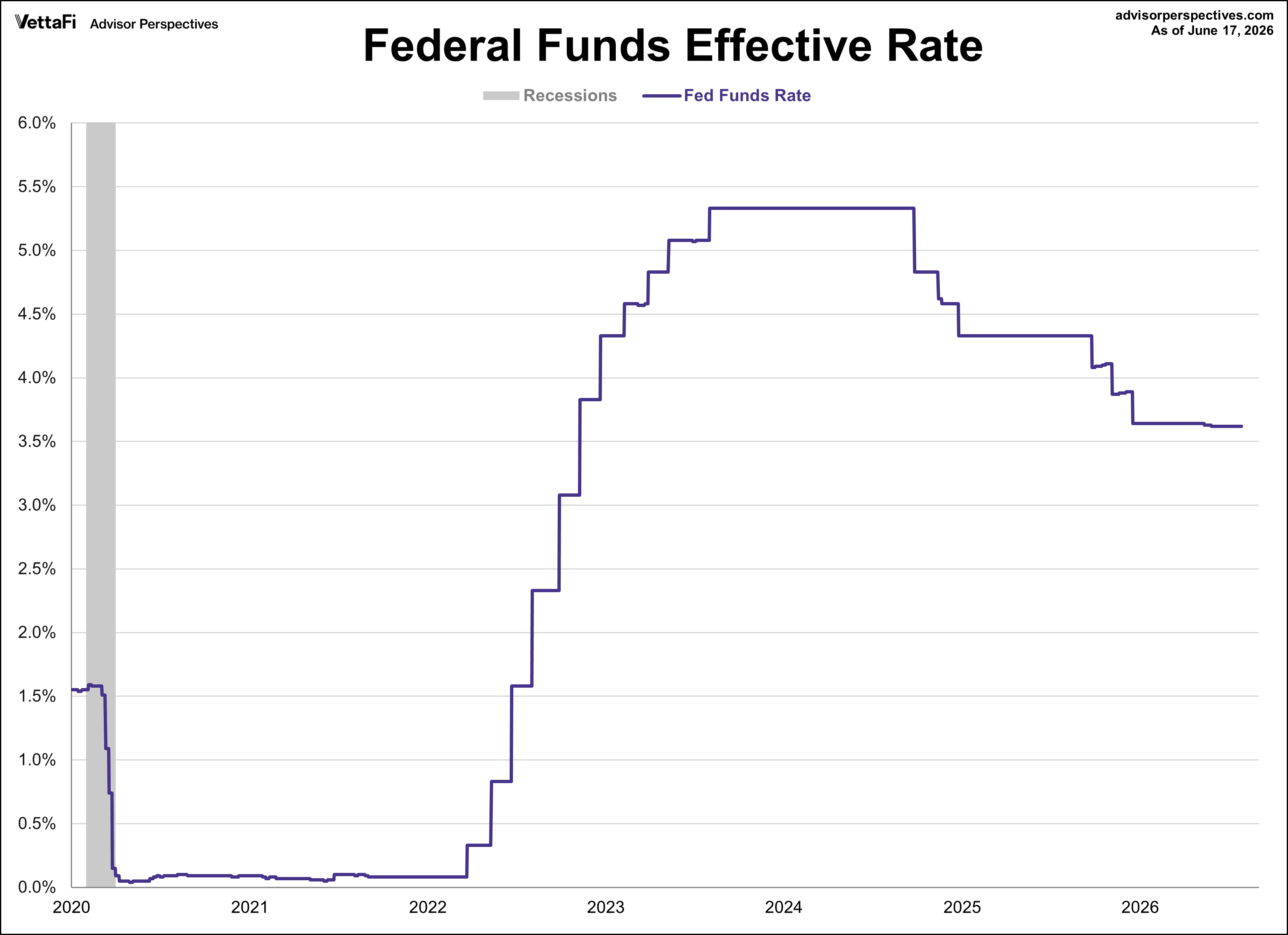

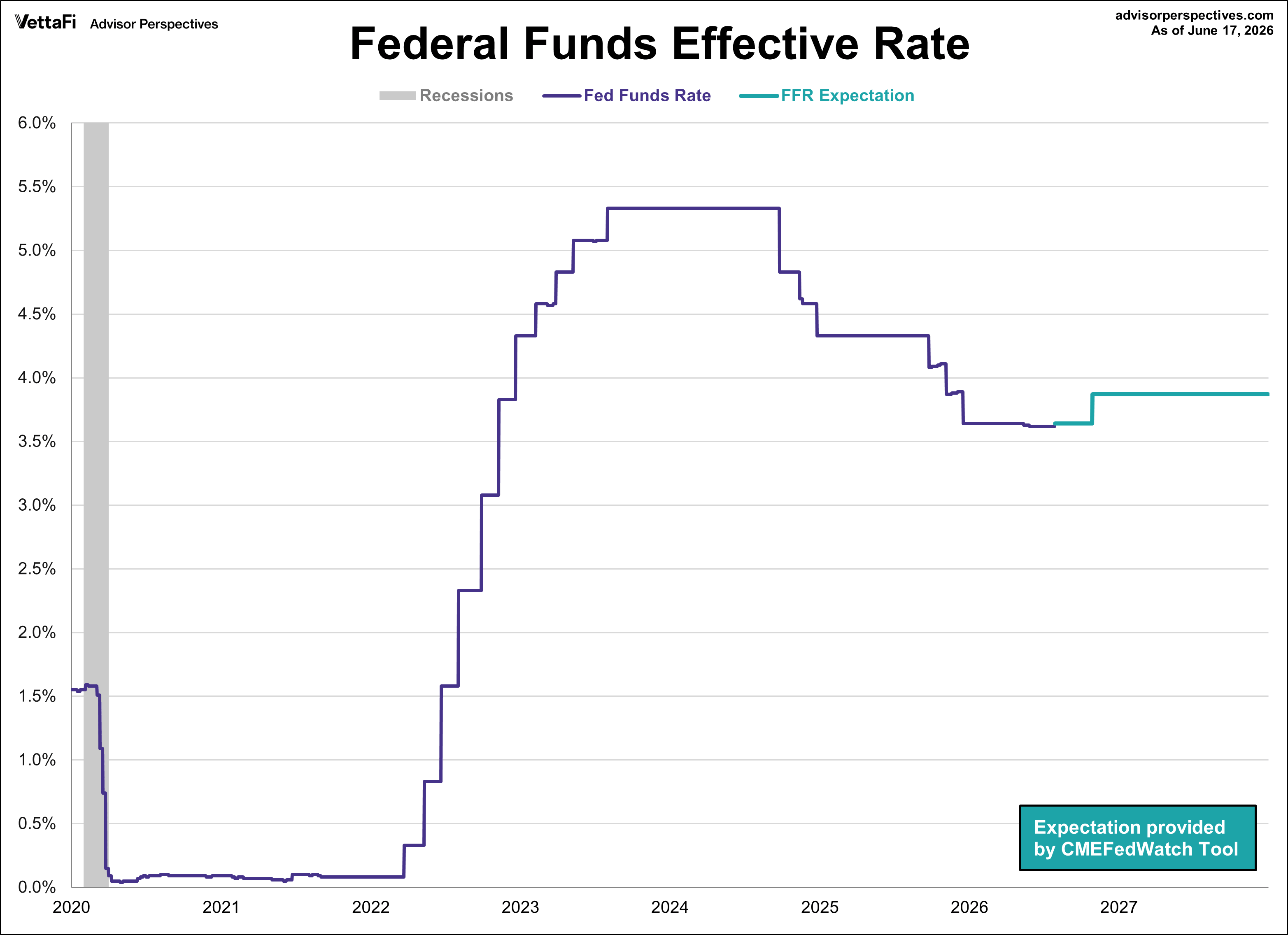

The Federal Reserve concluded its fourth meeting of the year by holding the federal funds rate (FFR) steady in the 3.50%-3.75% range. The decision, which markets had fully priced in, keeps the benchmark rate at its lowest level since November 2022 for the fourth meeting in a row.

Key Takeaways

-

The FOMC voted 12–0 to hold the federal funds rate steady at 3.50%–3.75% for the fourth consecutive meeting.

-

Markets currently price in one 25-basis-point interest rate hike by October 2026, with no further movement through 2027.

- Fed officials raised year-end rate projections to between 3.6% and 4.1%.

Here is a statement from the meeting:

The Federal Open Market Committee approved the following statement for release by a 12 – 0 vote:

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve's dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

Background on the Federal Funds Rate (FFR)

The federal funds rate is the interest rate that banks charge each other to borrow money overnight. It is set by the Federal Open Market Committee (FOMC), a committee within the Federal Reserve, which meets eight times a year. It is a primary tool used by the Federal Reserve to implement monetary policy and is a key driver of economic activity.

While it directly affects short-term borrowing between banks, the effects of the FFR can be felt across a variety of entities. For consumers, changes in the FFR influence mortgage rates, credit card interest, auto loans, and saving yields. For businesses it affects borrowing costs and investment decisions. Additionally, financial markets also react to rate changes, with shifts in bond yields and equity performance.

The FOMC adjusts interest rates based on key economic indicators focusing on inflation, employment, economic growth, and income. The Fed has a dual mandate of price stability and maximum employment.

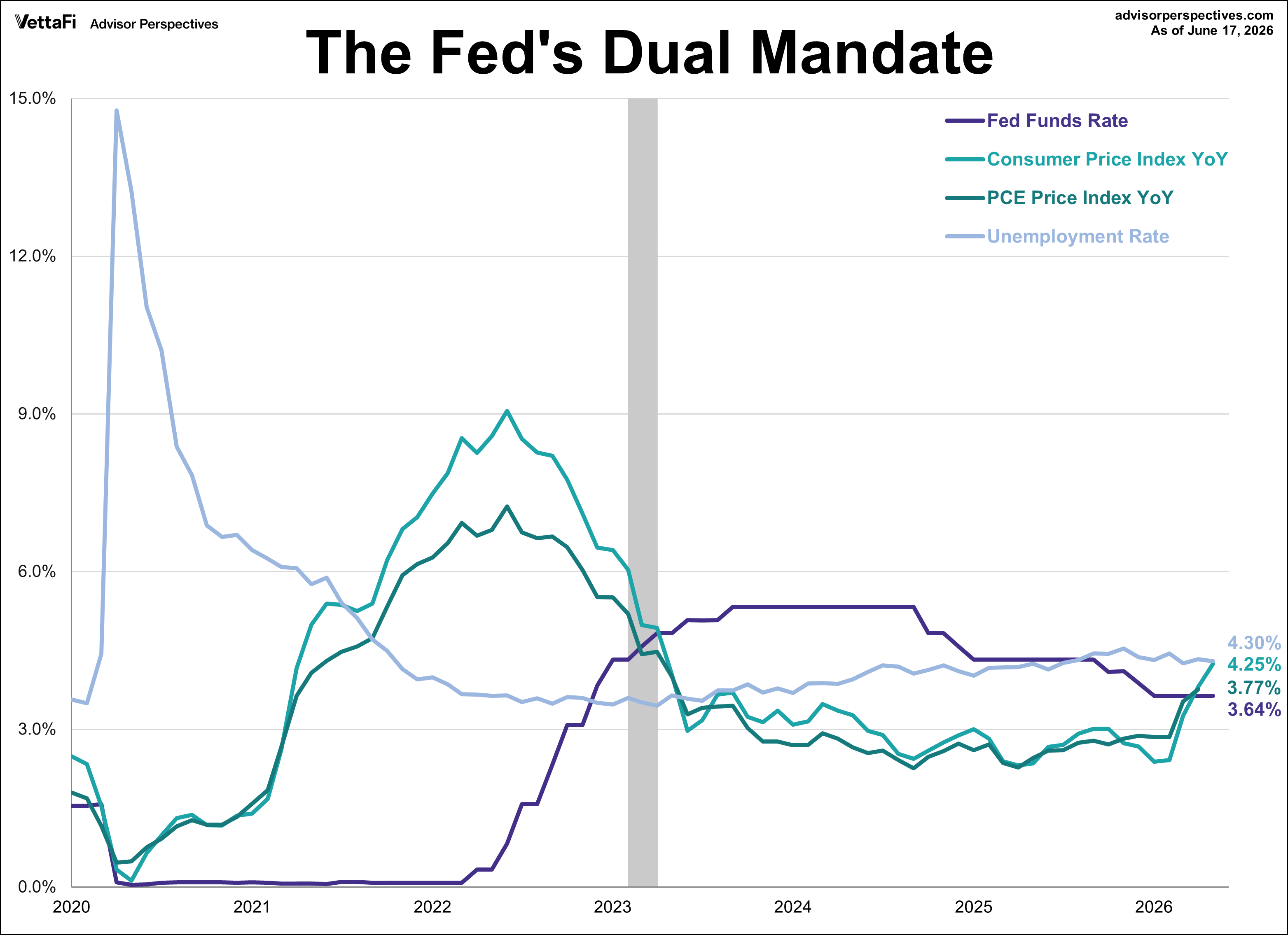

It's easy to see in the chart above how the FOMC's comments from their press release are ringing true. The unemployment rate has moved between 4.3%-4.5% over the past eleven months. Meanwhile, inflation has proven sticky over the past few years, with the most recent figures for both Consumer Price Index (CPI) and PCE Price Index still well above the Fed's 2% target level.

Historical Trends of the Federal Funds Rate (FFR)

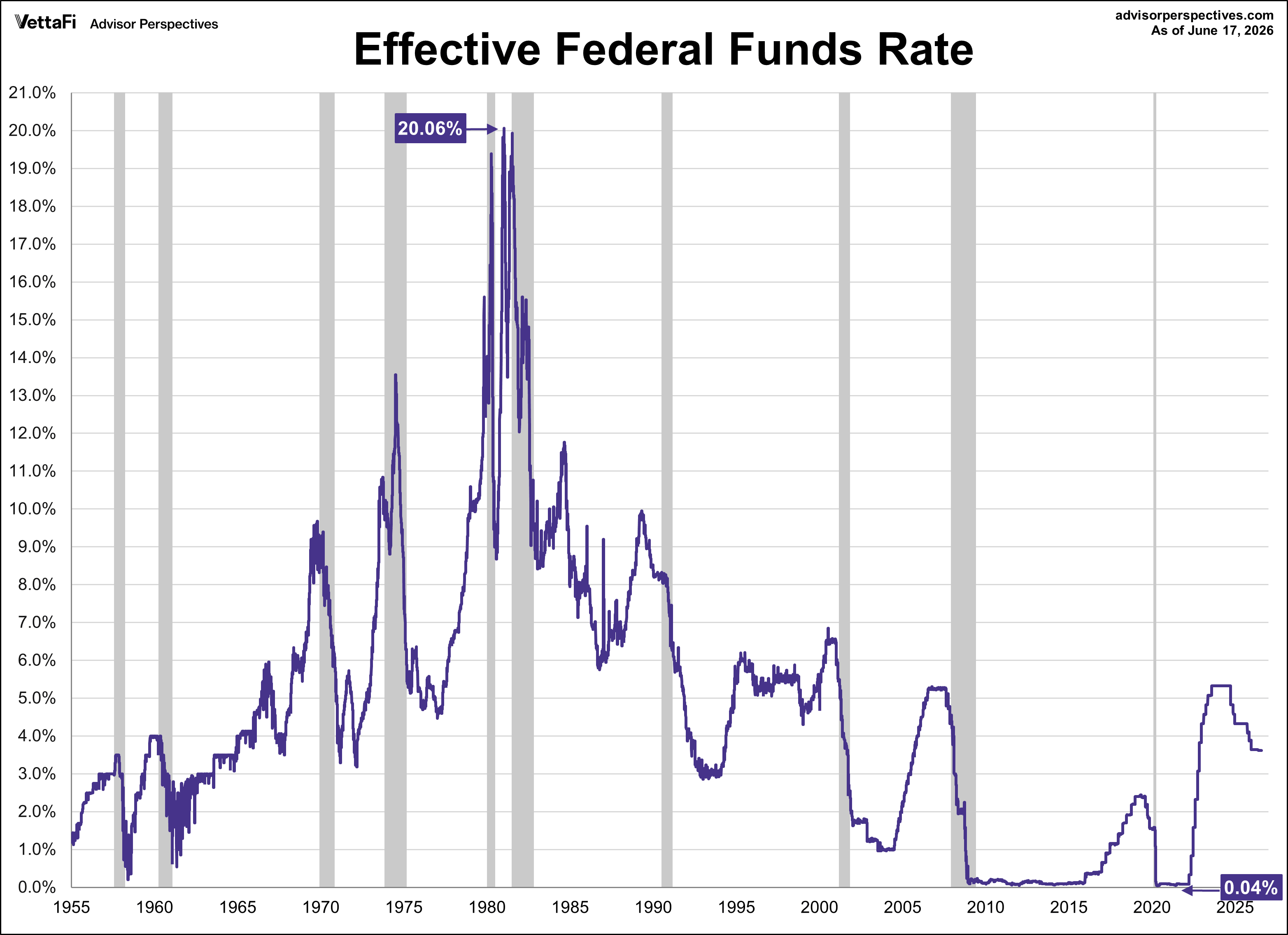

The stagflation crisis of the late 1970s and early 1980s demanded drastic measures. Under the leadership of Paul Volcker, the Federal Reserve pushed the FFR to a historic high of 20.06% in January 1981. This aggressive tightening of monetary policy was instrumental in curbing runaway inflation, albeit at the cost of a significant economic slowdown.

In stark contrast, the FFR was driven to near-zero levels in the aftermath of the 2008 financial crisis and again during the economic turmoil of the 2020 pandemic. Specifically, the FFR reached a record low of approximately 0.04% in May 2020. These periods of ultra-low interest rates aimed to stimulate borrowing, investment, and economic recovery.

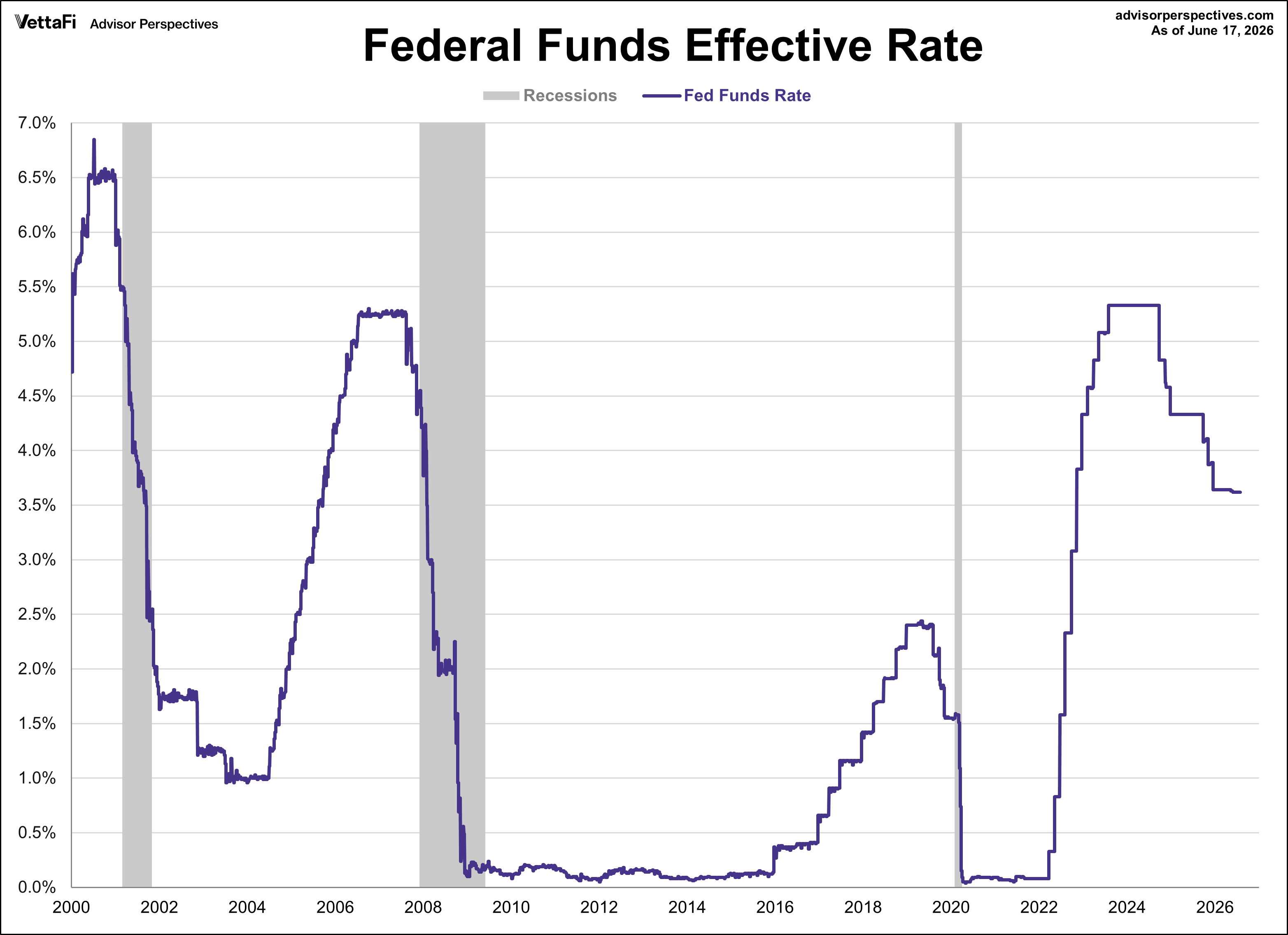

The federal funds rate has undergone significant fluctuations in the past two decades. Following the 2008 financial crisis, the Fed kept rates near zero until 2016. A gradual tightening cycle brought the rate to 2.25%-2.50% by 2019, but the onset of the COVID-19 pandemic led to a return to near-zero rates in 2020.

In response to soaring inflation—the highest in four decades—the Fed aggressively raised rates from March 2022 to August 2023, reaching a peak of 5.25%-5.50%, the highest level since early 2001. The central bank then shifted course in September 2024, implementing three consecutive rate cuts to bring the FFR to the range of 4.25%-4.50%. The Fed went on a similar path in 2025, holding rates steady until September where they then issued three consecutive cuts to bring the FFR to its current range of 3.50%-3.75%.

Federal Funds Rate: What's Next?

The CMEFedWatch Tool estimates the probability of future interest rate moves. The tool is updated in real-time in response to economic data releases, Fed statements, and market movements. The chart below shows the tool’s predictions through the end of 2027. (Note: the chart below is at the time of writing and expectations may have shifted since publication.)

The market is currently pricing in one 25 basis point hike by October 2026 with no further movement through 2027.

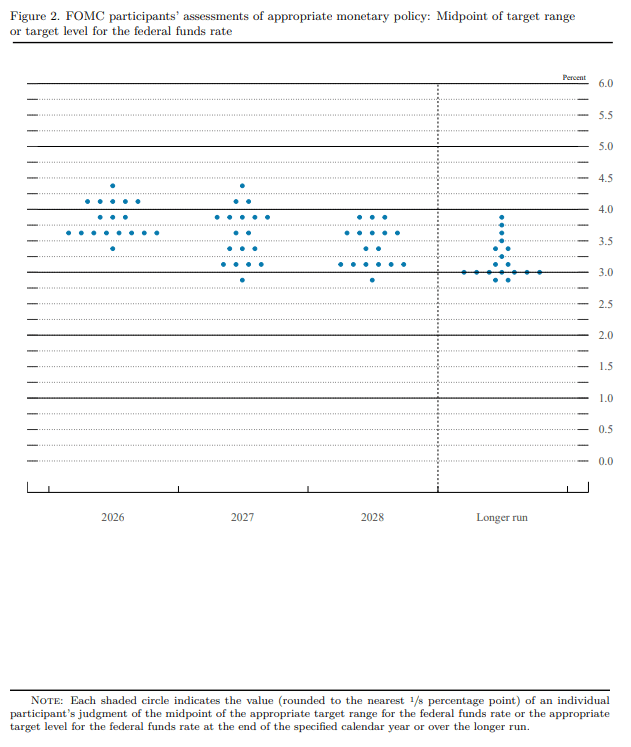

Once a quarter the Fed releases their "dot plot" to reveal each FOMC member's individual projection for the target level of the federal funds rate (FFR) at the end of the current year, at the end of the next two years, and in the "longer run". The latest "dot plot" from June 2026 shows a committee that expects to keep interest rates higher for longer than previously thought. For the end of 2026, most officials now expect the benchmark interest rate to sit between 3.6% and 4.1% (up from their previous estimate of 3.25% to 3.75%). While officials still expect rates to drift down slightly in 2027 and 2028, they are predicting a much slower, more cautious descent. Despite this near-term upward shift, the "longer run" anchor remains remarkably unified, with a heavy concentration of participants pinning the neutral rate exactly at 3.0% and reinforcing the collective belief that the era of ultra-low rates is behind us.

The Fed’s next meeting is scheduled for July 28-29th with the next dot plot released on September 16th.

Explore the relationship between the Fed Funds Rate and the 10-year Treasury yield in the video below.