The accelerating adoption of artificial intelligence technology is transforming many sectors of the global economy with remarkable speed, as we’ve discussed in Macro Signposts in January and February. Since we wrote those pieces, massive demand for AI – and for all the innovations, components, infrastructure, and energy that underpin it – has begun to augment inflationary pressures in the U.S. That price pressure is likely to continue given AI’s growing implications for national security.

However, in the medium to longer term, as the economy responds to AI’s influence, the pressures could turn disinflationary – especially if less of the overall income that AI fosters diffuses to workers and consumers.

Supercharging AI investment

In the past year, new models from industry leaders have continued to boost AI’s capabilities. According to various capabilities tests, Anthropic’s Mythos model has leapfrogged other AI models – including in the ability to thwart or support cyberattacks. As this has coincided with geopolitical flash points, including the war in Iran, the discussion in many organizations and governments seems to be shifting from AI as a means to increase efficiency and productivity to AI as a necessary technology to counter national security threats – including large-scale cyberattacks.

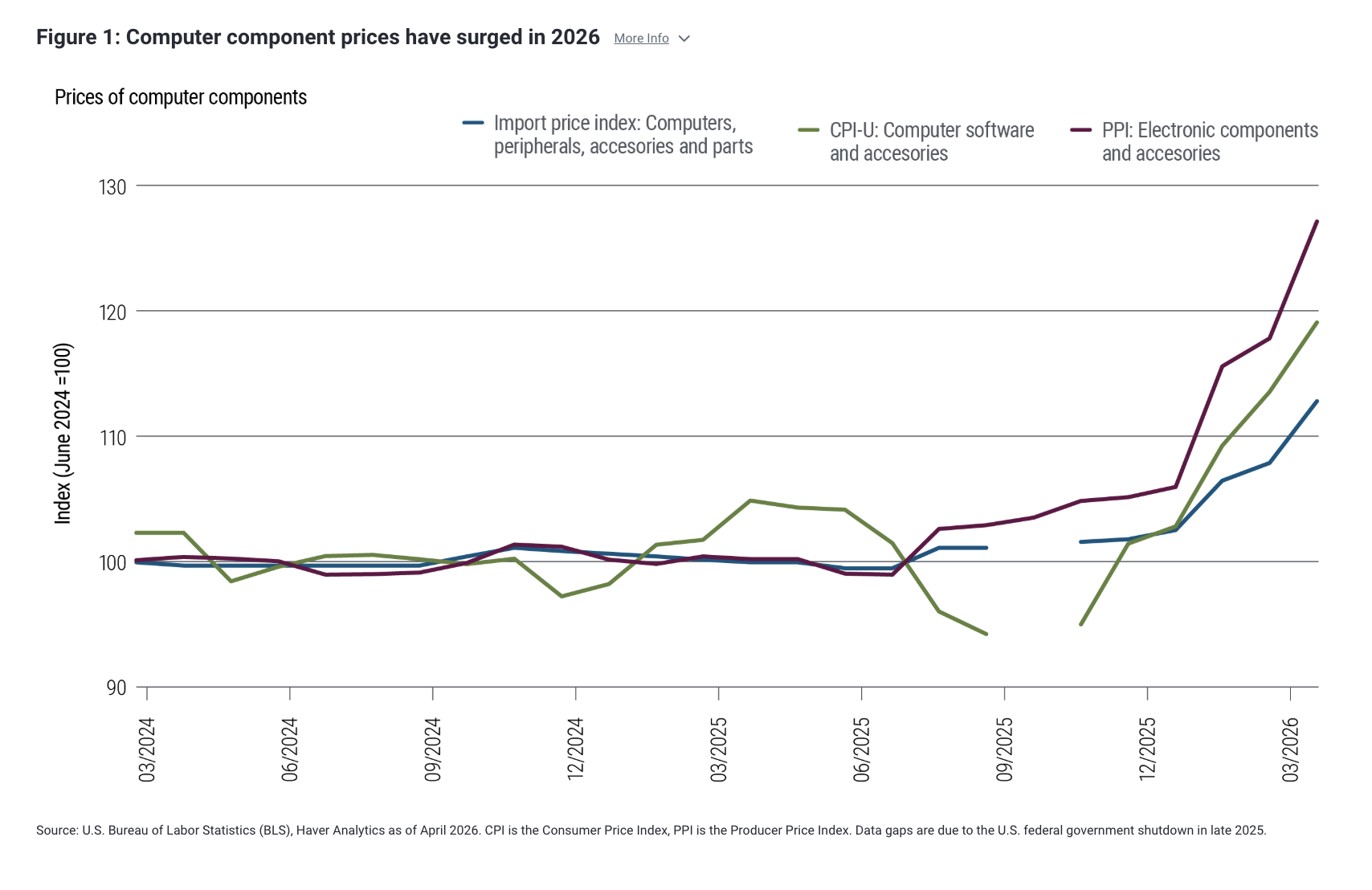

Meanwhile, despite the largest global energy supply-side shock in decades, expectations for AI-driven productivity gains have continued to buoy asset prices while U.S. investment in AI implementation and infrastructure has accelerated. The current confluence of factors appears to have created a new sense of urgency that has pulled forward demand for chips, memory cards, and other components, and their prices are skyrocketing, according to government data (see Figure 1).

The AI theme is providing a positive short-run boost to U.S. demand, and the consumer prices of computers, memory, gaming components, and other AI-adjacent products are shifting higher. And given these items’ higher relative weight in the Federal Reserve’s preferred inflation measure – the Personal Consumption Expenditures (PCE) Index – we’re seeing upward pressure on PCE inflation. This complicates the Fed’s job as it also deals with spillovers from the energy price spikes into core sectors such as travel services (see Macro Signposts, “U.S. Inflation Measures Tell Two Different Stories”). Indeed, markets are now pricing the Fed to hike rates in 2027 – though that is not our base case.

While markets and the Fed contend with the near-term economic impacts of AI, we shouldn’t lose sight of the medium-term effects. AI can expand the frontier of what’s possible, but the resulting gains may not be spread evenly across the economy. Capital, and some areas of skilled labor, may see the lion’s share.

As fewer of the gains of a potentially more efficient, productive, even affluent U.S. economy accrue to its workers – and real wages lag – the impact over time could be more disinflationary (albeit with possible policy-driven price swings).

Read more: What Would The Merton Model Say About AI Capital Spending?

Why unemployment isn’t always the best benchmark

We don’t need structurally higher unemployment – an inevitable outcome of AI, according to some industry insiders – for the gains from AI to be disproportionately captured by capital holders.

Taking a step back: Concerns that technological change would produce mass unemployment are not new. John Maynard Keynes warned of “technological unemployment” in 1930, and similar forecasts have surfaced with each major technological advancement.

However, history’s empirical evidence suggests that technological advances don’t structurally increase unemployment over time. Since 1960, U.S. labor productivity has increased nearly fourfold, while aggregate labor hours have risen roughly 2.3 times – broadly in line with the growth in labor supply (according to the Bureau of Labor Statistics or BLS). Across decades of profound innovations and transformations, the U.S. hasn’t experienced persistent mass unemployment.

That doesn’t mean technological change has been painless: It has displaced whole sectors of workers, while reallocating labor elsewhere. For example, the U.S. economy experienced a major reallocation away from manufacturing toward services in the 2000s. The internet revolution enabled easier outsourcing to China and other countries via innovations such as item tracking, just-in-time inventory systems, and improved communication across fragmented supply chains. Technology made it easier to separate physical production from design and management – a trend that trade economist Richard Baldwin termed the “second unbundling.”

The costs of this change were very real for workers. In the U.S., it wasn’t only a shift away from manufacturing employment, which coincided with de-unionization and lower labor bargaining power. As research from MIT’s David Autor has shown, some cohorts – particularly prime-working-age men – exited the labor force entirely.

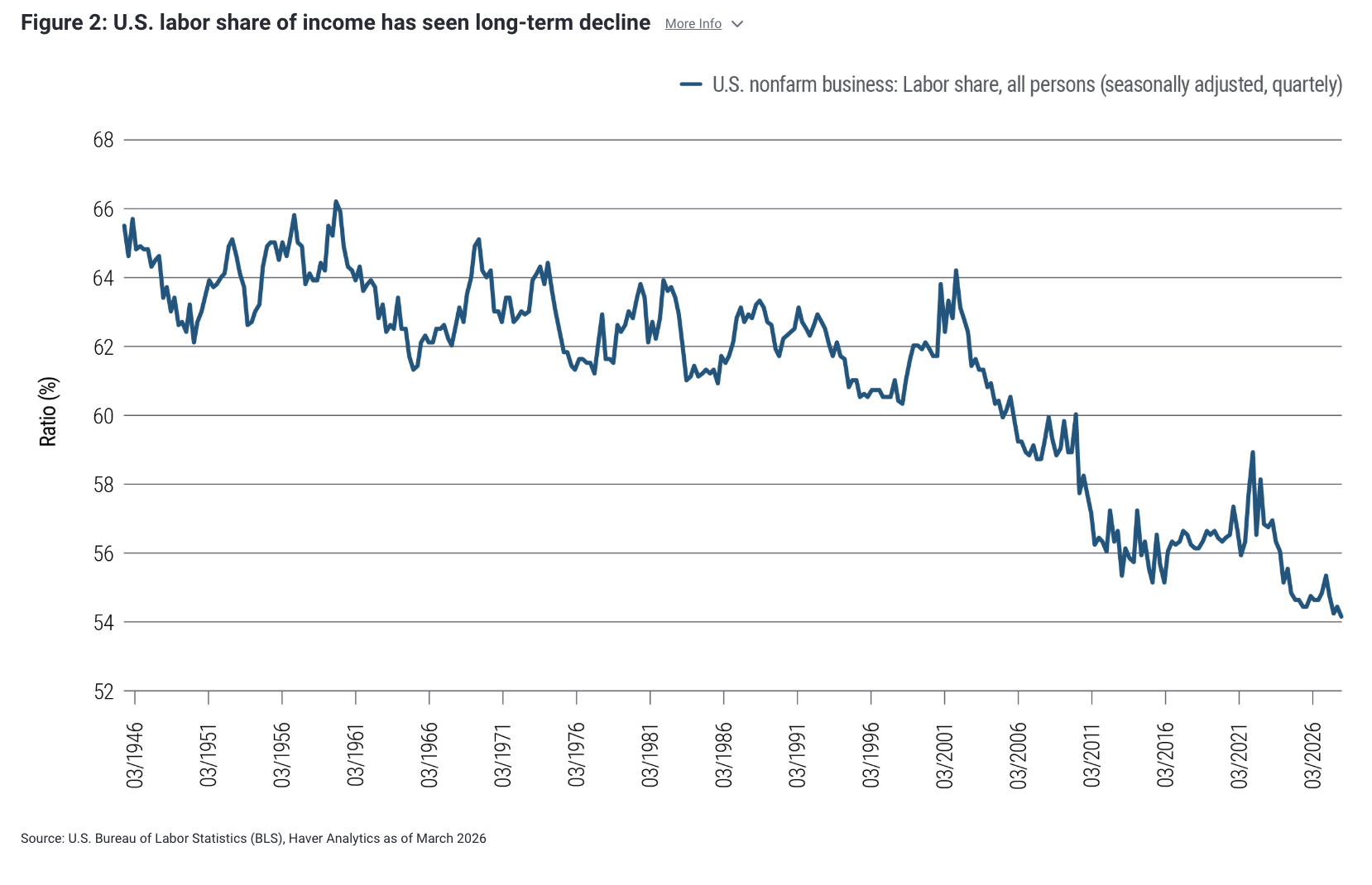

The long decline in U.S. labor share

Over the decades, a more informative indicator for measuring the impact of technological change has been labor share of income.

From the 1940s to around 1980, rising U.S. productivity coincided with a broadly stable labor share of income. Government investment in research, infrastructure, industrial capacity, and nuclear and space technology spilled over into the real economy, elevating productivity growth especially in the 1960s. During this period, technological progress and higher productivity benefited the manufacturing sector, but were largely complementary to domestic labor. In other words, U.S. workers were able to capture a generally consistent share of the gains.

Since the 1980s, however, that relationship has weakened. The labor share of income has trended lower, particularly since the 2000s (see Figure 2), as technology allowed for globalized production and supply chains that unlocked a large supply of low-cost labor. These labor share trends can be seen globally as well as in the U.S., across both net and gross indicators of labor share.

The benefits of technological gains over this period not only broadly favored capital over labor, but also favored skilled workers over less-skilled ones. Real wages for lower-skilled U.S. workers have been stagnant or declining since the 2000s (according to the BLS) – a pattern often described as skill-biased technological change.

Similar to what we saw in the 2000s, AI will likely disrupt some sectors and occupations more than others, but over time the economy will likely reallocate labor toward tasks that AI cannot perform. Sectors such as healthcare, education, and construction are already absorbing labor, reflecting both current technological limits and demographic demand. A key question is whether this reallocation will result in real wages keeping up with productivity.

Why labor share is particularly vulnerable

Two structural features of AI contribute to the risks for labor share.

First, substitution and scalability: AI is highly scalable, and it’s more likely to substitute for, or more narrowly complement, labor than to broadly augment it, relative to past technological innovations. In other words, AI will likely reduce the relative price of investment as it substitutes for what used to be labor-intensive tasks. The pace of technological progress and diffusion is also moving much faster than in the past, risking greater displacement before new labor-intensive tasks are generated at similar wage levels. Research by Eloundou et al.1 maps tasks and occupations exposed to AI. Based on that research, we estimate that roughly 4%–7% of the overall U.S. labor market faces a high likelihood of displacement – while a much larger share faces at least some task displacement in their current roles. Sectors such as IT, professional services, and finance – sectors that tended to pay higher relative wages before AI – are most exposed. Sectors least exposed – healthcare, personal services, food services, and construction – tend to have lower relative wages.

Second, the rising market power of hyperscalers: As AI adoption increases, hyperscalers are accumulating large and asymmetric knowledge bases. This may increase their market power and ability to capture a larger share of value. A recent research paper by an AI developer2 demonstrated it can easily synthesize how end users are using its models. Based on workflow utilization, this developer can map the actual tasks currently being displaced to the frontier of possible tasks ripe for automation and displacement (as outlined by Eloundou et al.). This concentration of information makes it more likely than in the past that a small subset of companies can increase markups and profits.

Broader implications of declining labor share

Higher productivity and a declining labor share of income imply that higher average living standards could come at the cost of persistently elevated inequality in income and wealth. If history is a guide, this could coincide with further shifts in median voter preferences toward more populist policies, while laissez-faire regulatory approaches may give way to greater government intervention to bolster populations facing the starkest challenges.

How governments intervene in AI is a separate question. AI might now be thought of as a national security imperative, analogous to the nuclear arms race of the mid-20th century. Leading AI firms are viewed as national champions. Over time, however, policymakers may need to balance national security priorities against the risks and costs of increasing market concentration, labor reallocation, and declining labor share of income – especially if under pressure from voters. We see evidence of AI backlash in polling and anti-data-center sentiment.

For investors, this time of heightened uncertainty suggests a focus on resilience – greater diversification, greater flexibility, reduced concentration, and active management. Some have argued that AI is increasing (and will continue to increase) the natural, or neutral, interest rate – what central bankers call r* – as investment demand and productivity rise.

However, we aren’t so certain. Higher demand for savings due to an increasingly uncertain labor market reallocation could offset the higher investment demand for AI infrastructure and other investments. As recently pointed out by New York Fed President John Williams – author of an influential 2003 paper on measuring the natural rate of interest – historically, factors that have driven down labor share of income have coincided with a lower r*. Research has also linked higher inequality to lower r*.

Footnotes

1 Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock. “GPTs are GPTs: An Early Look at the Labor Market Impact Potential of Large Language Models.” arXiv .org paper 2303.10130 (revised August 2023). ↩

2 Maxim Massenkoff and Peter McCrory. “Labor market impacts of AI: A new measure and early evidence.” Anthropic Economic Research (March 2026). ↩

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0520-5509613

© PIMCO

Read more commentaries by PIMCO