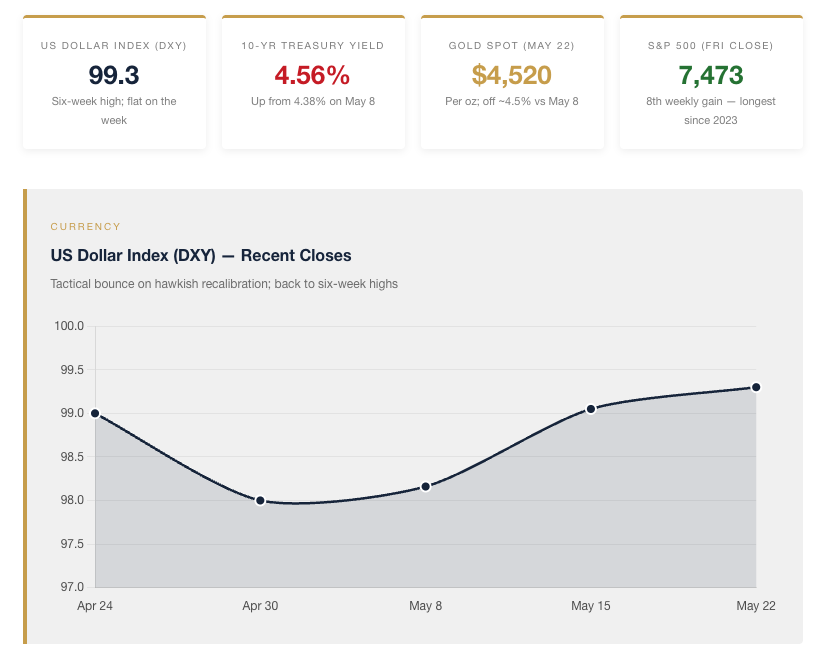

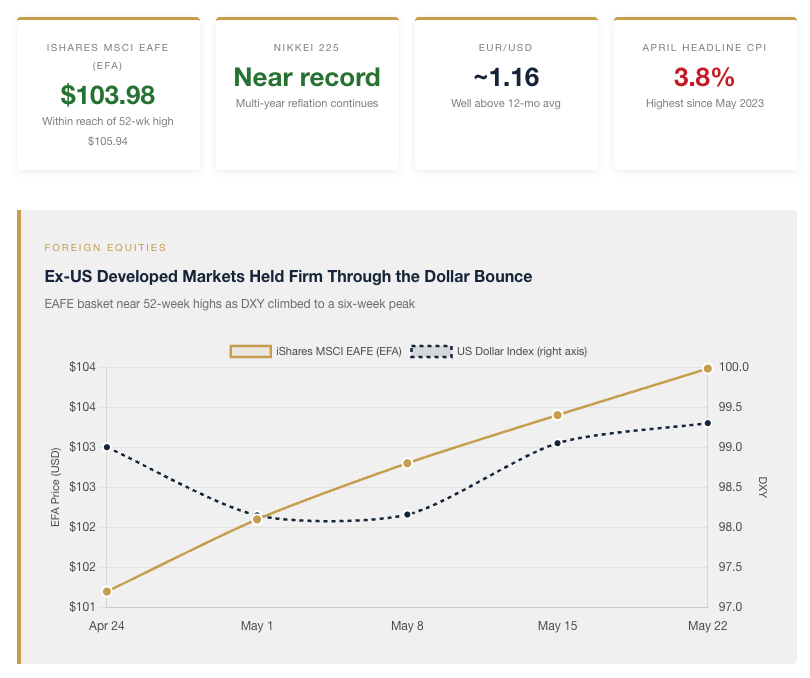

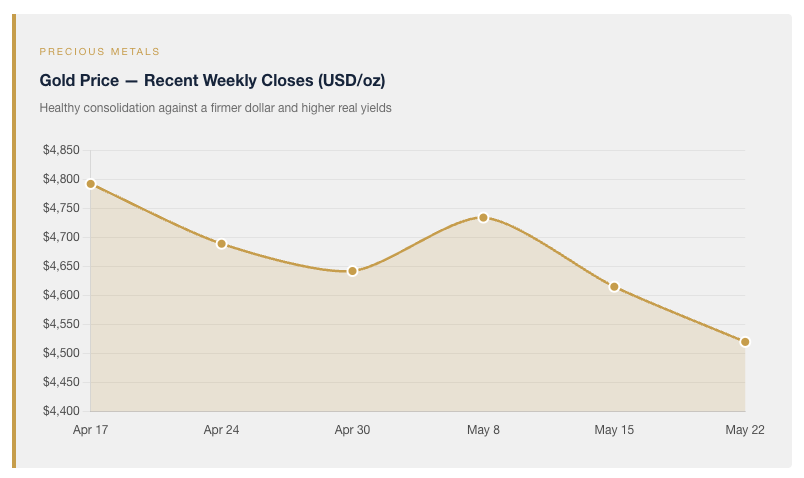

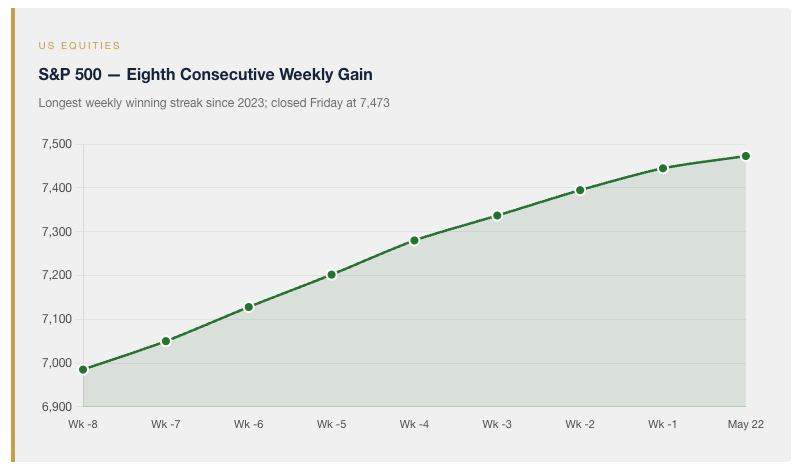

On the surface, last week looked engineered to embarrass our positioning. The dollar index climbed to a six-week high above 99.3 by Friday and finished the week roughly flat at those levels. The ten-year Treasury yield punched higher to 4.56%, gold drifted back to roughly $4,520 — about 4.5% below where it closed two weeks earlier — and the S&P 500 booked its eighth consecutive weekly advance, the longest such streak since 2023. The macro narrative coming out of the April CPI release, the renewed US-Iran headlines, and Friday's swearing-in of Kevin Warsh as Federal Reserve chair was thoroughly hawkish, thoroughly pro-dollar, and on every casual read, not friendly to a portfolio tilted toward international diversification. And yet, beneath that headline tape, the foreign markets we have argued the case for all year did something we believe is worth far more attention than the day-to-day moves in the dollar. They held their ground. The MSCI EAFE basket finished within striking distance of a 52-week high. The Stoxx Europe 600 advanced and Japanese equities continued the multi-year reflation that has carried the Nikkei to multi-decade highs. That cross-current is the real story of the week — and, in our view, the one with the most important investment implication.

Read more: The Cost of Being Too Liquid

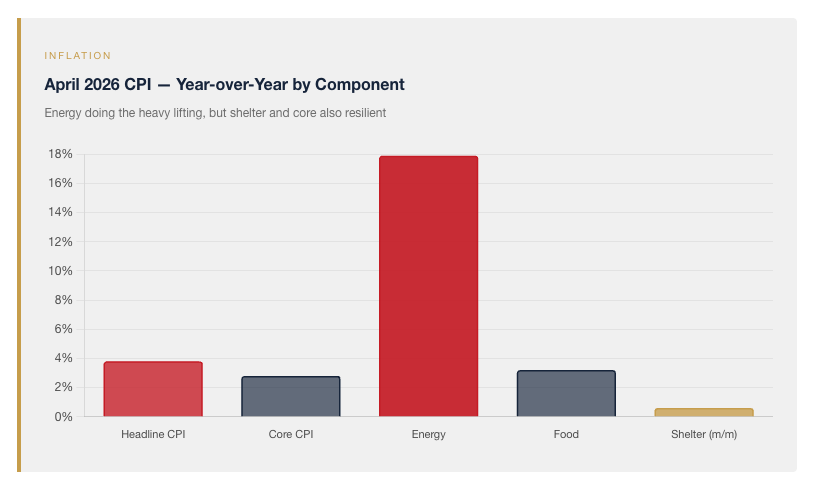

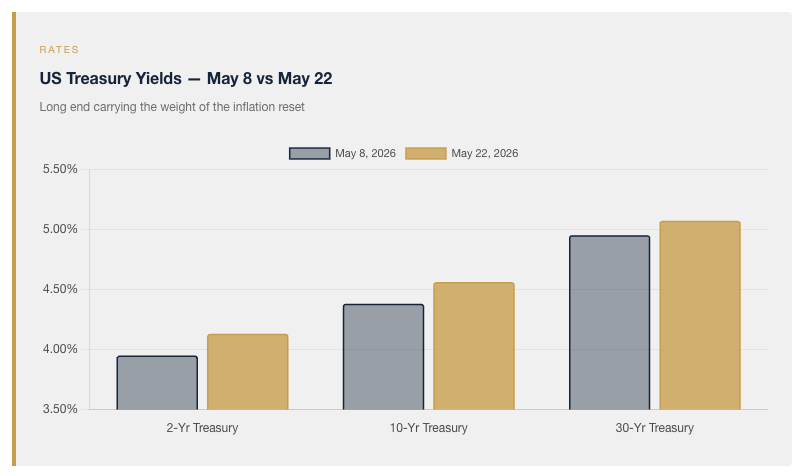

The reason the dollar rallied is straightforward. The April CPI release on May 12 came in at 0.6% month-over-month and 3.8% year-over-year, the hottest headline print since May 2023 and a half-percentage-point acceleration from March. Energy alone was up 17.9% over twelve months and accounted for more than 40% of the headline gain, but the rotation into shelter — up 0.6% on the month after several softer prints — made clear that the inflation pulse is not a pure tariff-and-tankers story. Retail sales on Thursday rose 0.5% in nominal terms but went modestly negative in real terms once inflation was netted out. The thirty-year Treasury briefly traded above 5.1% on May 15, its highest level in nearly a year. Markets, which only two weeks earlier had been pricing the possibility of a cut later in the year, are now pricing a meaningful chance of a rate hike before December. The dollar's bid is mechanical: hot inflation plus a more hawkish Fed reaction function pulls in foreign capital looking for nominal yield. That logic, narrowly applied to last week's tape, is correct.

What is less examined in the consensus read is what that bid is costing the United States in real time. Real ten-year Treasury yields above 2.1% combined with thirty-year yields above 5% are restrictive enough to bite. Mortgage rates have risen materially over the past month. April retail sales were dragged lower by furniture, autos, department stores, and clothing — the rate-sensitive and discretionary categories that respond first when real rates move. Consumer sentiment readings released through May sit near historic lows. We do not think the US economy is on the verge of recession — we have been explicit on that point all year — but we do think the market is currently asking the Federal Reserve, under brand-new leadership, to deliver a meaningful real-rate squeeze on the consumer in order to break a CPI line being pushed higher partly by tariffs and partly by an Iran-related energy shock that may already be on the path to resolution. That is a difficult ask, and not one we believe the policy mix can sustain through the second half of the year without consequence.

We owe readers an explicit acknowledgment of what is working in the United States. Consumer balance sheets, as we have written before, remain healthy in aggregate. The Q1 productivity print at 2.9% year-over-year confirms that the AI-driven capex cycle is genuinely lifting the productive frontier of the US economy — not merely the multiples of a handful of technology stocks. The S&P 500's eighth straight weekly gain, closing Friday at 7,473, reflects an investor base that sees these strengths and is willing to underwrite them. We are not in the business of denying that. Our positioning is not a recession bet, and our case for diversification has never depended on a US downturn. It depends on something different: the structural likelihood — not inevitability — that the marginal foreign holder of US dollar assets will increasingly demand a wider risk premium for concentration in a single currency block, a single regulatory regime, and a single fiscal trajectory.

Which brings us back to the part of the tape we believe was underreported. Foreign developed-market equities trading within striking distance of 52-week highs while the dollar climbs to a six-week high is a more bullish configuration than it appears at first glance. The translated dollar return on an EAFE basket holding firm against a stronger dollar implies an even stronger local-currency advance. The Stoxx 600 advanced through the week on news that US-Iran negotiations are, in President Trump's words, "proceeding in an orderly and constructive manner," and stands to benefit further from any meaningful disinflation if Hormuz tolls and uranium-stockpile disputes can be resolved. Japanese equities are riding a multi-year reflation, governance reform, and capital-allocation story that has been building since the Bank of Japan began normalizing in 2024 — the Nikkei finished the week within striking distance of an all-time high. The euro at roughly 1.16 against the dollar is still well above its twelve-month average even after this week's bounce. In our view, this is what a structurally constructive ex-US backdrop looks like when it meets a tactically hawkish dollar bid: the foreign markets do not crack, because the case for owning them was never primarily a weak-dollar trade.

There is also a horizon to keep in mind. The European Central Bank meets June 11 and the Bank of England meets June 18, and several large research desks are now flagging the possibility that both could begin discussing increases rather than cuts — a meaningful reversal from the rate-differential trade that has supported the dollar through much of the year. If the ECB and the BoE move first, or even hint at moving first, the rate-differential cushion under the dollar compresses. Combine that with the unique uncertainty introduced by Chair Warsh's stated intent to reform Federal Reserve communications — fewer press conferences, less forward guidance, a return to what he characterizes as more independent and less model-driven decision-making — and the credibility premium the dollar has historically commanded becomes harder to underwrite at exactly the moment markets are most exposed to it. Whatever one thinks of the substantive merits of Warsh's reform agenda, and there is a case for some of it, the transition introduces variance that did not exist a week ago.

That leaves us where we believe the data leaves a thoughtful allocator. Gold's pullback to the low-$4,500s is, in our reading, a healthy consolidation against a backdrop of higher real yields and a firmer dollar — not a revision of the structural thesis. The S&P 500 at a record high reflects genuine US strengths we are not interested in fighting. But for the dollar-denominated investor weighing where to add or reallocate at the margin, last week described almost exactly the cross-current our international value strategy is built to capture: ex-US equities holding their ground through a dollar headwind, valuation gaps wider than they were a year ago, and an FX configuration whose next move is more likely to compress than to extend in our favor.

If the past week's data has prompted you to reconsider how the international portion of your portfolio is built, we would encourage you to reach out to a Euro Pacific Asset Management advisor or visit EuroPac.com to learn more about our Value, Gold, and Emerging Markets strategies. The case for diversification is not a bearish call on America. It is a forward-looking allocation to a world whose returns are increasingly being earned in places the dollar headlines do not always describe.

Investment risk

Please read about the Risks of investing in the Funds. You should carefully consider the Fund’s investment objectives, risk, charges and expenses before investing. Investing involves risk, including potential for loss of principal. The risks of investing in emerging market and foreign securities may be higher than the risks associated with investing other securities. Diversification cannot assure a profit or protect against loss in a down market. Dividends are not guaranteed and may fluctuate. Fund holdings are subject to change and risk. Past performance cannot predict future results.

To obtain a prospectus or summary prospectus that contains this and other information about the Funds, please Click Here or call 1-866-878-2881. Please read the prospectus carefully before investing. Euro Pacific Asset Management Funds are distributed by Distribution Services, LLC (Euro Pacific Asset Management is not affiliated with Distribution Services, LLC).

Disclosure: Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and it is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Funds nor any of its representatives may give legal or tax advice.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Euro Pacific Capital

Read more commentaries by Euro Pacific Capital