Risk Management For Retirees: When To Reduce Exposure

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Last week, a viewer of the Morning Show emailed me about risk management for retirees. He asked the single most important question retirees face, and rarely get a straight answer to.

He’s right. And the conventional advice he’s been given is wrong.

Read more: Dollar Dominance Remains Alive And Well (Part 1)

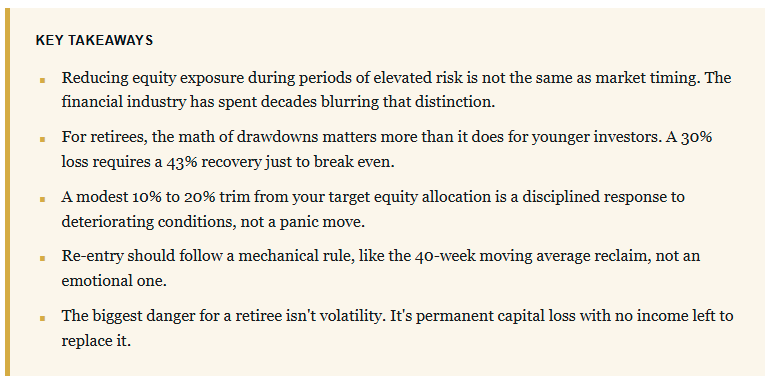

Risk management for retirees is not the same as market timing, and the financial industry has spent the better part of three decades blurring that distinction. The blur costs retirees real money, because by the time they figure it out, they’ve already sat through a drawdown they didn’t need to take.

So, why is the question of “should I just ride it out,” the same one that every retiree eventually asks? The “just ride it out” premise follows an age-old Wall Street narrative designed to keep you invested in the markets at all times. Why? Because that’s how they make money. The narrative is simple. That advice isn’t wrong for a 35-year-old with three more decades of contributions ahead of him. For someone in retirement, however, it’s a much harder argument to defend. A retiree isn’t adding new capital each month; rather, he is either close to, or is, drawing income out. The following is the more crucial aspect of “time.”

That advice isn’t wrong for a 35-year-old with three more decades of contributions ahead of him. For someone in retirement, however, it’s a much harder argument to defend. A retiree isn’t adding new capital each month; rather, he is either close to, or is, drawing income out. The following is the more crucial aspect of “time.” That reality changes the calculus completely. The reader who emailed me has already figured this out instinctively. Watching a six-figure decline feels different when you’re no longer earning a paycheck to replace it.

That reality changes the calculus completely. The reader who emailed me has already figured this out instinctively. Watching a six-figure decline feels different when you’re no longer earning a paycheck to replace it.

His reaction isn’t weakness; it’s the correct response to a real risk.

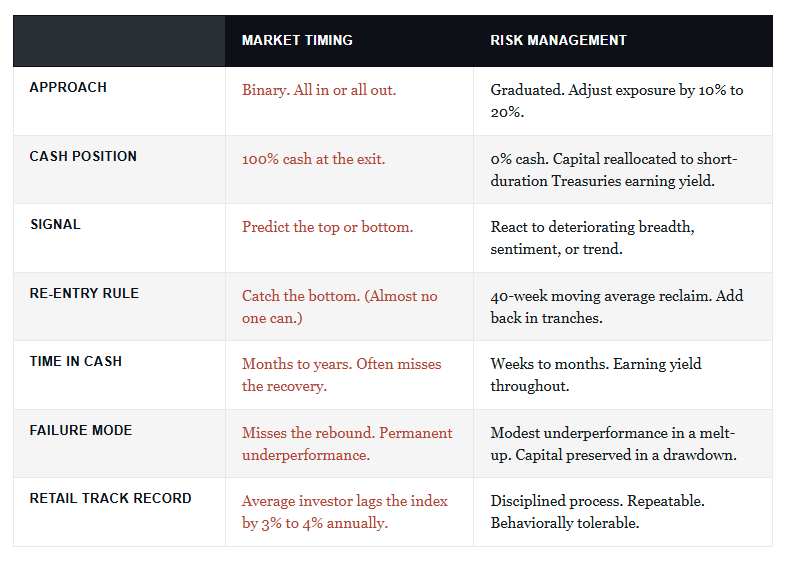

Risk Management Is Not Market Timing

First, we need a real understanding of what “risk” is. As discussed in “Portfolio Risk Management: The Hard Truth.” Here’s the distinction between market timing and risk management that matters, because most retirees don’t realize there’s a difference.

Here’s the distinction between market timing and risk management that matters, because most retirees don’t realize there’s a difference.

Market timing is binary. You sell everything at what you believe is the top, hold cash, wait for what you believe is the bottom, then buy everything back. The strategy fails not because the signals don’t exist, but because the psychology of getting back in is brutal. We’ve seen it in every cycle since 1987. Investors who go to cash almost never redeploy at lower prices. They wait for confirmation, and by the time they feel confirmed, the index is well above where they sold. So they sit. And they miss the recovery. They end up worse off than if they’d done nothing at all.

Risk management is a graduated process, not a switch. When conditions deteriorate, you reduce equity exposure modestly. Maybe 10%. Maybe 20%. Cash isn’t the destination. Staying invested matters because a sharp reversal to the upside shouldn’t leave you stranded on the sidelines. The proceeds go into something that earns yield while you wait, like short-duration Treasuries or a money market currently paying north of 4%. That leaves room to add exposure back when the setup improves.

I went through this distinction in detail in Correction Continues: The Value Of Risk Management. The key insight is that going to zero exposure is just market timing with extra steps. Maintaining some equity exposure while reducing risk produces materially better outcomes than either extreme.

The Math Of Loss For Retirees

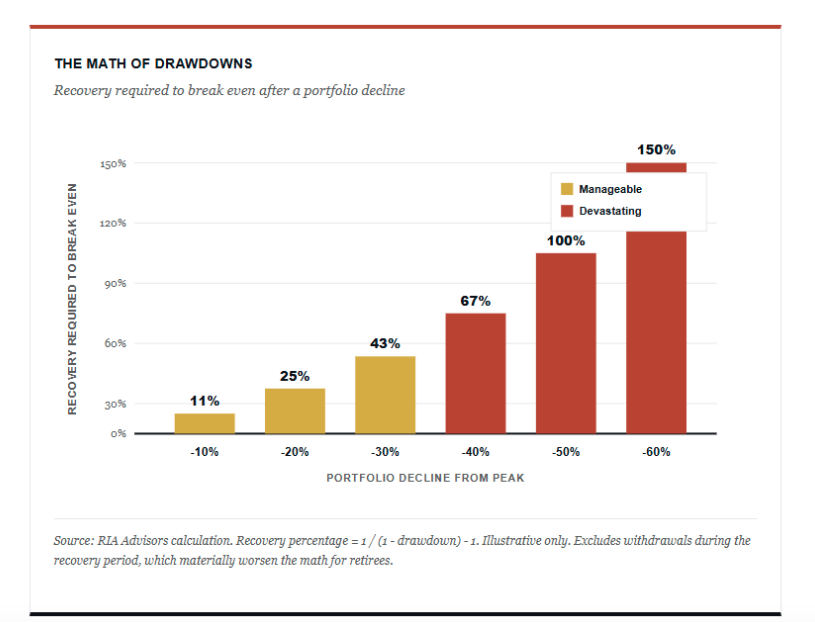

Here’s where the math gets uncomfortable, especially for someone withdrawing income from a portfolio.

- A 10% drawdown requires an 11% rally to break even. Not bad. Manageable.

- A 20% drawdown requires a 25% drawdown.

- Push the loss to 30%, and you need 43%.

- At 50%, the market has to double.

That asymmetry isn’t a statistical quirk. It’s the math of compounding in reverse. The deeper the hole, the steeper the climb. And the climb gets steeper at an accelerating rate as the drawdown grows.

For a retiree, this matters in a way it doesn’t for a younger investor, because the retiree is taking distributions during the climb. Every dollar pulled out during the recovery is a dollar that doesn’t participate in the rebound. The portfolio that drops 30% and then withdraws 4% annually through the recovery period doesn’t actually break even at a 43% rally. It needs significantly more.

I’ve made this point before, and I’ll keep making it. Capital preservation isn’t optional once you’ve stopped earning income. It’s the single most important variable in the equation. We covered the underlying logic in detail in Investing Lesson Of Math Learned The Hard Way, and nothing about that math has changed.

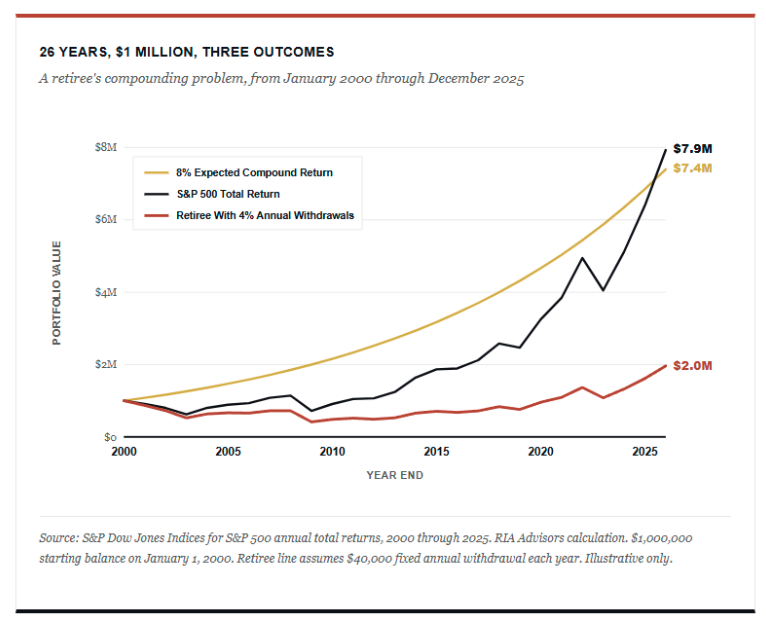

And the math is actually worse than advertised. There’s a piece most retirement plans don’t show you.

Investors are told that markets compound over time. Therefore, just save consistently, hold equities, let compounding work, and you’ll get to your number. The problem is that a market loss breaks that compounding. What actually compounds, year after year, is the required rate of return needed to reach a financial goal. A 10% loss followed by an 11% gain returns the portfolio to even, but not the portfolio objective. Let me explain.:

If you needed a 6% return that year to stay on track, you didn’t just lose 10%, you also lost the 6% you should have earned, and that gap compounds for every remaining year over the horizon. Add a 4% annual withdrawal during the decline, and the math goes from bad to ruinous.

The chart above traces this for a $1 million portfolio invested at the start of 2000. The gold line shows what an 8% annual compound return, the assumption that fills most retirement projections, would have produced. Beside it, the navy line traces what the S&P 500 actually delivered on a total return basis. Below them, the red line shows what a retiree experienced who started drawing $40,000 a year from the same portfolio over the same period.

Notice that the S&P 500 caught up to the 8% expected line over the full 26-year window. From a buy-and-hold perspective, the market roughly delivered on the plan’s promise. From a retiree’s perspective, however, the same period destroyed close to three-quarters of the wealth the plan was supposed to provide. The S&P 500 finished where it was supposed to. The retiree did not. That gap is what disciplined risk management is supposed to protect against.

The “Just Ride It Out” Counterargument

However, let me steel-man the “just stay invested” crowd, because the argument isn’t crazy, it’s just incomplete.

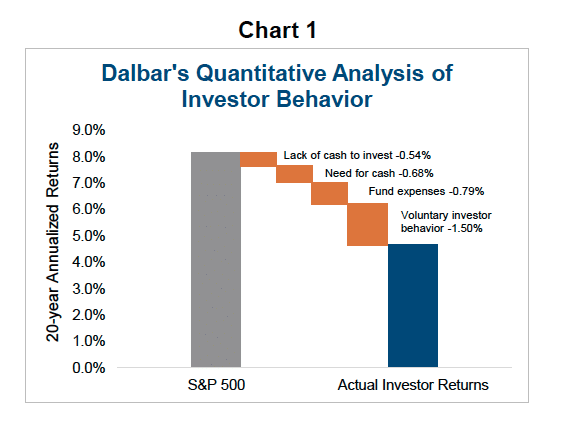

The buy-and-hold camp is right about one thing: the vast majority of people who try to time markets fail badly. The Dalbar QAIB study has shown for years that the average retail equity investor underperforms the S&P 500 by something like three to four percentage points annually, and the gap widens during periods of high volatility because investors panic at exactly the wrong moments. That gap is real, and it’s a strong argument against active management for the average investor.1

However, here is where the argument breaks down. The Dalbar study measures emotional reactions, not disciplined risk reduction. The investors who underperform aren’t the ones who trimmed exposure modestly after a deterioration in market internals. They’re the ones who sold everything in March 2020 after the index was already down 35%, then waited until July 2020 to buy back in. Those are two different behaviors. Lumping them together is how the industry talks retirees into accepting drawdowns they don’t have to accept.

However, here is where the argument breaks down. The Dalbar study measures emotional reactions, not disciplined risk reduction. The investors who underperform aren’t the ones who trimmed exposure modestly after a deterioration in market internals. They’re the ones who sold everything in March 2020 after the index was already down 35%, then waited until July 2020 to buy back in. Those are two different behaviors. Lumping them together is how the industry talks retirees into accepting drawdowns they don’t have to accept.

The other problem with “just ride it out” is that it assumes the investor’s time horizon matches the bear market’s recovery period. For a 30-year-old, that’s a safe assumption. For someone in their 70s taking distributions from the portfolio, it isn’t. The S&P 500 took roughly 13 years to recover its 2000 peak in real terms. That’s longer than many retirees have, and certainly longer than they can afford to wait without depleting capital.

How To Reduce Exposure In Practice

Practically speaking, here’s how a retiree using index funds can apply risk management without falling into the market-timing trap.

- Start with your target allocation. If the financial plan calls for 60% equities, that’s your baseline. You don’t need to overthink it.

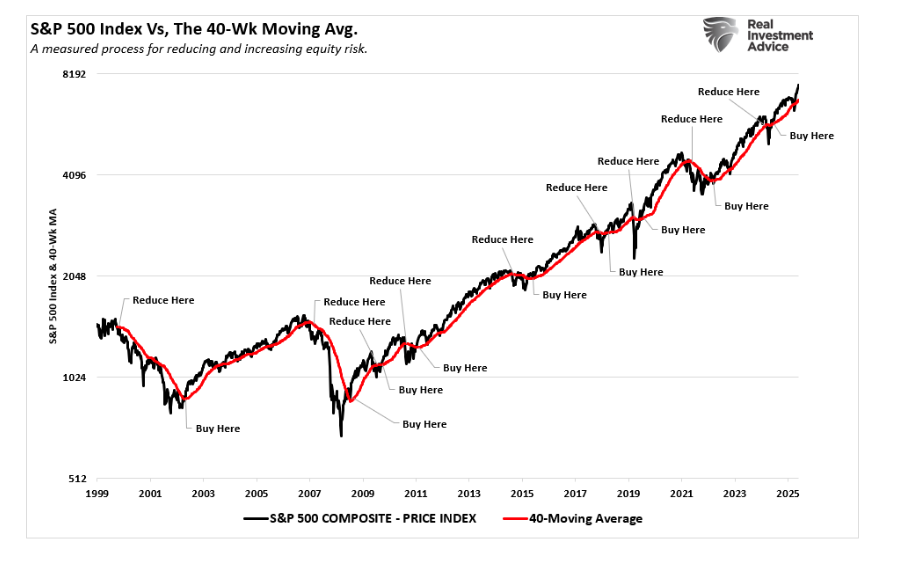

- From there, define the conditions that warrant reduction. Examples include a meaningful violation of the 40-week moving average, a collapse in market breadth, sentiment readings at historical extremes, or yield curve dynamics that historically precede recessions. These aren’t guesses. They’re observable conditions you can monitor without watching financial television every morning.

- When those conditions cluster, trim your target equity allocation by 10% to 20%. A 60% baseline becomes 45% to 50%. The proceeds are invested in short-duration Treasuries or a money market. Sitting in cash earning nothing isn’t the goal. Earning yield while you wait is. Importantly, you’re not trying to predict where the market goes next. You’re acknowledging that the distribution of outcomes has shifted, and you’re sizing your exposure accordingly.

- Most critically, write the rules down before you need them.

The moment to decide on your risk-reduction protocol is not during a 5% selloff with red headlines on every screen. Write the rules in calm conditions, then follow them mechanically when conditions deteriorate. That’s the behavioral discipline I argued for in our 15-Risk Management Rules To Wind The Long-Game.

How To Get Back In Without Catching A Falling Knife

The exit isn’t the hard part. The re-entry is.

The viewer’s instinct in his email was to wait until the market “rises back through the point you sold.” That’s reasonable as a rule of thumb, and better than no rule at all. I’d suggest something even simpler and more mechanical.

- When the S&P 500 reclaims its 40-week moving average from below after a correction, that’s historically a high-probability moment to add exposure back. It won’t be the exact bottom. The market will already have rallied 8% to 12% off the lows by the time the moving average reclaim triggers. That’s the point. You’re not trying to catch the bottom. You’re trying to participate in the recovery while avoiding a false signal.

- Add the exposure back in tranches rather than all at once. If you trimmed 15% off your equity allocation on the way down, add 5% back on the moving average reclaim, another 5% on a successful retest of the moving average from above, and the final 5% when breadth and volume confirm the trend. This isn’t precision timing. It’s graduated participation, and it solves the psychological problem that destroys most attempts at active risk management.

Does this process get you out at the exact top and in at the bottom? No. You will always be late; however, what should be evident is that over time, the process can help you safely navigate market risk.

The reason this works is the same reason most market timers fail. By the time the average investor feels safe enough to redeploy capital, the index is well above the price at which they sold. The 40-week moving average rule forces a decision before that emotional certainty arrives. You add exposure when the rule says to, not when financial television says to.

What This Looks Like Right Now

The reader wrote in at a useful moment in the cycle. We laid out the current case in detail in Market Correction Risk: Why Summer 2026 Looks Risky, and the short version is this. The S&P 500 hit all-time highs in May and has recorded 9 consecutive weeks of gains. This is occurring even as the median stock in the index sits 13% below its 52-week peak, breadth remains weak, and positioning is stretched. Seasonality is the worst window of the year. Historically, the political cycle is the worst year for equities.

None of that guarantees a correction this summer. What it does is shift the distribution of outcomes. The reward for staying maximally aggressive at this point in the cycle is small. A 20% to 30% drawdown for a retiree can be permanent. That’s the kind of asymmetric setup where modest risk reduction earns its keep, even if the correction doesn’t arrive.

The investors who survive long market cycles aren’t the ones who catch every uptick or the ones who worry about “beating some random benchmark index.” They are, however, the ones who refuse to be wiped out when the setup turns against them. Here is the most important lesson to take away from this article. That asymmetry should drive every exposure decision a retiree makes right now.

That asymmetry should drive every exposure decision a retiree makes right now.

So the reader who wrote in is right. He’s been listening. He’s been doing the work. His instinct to reduce exposure modestly in front of an unfavorable setup isn’t panic. It isn’t market timing. It’s risk management, and the difference matters.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All