Investment Discipline Amid the AI Infrastructure Boom

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- The AI boom is generating tremendous physical infrastructure needs. Data centers, power production, and chips must be built to support AI’s growth, creating long‑lasting investment opportunities.

- Many of the biggest areas of opportunity are in bonds and loans. Large, established technology companies are increasingly borrowing to fund infrastructure spending, opening a door for fixed income investors.

- Focus on well-structured deals with claims on hard assets. By investing in essential infrastructure through secured financings, one can seek steady returns while mitigating risk – even as technology continues to evolve.

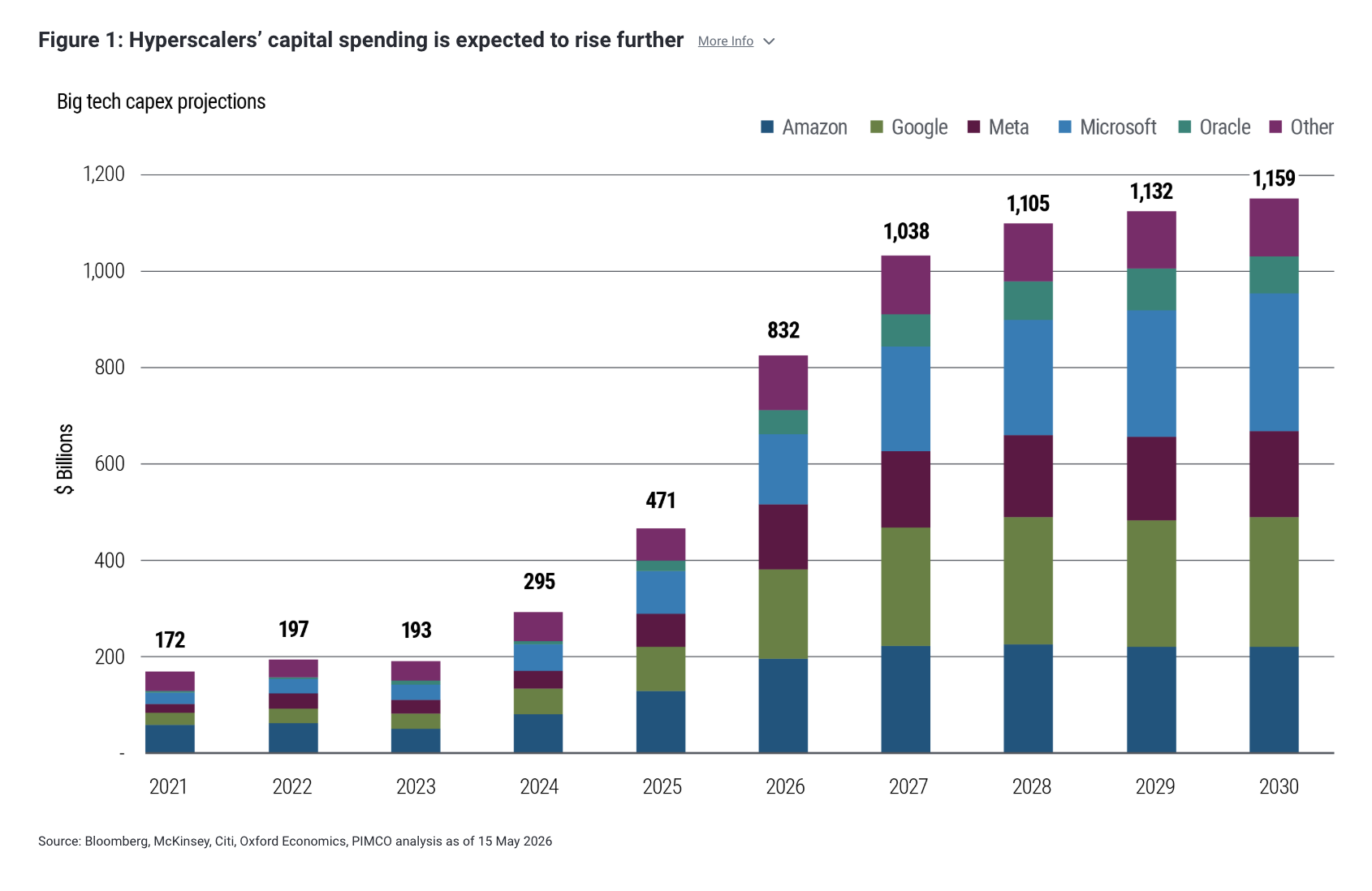

Businesses are racing to build the physical infrastructure that makes AI usable at scale – data centers, the graphics processing unit (GPU) hardware stack, power, and cooling. Estimates suggest more than $5 trillion could be needed through 2030 to fund this buildout across the broader AI ecosystem (see Figure 1). For investors, the opportunity is not just the scale of spending; it’s the ability to finance essential infrastructure through structured credit backed by real assets and predictable, contracted cash flows.

The key question is how to commit capital to long-duration projects while technology and business conditions evolve. In our view, rather than trying to pick AI winners, the answer is to focus on the infrastructure layer itself – one layer below the AI applications – through enforceable collateral, control over key contracts, and protections that help ensure repayment even if things don’t go as planned.

Stewardship also matters in how these projects are developed. The strongest data center investments are built in partnership with local utilities and communities. Done well, they can add needed power and grid infrastructure, distribute fixed costs, support local economic development, and avoid worsening affordability by ensuring that communities share in the benefits of the buildout. We look for projects where the data center contributes to the broader infrastructure needs of the region, rather than simply adding power demand to an already constrained system.

Counterparty quality matters as well. Large global hyperscalers – the biggest tech companies and cloud service providers – typically have diversified revenues, strong balance sheets, and long-term strategic flexibility, even as their capital spending continues to rise. By contrast, tenants tied solely to a single AI application and still operating at a loss present very different risks.

Read more: AI Credit Expansion: Assessing the Micro and Macro Risks

What a well-structured deal looks like

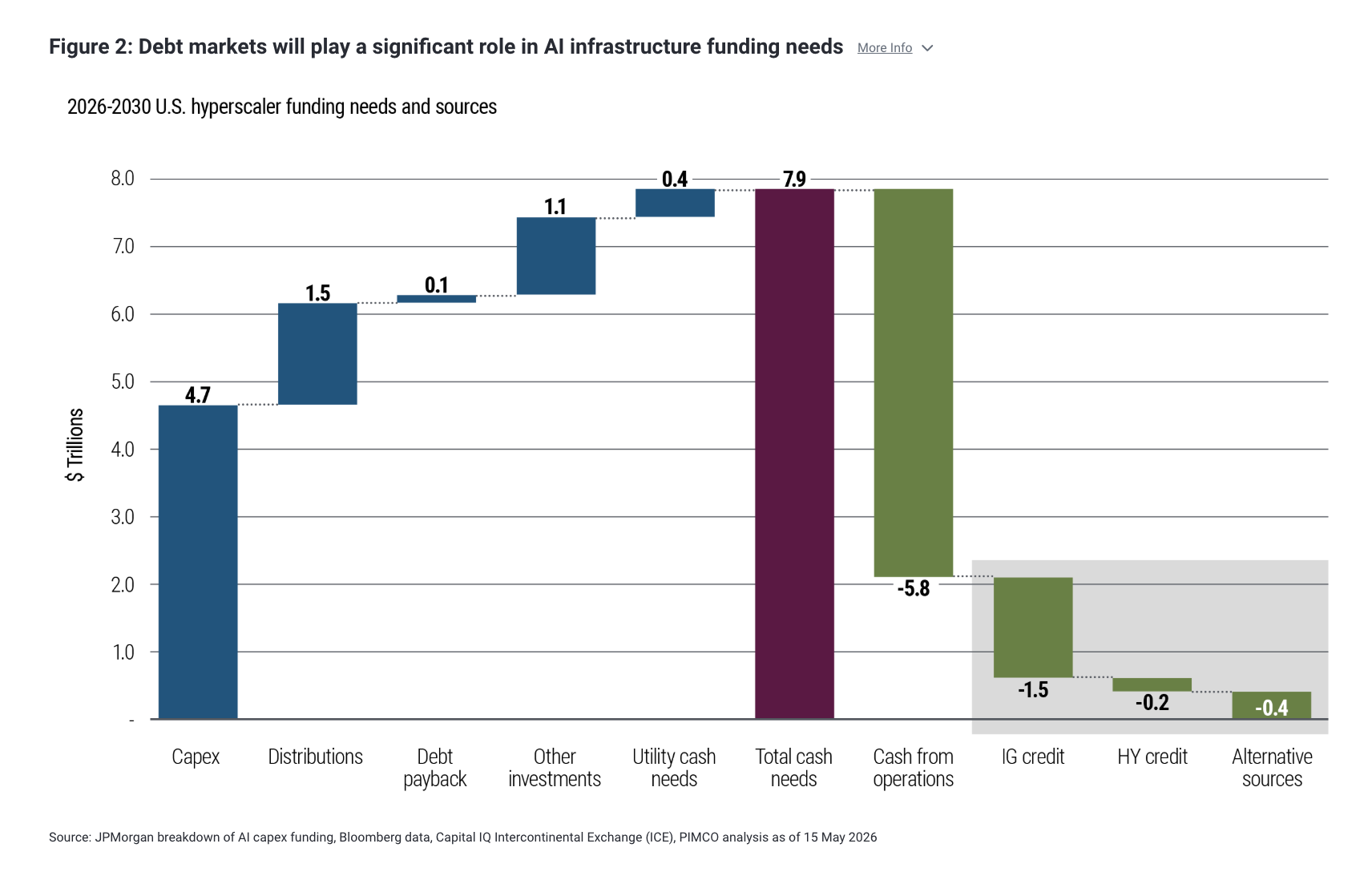

Of the $5 trillion in potential capital spending through 2030, we estimate that upwards of 40% may need to be financed through debt markets (see Figure 2). This anticipated wave of new borrowing makes it especially important to be selective and to structure deals carefully (for more, see our 22 May publication, “AI Credit Expansion: Assessing the Micro and Macro Risks”).

In this context, secured financing means investors have direct claims on the physical assets, lease revenues, and contracts that generate cash flow – not just a general promise to repay. In GPU financings, that extends to liens on the chips themselves and the accounts that collect revenue. Key contracts, such as data center leases and power purchase agreements, should also be pledged and locked into the collateral package.

Equally important are cash flow controls. If revenue falls short or debt coverage ratios drop below agreed thresholds, a well-designed structure can redirect cash into reserve accounts to protect lenders – with debt paid down more quickly if the shortfall persists.

When it comes to deal pricing, credit spreads should reflect not just today’s risk, but also the supply outlook in a sector where longer-term debt issuance is rapidly ramping up. In our view, investors should seek to maximize liquidity, recognizing that bespoke, private-credit-style safeguards do not have to come at the expense of tradability. Structures such as Rule 144A private placement bonds can help preserve flexibility and accountability for issuers, while allowing large investors known as qualified institutional buyers (QIBs) to trade the securities in a deep and liquid market (for more, see our March 2026 commentary, “Spreads May Be Converging Across Public and Private Markets, But Liquidity Is Not”).

Areas of caution

In a sector awash with enthusiasm, some of the most important decisions involve knowing what to avoid.

Speculative builds without contracted cash flows. Repayment that depends on future demand rather than signed, enforceable contracts introduces risks that may not be adequately compensated. Investors should look for deals backed by committed agreements with creditworthy counterparties. We prefer structures where repayment is driven by committed contracts with clear remedies and lender control over the associated cash flows.

Maturity and repayment risk. A 20-year hyperscaler lease financed by a five-year debt maturity creates risks if market conditions make refinancing a challenge. Given the volume of five-year maturities being issued across the sector, a refinancing wall of potentially hundreds of billions of dollars could emerge in 2030. Structures that pay down debt over time from lease cash flows – rather than relying on refinancing – are more resilient. The same principle applies to residual value: It is nearly impossible to predict what data centers or GPUs will be worth in five to 10 years, so a conservative approach assumes zero residual value, with debt paid down entirely from contracted cash flows. Our bias is for liabilities that amortize from contracted cash flows and do not depend on favorable refinancing conditions down the road.

Lack of transparency into underlying contracts. Lease termination provisions, construction delay clauses, force majeure clauses, power interruption remedies, and casualty-event mechanics can all materially reduce contractual cash flow or reduce payments below what is needed for debt service. Investors who cannot conduct diligence on the underlying contracts face risks that are hard to fully assess. If we cannot diligence the actual contract mechanics, we treat the risk as unpriced and step back.

Discipline over FOMO

The expansion of AI infrastructure is a multiyear investment cycle that will generate deal flow across asset types, geographies, and capital structures. The sheer volume of expected financing needs is an advantage for disciplined investors: There is no need to chase any single transaction.

We believe the most durable approach involves focusing on the infrastructure layer rather than making bets on which AI applications will ultimately prevail. In a sector defined by rapid change, investing one layer below the technology itself – with real assets, strong collateral, and clear cash flow controls – is how debt investors can participate without sacrificing the discipline that protects capital when cycles turn.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission.| PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany) is authorized and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). | PIMCO Europe GmbH Italian Branch (Company No. 10005170963, Via Turati nn. 25/27 (angolo via Cavalieri n. 4) 20121 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain), PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50–52 Boulevard Haussmann, 75009 Paris, France) and PIMCO Europe GmbH (DIFC Branch) (Company No. 9613, Index Tower Floor 10, unit 1001 Dubai International Financial Centre, Dubai, United Arab Emirates) are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Title V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively, (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF and (6) DIFC Branch: Regulated by the Dubai Financial Services Authority ("DFSA") (Level 13, West Wing, The Gate, DIFC) in accordance with Art. 48 of the Regulatory Law 2004. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. According to Art. 56 of Regulation (EU) 565/2017, an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO Europe GMBH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2, Brandschenkestrasse 41 Zurich 8002, Switzerland). According to the Swiss Collective Investment Schemes Act of 23 June 2006 (“CISA”), an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO (Schweiz) GmbH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (8 Marina View, #30-01, Asia Square Tower 1, Singapore 018960, Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited (Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance Street, Central, Hong Kong) is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Investment Management (Shanghai) Limited. Office address: Suite 7204, Shanghai Tower, 479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social credit code: 91310115MA1K41MU72) is registered with Asset Management Association of China as Private Fund Manager (Registration No. P1071502, Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. To the extent it involves Pacific Investment Management Co LLC (PIMCO LLC) providing financial services to wholesale clients, PIMCO LLC is exempt from the requirement to hold an Australian financial services licence in respect of financial services provided to wholesale clients in Australia. PIMCO LLC is regulated by the Securities and Exchange Commission under US laws, which differ from Australian laws. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. member of Investment Management Association of Japan and Type II Financial Instruments Firms Association. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is an independently operated and managed company. The reference number of business license of the company approved by the competent authority is (115) Jin Guan Tou Gu Xin Zi No. 006. The registered address of the company is 40F., No.68, Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan (R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | Note to Readers in Colombia: This document is provided through the representative office of Pacific Investment Management Company LLC located at Carrera 7 No. 71-52 TB Piso 9, Bogota D.C. (Promoción y oferta de los negocios y servicios del mercado de valores por parte de Pacific Investment Management Company LLC, representada en Colombia.). | Note to Readers in Brazil: PIMCO Latin America Administradora de Carteiras Ltda.Av. Brg. Faria Lima, 3477 Itaim Bibi, São Paulo - SP 04538-132 Brazil. | Note to Readers in Argentina: This document may be provided through the representative office of PIMCO Global Advisors LLC AVENIDA CORRIENTES, 299, Buenos Aires, Argentina. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2026, PIMCO.

CMR2026-0518-5503016

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All