Gold Bugs' Faulty Thesis: M2 & Inflation

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Gold bugs often claim that when more dollars are in circulation, each dollar buys less; prices rise, and gold, as a store of value, helps protect purchasing power from that decline. As a result, they believe that a rising money supply, in and of itself, is inherently inflationary.

The problem with the gold bugs’ thesis is twofold. First, it lacks critical context. Second, it fails to consider another key factor driving inflation: the velocity of money.

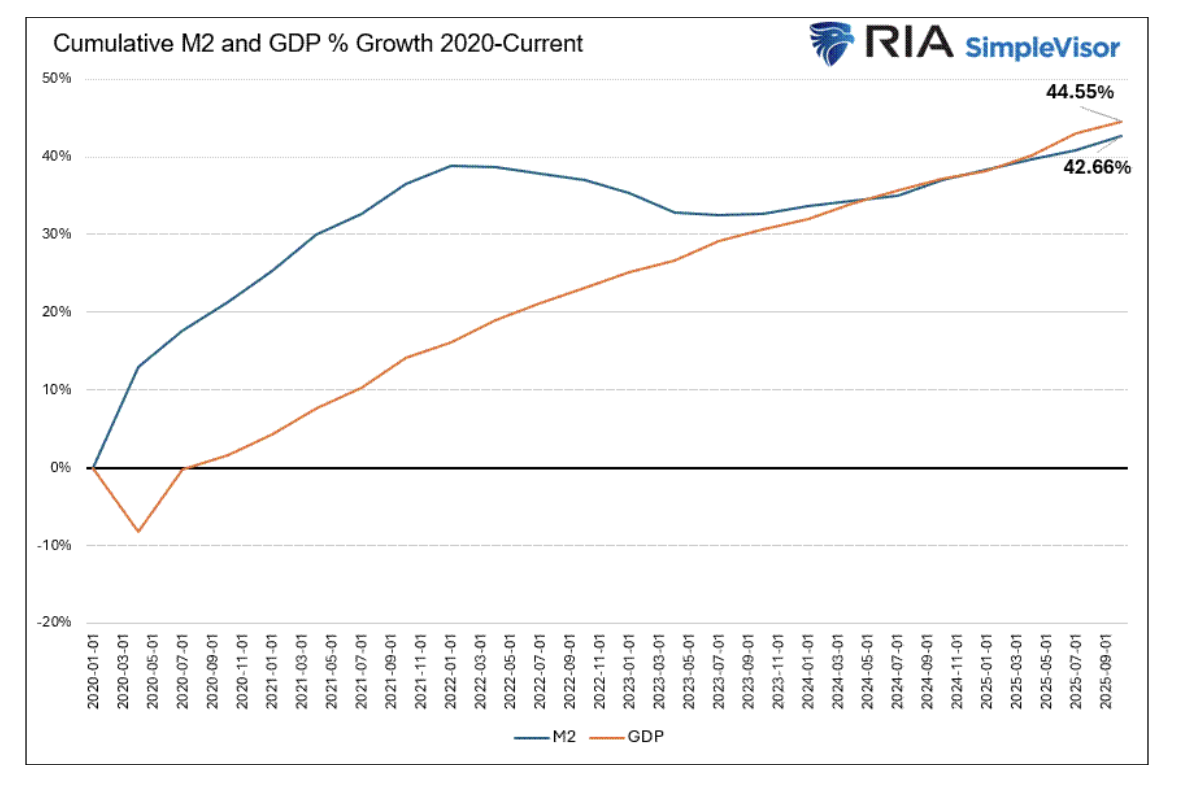

A recent note from Michael Oliver of Momentum Structural Analysis drove us to revisit this topic. Oliver explained that the money supply (M2) has grown 45% since 2020. As a result, cash is eroding in real value "year by bloody year," and gold remains the essential alternative.

It is a compelling narrative. But as we will show, the relationship between money supply growth and inflation is far more nuanced than many gold bugs suggest. Furthermore, having the proper context for M2 growth is imperative.

To be fair, Oliver is not a gold bug solely because of M2 growth. He currently has other rationales as follows:

- Long-term debasement of fiat currencies by central banks;

- Technical analysis;

- Loss of confidence in central bank credibility;

- Geopolitical instability driving safe haven demand; and

-

Government fiscal deficits requiring ongoing monetary financing.

Context Matters

Just quoting M2 growth is worthless without context. To better explain what we mean by that statement, we share our thoughts from a recent commentary:

If we assume inflation is the basis on which to buy or sell gold, then what matters most is the change in the money supply in relation to the change in the economy. As we share below, the money supply grew much quicker than the economy in 2020 and 2021. But since then, it has grown considerably slower. Over the six years Oliver highlights, GDP growth has slightly outpaced the M2 money supply.

If we assume monetary velocity is constant (we elaborate on velocity further below), then the growth in M2 was inflationary in 2020 and 2021, but if anything, it has become disinflationary or deflationary.

Think of it this way. If an economy produces 10% more goods and services but the money supply only grows 5%, there is more stuff available to buy, but not proportionally more money to buy it with. Sellers must either lower prices to sell their goods or let their unsold inventory grow.

Either way, the price pressure is downward, not upward. Thus, if the reason to hold gold is to protect against inflation, the relative growth of the money supply may have been a valid rationale a few years ago, but it is no longer the case.

Monetary Velocity Also Matters

What if, hypothetically, the government secretly printed a zillion dollars, put it in a vault, and threw away the key? Would the surge in the money supply cause the prices of goods and services to rise precipitously? No, it would have zero impact.

However, if word leaked about the secret zillion-dollar stash, prices could be affected by fear that the money ultimately could be released. The point in this hypothetical case is that price changes are not just about the amount of money outstanding. What matters equally as much is the desire and ability to spend it. In economics, that’s called monetary velocity.

What Is Monetary Velocity?

The St. Louis Fed said:

The velocity of money is the frequency at which one unit of currency is used to purchase domestically- produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity of money is increasing, then more transactions are occurring between individuals in an economy.

Velocity is thus a function of economic activity and the money supply. The money supply could be shrinking, but if economic activity is brisk, velocity could increase, thus putting upward pressure on prices. Conversely, the money supply could be soaring, but if that money is not being spent, the demand for goods and services is weak, and prices could fall.

What Impacts Velocity?

The following bullet points outline key factors that affect velocity.

Positively Correlated — Higher Velocity

- Lower interest rates — lower rates incentivize spending and investing over holding cash

- Consumer and business confidence — optimistic economic outlooks encourage more spending

- Inflation expectations — if people expect prices to rise, they spend sooner rather than later

- Credit availability — easy access to credit amplifies the spending power of each dollar

- Technological innovation — new products and services create new spending opportunities

- Income growth — rising wages boost consumer confidence and can increase the frequency and size of transactions

- Economic expansion — growing economies naturally generate more transactions per dollar

Negatively Correlated — Lower Velocity

- Recessions and economic uncertainty — fear encourages saving over spending

- Deflationary expectations — if prices are expected to fall, consumers delay purchases

- Rising interest rates — money sitting in higher interest rate savings accounts turns over more slowly

- Financial deleveraging — paying down debt removes money from circulation

- Aging demographics — older populations tend to save more and spend less

- Banking system stress — credit contraction reduces the multiplier effect of each dollar

M2 and Core CPI

With a better understanding of velocity, let's revisit the assertion of many gold bugs that M2 and inflation are highly correlated. To quantify the relationship, we do a regression analysis of quarterly M2 and monetary velocity data versus core CPI since 2010.

It’s important to note that we use core CPI rather than CPI because it strips out volatile food and energy prices. The prices of food and energy are influenced by many factors, including geopolitical events and weather. Using core CPI versus CPI improves the statistical relationships we analyzed below.

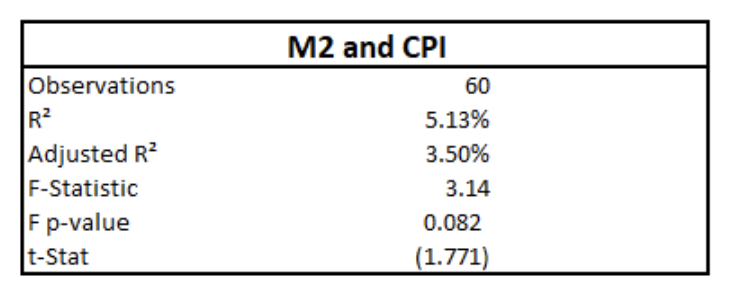

Our first analysis quantifies the relationship between M2 and Core CPI.

The table shows that M2’s money supply growth, on its own, has a very weak and statistically insignificant relationship with core CPI. The R-squared figure means that 5.13% of the variation in core CPI is explained by changes in M2.

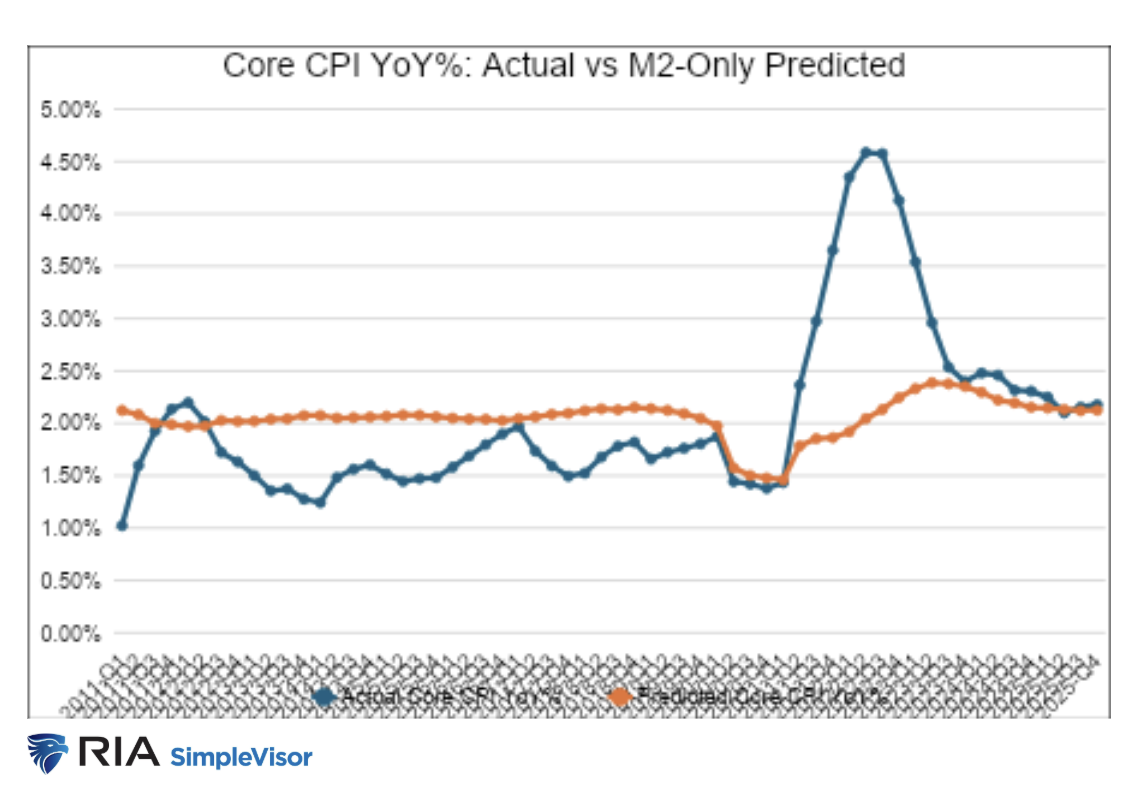

Further, the negative t-statistic (-1.771) indicates a negative relationship. In other words, higher M2 growth leads to lower CPI. Using the regression formula, even though it is insignificant, we can estimate core CPI based on changes in the money supply. As shown below, the forecast is worthless.

Bottom line: The relationship between M2 and CPI is not statistically significant.

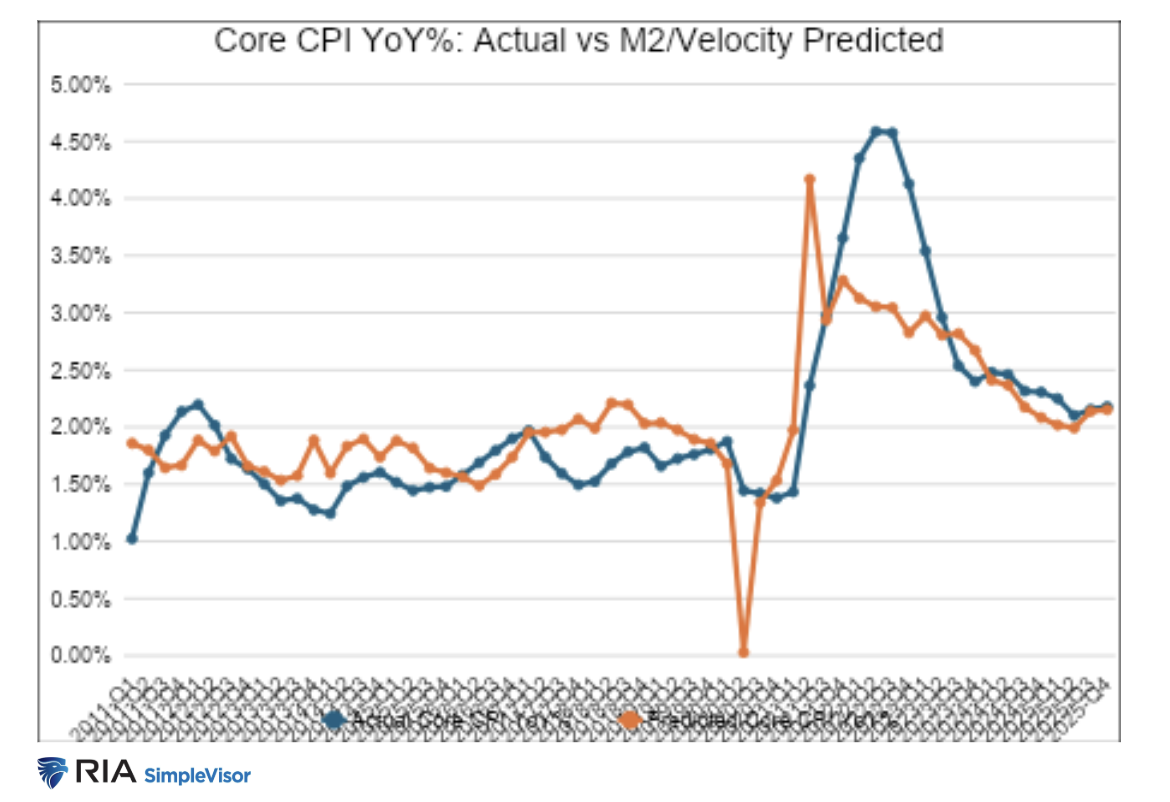

M2, Velocity, and CPI

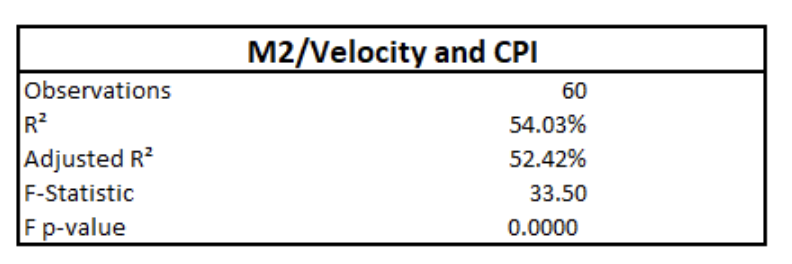

Next, we add monetary velocity into the multiple regression analysis.

The R-squared indicates that the statistical relationship is much more significant when combining velocity and the money supply, accounting for over half of the movements in core CPI. The F p-value statistic indicates a near-zero chance that the relationship is not significant.

Lastly, we can graph the expected core CPI from our analysis to see that the combination of velocity and the money supply is a good indicator of inflation.

Summary

There are reasons to buy and hold gold. However, for those trading gold, it’s important to understand the narratives driving short-run gold prices.

The rising money supply narrative sounds great, but as we discussed, it's important to contextualize the relationship with economic growth. Second, it's not just how much money there is, but how often it circulates.

Many narratives make a lot of sense until you dig into them. It is in these faults that investors can gain a better grasp of the factors driving asset returns and, accordingly, avoid being surprised when the narrative fails.

Read more by Michael Lebowitz:

- BDCs: Not All Yield Is Created Equal

- GFC 2.0 or False Alarm: What Private Credit Is and Isn’t

- Will Private Credit Cause the Next GFC?

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All