The bonds sold by hyperscalers to fuel their artificial intelligence ambitions have become a drag on investor portfolios from London to Tokyo.

Exchange-traded funds can be the source of liquidity that retail investors need after ramping up exposure to private assets, BlackRock Inc. executives wrote in a report.

Credit investors are unwinding long positions worth tens of billions of dollars and jumping into hedging trades.

European real estate companies have been buying back junior bonds like never before, seeking to get their balance sheets in order after a tumultuous few years.

Investors are increasingly viewing bonds from large corporations like Microsoft and Siemens as safer than the sovereign debt of their home governments, a conclusion driven by a sharp contrast in fiscal management.

Bond investors are accepting the smallest compensation in years in return for taking default risk, as a potent combination of economic optimism and too much cash chasing too few securities skews costs.

Credit investors squeezed by the tightest spreads in almost 20 years are opting for bare-bones strategies, creating a boom for Europe’s fixed-maturity funds.

Credit risk fell in reaction to Donald Trump’s US presidential win, even though his presidency may be marred by tariffs and possible trade wars.

Credit bulls are pointing at a set of metrics to show that high-grade bonds have rarely been this cheap, burnishing the appeal of corporate debt at a time when it’s offering little upside over government securities.

Less than a year ago, investors were gaming out what would happen when billions of dollars of bonds reached maturity dates, leaving borrowers potentially crushed by costly refinancings. Now, those fears are fizzling away, with companies rushing to sell debt to a buoyant market.

Cash may still be king for the moment, but after more than $1 trillion flowed into money-market funds last year as short-term rates rose, investors are trying to figure out where it goes next.

Nomura Asset Management’s Richard Hodges began the year by buying credit default swaps, worried that rate-cut bets were becoming too aggressive. He reduced the hedge when the cost of protection increased, and now stands ready to dip in again.

Global corporate bond returns just hit their highest level this year on bets that the inflation crisis is coming to an end. Some investors say this may be as good as it gets, with dangers lurking in credit markets for the second half.

Investors are bailing on preferred shares at a historic clip because of the growing concern about the health of US regional banks.

Junior debt issued by banks is normally one of the riskiest types of fixed-income in the US and Europe. It’s typically not backed by collateral and in the event of a crisis it only gets paid back after other bonds.

January’s optimism about the bond market seems like a long time ago.

Demand for Europe’s debt sales has topped half a trillion euros already this year as investors seek to put money to work in bonds offering some of the highest yields in years.

Global bonds rebounded in November, adding a record $2.8 trillion in market value, as investors bet that central banks are getting a grip on inflation. But how long the party lasts is another matter.

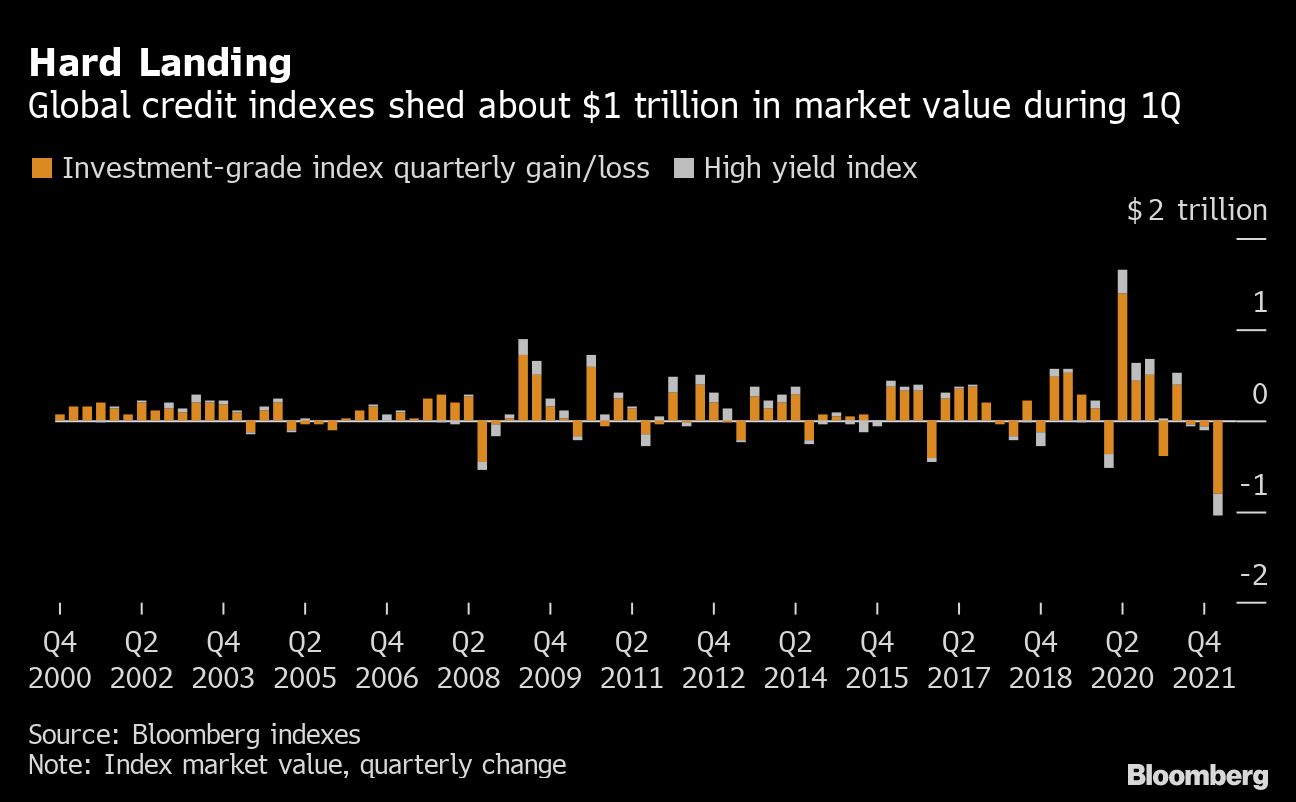

Investors in corporate bonds are bracing for more trouble after getting hammered by rampant inflation and rising yields in the first quarter.

Borrowing costs are soaring across global credit markets as investors prepare for the end of an era of loose monetary policy.