Markets weathered turmoil in the first half, helped by solid earnings with signs of broadening beyond a few AI beneficiaries. If the war in Iran eases, oil prices could normalize, reducing inflation pressure. Still, growth, inflation and policy risks may be underestimated.

The multi-asset playing field presents income investors with broad opportunities across asset classes. But investors that rely only on traditional stock dividends and bond interest may be missing out on other attractive income sources.

A healthy mix of income and growth potential may yield a more effective equity allocation.

The playing field presents broad opportunities for income investors today, with income and growth potential across asset classes. But an effective defense is also critical in capturing that potential. When it comes to the tools of the trade, we think broader is better.

Income investors face a promising landscape today. But we think income investing should be more than simply combining the highest yielders in each asset class, which could create unintended risks. In our view, an efficient multi-asset approach can help find the right balance between income, growth and diversification.

After a turbulent start to 2025 defined by US policy shocks, attention shifted to AI optimism and corporate fundamentals, with earnings and capex intentions often eclipsing traditional data releases. Despite these twists, returns were solid across asset classes.

We think today’s market landscape calls for a different mix in multi-asset income strategies.

For multi-asset income investors, adapting portfolios for equity defense, credit potential and duration exposure should be on the docket for 2024.

An improved income outlook for multi-asset investors, including higher yields, sharply contrasts with cloudy conditions at 2023’s start.

We think dividend-income strategies can be effective across multiple environments, provided that they’re designed to tap into a wider opportunity set beyond traditional dividend payers alone.

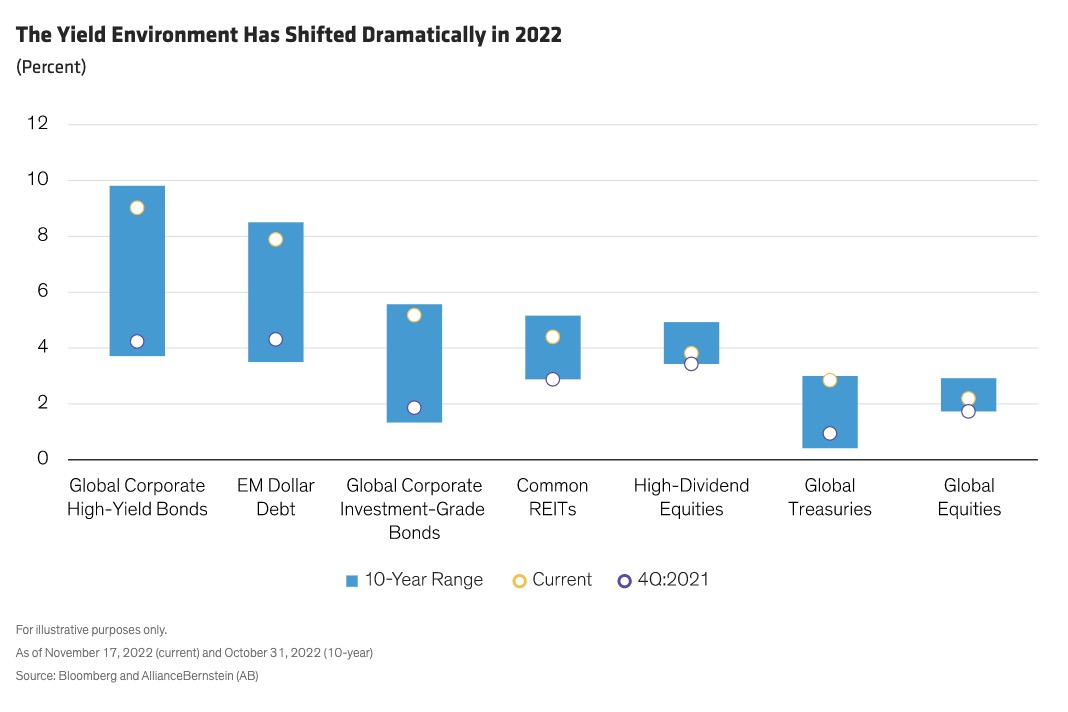

In one of the most challenging years for markets, 2022 brought persistently high inflation, aggressive central bank tightening and heightened geopolitical risks, leaving investors with few places to hide.

Global indicators continue to signal a sharp business recovery from last year’s COVID-19 pandemic lows. While inflation expectations are increasing as a result, business improvements offer multi-asset investors good reasons to remain tilted to equities for the next stage of the recovery.

Having strongly underperformed the wider stock market in 2020, high-dividend stocks have shown early signs of a rebound in recent weeks.

Higher-income assets underperformed in the second-quarter rebound. But that also means there’s pent-up potential in income-generating assets that may begin to show in later stages of the recovery.

The last decade produced great performance across most asset classes. But in the 2020s, we expect investment market returns will be lower and risk harder to manage. Looking forward, a disciplined multi-asset approach will be especially valuable to identify opportunities and help mitigate setbacks.

With the global economy moving into its late-cycle stages, we think it’s a good time to bolster portfolio inflation protection by embracing several recently unloved investments—including natural resources and commodities.

There are a lot of suggestions these days about where to get extra income, but less discussion about the cost attached to it. A diversified multi-asset approach can help—and provide additional growth potential. But how it’s designed matters.

As the new year begins to unfold, the environment for risk assets is still benign: the global economy is strong, monetary policy is accommodative, and volatility is low and steady. At this point, we don’t see excesses developing that could change that.