Key takeaways:

- Tech earnings are the primary driver of the upward revision to our S&P EPS estimate

- S&P 500 companies continue to operate near record profitability

- A resolution of the US-Iran conflict will help ease inflation concerns

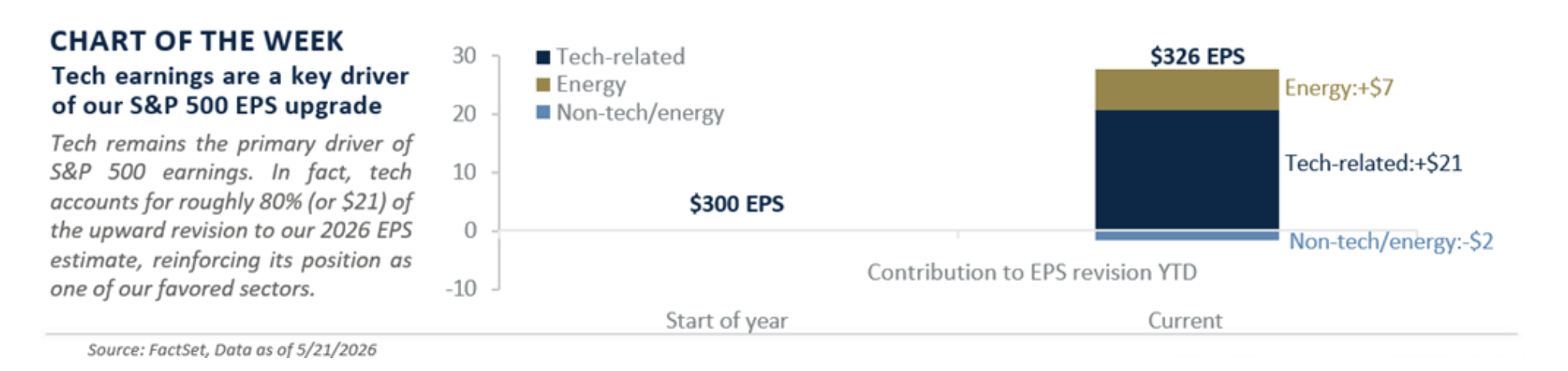

Despite headwinds from rising oil prices, fundamentals have remained strong. The S&P 500 has notched 18 record highs year to date and, more importantly, surpassed our prior target of 7,250. Following a standout 1Q earnings season, we are raising our 2026 earnings per share (EPS) estimate to $326 from $300. With limited scope for multiple expansion, earnings should be the primary driver of further upside, supporting our revised year-end target of 7,650. Here are three factors behind this upgrade:

Robust tech earnings

S&P 500 1Q26 earnings have been exceptionally strong, with EPS delivering 27% year-over-year growth, well above the 12% expected at the start of earnings season. Companies have also beaten EPS estimates by ~18%, the strongest in five years. Technology continues to do the heavy lifting. For example, MAGMAN* – a composite of mega-cap tech – delivered 61% EPS growth year over year in 1Q as companies linked to AI (e.g., semis and cloud) have driven the bulk of upside surprises. Notably, tech accounts for roughly 80%, or $21, of the upward revision to our 2026 EPS estimate, reinforcing its position as one of our favored sectors.

Strong margins

Despite headwinds from tariffs, higher energy costs and supply chain pressures, S&P 500 companies continue to operate near record profitability. Case in point: Net margins rose for a fifth straight quarter in 1Q, reaching a record 15.3%. Looking ahead, several tailwinds should help support margins, including easing energy prices if the US–Iran conflict is resolved by July as we expect, some tariff relief following the Supreme Court IEEPA ruling, and continued AI-driven productivity gains.

Resilient economy

The US economy remains on solid footing, with GDP expected at ~2.4% this year. Consumer spending continues to hold up, supported by indicators like credit card activity, restaurant bookings and department store sales. The labor market remains firm, with jobless claims near 50-year lows. At the same time, tailwinds from the One Big Beautiful Bill are supporting businesses and consumers through tax incentives and higher tax refunds, respectively. This backdrop should continue to support earnings beyond tech.

Yields have moved sharply higher since the start of the Middle East conflict, with the 10-year Treasury up over 60 bps to 4.55% and the 30-year pushing above the key 5% level. The story is fairly straightforward: Higher energy prices are adding to inflation pressures, prompting a meaningful repricing in the Federal Reserve (Fed) outlook, with markets now factoring in the potential of a rate hike rather than rate cut this year. Below, we highlight three factors that could help bring yields back down.

Read more: Housing Market 2026: Frozen, Not Broken

Resolution of US-Iran conflict

A diplomatic resolution and reopening of the Strait of Hormuz would ease supply constraints and push oil prices lower (Raymond James year-end estimate: ~$70 per barrel). Markets have already begun to reflect this dynamic as headlines signaling any progress have consistently driven both oil prices and yields lower. A durable agreement could extend that trend, easing inflation concerns and prompting a reassessment of the Fed rate path, driving yields lower particularly at the front end.

Growth and inflation are not overheating

Growth has remained resilient despite a series of shocks, but markets are increasingly concerned the latest oil spike could unanchor inflation expectations, especially with inflation above the Fed’s 2.0% target for five straight years. The recent uptick, driven by energy prices and Bureau of Labor Statistics (BLS) distortions, is testing patience, particularly as new Fed Chair Warsh is sworn in today. That said, the fixed income market is acting as if the economy is overheating. We disagree. There are signs consumers are pushing back on higher prices, pointing to emerging pockets of stress that should help contain inflation and ease the upward pressure on yields.

Yields have become sufficiently attractive

With the Middle East conflict dragging on, G10 sovereign yields have climbed to multi-year highs. While higher rates have yet to restrain economic activity, front-end US rates now sit over 40 bps above the mid-point of fed funds target range, pricing in potential hikes, and long-term yields above 4.5% – a level that has historically started to weigh on equities – additional upside should prove increasingly self-limiting. With the 10-year Treasury’s 14-day Relative Strength Index near 70, suggesting the move is getting stretched, yields are becoming more attractive and are at levels where demand starts to pick up.

*MAGMAN represents a composite of Microsoft, Apple, Google, Meta, Amazon, Nvidia.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition – March 2026 (PDF)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

More Insurance & Annuities Topics >