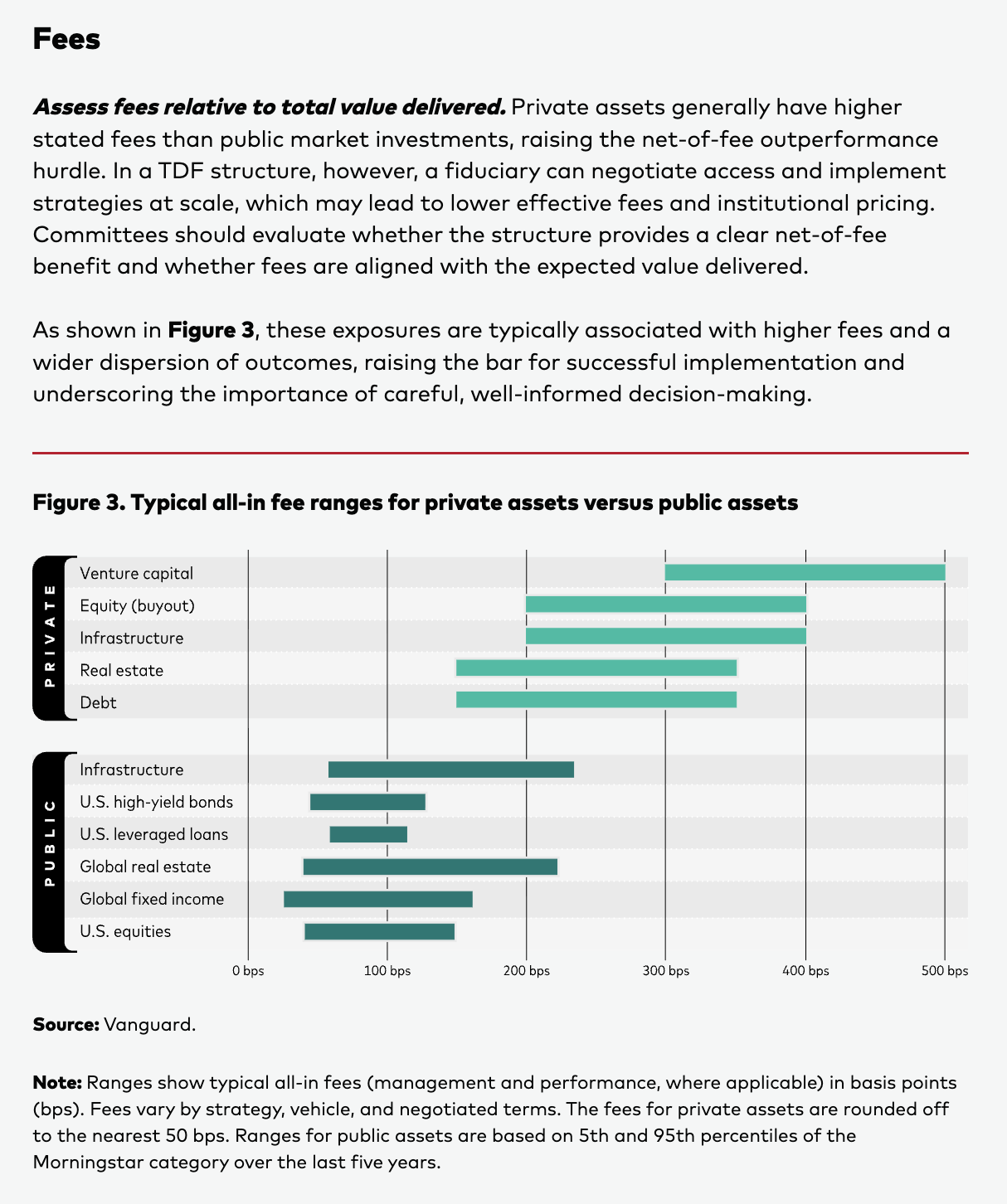

Access to private equity, private credit, private infrastructure, and private real estate assets can potentially improve long-term investment outcomes for participants.

This article outlines a fiduciary evaluation framework for defined contribution (DC) plans and target-date fund (TDF) providers, focusing on six key considerations: performance, fees, liquidity, valuation, meaningful benchmarks, and complexity.1 Together, these considerations frame the governance and implementation approach needed to assess the appropriate role of private assets in target-date design.

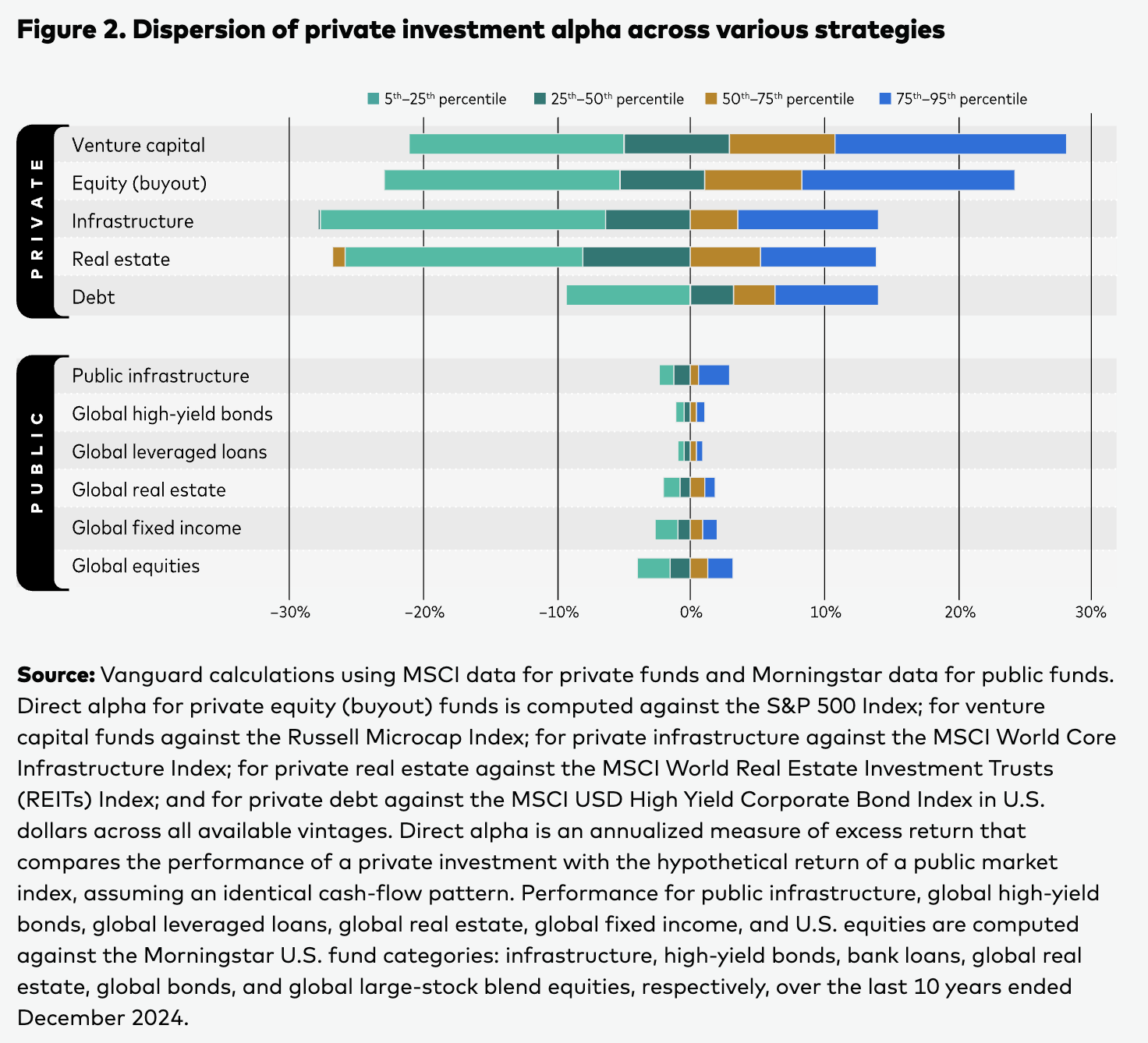

Our research affirms that the investment case is straightforward. Integrating private assets may (1) enhance returns through a liquidity premium, (2) benefit from an active management skill set, and (3) improve diversification through new sources of return. Private markets have also expanded significantly, growing from less than $1 trillion in 2006 to more than $10 trillion today.2 Currently, 85% of U.S. companies with more than $100 million in revenue are private.3 We believe this makes private assets a worthwhile opportunity to explore and evaluate.

Implementation, however, is more complex. There is no widely available, low-cost private market index fund. In practice, the active management required for adding private assets can potentially include higher fees, less transparency, and a wider range of outcomes. Currently, very few participants can access private assets through self-directed DC plans, though policymakers and industry stakeholders are exploring ways to extend access to everyday investors. Against this backdrop, investment managers are devoting considerable time and resources to addressing these challenges with the view that, through thoughtful design, prudent oversight, and clear guardrails, private assets can be integrated into TDFs in a way that manages risks responsibly while expanding the opportunity set for retirement savers.

For DC plans, most investment activity is concentrated in qualified default investment alternatives. Over the past decade, the percentage of participant contributions directed into TDFs rose from 46% in 2015 to 64% in 2025.4 Incorporating private assets into TDFs—where allocation and oversight are professionally managed—has the potential to expand adoption among DC plan participants. Figure 1 illustrates the growing share of private investments within global equity markets, underscoring the increasing role of private assets in the broader investment landscape.

Read more: (More) Roses Amid Garbage and Trap Doors

The bottom line: Advantages of private markets in retirement plans

Overall, the potential benefits of private assets in TDFs make them a worthwhile area for committees to explore and evaluate, particularly as part of the ongoing evolution of target‑date design. When thoughtfully implemented, a private asset sleeve can enhance long‑term participant outcomes, but success depends on more than simple inclusion. It requires a rigorous investment process, strong governance, disciplined implementation, and clear alignment with participant needs and behaviors. For many committees, this means carefully evaluating available solutions, establishing a governance framework that can remain resilient across market environments, and selecting a provider with a well‑established, repeatable, and transparent implementation approach.

Glossary

Evergreen fund: Usually refers to an open‑ended, perpetual investment vehicle with no fixed termination date, designed to continuously raise, deploy, and reinvest capital. Unlike closed‑end private funds, it generally permits periodic subscriptions and redemptions, subject to liquidity constraints. In private assets, evergreen structures enable sustained, multivintage exposure while supporting disciplined cash‑flow and liquidity management.

Private equity (buyout): Typically refers to acquiring controlling stakes in companies and working to improve and grow earnings over several years. In a retirement portfolio, buyout exposure can serve as a long-term growth allocation that may enhance return potential, but it usually requires a long horizon because outcomes can vary and capital may be tied up for extended periods.

Private credit: Generally involves lending to companies outside the public bond market in exchange for contractual interest payments and repayment of principal. Private credit can play an income-oriented role in the portfolio, potentially offering a steadier return stream over equity-like private assets while still carrying meaningful credit risk that tends to emerge during economic downturns.

Private infrastructure: Usually refers to investing in long-lived, essential assets, such as utilities, transportation networks, and communications systems, where revenues are often supported by contracts or regulated pricing. In a retirement portfolio, private infrastructure can offer a long-term inflation hedge and help balance exposure to traditional stocks and bonds.

Private real estate: Typically involves owning or financing properties, with returns driven by rental income and changes in property values over time. Private real estate can provide income and real-asset exposure that may be beneficial in certain inflationary environments, but it is also sensitive to interest rates and local market conditions, underscoring the importance of diversification across property types and regions.

Because the four private asset categories differ in cash-flow patterns, valuation behavior, and liquidity, return expectations are adjusted for reduced flexibility before being incorporated into portfolio design.

Sources:

1 Private Assets in Defined Contribution Plans: Benefits, Risks, and Implications. Vanguard, 2025.

2 An estimate using MSCI for private equity and total global market capitalization for public equity suggests that private equity accounted for approximately 6% of total global equity as of December 31, 2024.

3 S&P Capital IQ, as of April 2024.

4 How America Saves 2025. Vanguard.

5 See Glossary section for definition.

Notes:

For more information about any fund, visit workplace.vanguard.com or call 866-499-8473 to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

Investments in Target Retirement Funds and Trusts are subject to the risks of their underlying funds. The year in the fund or trust name refers to the approximate year (the target date) when an investor in the fund or trust would retire and leave the workforce. The fund/trust will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. The Income Trust/Fund and Income and Growth Trust have fixed investment allocations and are designed for investors who are already retired. An investment in a Target Retirement Fund or Trust is not guaranteed at any time, including on or after the target date.

Vanguard Target Retirement Trusts are not mutual funds. They are collective trusts available only to tax-qualified plans and their eligible participants. Investment objectives, risks, charges, expenses, and other important information should be considered carefully before investing. The collective trust mandates are managed by Vanguard Fiduciary Trust Company, a wholly owned subsidiary of The Vanguard Group, Inc.

Vanguard is responsible only for selecting the underlying funds and periodically rebalancing the holdings of target-date investments. The asset allocations Vanguard has selected for the Target Retirement Funds are based on our investment experience and are geared to the average investor. Regularly check the asset mix of the option you choose to ensure it is appropriate for your current situation.

All investing is subject to risk, including the possible loss of the money you invest. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss. Past performance is no guarantee of future results.

With private equity (PE) investments, there are five primary risk considerations: market, asset liquidity, funding liquidity, valuation, and selection. Certain risks are believed to be compensated risks in the form of higher long-term expected returns, with the possible exceptions being valuation risk and selection risk. For selection risk, excess returns would be the potential compensation; however, limited partners (LPs) must perform robust diligence to identify and gain access to managers with the skill to outperform. PE investments are speculative in nature and may lose value.

Market risk: Private equity, as a form of equity capital, shares similar economic exposures as public equities. As such, investments in each can be expected to earn the equity risk premium, or compensation for assuming the nondiversifiable portion of equity risk. However, unlike public equity, private equity's sensitivity to public markets is likely greatest during the late stages of the fund's life because the level of equity markets around the time of portfolio company exits can negatively affect PE realizations. Though PE managers have the flexibility to potentially time portfolio company exits to complete transactions in more favorable market environments, there's still the risk of capital loss from adverse financial conditions.

Asset liquidity risk: Various attributes can influence a security's liquidity; specifically, the ability to buy and sell a security in a timely manner and at a fair price. Transaction costs, complexity, and the number of willing buyers and sellers are only a few examples of the factors that can affect liquidity. In the case of private equity, while secondary markets for PE fund interests exist and have matured, liquidity remains extremely limited and highly correlated with business conditions. LPs hoping to dispose of their fund interests early—especially during periods of market stress—are likely to do so at a discount.

Funding liquidity risk: The uncertainty of PE fund cash flows and the contractual obligation LPs have to meet their respective capital commitments—regardless of the market environment—make funding risk (also known as commitment risk) a key risk LPs must manage appropriately. LPs must be diligent about maintaining ample liquidity in other areas of the portfolio, or external sources, to meet capital calls upon request from general partners (GPs).

Valuation risk: Relative to public equity, where company share prices are published throughout the day and are determined by market transactions, private equity net asset values (NAVs) are reported quarterly, or less frequently, and reflect GP and/or third-party valuation provider estimates of portfolio fair value. Though the private equity industry has improved its practices for estimating the current value of portfolio holdings, reported NAVs likely differ from what would be the current “market price,” if holdings were transacted.

Selection risk: Whether making direct investments in private companies, PE funds, or outsourcing PE fund selection and portfolio construction to a third party, investors assume selection risk. This is because private equity does not have an investable index, or rather a passive implementation option for investors to select as a means to gain broad private equity exposure. While there are measures an investor can take to limit risk, such as broad diversification and robust manager diligence, this idiosyncratic risk cannot be removed entirely or separated from other systematic drivers of return. Thus, in the absence of a passive alternative and significant performance dispersion, consistent access to top managers is essential for PE program success.

© 2026 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor of the Vanguard Funds.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Vanguard

Read more commentaries by Vanguard