Dollar Dominance Remains Alive And Well (Part 1)

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. The narrative goes that BRICS countries are building an alternative, that China is dumping Treasuries, that gold is replacing the dollar as the world’s reserve asset, and that Washington is so desperate to find buyers for the next debt issuance that it’s now offering dollar swap lines to Gulf states as a backdoor liquidity rescue. Make no mistake, the “Persistent Purveyors of Doom” have a story. However, the data doesn’t support any of it.

Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

Thesis Vs. Reality

I’ve been arguing for years that the “dollar collapse” thesis confuses inflation with debasement. You can’t be debasing a currency that the rest of the world is fighting harder than ever to acquire. We covered the rebasement argument in our previous piece on the dollar’s plumbing, and in “The Dollar’s Death is Greatly Exaggerated.” The latest data only sharpens the case for dollar dominance.

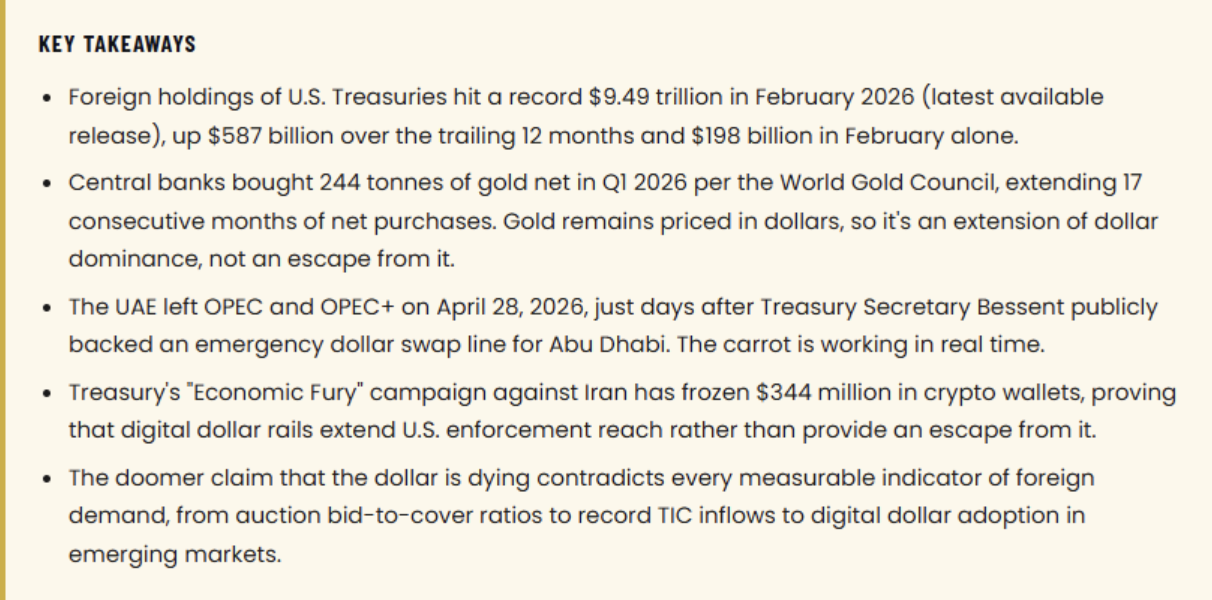

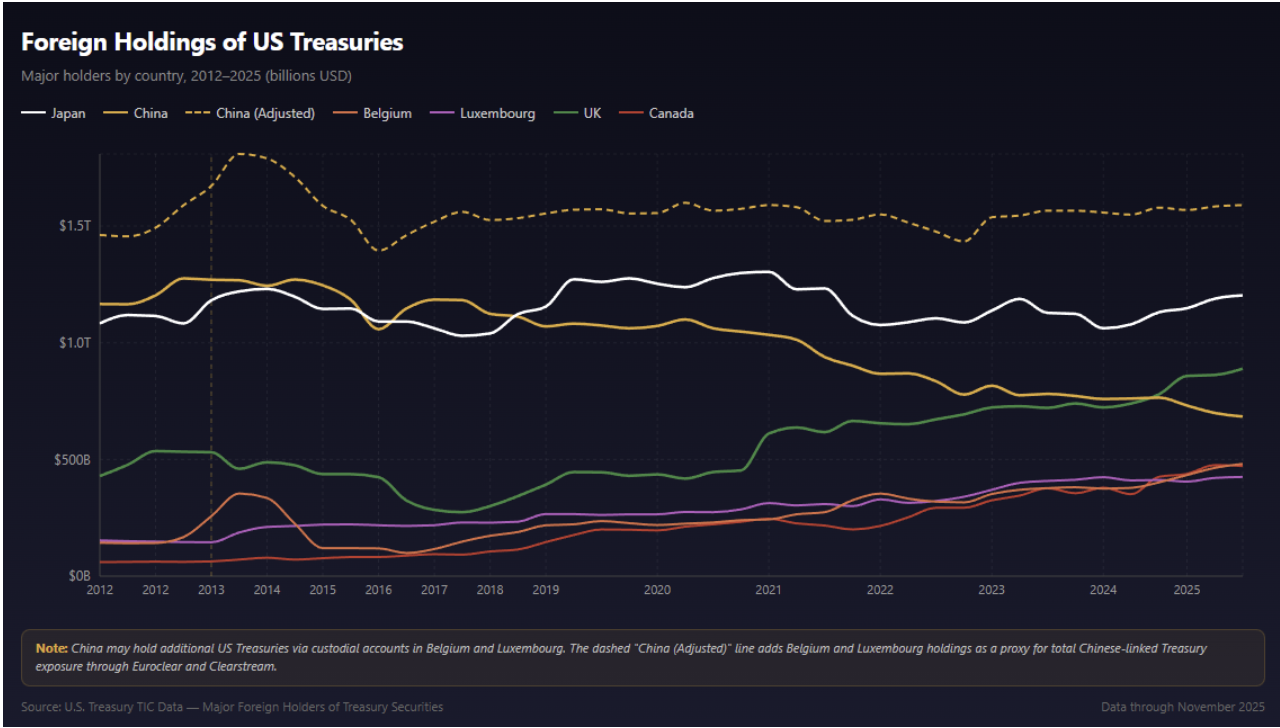

According to the U.S. Treasury’s most recent Treasury International Capital report, released April 15 with February 2026 data, foreign residents purchased $101 billion of long-term U.S. securities in February alone. Net TIC inflows totaled $184.5 billion for the month. On top of that, foreign holders added $91.6 billion to their Treasury bill holdings. Total foreign ownership of U.S. Treasuries hit a record $9.49 trillion in February, up $198 billion in the month and $587 billion over the trailing 12 months. However, that headline number actually undercounts the reality. It excludes foreign holdings managed through U.S.-domiciled hedge funds and the Cayman Islands basis trade, which the Federal Reserve estimates pulls another $1.5 trillion of de facto foreign demand into the bid stack. Adjusted for that, true foreign-linked exposure runs closer to $11 trillion.

Beyond stock-of-debt figures, the flow data tells the same story. Indirect bidder participation, the auction proxy for foreign demand, has run consistently above 70% of accepted bids on recent benchmark issues. Bid-to-cover ratios on 10-year and 30-year auctions have held above 2.5 across multiple cycles. If the world were truly walking away from the dollar, we’d see weak auctions, tailing yields, and a steepening term premium driven by rejected supply. Instead, we see the opposite. The U.S. just printed roughly two-and-a-half trillion in deficits over the past year, and global investors absorbed every basis point of it.

That doesn’t sound like a fire sale. On the contrary, that looks like the strongest sustained demand for U.S. sovereign debt in history.

Read more: The Future Arrives Unevenly

Why Central Bank Gold Buying Reinforces Dollar Dominance

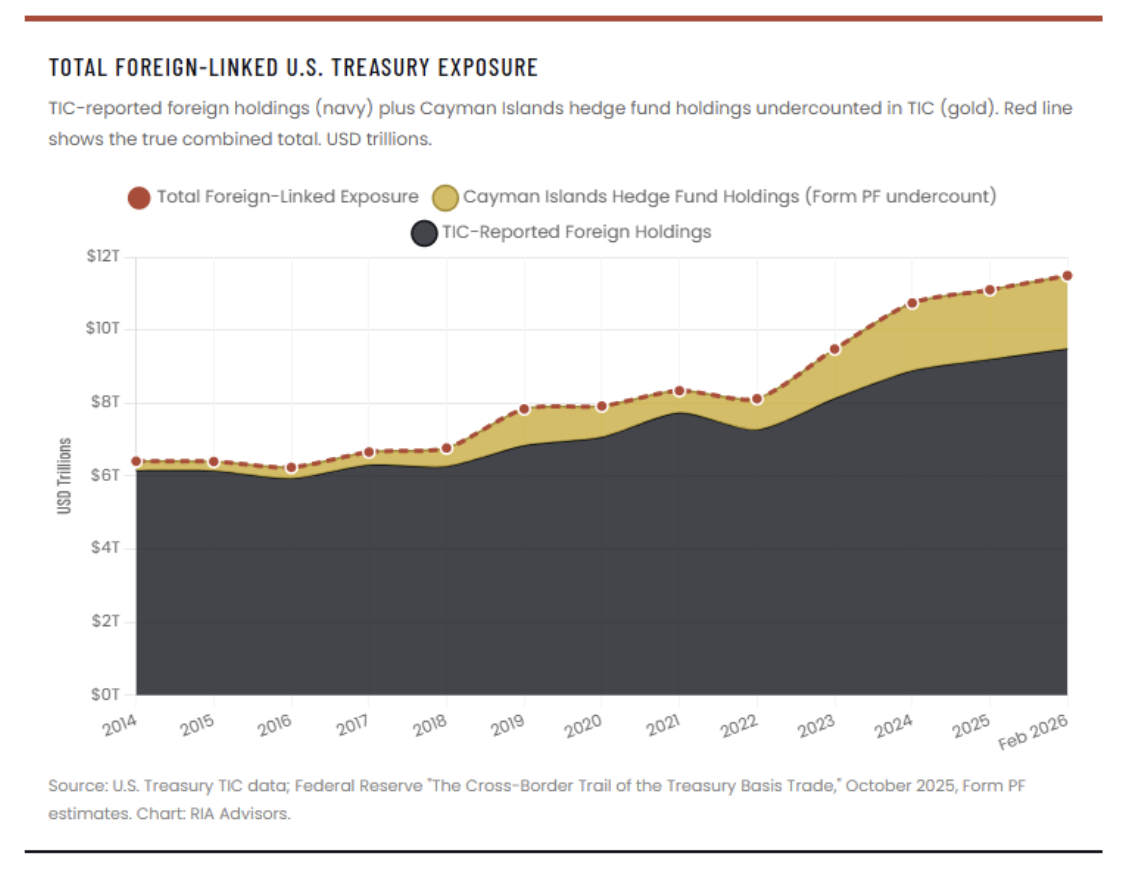

Here’s the part of the story the doomers consistently get wrong. The gold bugs have built an entire belief system on a category error. Of course, central banks have been buying gold in size. The World Gold Council’s Q1 2026 Gold Demand Trends report, published April 29, shows central banks bought 244 tonnes of gold net in Q1 2026 alone, up 3 percent year-over-year. That extends 17 consecutive months of net official-sector purchases, even with gold prices peaking above $5,400 an ounce in January.3 Total Q1 physical gold demand reached 474 tonnes, the second-highest quarter on record. Furthermore, the WGC forecasts roughly 850 tonnes of central bank purchases for full-year 2026, on par with 2025 and consistent with the multi-year pace. The trend is real and significant. However, it is not, in any practical sense, an escape from the dollar.

Gold is priced in dollars. The LBMA Gold Price, the global benchmark used to mark central bank holdings, settles in U.S. dollars per ounce. When the People’s Bank of China, the National Bank of Poland, or the Reserve Bank of India accumulates gold, the value of those reserves is reported, audited, and benchmarked in U.S. dollars. Of course, the unit of account doesn’t change just because the asset does. Furthermore, when those same central banks need to deploy gold for liquidity, the counterparty pricing reverts to dollars. That applies whether the deployment is through swaps, repo, or sale. The gold and dollar markets are not parallel systems. They’re the same system, with gold serving as a dollar-priced reserve asset.

That distinction matters because it reframes the entire de-dollarization narrative. A central bank that shifts 5% of reserves from Treasuries into gold has not abandoned the dollar. Instead, it has rebalanced inside the dollar-priced reserve system. The same is true for the Bank for International Settlements gold swaps, the Shanghai Gold Exchange yuan-quoted contract, and even the Russian central bank’s pre-sanction accumulation. Every one of those positions has a dollar-equivalent value because dollars are how the world prices reserve wealth. Even when gold is bought, sold, or pledged, the cross-rate to USD is the reference point. There’s no other deep, liquid pricing rail. In that sense, gold accumulation reinforces dollar dominance rather than threatens it.

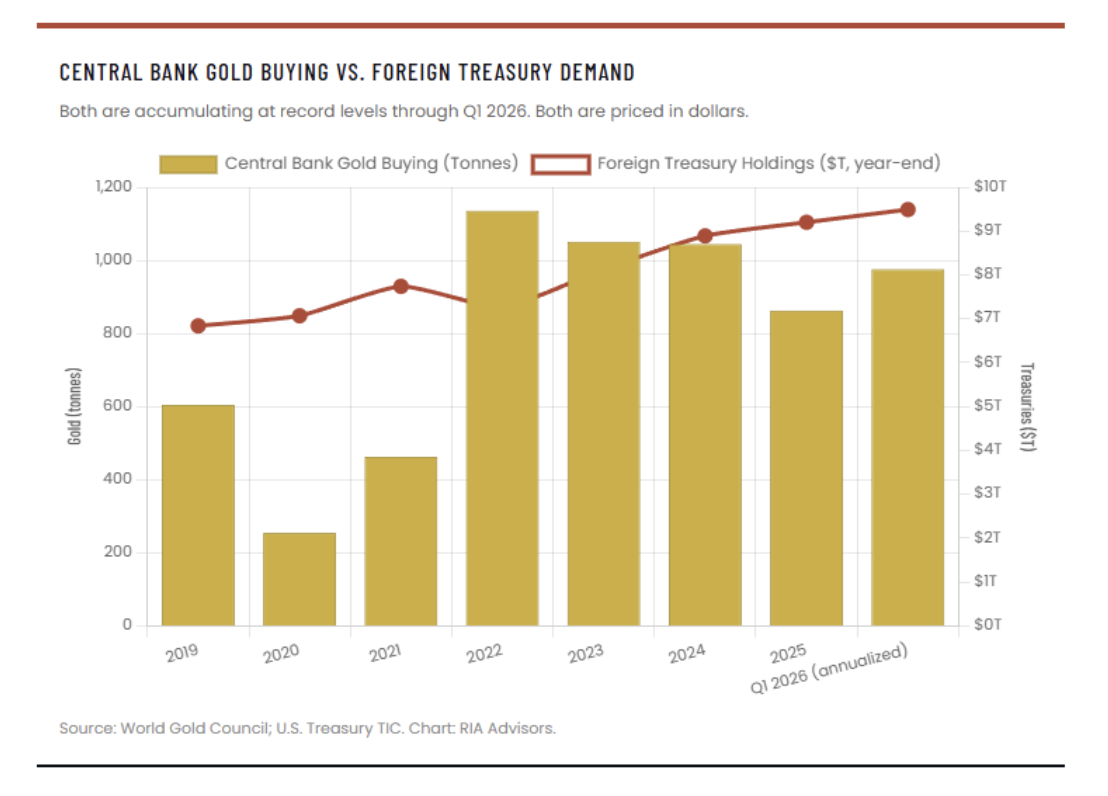

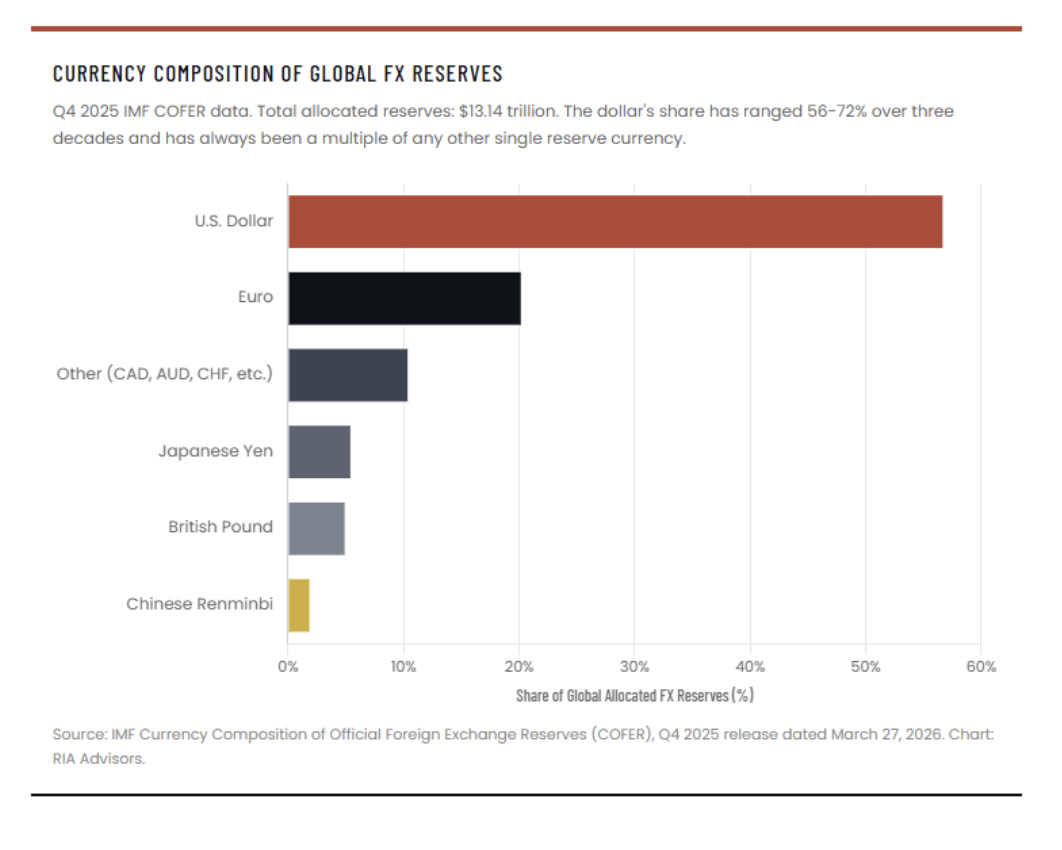

The same World Gold Council survey that gets cited to “prove” a dollar decline shows that 73% of central bank respondents expect a moderately or significantly lower USD share of reserves over the next five years. The doomers stop reading at that headline. The reality is that the IMF’s most recent COFER release, covering Q4 2025, puts the dollar’s share of allocated reserves at 56.77%. That figure is essentially flat versus the prior quarter, with most of the variation explained by exchange-rate effects rather than active selling.

Total foreign exchange reserves stood at $13.14 trillion at year-end 2025. The dollar’s share of reserves has fluctuated between roughly 56% and 72% over the past three decades. At every level, however, it has been a multiple of every other reserve currency combined. The euro sits at 20.25%, and the yen and pound around 5% each, with the yuan, despite all the hype, still under 2%.

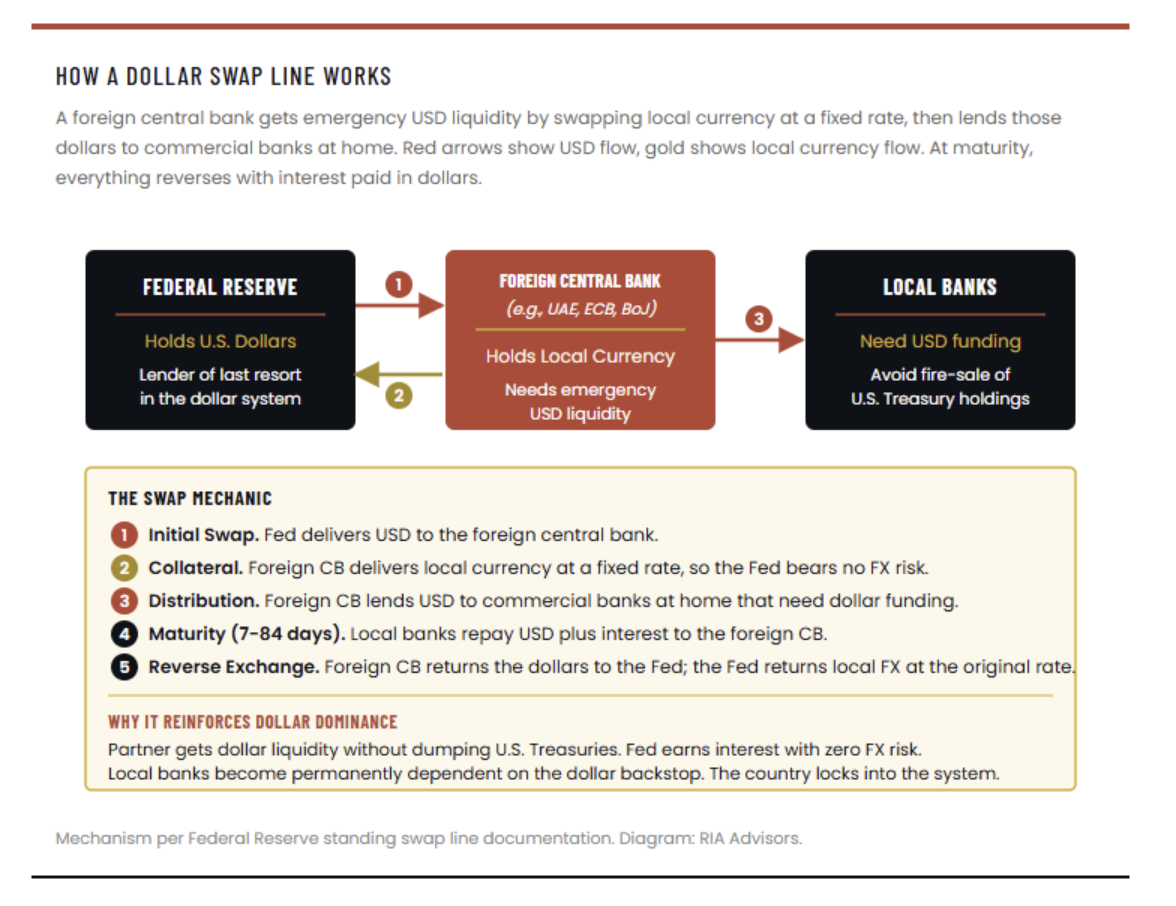

Bessent’s Dollar Swaps Extend Dominance

Indeed, Treasury Secretary Scott Bessent has spent the last several weeks discussing the possibility of extending dollar swap lines to allies in the Persian Gulf and Asia, with the United Arab Emirates as the lead candidate. Predictably, the doomers have framed this as a fire-sale-prevention move, claiming that Washington is offering swaps to keep Gulf sovereigns from dumping Treasuries amid the Iran conflict. However, that reading misses the strategy entirely.

Bessent said it himself in plain language. In his April 22 testimony to the Senate Appropriations Subcommittee, he stated that swap lines “are to maintain order in the dollar funding markets and to prevent the sale of U.S. assets in a disorderly way.” Two days later, in a coordinated X post, he went further: “Additional swap lines can benefit our nation by reinforcing dollar usage and liquidity internationally,” and “extending permanent swap lines can be a major first step in creating new U.S. dollar funding centers in the Gulf and Asia.” He closed with the line that defines the entire policy framework:

“Dollar dominance and reserve currency status are strengthened by constant long-term initiatives, including countering the growth of problematic, alternative payment systems.”

That’s not the language of a desperate Treasury Secretary trying to plug a leaky bid stack. On the contrary, that’s the language of a policymaker using monetary infrastructure to extend American financial reach. Swap lines are how Washington exports dollar liquidity. The 2008 crisis playbook used them defensively to backstop European and Japanese banks. Bessent is now reaching for the same tool offensively. He’s planting new dollar funding nodes in regions where alternative payment systems, including BRICS clearing rails and yuan-denominated commodity pricing, have been making noise.

Consider the geometry. Permanent swap line access turns a partner country’s central bank into a node of the dollar system. Once that line is in place, local banks have a guaranteed dollar liquidity backstop. As a result, there is no real incentive to develop a non-dollar alternative. The UAE flirted publicly with yuan-denominated oil pricing as recently as last year. A swap line eliminates that option in practice. It makes the dollar backstop too cheap and reliable to abandon. This is the same logic that has kept the existing G7 swap lines (Canada, ECB, Japan, UK, Switzerland) firmly inside the dollar orbit since the financial crisis.

Furthermore, this isn’t theoretical. Bessent has already run this playbook in practice. In September 2025, the Treasury used the Exchange Stabilization Fund to extend a $20 billion swap line to Argentina ahead of Milei’s pivotal October election. The strategic logic was identical. Reinforce dollar liquidity in a partner economy. Prevent disorderly Treasury liquidations during a political stress event. Lock the country into the dollar system at the moment of maximum strategic value. Bessent has publicly stated that the Argentina facility was fully repaid within months, validating the operational template. The UAE proposal extends the same framework to the Gulf, and the broader Asian conversation that Bessent referenced suggests the network is about to expand significantly.

Swap lines are the carrot. Sanctions are the stick. Bessent has been just as direct about the second tool as about the first, and the timing of the messaging is no accident.

Furthermore, in late April, the Treasury unveiled what it’s calling “Economic Fury,” a coordinated campaign to “systematically degrade Tehran’s ability to generate, move, and repatriate funds.” The mechanics are revealing. The U.S. Navy is enforcing a blockade of Iranian ports. Kharg Island oil storage is filling up because Iranian crude has nowhere to go. Tankers facilitating covert trade face direct sanctions exposure. Critically for this discussion, OFAC has already frozen $344 million in cryptocurrency wallets tied to the regime.

That last data point matters more than the doomers will admit. It directly validates the argument we made in our previous piece on digital dollar infrastructure. Stablecoin and crypto rails are not an escape from the dollar system. Instead, they’re an extension of it, with new enforcement capabilities attached. When Treasury can freeze nine-figure crypto positions through compliance pressure on issuers and exchanges, the supposed “uncensorable” alternative to dollar custody turns out to be more censorable, not less.

The reality is that dollar dominance is reinforced by both tools simultaneously. On the carrot side, you have liquidity provision, swap lines, digital dollar adoption, and the deep Treasury bid. On the stick side, you have sanctions reach, OFAC freezes, blacklisting, and naval enforcement of commodity flows. Of course, both capabilities are expanding, not contracting. Foreign reserve managers know this. Furthermore, they are also calculating that being inside the dollar orbit, even with custodial diversification, is far safer than being targeted by it.

The UAE OPEC Exit Validates the Strategy

Then came April 28. The UAE announced it was leaving both OPEC and OPEC+, dealing a heavy blow to the cartel and to its de facto leader, Saudi Arabia. The timing was not coincidental. Just six days earlier, Bessent had publicly endorsed an emergency dollar swap line for Abu Dhabi before the Senate. The UAE central bank governor, Khaled Mohamed Balama, had traveled to Washington during the IMF and World Bank spring meetings to meet with Bessent and Federal Reserve representatives.

Read the sequence carefully. First, Iran’s missile strikes hit Gulf infrastructure, and then the Strait of Hormuz closes. UAE faces a real liquidity stress event. Washington offers an emergency dollar backstop, security guarantees, and the deployment of Israel’s Iron Dome on UAE soil. Days later, the UAE walks out of the petroleum cartel that the doomers have spent years claiming was about to abandon the dollar in favor of a “petroyuan” alternative. Instead, the UAE just publicly chose the dollar bloc over its OPEC peers. The swap line offer didn’t avert a crisis through emergency liquidity. It reorganized a major Gulf state into the U.S. financial orbit at the moment of maximum strategic opportunity.

That is dollar dominance functioning exactly as Bessent described it in his testimony. Carrot first. Then, the strategic realignment is second. The petroyuan narrative just lost its most credible Gulf candidate.

Pushback: But What About De-Dollarization?

The strongest version of the de-dollarization argument runs as follows. After the 2022 sanctions on Russia froze roughly $300 billion in central bank reserves, every other sanction-vulnerable country had to reassess custodial risk. China shifted holdings from direct U.S. custody to Belgium and Luxembourg. BRICS expanded membership. The Saudi-Iran rapprochement, brokered partly by Beijing, signaled a regional pivot. In addition, Russia and China increased bilateral trade settled in yuan and rubles. All of this is true.

However, none of it actually undermines dollar dominance at the system level. Sanction-driven custodial diversification moves Treasuries from the New York Fed to Euroclear. Yet it doesn’t move them out of the Treasury market. China’s reported direct holdings have declined, but its total exposure, including third-country custody, has remained roughly flat. Furthermore, BRICS settlement still reverts to dollars at the cross-border invoicing layer. No participant wants to hold rubles, rupees, or yuan as a long-term store of value. Bilateral yuan settlement, despite the headlines, remains a sliver of total trade flows.

The reality is the doomers are confusing diversification with abandonment. Foreign reserve managers are doing two things at once. First, they’re spreading custodial risk across more jurisdictions. Second, they’re adding gold as a politically neutral hedge. Both moves leave the dollar as the dominant unit of account, the dominant settlement asset, and the dominant store of value. As shown above, the share has barely moved.

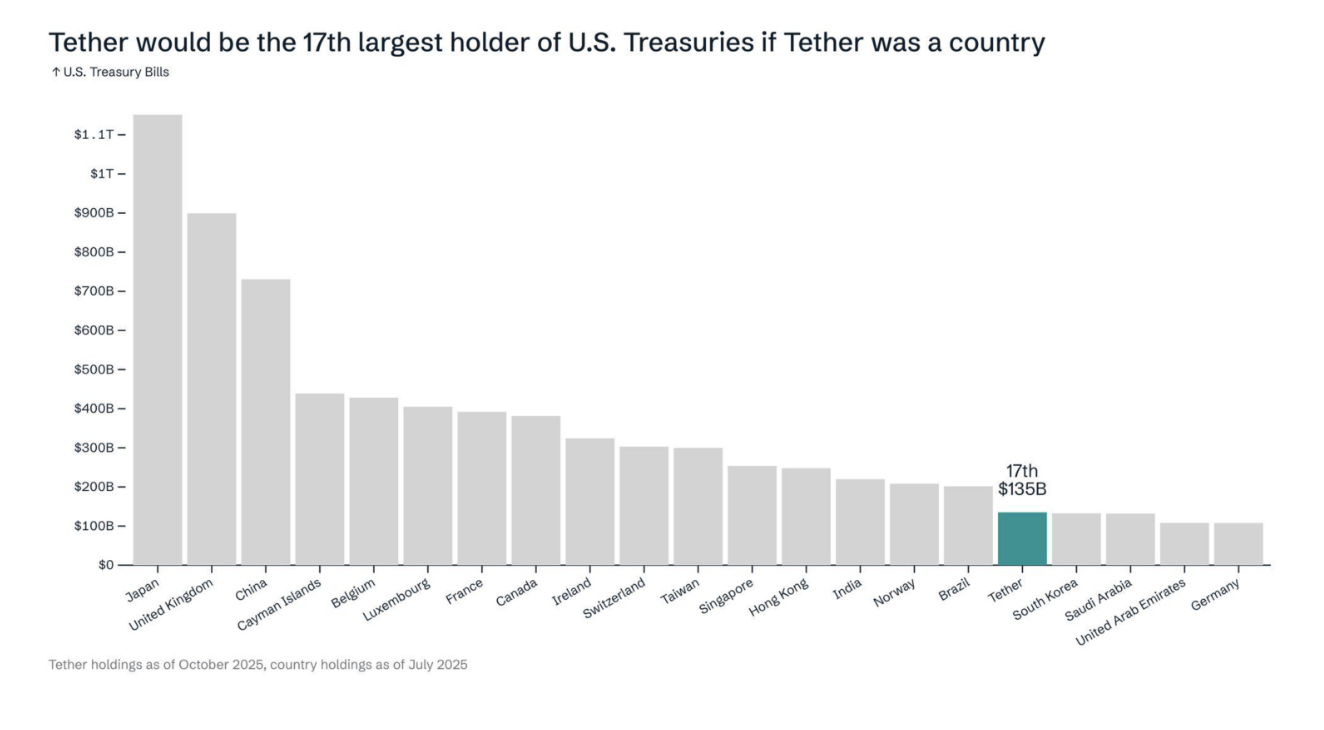

Beyond the traditional reserve channel, digital dollar infrastructure is rapidly expanding the dollar’s reach into emerging markets. Demand for dollar-denominated digital tokens has hit all-time highs in Latin America, Africa, and Southeast Asia. Tether’s Q1 2026 attestation, published May 1, confirmed direct and indirect U.S. Treasury exposure of approximately $141 billion as of March 31, against $191.8 billion in total assets and $183.5 billion in liabilities. The reserve buffer reached a record $8.23 billion, and Q1 net profit hit $1.04 billion. That makes Tether the 17th largest holder of U.S. Treasuries globally.

Furthermore, USDT circulation grew by more than $5 billion during April alone, pushing total supply above $188 billion. In Latin America, dollar-pegged digital tokens accounted for 40% of crypto purchases in 2025, surpassing Bitcoin’s share. The Bitso report on 10 million Latin American users described the trend bluntly as “digital dollarization.” That kind of grassroots demand is dollar dominance in action at the consumer layer.

The GENIUS Act, signed into law last July, created the first federal framework requiring permitted issuers to back tokens with high-quality liquid assets, primarily short-term Treasuries. The April 2026 FinCEN/OFAC proposed rule extends sanctions enforcement directly into the issuer layer. As a result, Washington can freeze, block, or seize dollar-denominated digital tokens through the issuer’s compliance program. That isn’t a workaround away from the dollar system; it’s an extension of it, with new enforcement rails attached.

What This Means for Investors

The investment implications cut several ways. First, foreign demand for U.S. Treasuries is structurally strong, which keeps a bid under the long end of the curve even as deficits widen. Indeed, that’s bullish for duration. Second, central bank gold buying creates a price floor under bullion that didn’t exist in prior cycles. Investors should hold some allocation to gold. However, they should hold it for the right reason. It’s a dollar-priced inflation hedge and a political risk diversifier, not a fiat escape hatch. Finally, the digital dollar buildout is creating a new investable vertical. Custody, payments infrastructure, and compliant on-ramp providers (CRCL, COIN, V, MA, JPM, BK) sit at the intersection of fiat and digital dollar plumbing.

The contrarian read is this. If you bought into the dollar collapse narrative over the last five years, you missed gains in U.S. equities. You missed the Treasury bid that compressed yields during recent risk-off episodes. You probably overweighted gold and Bitcoin at peaks. The bottom line is that the trade that has worked across cycles is owning U.S. assets denominated in U.S. dollars. Diversifying across the dollar-priced reserve system has worked. Diversifying against it has not.

What does this mean for portfolio positioning right now? It means duration risk is rewarded by structural foreign demand. Equity risk is supported by the dollar-priced earnings of multinational franchises. Gold belongs in the portfolio at a strategic weight, not a doomsday weight. Furthermore, investors should pay close attention to which firms are positioning for the digital dollar buildout. That’s where the next leg of dollar dominance is happening.

The doomers will keep selling fear. That’s the business model. Make no mistake, real risks exist. Fiscal trajectory, debt servicing costs, sanctions blowback, and CBDC competition are all worth tracking carefully. However, none of those risks add up to the collapse narrative being pitched on social media every other day. The reality on the tape is that foreign Treasury demand is at an all-time high. Central bank gold buying continues to reinforce dollar pricing. Swap lines are being deployed offensively to extend dollar reach. Digital dollar infrastructure is colonizing real-time commerce in emerging markets.

If the dollar were truly dying, none of this would be happening. The fact that all of it is happening simultaneously tells you everything you need to know about where the smart money is positioning. The dollar isn’t dying. It’s evolving. And dollar dominance is going to be the central pricing rail of the global financial system for a long time yet.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All