Key takeaways

-

AI is fueling a new, debt-driven investment cycle: Even as hyperscalers start from a position of strong balance sheets, rising capital spending and falling free cash flow signal a shift toward leverage.

-

Big questions are still unresolved: Investors face wide-ranging potential outcomes and layered risks as demand, value creation, and returns across the AI ecosystem remain uncertain, making selection and structure critical.

-

History offers a cautionary guide, if not a perfect template: Past infrastructure booms – from railroads to telecom – show that transformational technologies can still lead to overinvestment and uneven returns.

Since the post-COVID recovery began, U.S. nonfinancial corporations have generally managed capital conservatively. They have kept credit metrics stable and, in many cases, actively improved them. That discipline was not entirely voluntary: The sharp adjustment in funding costs triggered by the Federal Reserve’s 2022–2023 rate hiking cycle raised the bar for incremental borrowing and pushed management teams toward balance sheet restraint.

Over the past 18 months, however, one corner of corporate America has broken decisively from that pattern. AI-related capital expenditure has increasingly turned to debt markets for funding, not just among the major investment grade (IG) hyperscalers, but also among neoclouds in high yield (HY). (Hyperscalers are massive-scale cloud service providers for general purposes, while neoclouds are specialized cloud service providers focused on AI processing.)

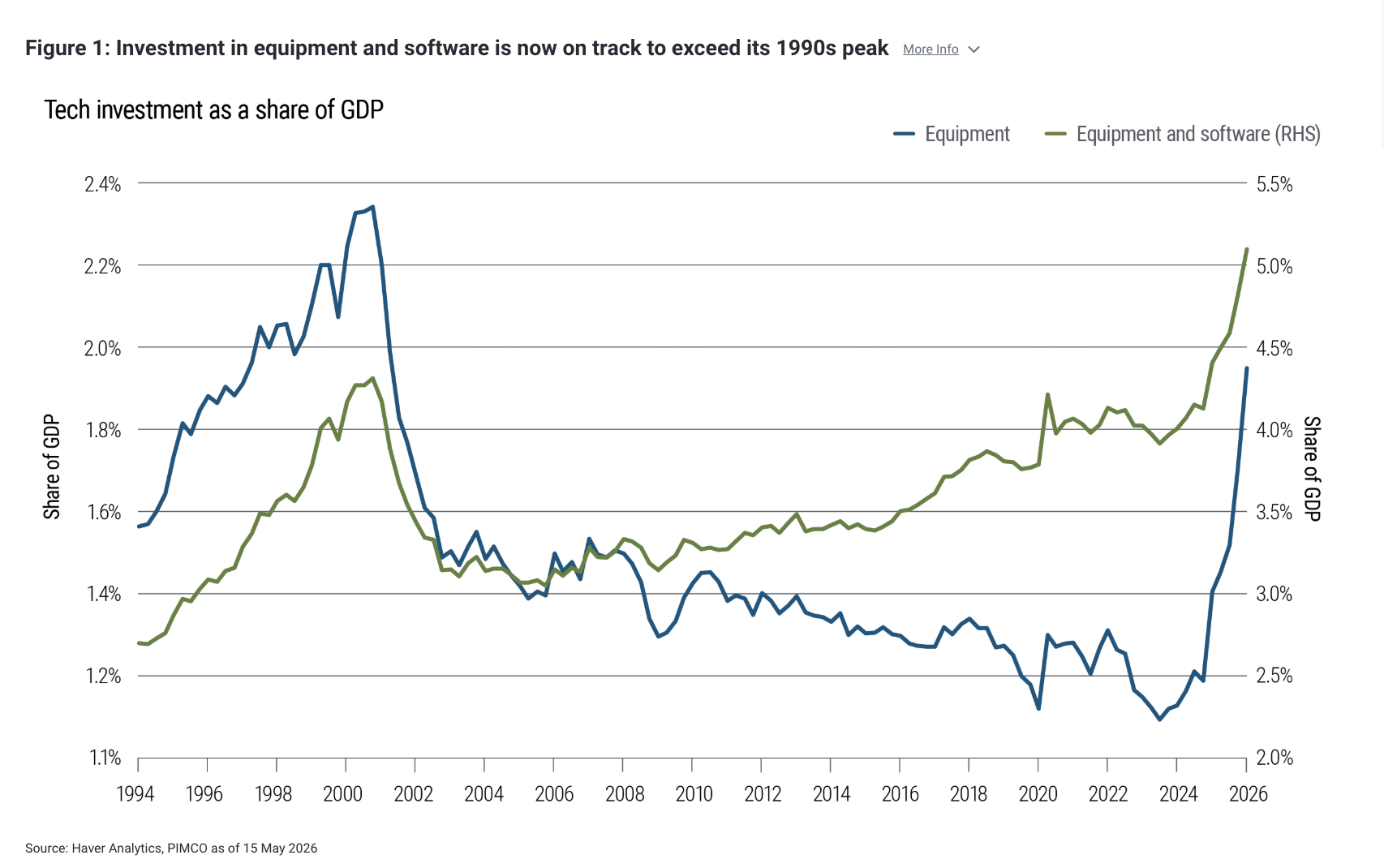

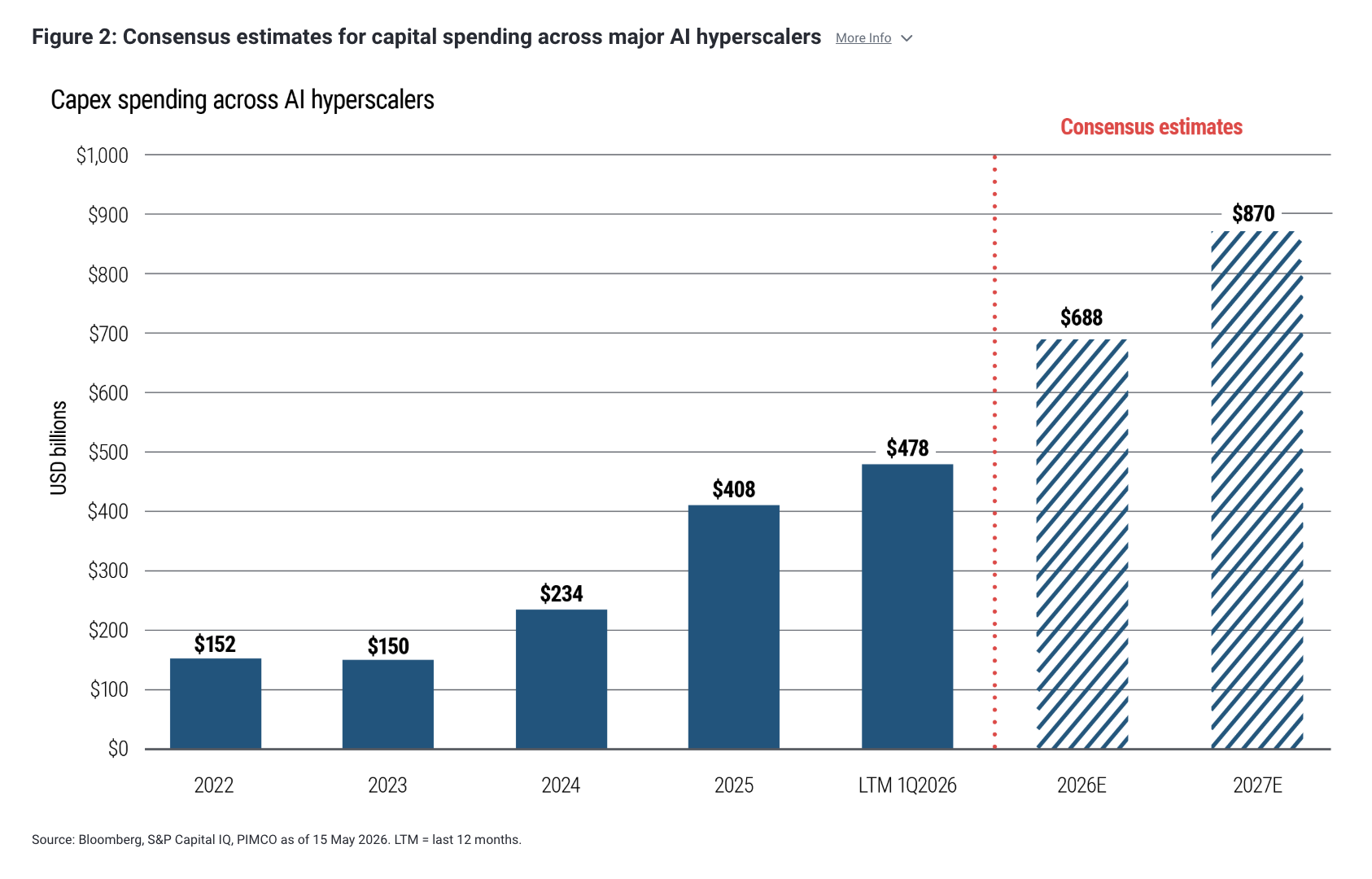

The numbers speak for themselves. As Figure 1 shows, investment in equipment and software as a share of U.S. GDP is now on track to surpass the peak reached in the late 1990s. Meanwhile, consensus estimates for the five largest hyperscalers’ capex have climbed to nearly $690 billion for 2026 and $870 billion for 2027, up from roughly $480 billion at the start of this year (see Figure 2).

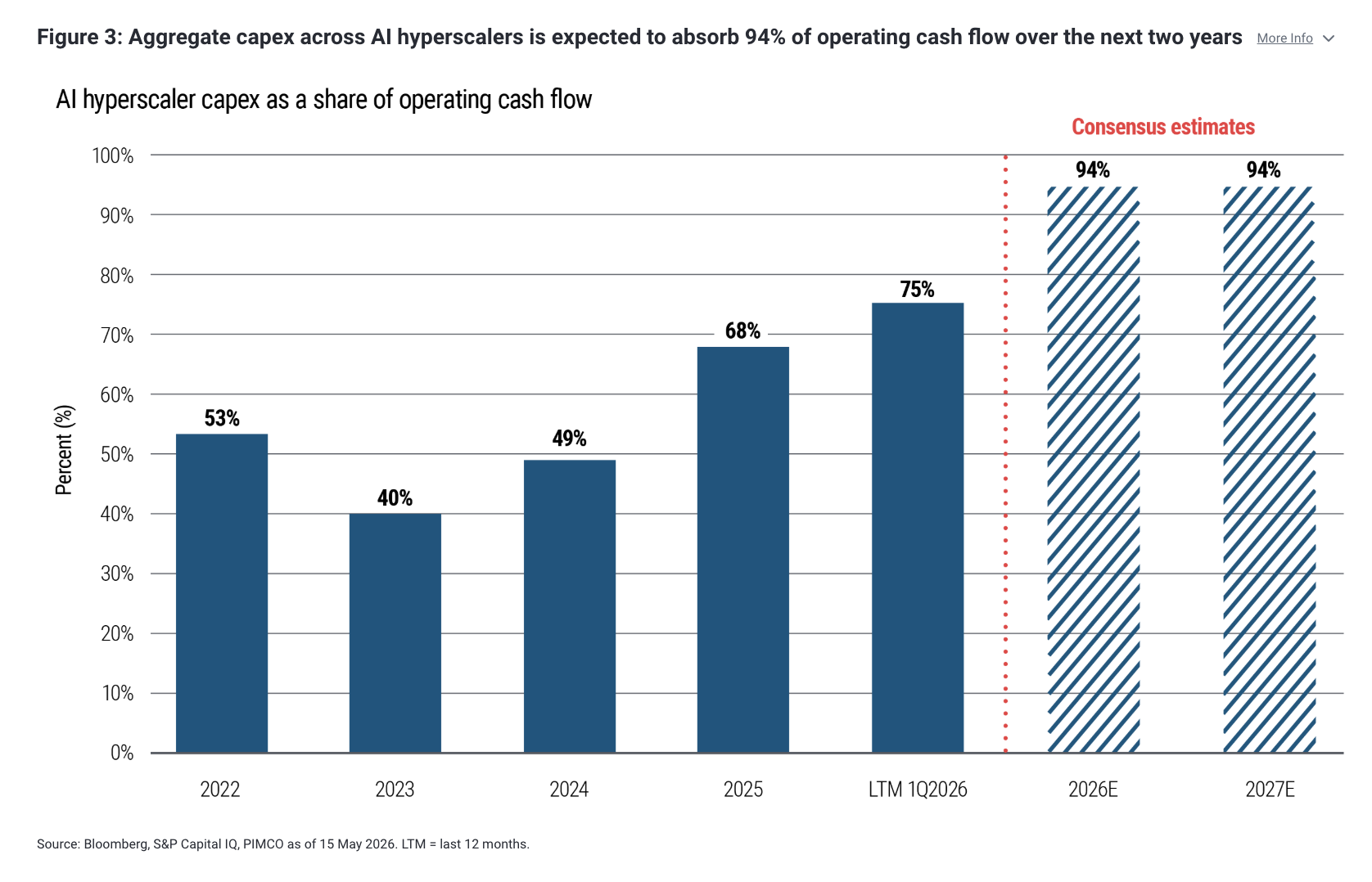

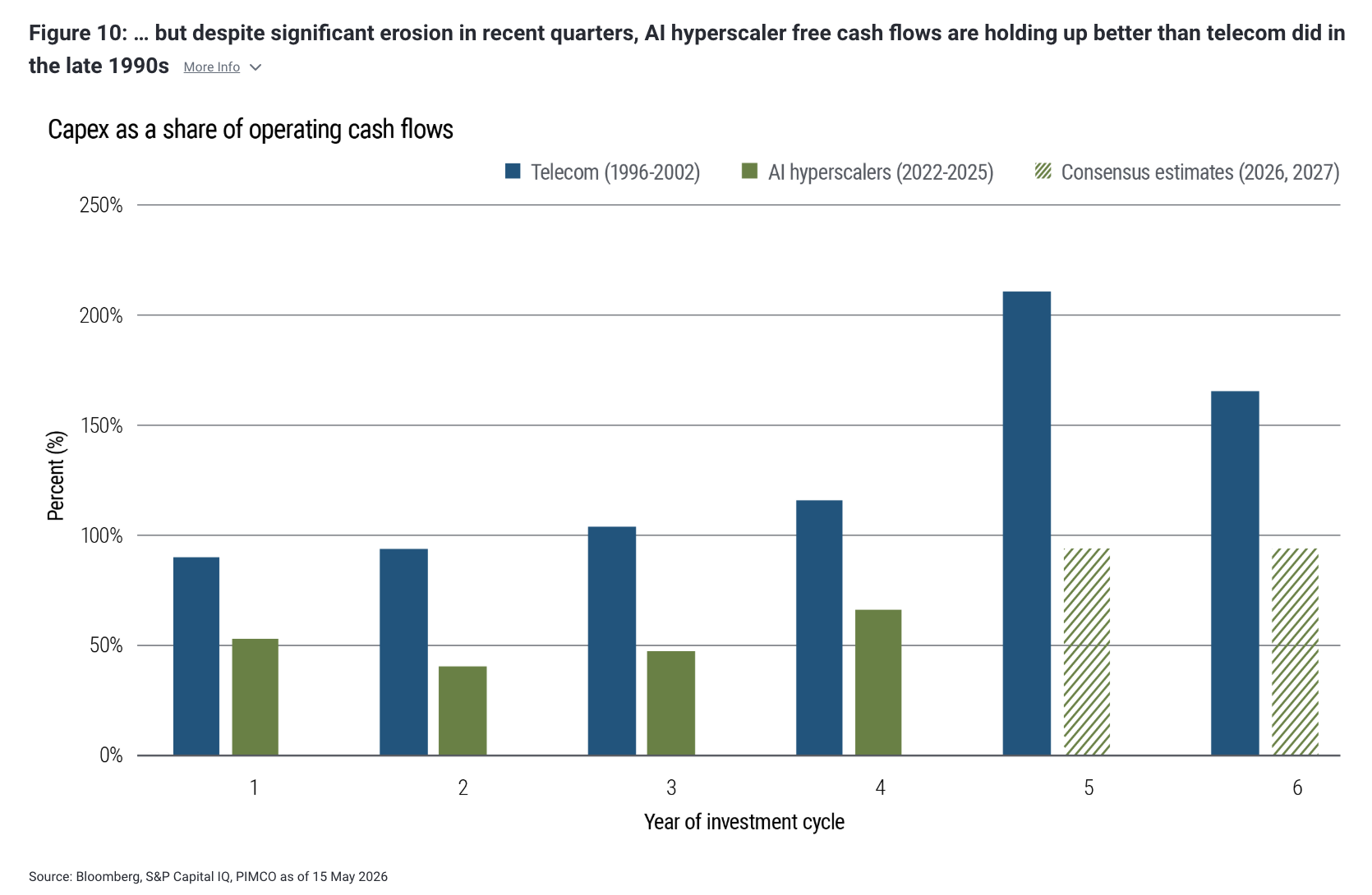

Capex is now expected to absorb 94% of cash flow from hyperscaler operations in both years, versus just 40% in 2023, a sharp inflection that has fundamentally altered the funding equation (see Figure 3).

This shift is already visible in primary credit markets. The volume of index-eligible new debt issuance from hyperscalers has reached roughly $136 billion year-to-date, already eclipsing full-year 2025 totals. This comes on top of another $58 billion of issuance tied to data centers across the IG and HY markets.

Future lease obligations add another layer to the supply story. Recent 10-Q filings point to a combined $822 billion of future non-discounted lease commitments (versus $675 billion as of the end of February 2026) that have yet to be recognized on hyperscaler balance sheets.

The recent wave of jumbo offerings has started to test the market's appetite for duration risk in AI-linked credit. But a key ingredient has been, and will likely remain, deal structure. The protections embedded in covenants, maturity profiles, and creditor hierarchies matter just as much as headline spreads, making structural safeguards not just a legal detail but a first-order investment consideration. Secured financings and deals with claims on hard assets offer a way to invest in essential infrastructure while mitigating risk as technology evolves.

As the AI capex cycle continues to mature, it will raise interconnected questions at the micro and macro level. From a micro standpoint: Will the ongoing credit expansion materially erode balance sheet quality across AI-exposed issuers, and does the growing index footprint of hyperscalers risk spilling over into broader IG and HY fundamentals? From a macro standpoint: Is this capex cycle planting the seeds of the kind of overinvestment that defined the late-1990s telecom boom – and could a correction threaten the durability of the current business cycle?

History suggests that the time to assess these risks is when balance sheets are still strong, not after they have already weakened.

Read more: AI, Market Power, and Diminishing Labor Share

Strong balance sheets, uncertain assumptions

The range of outcomes facing investors is unusually wide, and the risks are layered. Three stand out, in our view.

First, AI adoption is anything but deterministic. The trajectory of AI capital spending hinges on the pace of efficiency gains, but the investment implications cut both ways. If gains arrive faster than expected, computing requirements could scale nonlinearly, justifying ever-larger capacity additions and ever-more debt. If gains lag, the required capital base could shrink materially, stranding assets built for a world that never arrived. Either path reshapes the investment calculus, and neither is easy to forecast. Compounding this, many bullish scenarios implicitly assume utilization rates not yet observed at scale.

Second, value accrual is uncertain across the stack. A more fundamental question looms: Where will economic value ultimately settle along the AI supply chain? At the bottom sits the semiconductor layer, where pricing power has been extraordinary but remains tethered to the durability of the capex cycle itself. Above that is the infrastructure and cloud layer, where hyperscalers are projected to spend trillions on data centers even as the useful life of AI hardware shortens with each new generation of chips and architecture. Then comes the model layer, where training costs are enormous, differentiation is fleeting, and developers are locked in a costly arms race with uncertain pricing power. At the top sits the enterprise and application layer – the ultimate source of demand that must validate the entire chain – where adoption curves remain early-stage and willingness to pay is still being tested. The current pace of capital expenditure requires not just that AI deliver transformative productivity gains, but that those gains accrue to the specific layers taking on leverage. As it stands, no one knows with confidence which layers will capture the lion's share of value – or whether today's infrastructure buildouts will even be met with sufficient demand.

Finally, circular financing is not a guarantee of future demand. Suppliers and large customers are increasingly seeding demand through prepayments, offtake commitments (where buyers contract to purchase goods or services not yet produced), financing support, and contract-backed borrowing structures. While these interlinkages can accelerate the buildout, they also introduce circularity: The same firms benefiting from AI infrastructure spending may, directly or indirectly, be helping to finance the demand that supports it. This kind of induced demand – underwritten by the ecosystem itself – is not the same as organic demand driven by broad enterprise adoption, real productivity gains, and end-user willingness to pay. The former can sustain momentum for a time; only the latter can validate it. Should the transition from one to the other take longer than the supply side anticipates, return profiles could compress sharply, increasing the strain on debt service tied to current financing structures.

A real re-leveraging impulse that hasn’t gone unnoticed by the market

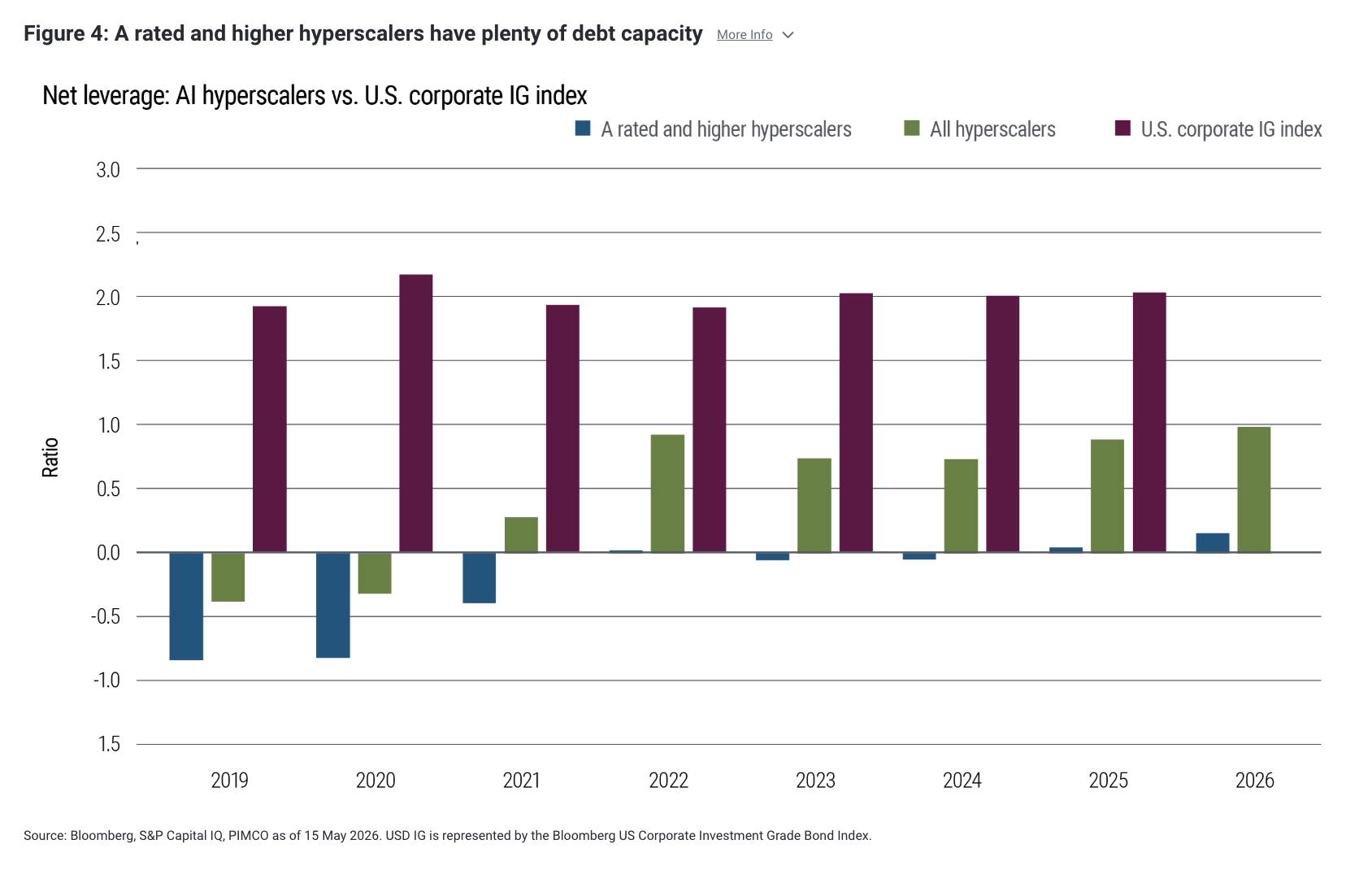

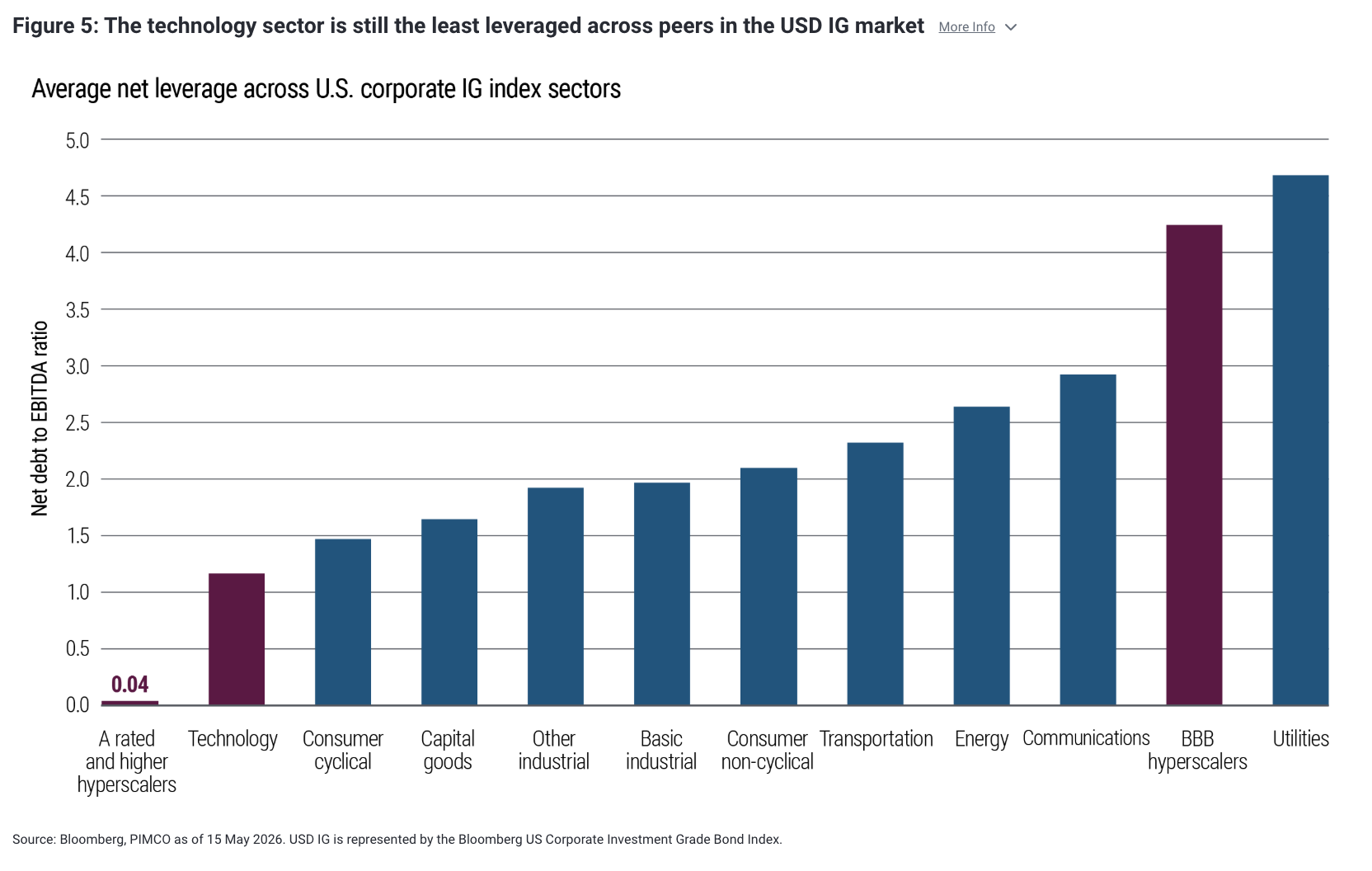

From a credit quality standpoint, the direction of travel seems clear: AI infrastructure is becoming increasingly debt-financed. The good news is that the starting point remains strong. Four of the five hyperscalers report net leverage that is barely positive, and even after the recent surge in issuance, the broader technology sector remains the least leveraged sector in the U.S. IG market (see Figures 4 and 5). In absolute terms, balance sheet quality still looks stable, and high quality hyperscalers retain meaningful debt capacity.

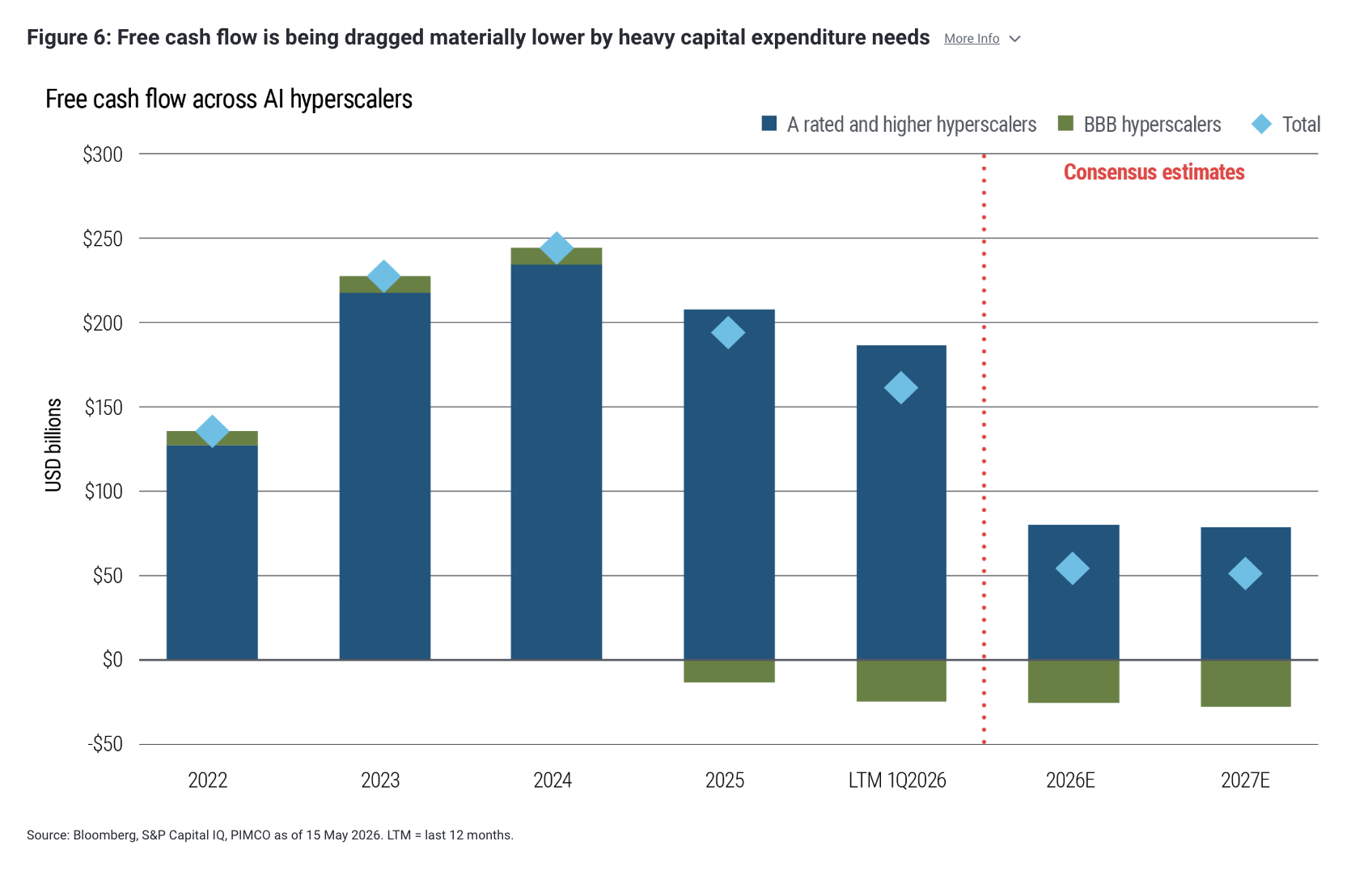

The bad news is the direction of travel. Free cash flow expectations are being dragged materially lower, particularly this year, and balance sheet liquidity has eroded notably in recent quarters (see Figure 6). Reported leverage also likely understates future obligations, given the scale of lease commitments still sitting outside recognized debt metrics. Whether these liabilities will ultimately be justified by future earnings growth remains the central question. The bottom line is that the re-leveraging impulse is real, even if it is starting from an exceptionally strong base.

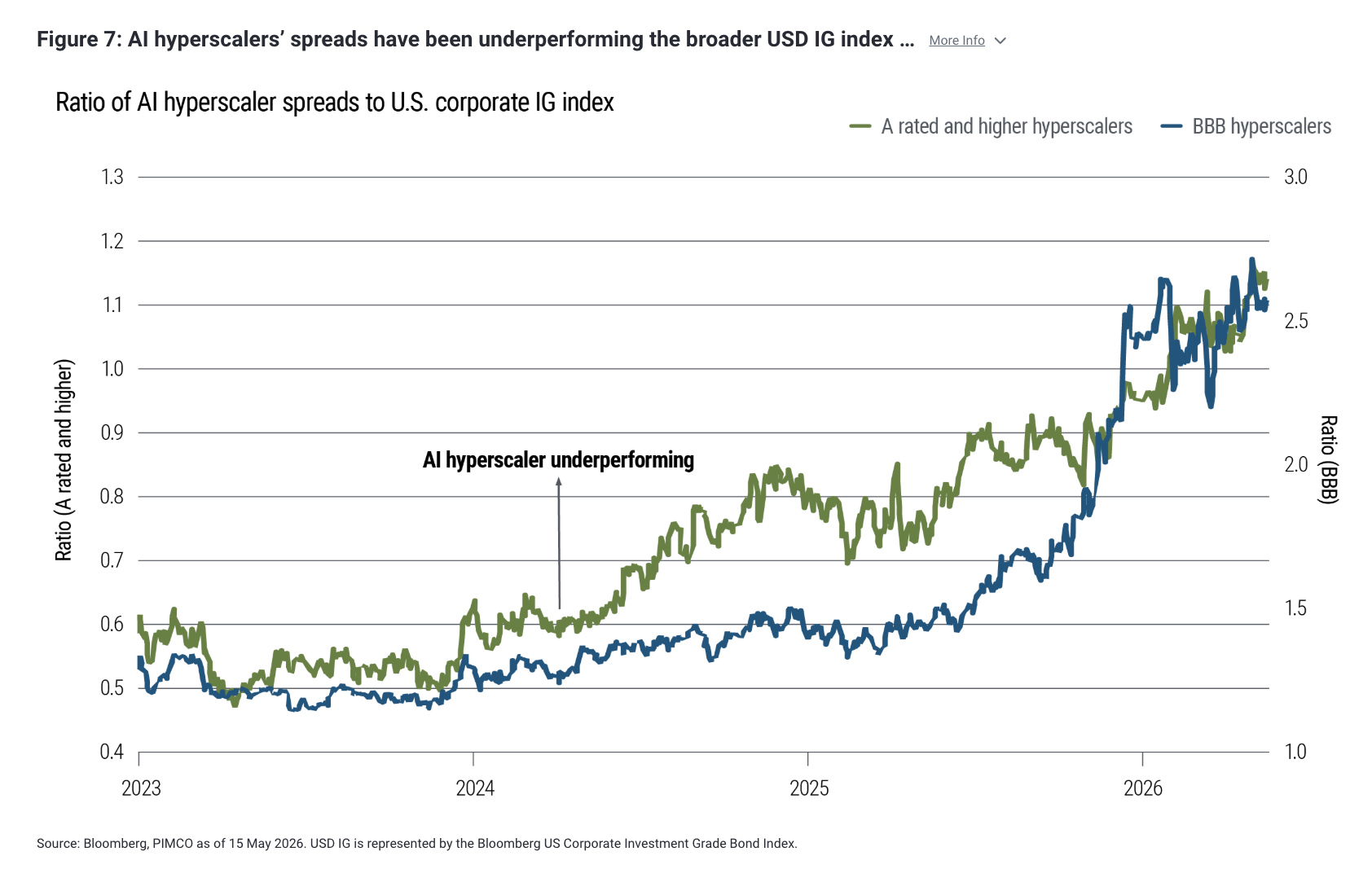

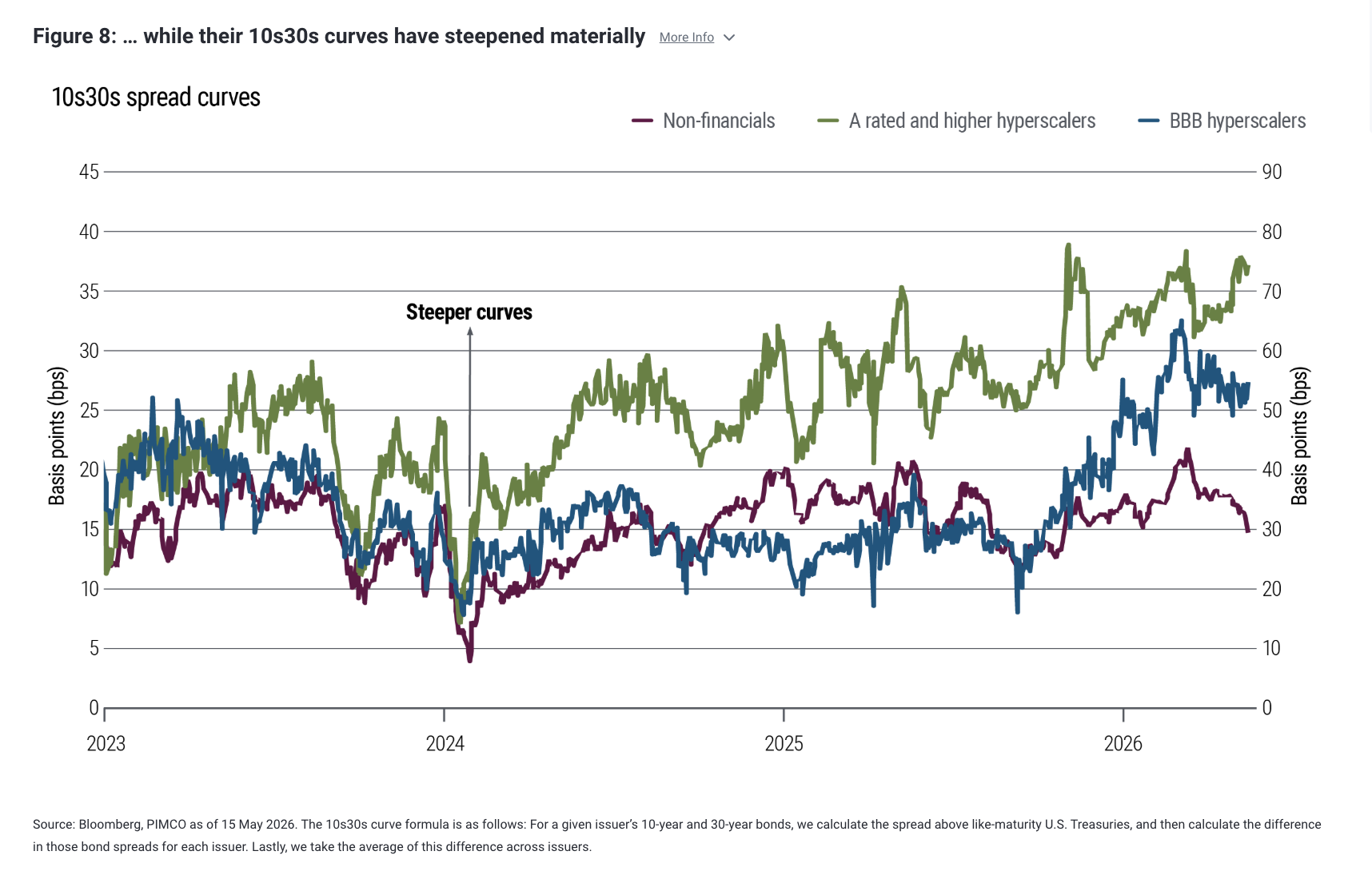

Markets have taken note. In credit, hyperscalers have underperformed the broader IG index on a spread basis (see Figure 7), while their 10s30s curves have steepened meaningfully (see Figure 8). This is a sign that investors are demanding more compensation for duration risk precisely where issuance has been heaviest.

The equity signal is more nuanced, with investors generally rewarding firms perceived as having a credible path to monetizing AI capex and penalizing those with a murkier case for return on investment (ROI).

Taking a step back and looking more broadly at the AI supply chain, semiconductor stocks have significantly outperformed, with Korea and Taiwan among the standout equity markets globally given their outsize exposure to the AI chip supply chain. Overall, the signal is clear: Investors are no longer underwriting the buildout on faith alone.

The 1990s telecom parallel: Useful, but incomplete

Market participants instinctively look for historical precedents when navigating uncertain technological transitions. Two comparisons that are most frequently cited in the context of today’s AI infrastructure buildout are 19th-century railroads and the late-1990s telecom fiber boom. Both are useful, but for different reasons.

The railroad analogy captures the defining feature of general-purpose infrastructure manias: enormous, irreversible capital commitments made years ahead of demand, which ultimately enable economic transformation far broader than investors initially imagined. That said, it also carries an important warning. Railroad investors frequently lost money even as the technology itself proved transformative. The lesson is clear: Being right about technological impact does not guarantee attractive returns if you are wrong on timing.

While that lesson does apply to AI, the analogy has limits. Railroads are zero-sum immovable physical assets with relatively straightforward revenue models and decades-long depreciation cycles. AI infrastructure is different. Its usability is not tied to a specific geography, its assets have much shorter life cycles, it embeds non-rival economics (i.e., non-zero-sum), and it sits within a contested value chain where the ultimate monetization hierarchy remains unclear. That makes the ROI math fundamentally harder to estimate.

The telecom analogy is more salient. The fiber bust at the turn of the 21st century occurred not because internet traffic failed to grow, but because supply was built for a demand trajectory that took much longer to materialize than models projected. The “we can’t afford to fall behind” logic encouraged aggressive competitive behavior, pulled forward investment, and eventually fueled significant overcapacity for the time.

Vendor financing also amplified the telecom cycle. Equipment suppliers effectively lent to their own customers so those customers could buy more switches, routers, and optical gear, allowing suppliers to pull forward sales while pushing back credit risk deeper into the ecosystem. That circularity made demand look more durable than it ultimately was.

The central lesson from the late-1990s fiber bust is that the underlying investment can be directionally correct while the supply response is still so far ahead of demand that it destroys capital.

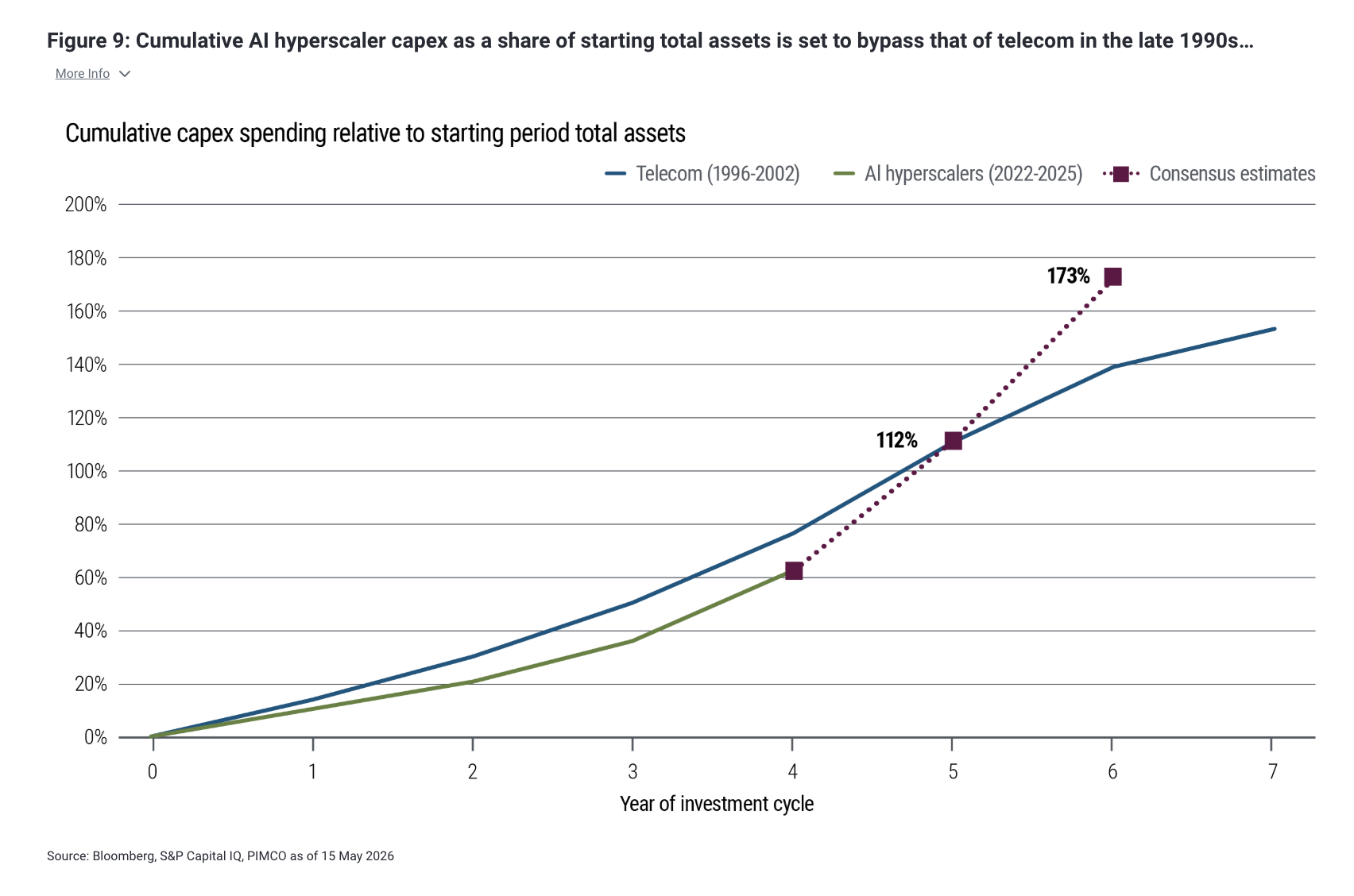

The parallels with today’s AI capex cycle are real. Capex is surging both in absolute and relative terms. Hyperscaler capex growth relative to starting total assets is projected to outpace that of telecom in the late 1990s, although it is still projected to be lower as a share of operating cash flows (see Figures 9 and 10). These dynamics naturally invite comparisons to the overinvestment and subsequent bust that defined the dot-com era. However, while the credit market footprint is changing as hyperscaler issuance reshapes index composition, the increase remains more modest so far than telecom’s late-1990s expansion.

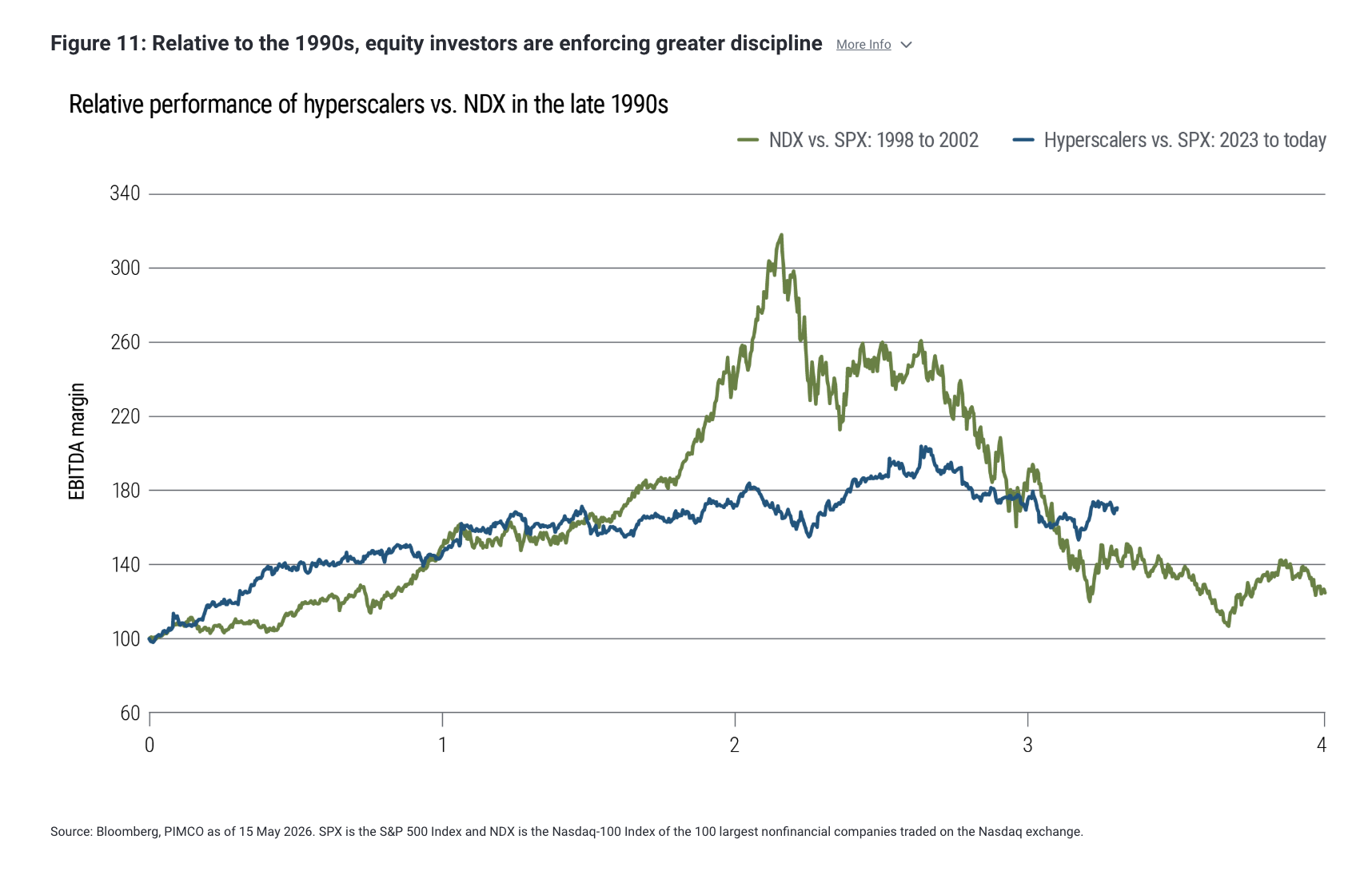

Two other critical differences deserve emphasis. First, equity investors have been more disciplined in this cycle. They are underwriting ROI expectations more explicitly and incorporating the expected hit to free cash flow, forcing management teams to operate with tighter constraints than many telecom companies faced in the late 1990s (see Figure 11). This market-imposed discipline is a meaningful check on the kind of unconstrained, debt-fueled expansion that characterized the telecom boom.

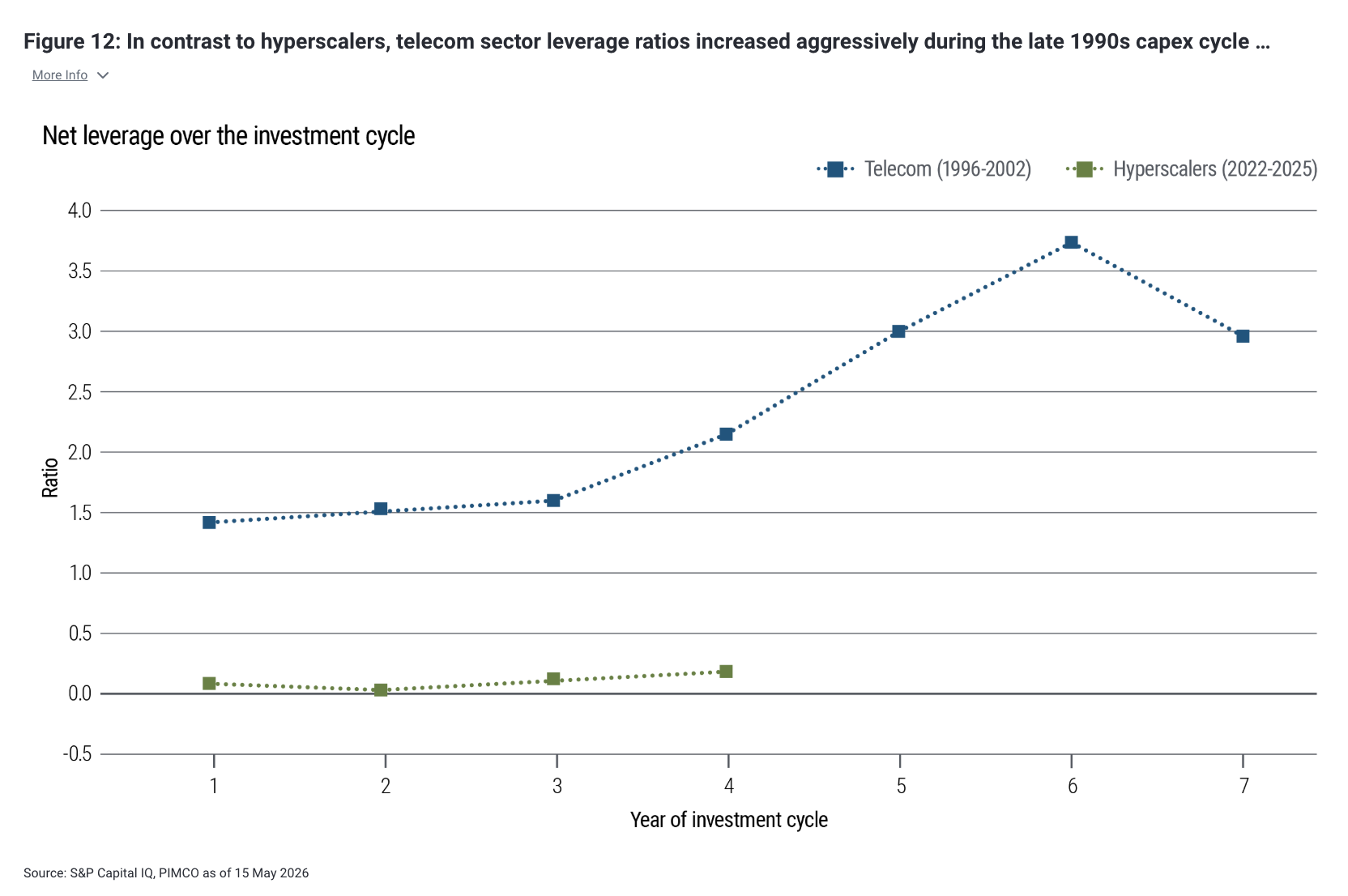

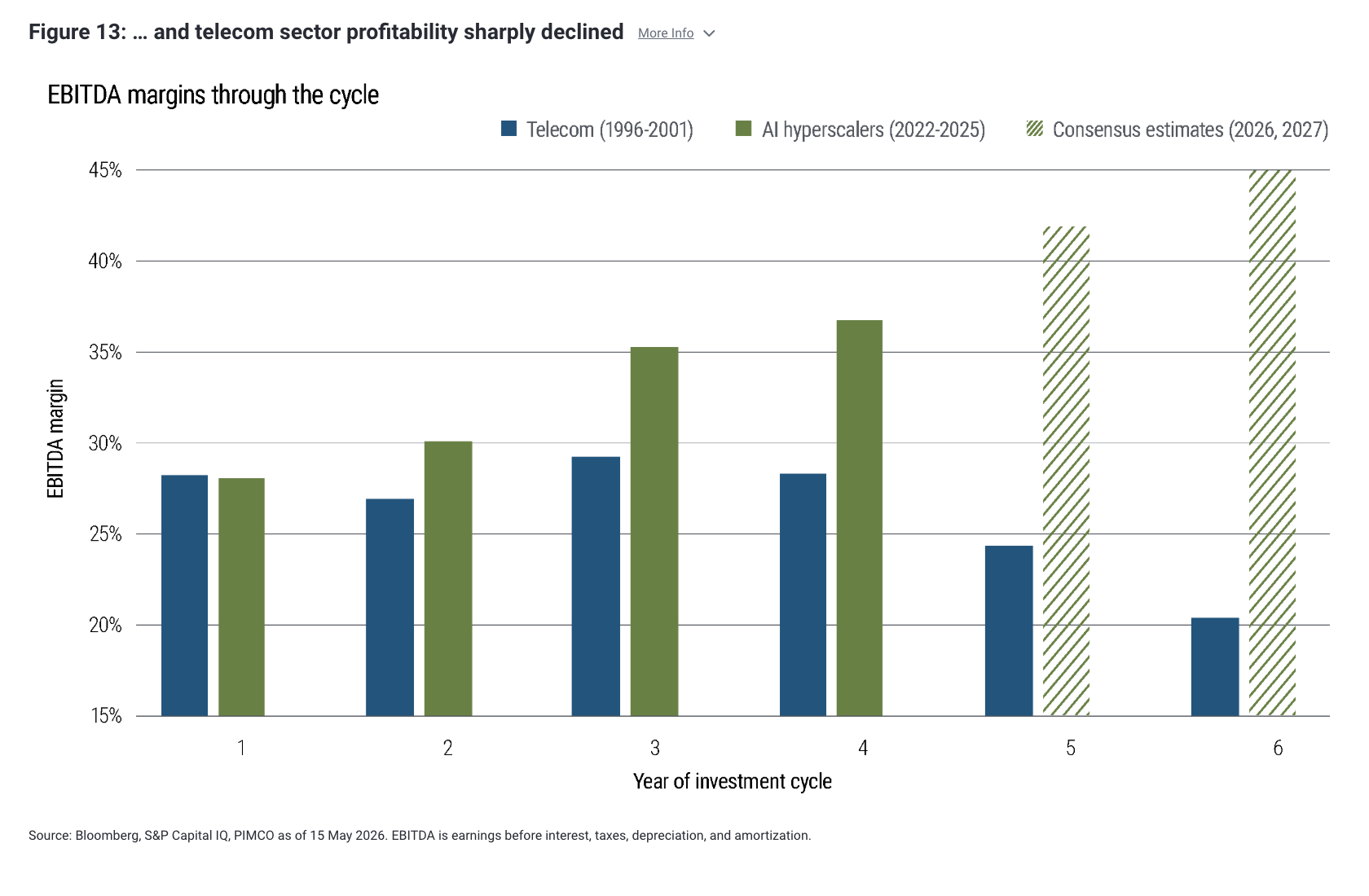

Second, today’s starting point for credit quality appears dramatically stronger, at least among the highest-quality hyperscalers. Many telecom issuers entered the turn-of-the-century downturn with aggressive leverage, weaker profitability, and heavy dependence on external capital. By contrast, the largest AI infrastructure spenders are beginning from exceptionally strong balance sheets (see Figure 12), and profit margins among the hyperscalers are also significantly higher than telecom’s back in the late 1990s (see Figure 13).

To be clear, as noted above, although free cash flow has eroded and the direction of travel is clearly less credit-friendly, today’s high quality hyperscalers still screen far better than telecom did at a comparable stage of its capex cycle.

Put differently, AI is in the midst of a capex boom with genuine risks: uncertain monetization, potential overbuild, shortening asset lives, and growing reliance on debt. But for now, it is a more disciplined and far more financeable cycle than the late-1990s telecom boom.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index.

Investments in asset-based lending and asset-backed instruments are subject to a variety of risks such as, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Equity investments may decline in value due to both real and perceived general market, economic and industry conditions, while debt investments are subject to credit, interest rate and other risks. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio. Leverage, including borrowing, may cause a portfolio to be more volatile than if the portfolio had not been leveraged. The current regulatory climate is uncertain and rapidly evolving, and future developments could adversely affect the technology and AI sector.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0520-5511141

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Back to top

© PIMCO

Read more commentaries by PIMCO