The dollar holds a central place in global markets due to its role as the world’s reserve currency. Its movements influence cross-asset correlations, shape liquidity conditions, and often offer early indications of shifts in the broader macro regime. In short, it is a critical variable that warrants close attention.

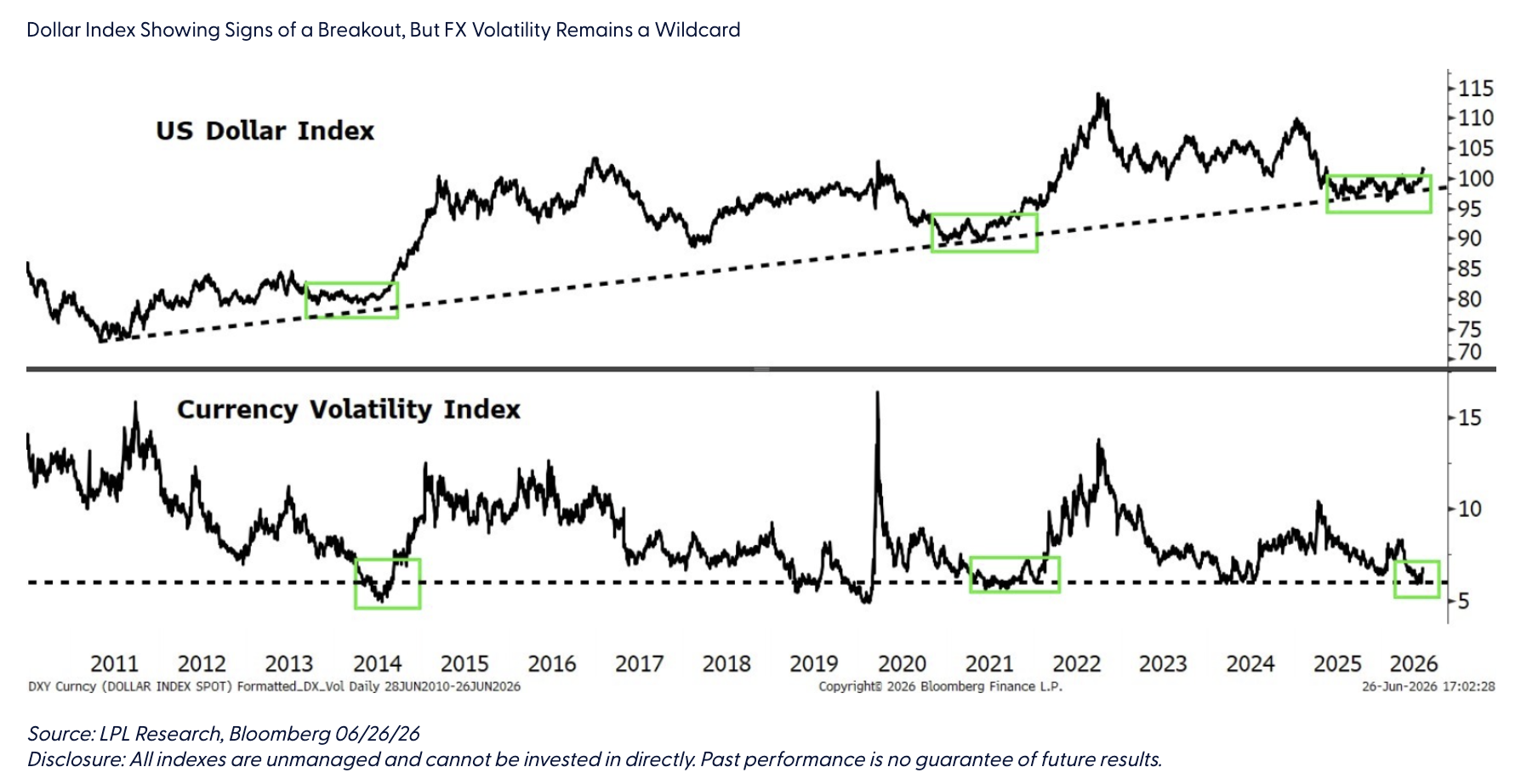

Over the past 11 months, the U.S. Dollar Index (DXY) has traded within a relatively tight five percent range, a notable period of consolidation. More importantly, there are now early signs of a breakout, with price action beginning to push higher and move beyond the confines of the recent range. Equally significant is that throughout the recent period of consolidation, the dollar repeatedly threatened to break the secular uptrend that has been in place since 2011, and despite numerous attempts to move lower, the dollar never really cracked.

From a technical standpoint, this current setup is constructive. Breakouts from extended consolidations often see meaningful follow through, particularly when they emerge from a backdrop of compressed volatility. And as highlighted in the Dollar Index chart, foreign exchange (FX) volatility has been notably subdued recently with several measures of currency volatility reaching near four-year lows. Given the mean reverting nature of volatility, that kind of compression often behaves like a coiled spring, and when it releases, the resulting moves are often both sharp and persistent.

In terms of levels, a sustained move through 103 on the DXY would go a long way toward confirming that a more durable bottom is in place. That would shift the balance of risks higher, and potentially even signal the resumption of the secular dollar uptrend. But a move like that would not occur in isolation. It would carry important cross asset implications. For instance, historical periods of dollar strength have been associated with relative outperformance of U.S. equities versus the rest of the world.

Read more: Could the Dollar Be in Trouble – If So, What Then?

On the fundamental side, the recent firming in the dollar has not occurred without support. The U.S. continues to maintain a meaningful rate advantage relative to other G10 economies. At the same time, the Federal Reserve (Fed) has leaned more hawkish at the margin, while incoming U.S. economic data has continued to show signs of improvement. The combination of relative policy stance and a resilient growth backdrop have helped underpin the recent move higher in the dollar. That said, the policy side is not without risk. While markets continue to price the potential for further Fed tightening, actually delivering additional hikes may prove to be a high bar. The gap between market expectations and realized policy will be something to watch closely. In our view, the key risk to this developing uptrend in the dollar would be a shift in tone from the Fed back toward a more definitive neutral posture, as any softening in policy expectations would likely take some of the support out from under the currency.

On the downside, there are a couple of key levels to note. A move back below the 200-day moving average, which sits near 99.00, would raise concerns that the recent strength is just another false start of many over the past year. A deeper decline through 95.50 would reopen the case for a broader secular shift lower. For now, the weight of the evidence suggests the path of least resistance for the dollar is higher. If that view is correct, the implications will extend well beyond FX and into the broader macro landscape.

Kristian Kerr drives the broad, house investment strategy for LPL Financial Research. His career includes over 25 years of industry experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1133108

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

More Portfolio Building Topics >