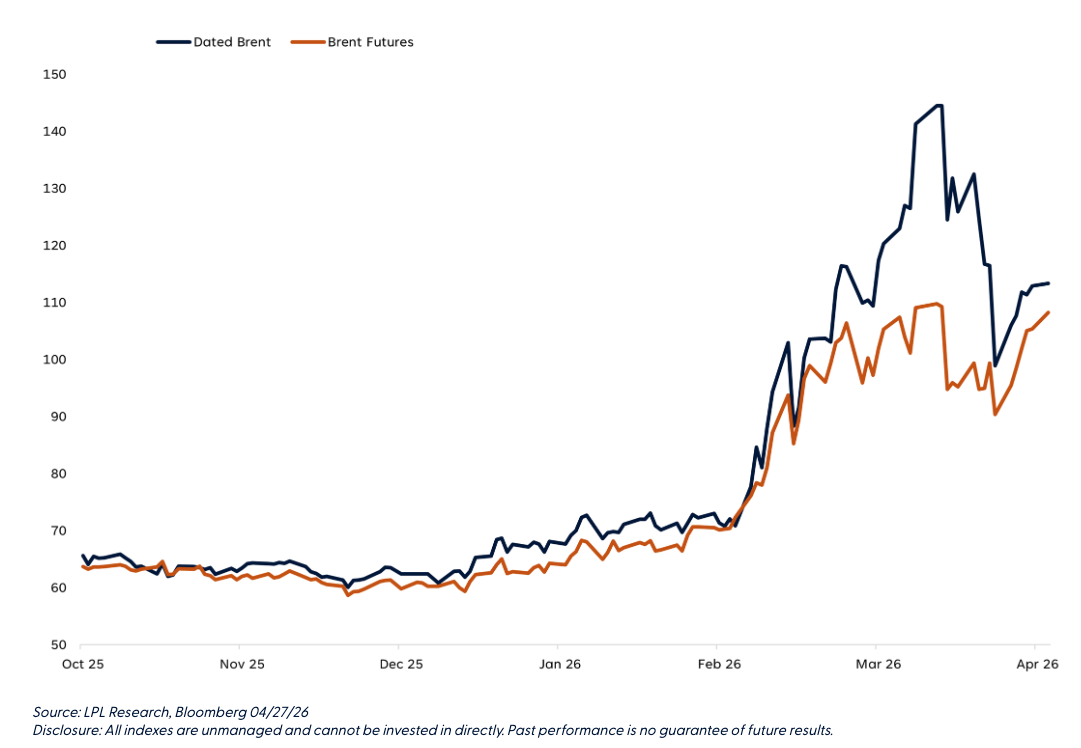

Headlines have broadly focused on futures prices across the so-called paper market, but what slipped under the radar was a disconnect beginning in mid-March between the physical market. As evidence of the supply squeeze, futures prices remain lower than dated Brent prices (the benchmark for physical oil prices) and have resumed moving higher despite coming back to earth a bit after soaring past $140 per barrel before the U.S.-Iran ceasefire.

Dated Brent and Brent Futures Remain Disconnected

Considering that the final cargoes that departed the Strait of Hormuz before the conflict arrived at their destinations during the week of April 13, simply securing barrels of crude is rapidly becoming paramount. Japanese refiners have snapped up U.S. oil, Chinese refiners drove shipments from Vancouver to record highs, and India has lifted purchases of Venezuelan oil, and reports indicate traders at some Asian refineries reportedly disregarded price in recent transactions.

Although futures prices may fall following the first headlines of a durable reopening of the Strait, the futures curve suggests a new floor for crude has been set as impacts in the physical market linger, potentially leading to a structural change for energy surrounding a shift from a just-in-time market to one involving a renewed importance in strategic inventory reserves.

What’s the Buzz Around the Petrodollar?

Another hot topic related to the physical oil squeeze has been the so-called death of the petrodollar. However, we don’t believe the petrodollar dynamic (a product of a 1970s U.S. agreement with Saudi Arabia to price oil in dollars, which has fueled capital recycling into U.S. assets) is over. Iran accepting tolls in Chinese yuan sparked angst around the end of the petrodollar, but the idea of a “petroyuan” seems farfetched as a meaningful shift would take years (potentially decades), not weeks or even months. We note the offshore petrodollar may not be as potent during this shock as in the past, given a few factors. One being Gulf States’ shift away from investing in traditional reserve assets (like U.S. Treasuries and dollars) toward sovereign funds buying equities. Another being the Saudis issuing dollar-denominated bonds rather than solely buying them. And of course, reduced Middle East energy sales from the Strait of Hormuz closure. But the U.S. acting as a net exporter will likely keep North American oil flush with onshore dollars.

What About Equities?

What about equities? Well, as evidenced by global market performance since the end of February, the impacts of higher oil prices are not felt equally across the globe. The U.S. has firmly established itself as a net exporter of total petroleum products. This provides domestic equities with relative insulation compared to the rest of the world, and U.S. equities also display less exposure to overseas revenue compared to their global counterparts — likely acting as a buffer from spillover across the Atlantic and Pacific. Developed international markets, however, are more exposed.

As European underperformance during the conflict suggests, higher energy and raw-materials costs may pressure margins, limiting the runway for European earnings growth. Plus, with inflation often “imported” as energy prices rise, market expectations of a European Central Bank and Bank of England rate hike have risen for this summer. Despite the shock being treated as a temporary, near-term inflation disruption by markets rather than a policy regime change, more restrictive monetary policy may challenge the upside potential for European stocks over a tactical time frame.

Japanese equities remain acutely exposed given approximately 88% of the archipelago’s oil imports originate from the Middle East. However, equities have displayed some resilience with the recent rebound in tech shares supporting benchmarks — a similar story to the emerging markets across Asia as exchanges without a sizable technology sector, such as Thailand and Indonesia, have been hampered by oil prices and the supply crunch compared to the tech-leaning markets of South Korea and Taiwan.

Conclusion

This historic energy supply shock does warrant monitoring by investors. Market pricing suggests higher oil prices may linger, and physical markets potentially face a structural shift as supply normalization will take time. However, we don’t believe this spells doom and gloom for the dollar or equity markets. The U.S. dollar index has strengthened since the start of the conflict and its reserve status remains secure. Calls for the end of the petrodollar may be over the top. Given both Washington and Tehran appear committed to holding the temporary ceasefire and working towards an agreement on the Strait of Hormuz, equity trading will likely continue refocusing on fundamentals, leaving the effects from the de facto closure of the waterway an undertone. In the near-term, we expect the U.S. to outperform developed international and emerging markets as tech-driven earnings strength will likely outweigh smaller relative drags from the oil shock.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1097803

Read more commentaries by LPL Financial