Trying Tango

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEditor’s Note: Last month, I attended a meeting of global chief economists in Argentina. Following are the key observations that emerged from our conversations.

The name “Buenos Aires” was given to our host city by the Spanish conquistador Pedro de Mendoza. It had a dual meaning: it was both a tribute to the favorable winds that aided passage across the Atlantic and the cooler air that held down the mosquito-borne diseases typical of countries to the north.

The city’s position at the head of the Rio de la Plata made an ideal commercial center. It developed into a major trade route for Argentina’s agricultural and mineral exports, and it served as a channel for waves of inbound immigration. The wealth of the city, and the architecture it supported, earned Buenos Aires the nickname of “The Paris of the South.”

Walking through the city’s neighborhoods, you can see the vestiges of the fin de siècle style. But you can also see the signs of decay brought on by decades of financial mismanagement and complicated politics.

Argentina’s experience with trade, debt, demographics and natural resources made it a fitting place to discuss those themes, which are pressing in the present day. My peers and I maintain reasonably favorable forecasts for the global economy, but we sometimes felt surprised that the numbers were so positive when the wall of worry is so tall.

Following are summaries of the discussions, grouped by major topic.

Read more: Guided by Fundamentals: Navigating Emerging Markets with Value

The Spoil of War

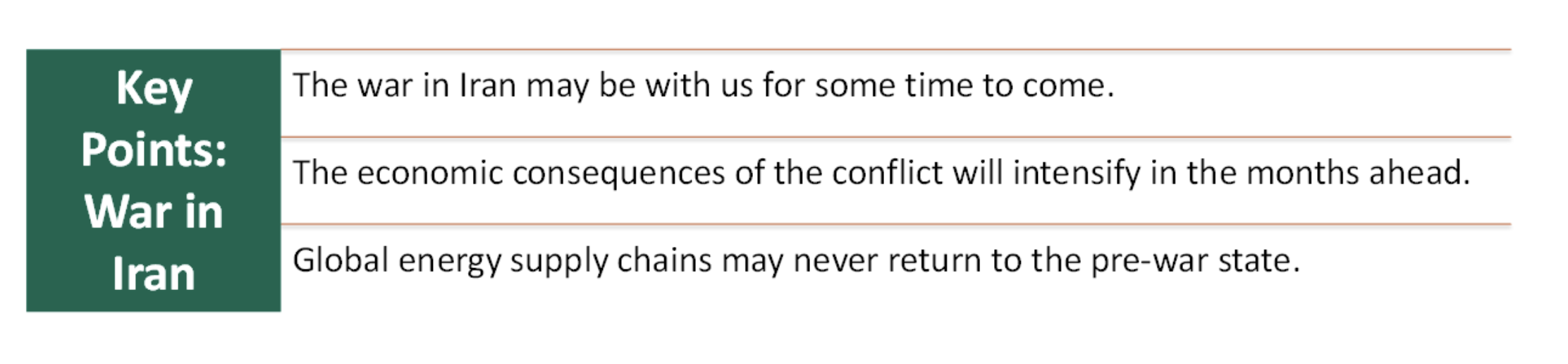

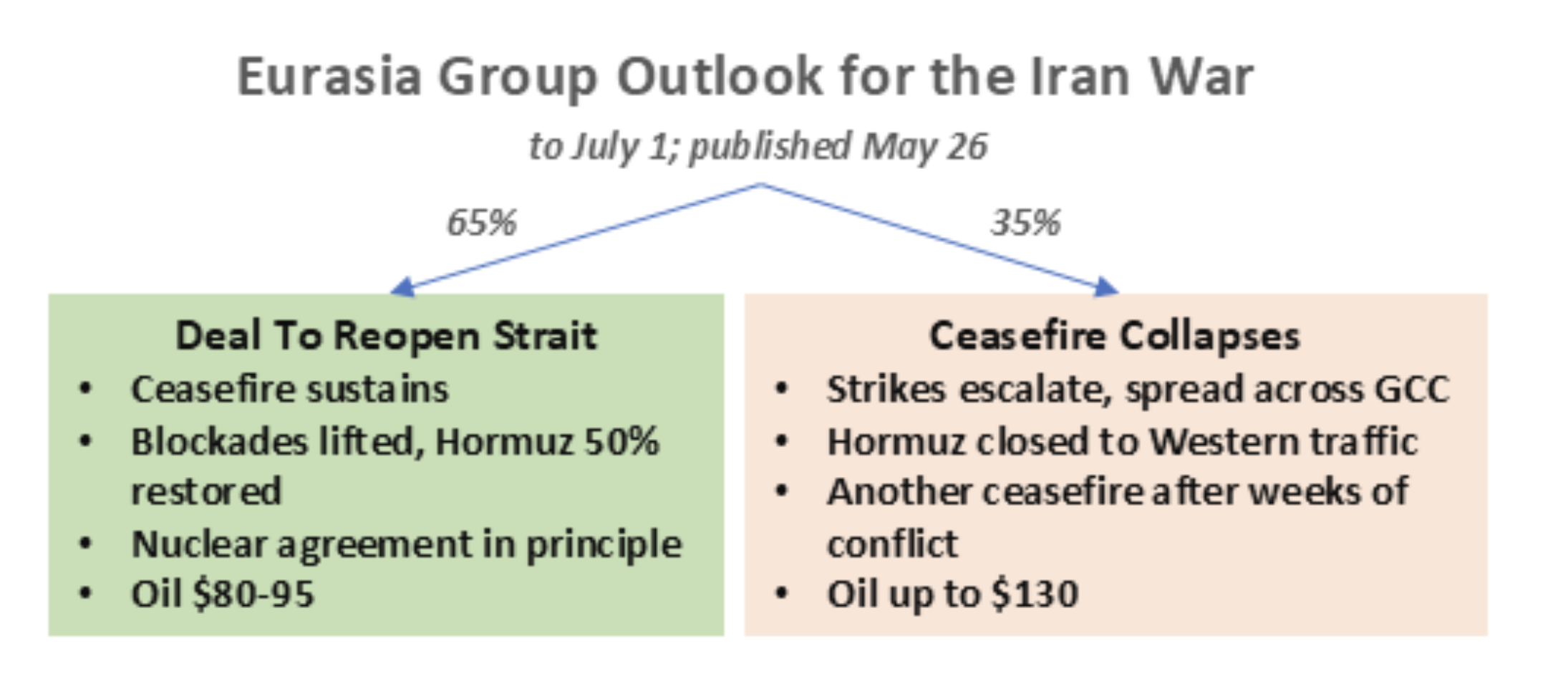

Despite periodic reports of progress in negotiations, the consensus among the group seemed to be that the conflict will be with us for a while longer. The distance between negotiating positions and the challenge of mediating among a multitude of stakeholders suggest a timeline measured in months.

The potential economic consequences of the war cover a wide range. Oil prices are the main variable in each scenario, but not the only one. It was interesting, if somewhat alarming, to hear members describe the range of disruptions caused by the conflict. They go beyond basic commodity shortages (oil, fertilizer, plastics, helium, etc.) to a host of finished products whose supply chains have been compromised. Some regional scarcities will be particularly challenging to deal with, such as dislocations related to jet fuel.

Stockpiles have been drawn down to support production, and simple shipping adaptations have been applied. But these measures cannot be sustained indefinitely. More severe shortages and much higher prices could take hold as the conflict wears on; even if resolution is reached, normalcy may take a long time to restore. Inflation may follow a steeper trajectory than many anticipate.

The war has produced the third global supply shock of this decade. Four years ago, the Middle East was a source of resilience when the fighting in Ukraine began; the Gulf is now seen as a source of vulnerability. Even if peace is achieved soon, this manifestation of regional instability will lead countries and companies to reconsider the wheres and whats of energy sourcing.

Counting The Costs

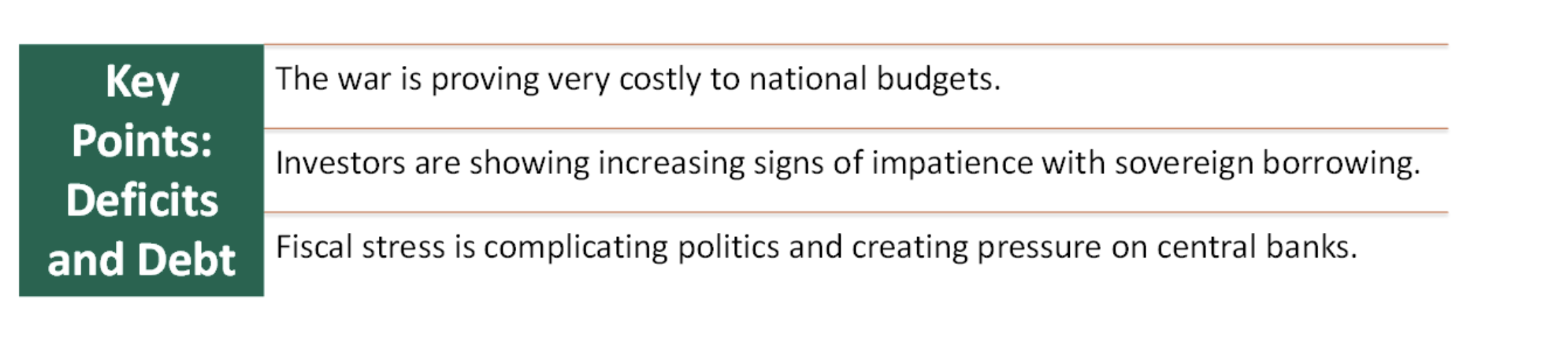

The situation in the Middle East will take a steep toll on national budgets, even in countries far from the fighting. The added fiscal stress comes at an uncomfortable time.

The combatants are spending billions on arms. Substantial damage has been done within the region, which will be costly to repair. A range of countries have offered subsidies to buffer costs to consumers. Economic growth and national revenues have diminished.

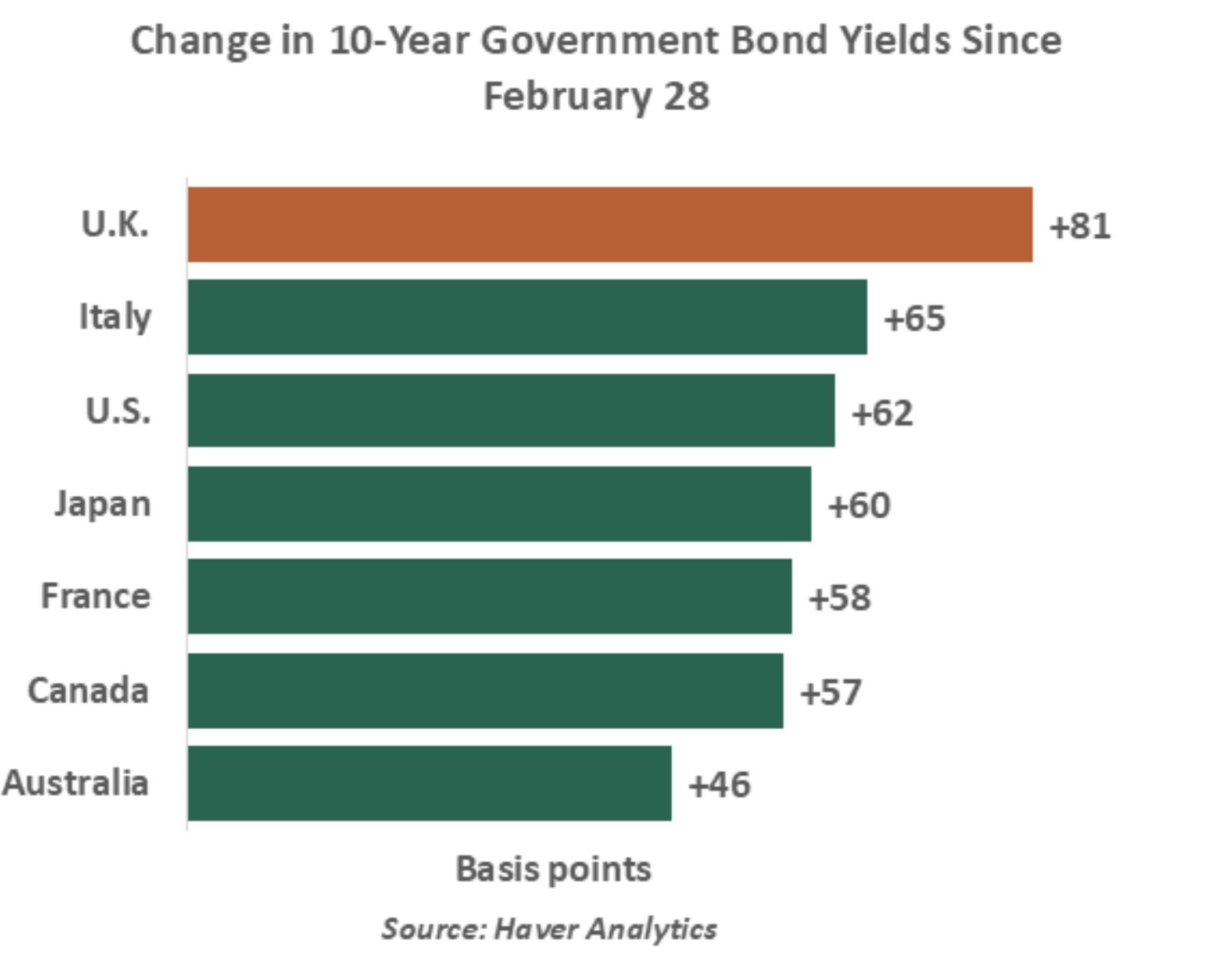

But the most significant change in sovereign finance centers on debt service. Interest rates across countries and across the maturity spectrum have increased significantly since the beginning of March. Prospects for higher inflation have changed the outlook for global monetary policy and led bond investors to demand higher yields.

Increased interest payments will diminish budget buffers and crowd out other spending priorities. Countries that operate under formal or informal deficit targets will be particularly pressured: the United Kingdom is chief among them. Questions about whether governments can sustain the debt they have accumulated are mounting.

The group noted that budget pressure has created, and been exacerbated by, political instability. Timelines for implementing economic plans in most countries now match election cycles; there is little room for long-term thinking. Increasingly, governments are pressuring their central banks for support, through lower rates and ownership of sovereign debt. These are two forms of financial repression.

But global monetary policy is moving in the opposite direction. Inflation is likely to lead to overnight rate increases during the balance of 2026, and central banks from Tokyo to Washington are seeking ways to reduce their balance sheets.

There was consensus among the group that quantitative tightening amid a backdrop of rising sovereign debt would be a very delicate process. It will be hard to determine a level of reserves that supports market function without raising concerns over monetizing government debt. Recent tests of central bank independence have been passed, but those tests may keep on coming.

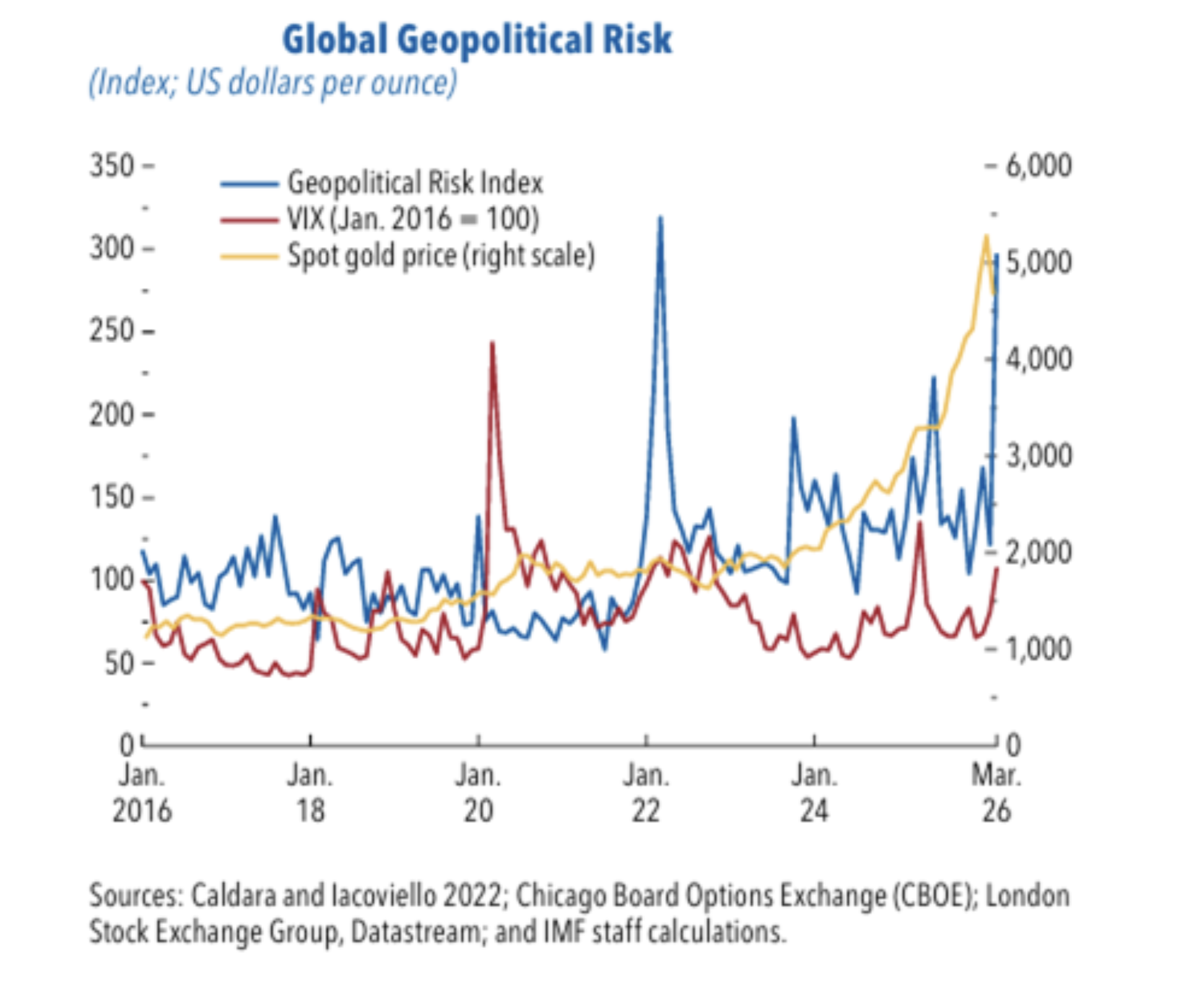

Loss of Order

Geopolitical risk dominated the roster of top concerns that emerged from the group’s outlook survey. The Iran conflict has added another shock to the rise of tariffs, the war in Ukraine, and lingering impacts of the pandemic. Against that backdrop, the resilience of global growth has been remarkable, but there are questions over how long that can be sustained.

At the moment, the war is dominating our thinking. But our group didn’t have to strain much to describe other proximate scenarios that might have comparable effect. Potential action by China against Taiwan headlined this list.

The decline of the old global order may not have led to the current conflict; the Middle East has been fought over for centuries, and it has been particularly volatile over the past 60 years. But weaker international coordination will make it harder to bring the fighting to an end and to manage the recovery process.

The root causes of global disengagement date from the 2008 financial crisis. Since then, trade flows have leveled and cross-border capital flows have diminished. The consequences are lower levels of economic growth, reduced investment and innovation, and greater exposure to shocks.

Multilateral organizations designed to promote economic integration and global stability have often failed to deliver on their promises. Trade has displaced workers in a number of locations, and their anxieties have driven elections and informed policy. Regions and countries are looking inward as they steer economic policy. Political parties aiming to put their countries first have multiplied.

This has been especially hard for Europe. Efforts to increase innovation as a path to improve Europe’s sluggish productivity growth are still fragmented, and behind schedule. Funds have been appropriated to enhance security, but deployment has been slow. Financial integration, which would include a saving and investment union, still seems far off.

The group was encouraged by the recent Hungarian election, which removed an obstacle to continental collaboration. But nationalist parties in other European countries remain well-entrenched. Poor economic results may bolster their standing.

A central question of our conference was whether the aggressive tone from Washington that has prevailed over the past 16 months is temporary or permanent. The sustainability of the Trump agenda will be tested in the November mid-term elections, and international interest in the outcome is very high. Divided government is the most likely outcome.

The U.S. tariff program will be among the issues in focus for voters. American courts have undercut the basis for most of the tariffs implemented over the past year; the government has been ordered to refund $166 billion to those who paid them. Efforts are underway to restore some of the tariffs, but the U.S. has clearly lost trade leverage.

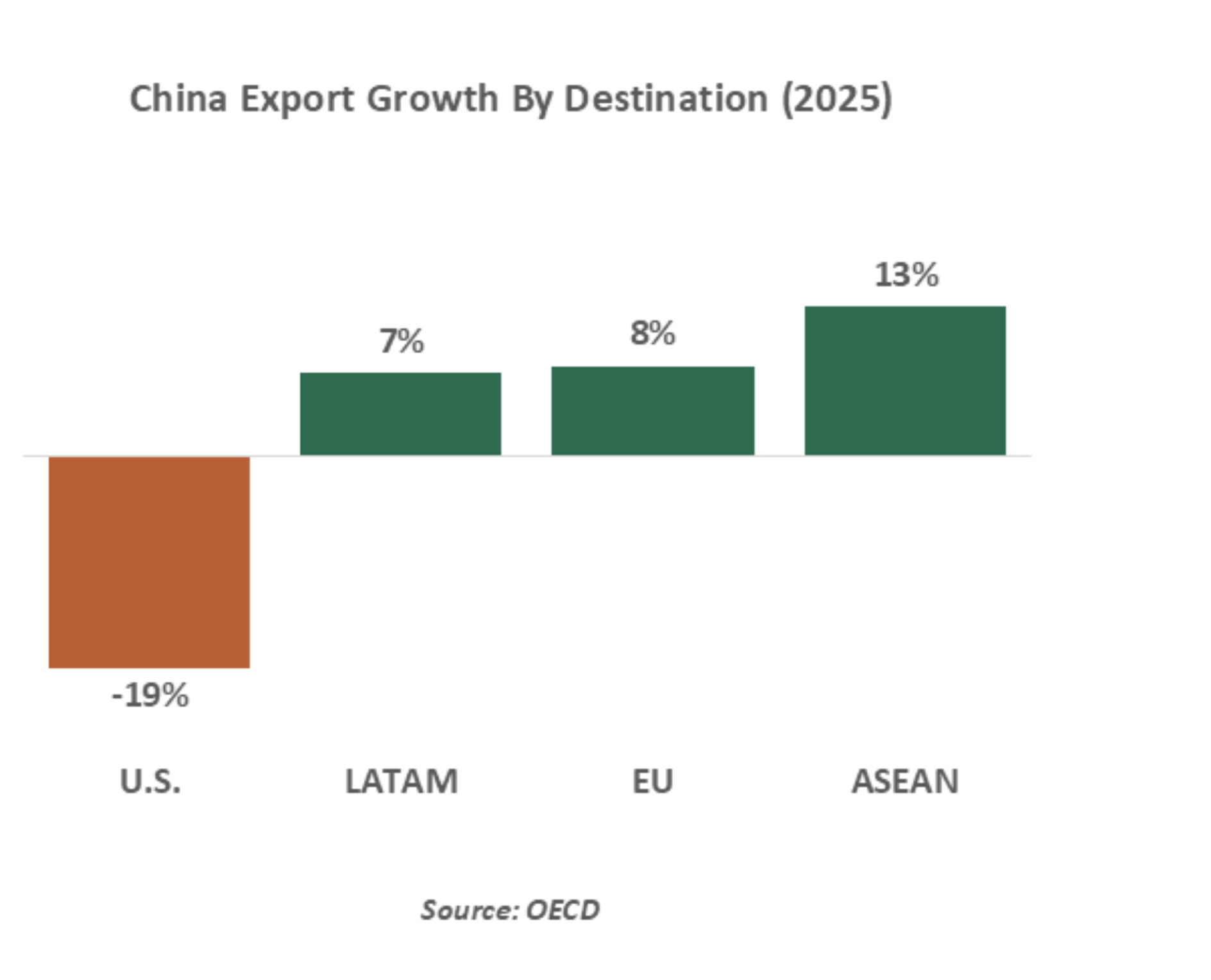

Middle powers like Canada and Australia have opened their options with China and planned for additional self-sufficiency. Inbound industrial investment to the U.S. has not changed course. Tariff uncertainty has been unhelpful to U.S. multinationals.

China, the main target of American trade antipathy, has continued to grow its exports. Shipments to the U.S. are down, but sales to other regions have more than compensated. Transshipment has been used effectively as an evasive measure; the ability of the White House to combat this practice may be limited.

Seeking A Copilot

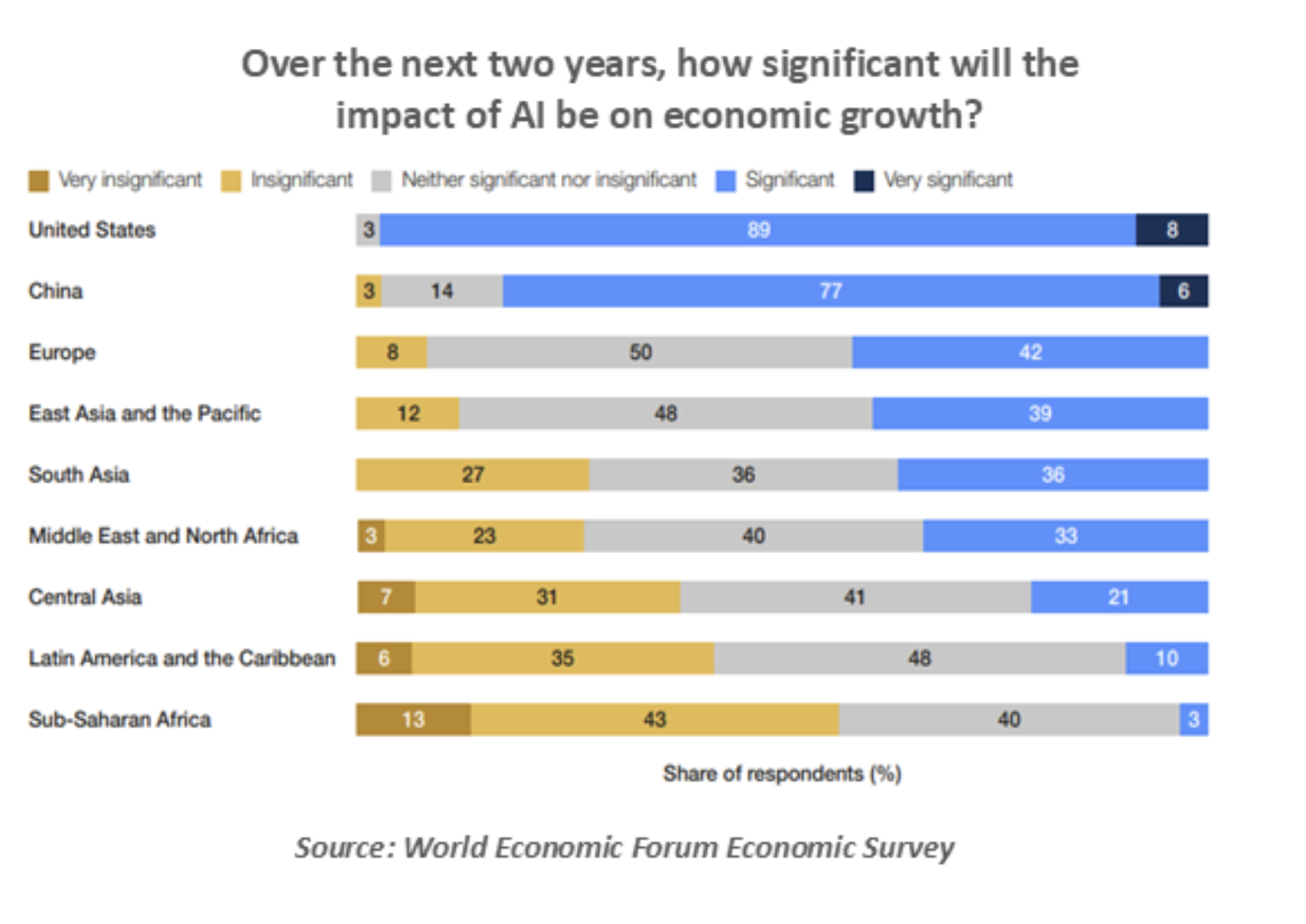

There were several sessions during the conference that focused on AI. At times, it seems like there are two different economies: the “normal one” and the one focused on tech development. The latter has progressed in a manner that seems almost impervious to the challenges being faced by the former.

The stakes are substantial. Demographic decline and debt increases make it imperative that countries find ways to sustain economic growth. AI presents an avenue to increase productivity, which would be very much welcome. There are no real alternatives with the same promise.

But realizing the full benefits of AI may take time. Adoption curves have shallow slopes; data quality can limit the effectiveness of agents; power and water shortages may limit capacity; and the appearance of Anthropic’s Mythos highlights the cyber security risks created by the new technology.

Different members of our group have attempted to plot the progress of AI-related productivity, but the exercise is highly imprecise. But there was consensus that China and the U.S. will lead, and other regions will lag.

The debate over whether the primary outcome of AI will be job displacement or job augmentation is a very active one. AI does appear to be impeding job prospects for software professionals and those new to the labor force; it is also showing its potential for disrupting business models. Regulations to limit the impact of AI on employment may ultimately be implemented in several places.

Economies around the world aren’t just reliant on AI investments for growth. The appreciation of AI stocks has supported spending, which is following “K-shaped” patterns. A significant correction to the valuations of tech leaders would therefore be even more likely to result in recession.

Summing Up

As I prepared to distill this year’s proceedings, I took a look back at last year’s conference summary, which was entitled “The Great Unwind.” The 2025 meeting took place close to “peak tariff,” and there wasn’t a great deal of optimism among the membership. And yet most economies and markets have performed very well since then. I share this to highlight the resilience that has been on display, and that hopefully will be sustained.

On the last evening of our formal program, we had the chance to experience tango. The tango is more than just a dance. It symbolizes tension, conflict and reconciliation between partners. All of those assembled expressed the wish that the countries of the world are dancing in better unison, and more closely a year from now.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All