BDCs: Not All Yield Is Created Equal

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Gated funds, collateral fraud, and auto-sector defaults are giving investors in private credit funds and their stock-market equivalents — business development companies (BDCs) — a headache.

We have discussed the recent woes of private credit funds (HERE, HERE, and HERE), yet we haven't addressed BDCs. The similarities and differences between private credit funds and BDCs are important. For instance, take the bad press about the widespread gating of private credit funds. While BDCs own similar assets, they trade on a stock exchange. Thus, investors who want to sell don’t have to rely on a fund manager's whim; they can sell their shares in seconds.

The poor sentiment toward private credit funds has dragged down many high-quality BDCs, as well as weaker ones. The chaos and bad press surrounding private credit funds are not reasons to avoid BDCs. In fact, we think it’s a reason to consider them.

What Is a BDC?

Congress passed the Small Business Investment Incentive Act of 1980 to provide capital to small and midsized private businesses that lacked access to public credit and equity markets. Per Congressional records, BDCs encourage the mobilization of capital for new, small and medium-sized, and independent businesses.

BDCs, like private credit funds, are professionally managed portfolios of private loans, but unlike private credit funds, they trade on a stock exchange. Some BDCs also hold equity in the companies they lend to.

The BDC structure is similar to that of real estate investment trusts (REITs) in that BDCs must distribute at least 90% of their taxable income to shareholders. This partially explains why they tend to have above-average dividend yields.

Liquidity

As we led this article, liquidity is a key difference between a BDC and a private credit fund. The headlines about private credit fund investors being unable to redeem their investments stem from a liquidity mismatch. The funds made loans for three or more years, but promised investors they could get their money back quarterly. When redemption requests exceed the fund's liquidity, the fund must limit — or gate — redemptions. BDC investors don't face that problem. Shares are never redeemed, just traded from one investor to another.

However, there is a cost for liquidity. BDC investors face price volatility. Because the stock price trades daily while the underlying portfolio’s value (NAV) is released only quarterly, BDCs' stock prices are highly sensitive to positive or negative sentiment and NAV forecasts.

Private credit fund investors only see their price (NAV) change quarterly; the volatility is hidden, not absent. BDC investors see volatility in real time, which is uncomfortable, but it also creates opportunities.

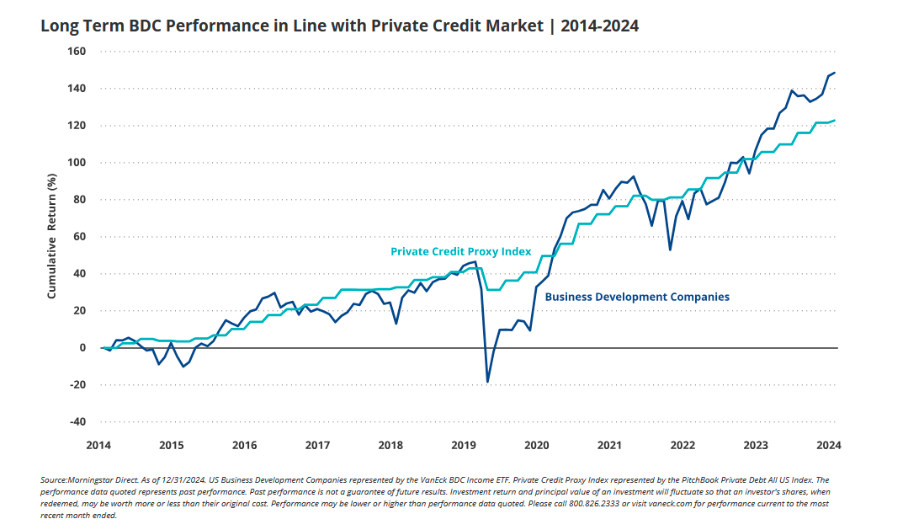

The graph below, courtesy of VanEck, shows that the return profiles of BDCs and private credit funds are similar, although BDCs exhibit more volatility. Again, the volatility you don’t see in private credit can be more problematic than the volatility you see with BDCs.

Net Asset Value (NAV)

When evaluating a BDC, the most important consideration is the NAV per share. NAV/share represents the estimated fair value of all loans and equity investments in the portfolio, minus liabilities, divided by the number of shares outstanding. It's like the price-to-book ratio valuation.

When a BDC trades at a discount to its NAV, the market is effectively worried about one of two things:

- It doesn't trust the stated NAV; or

- It believes the portfolio’s value has deteriorated from the last reported NAV.

When a BDC trades at a premium to NAV, it is because investors think the real NAV has appreciated since it was last reported. Or investors are paying up for something they believe is worth more than the sum of its parts. This includes a manager with a proven track record of consistent NAV growth, conservative underwriting standards, cost advantages, and structural advantages that competitors lack.

Currently, the private credit selloff has pushed many BDCs to meaningful discounts. Some are warranted if their NAVs have fallen; others are not. Determining which requires understanding the contents of the BDC portfolios and how they are managed.

Internal or External Management

An important differentiator of BDCs is whether the portfolio manager is internal or external. The vast majority of BDCs are externally managed. In these cases, an outside firm manages the portfolio and charges fees to the funds.

Typically, this includes an annual management fee of around 1.50% of total assets, plus an incentive bonus of roughly 15–20% of income above a hurdle rate. Those fees are paid before an investor receives a dime of dividends.

The payment structure creates a so-called principal-agent problem. Shareholders want the manager to maximize risk-adjusted returns. However, the manager is paid the most when they maximize assets under management. Those two objectives are not the same.

Managers are incentivized to deploy capital even when the best opportunities aren't available. They can compromise on credit quality, reach for yield in riskier loans, and leverage the portfolio to make marginal loans look attractive.

Internally managed BDCs avoid fees and the principal-agent problem. Internal portfolio managers' interests closely align with those of shareholders because they are the same entity. The cost advantage of not paying fees compounds over time, and the incentive structure rewards making good loans rather than making more loans.

Internally managed BDCs are rare, which is one reason the best-performing ones trade at a premium to their NAV.

Portfolio Composition

When evaluating a BDC, the industry breakdown of its loan book is an important assessment. That is especially true today, when estimates suggest that BDCs and private credit funds have made over a quarter of their loans to software companies.

Recurring-revenue software-as-a-service (SaaS) models were among the favorites of direct lenders when interest rates were low. Those companies with strong income statements are now being squeezed by higher borrowing costs and AI disruption narratives that have called business models into question. When software valuations fall, the collateral underpinning those loans shrinks.

BDCs that lend to industries such as construction, healthcare, food services, and manufacturing carry materially less of the specific risk that is weighing heavily on software companies today.

Capital Structure

Beyond industry exposure, investors should understand capital structure positioning. BDCs make first-lien and subordinated loans. First-lien debt is secured by assets and paid to first-lien holders before other creditors in the event of a default. Second-lien and subordinated debt are paid after all first-lien obligations have been met.

In a weakening credit environment, the position in the capital structure makes a huge difference in how much principal is returned.

PIK Income

One more consideration is payment-in-kind (PIK) income as a percentage of total income. This structure allows a borrower who can't pay cash interest to issue more debt to cover the shortfall. A rising PIK-to-total income ratio is an early warning sign that a BDC’s borrowers are struggling.

Leverage and Dividend Coverage

BDCs are permitted to leverage up to 2:1 debt-to-equity. Most are managed at a 1:1 to 1.5:1 ratio. Higher leverage increases both income and losses. Leverage makes the BDC look more attractive in calm markets and riskier when credit conditions tighten.

Many investors focus on the dividend yields but not the dividend coverage. The coverage, or how much they earn relative to the dividend, is critical to assessing the probability that the BDC can make current dividend payments going forward. A coverage ratio above 100% means the BDC earns more than it distributes. Below 100% indicates the shortfall is being funded by the return of capital, meaning investors are gradually receiving their own money back.

Analyzing 2 BDCs

To further your knowledge of BDCs, we thought it would be helpful to conduct a quick analysis of two BDCs and illustrate some of the factors we look at in BDC investments. In this example, we compare internally and externally managed BDCs. As a disclaimer, our clients own both BDCs discussed below.

Blackstone Secured Lending Fund (BXSL)

Per Blackstone: Launched in 2018, BXSL is a business development company focused on first-lien senior secured opportunities that offer structural protection. As part of Blackstone Credit & Insurance, BXSL benefits from the scale, deep relationships, market insights, and operational expertise of one of the world’s leading credit platforms.

Main Street Capital (MAIN)

Per Main ST Capital Corporation: Main Street is a principal investment firm that primarily provides customized long-term debt and equity capital solutions to lower-middle-market companies and debt capital to private companies owned by or in the process of being acquired by a private equity fund. Main Street's portfolio investments are typically made to support management buyouts, recapitalizations, growth financings, refinancings, and acquisitions of companies that operate in diverse industry sectors.

The following table shares a few of the factors we use to assess BDCs.

- NAV: BXSL trades at a discount while MAIN trades at a significant premium. That largely explains the difference in dividend yields between the two.

- Net interest income (NII): Both stocks should be able to sufficiently maintain their dividends for the time being.

- Non-accrual: This measures the percentage of their loan balances where borrowers have stopped making interest or principal payments, typically for 90 days or more. Both BDCs have extremely low non-accrual rates.

- Net debt/equity: BSXL has a ratio of 1.22x, implying that the fund is funding its loans with $1.22 of debt for every $1.00 of equity. This equates to a capital structure that is 55% debt and 45% equity. Conversely, MAIN uses less leverage, with a capital structure of 47% debt and 53% equity.

- First lien and software exposure: Both help us measure the credit quality of the underlying loans.

BXSL has slightly better credit quality but uses external management. MAIN has a great track record and internal management, but a lower yield due to its high premium to its NAV.

Summary

BDCs are not private credit funds. That distinction is easy to overlook when headlines lump the two together. Yet that is what makes BDCs an interesting investment option.

Private credit fund investors are learning that promised liquidity is not the same as actual liquidity. Unlike private credit fund investors, BDC investors know what their investment is worth, or at least what the market thinks it's worth.

Negative sentiment toward private credit has pushed many BDCs to discounts that don't fully reflect the quality of the underlying portfolios. However, not every BDC that is trading at a discount to NAV is an opportunity. Some are cheap for good reasons, such as heavy software exposure, external managers with misaligned incentives, rising PIK ratios, thin dividend coverage, and high leverage. Other BDCs have been caught in the same downdraft despite strong credit quality, conservative leverage, and disciplined underwriting.

Read more by Michael Lebowitz:

- GFC 2.0 or False Alarm: What Private Credit Is and Isn’t

- Will Private Credit Cause the Next GFC?

- The Apple AI Strategy: Discipline Over Hype

- Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All