ElmAI Overview

ElmAI Overview

- New rules at index providers may allow large IPOs to enter indexes more quickly than in the past, and with recently IPO’d stocks historically underperforming the market by 3-5% per year, index fund investors are understandably on edge about the coming wave of mega-IPOs from SpaceX, OpenAI, and others.

- But the math tells a calmer story: even $280 billion in IPO proceeds would represent just 0.4% of U.S. market cap, and a worst-case scenario implies roughly 0.2% drag on broad index fund returns – about what the market moves in 30 minutes on a typical day.

- Rather than worrying about IPO inclusion timing, investors would be better served focusing on the long-term expected returns of the markets they’re invested in.

Victor was a guest on CNBC and Bloomberg TV recently to give our view on whether index fund investors should be worried about a recent change in rules at Nasdaq and other index providers that will allow large IPOs to enter the indexes more quickly than has been the case. Historically, stocks of companies that have IPO’d have performed poorly relative to the overall market and to stocks with similar characteristics. It’s natural for investors to be concerned. Jay Ritter of the University of Florida, one of the most prolific researchers in this area, has found that over the five years following their IPO, these companies underperformed the market by 3% to 5% per year.1

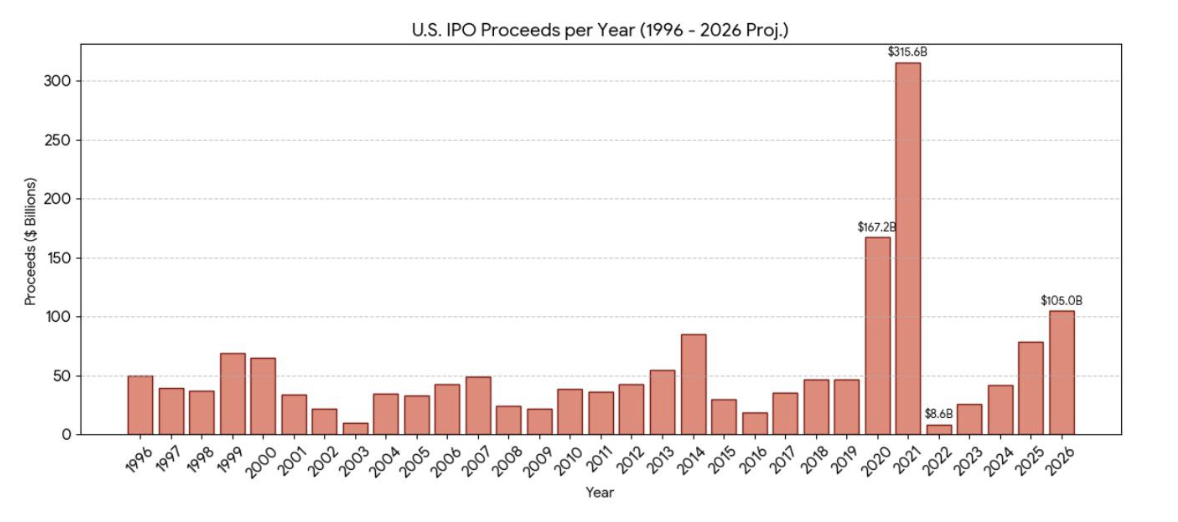

Most investors don’t need to read Professor Ritter’s research to have a feel for the dangers of holding “hot” IPOs beyond the initial post-IPO pop. Many will recall the dismal performance of the huge wave of IPOs in 2020 and the even larger, SPAC-dominated vintage of 2021. So it is understandable that investors are feeling nervous staring down the large volume of IPOs expected to come to market in the next year or two.

Observers forecast the combined market valuation of just the four largest and most well-known private companies – SpaceX, OpenAI, Anthropic, and Stripe – to be in the vicinity of $3 trillion, representing about 5% of total U.S. stock market capitalization. SpaceX alone is rumored to be looking to raise $75 billion to $125 billion of capital in its IPO, which by itself would be larger than all IPOs in 2025 combined. That this is within the realm of possibility is suggested by the recent $125 billion private capital raise completed by OpenAI.

Why the Impact on Index Funds Is Likely To Be Small

Some observers are warning that “the pending OpenAI and SpaceX IPO wave is an ‘existential risk’ to passive fund mechanics.” The impact of these mega-IPOs may well be consequential for the overall performance of the stock market, but their narrow impact on index funds – arising specifically from their accelerated inclusion in broad market indexes – is likely to be muted.

The math tells a calming story: the weight these stocks receive in the indexes will be proportional to the value of their freely floating shares, which initially equals the money raised in their IPOs.2 The Nasdaq 100 index is a notable exception to this treatment, but it represents only about 5% of assets indexed to U.S. stocks via mutual funds and ETFs.

Even if IPOs over the next 12 to 24 months reach $280 billion – at the high end of estimates, and 6x the 2025 total – this would represent just 0.4% of total U.S. stock market capitalization. That is the weight those shares would carry in most major indexes in the period following the IPOs. So even in a pretty nightmarish scenario where these IPOs taken together lost 50% of their value in the year following inclusion – ten times worse than the high end of historical underperformance – the drag on index fund returns would be about 0.2%. This is roughly the amount the stock market moves in 30 minutes of trading on a typical day and is much lower than the extra fees charged per annum by actively managed mutual funds who might tout their ability to dodge these IPOs.

The rule changes that have received so much media attention involve only a modest acceleration of inclusion timing, not a fundamental change in how indexes work. Broad market index funds need to be representative of the overall public equity market, and that means they eventually need to buy and hold stocks that come to market through IPOs. The question is merely one of timing, and the acceleration is small.

Broad Index Funds Are Well-Constructed and Well-Run

For investors tempted to move away from a broad stock market index fund – such as Vanguard’s Total U.S. Stock Market ETF (ticker VTI) – into a product that tries to sidestep the IPO issue, we would caution that the cure may be worse than the disease. Consider, for example, switching to an equal-weight S&P 500 ETF such as RSP, which carries a 0.20% expense ratio – meaningfully higher than VTI’s 0.03% – has 20% annual portfolio turnover, and is effectively engaged in stock-picking with no expert company analysis.

More broadly, the best index funds are impressively well-run. VTI, for example, reports annual portfolio turnover of just 2%. There is a limit to how much such low turnover could be hurting returns through the adversarial trading of hedge funds and trading firms. VTI, which tracks the CRSP index, arguably represents the best-constructed broad U.S. equity index product, but other well-built indexes from MSCI and FTSE are not far behind. On the other hand, narrower indexes such as the Dow Jones 30, the Nasdaq 100, and the S&P 500 are not the ideal vehicles for broadly diversified, low-cost equity exposure, as they are more concentrated and have more frequent reconstitution activity.3

The “Passive Departure” Claim

Some readers may have encountered the argument, advanced by Haddad, Plosser, and Sammon in their paper “Passive Departure,”4 that index funds suffer an opportunity cost of 0.5% to 0.7% per year compared to a more active strategy that the authors backtest. We think this claim deserves scrutiny. For an index fund like VTI with 2% annual turnover, a drag of 0.5% to 0.7% per year would imply that index funds are losing on the order of 25% to 35% on every dollar they trade – and that other market participants are earning correspondingly large profits on the other side. This is simply not plausible, particularly when one considers that much of an index fund’s turnover consists of activity that is unlikely to be exploited by other traders, such as selling shares into corporate stock buyback programs.

We have met a number of portfolio managers at Vanguard and other large index fund firms, and we’ve found them to be experienced and sophisticated operators. They typically have some discretion to manage trading risk and minimize market impact. The index publishers themselves are also aware of the potential costs their inclusion and exclusion rules can impose on index fund performance, and they generally design those rules to be difficult to front-run. Over time, even as indexing has grown dramatically, the hedge fund business of trading around index reconstitutions has seen its alpha decline.5

What Investors Should Focus On

Rather than worrying about the narrow impact of faster IPO inclusion on index fund performance, we think investors would be better served by focusing on the long-term expected returns offered by the markets in which they’re investing – in particular the U.S. and non-U.S. equity markets. These expected returns will, by far, be the most impactful inputs to how investors should allocate capital and budget spending. Capital market assumptions can be found online from many reputable sources, and they tend to be reasonably close to each other. Our own expected return forecasts are available at Elm CMAs and you can see how we use them to decide our asset allocation, currently and historically, with our allocation viewer.

Read more by Victor Haghani and James White:

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

1 Measured from the closing price on the first day of trading, not the IPO offer price. Ritter, Jay. “Initial Public Offerings: Updated Statistics.” University of Florida, 2025. Available here; and Loughran, T. and Ritter, J. (2004). “Why Has IPO Underpricing Changed Over Time?” Financial Management.

2 Over time, as insiders become free to sell their shares, the free float will increase, and so will their index weight.

3 The inclusion and exclusion decisions of the S&P 500 index can be quite subjective, which might sound like a good thing, until you consider that Tesla was kept out of the index for 10 years, missing an impressive amount of appreciation. In those 10.5 years of waiting for inclusion, Tesla stock appreciated 230-fold. If it had been included at the start with a weight of just 0.015% of the S&P 500 index, it would have added about 0.3% per year to the 10-year return of the S&P 500. IPO’d stocks don’t always underperform, and early inclusion isn’t always a bad thing.

4 Haddad, V., Plosser, M., & Sammon, M. (2023). “Passive Departure.” Working Paper, Harvard Business School.

5 For example, see “The Index Inclusion Effect: More Crowded, More Complex,” Goldman Sachs (2024, 2025)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Victor Haghani, James White

ElmAI Overview

ElmAI Overview