Weekly Economic Snapshot: Softening Labor Market and Cooling Inflation

The economic narrative last week was dominated by a mix of cooling inflation and a softening labor market. The ADP employment report signaled a continued slowdown by showing a surprise drop in private sector jobs, while the Fed's preferred inflation gauge offered minor relief by unexpectedly inching lower. Separately, the University of Michigan Consumer Sentiment Index showed consumers' mood remains somber despite a slight rise in overall optimism. Against this backdrop, the S&P 500 index nonetheless extended its powerful rally, recording four consecutive daily gains to inch within striking distance of a new all-time high. With a shutdown-delayed economic calendar complicating the outlook ahead of the Federal Reserve's final meeting of the year this week, policymakers face the difficult task of balancing signs of an economic slowdown against still-elevated inflation.

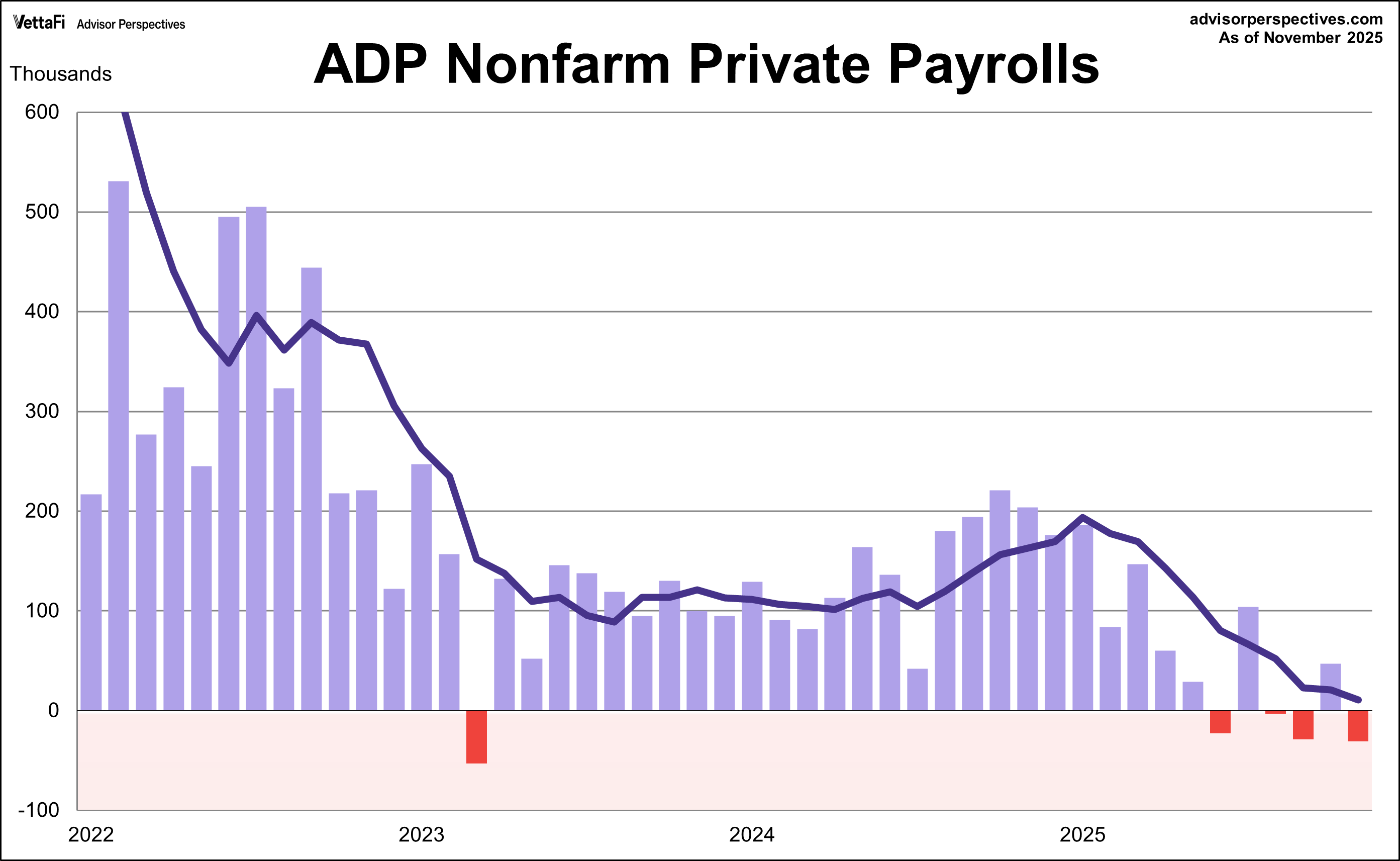

ADP Employment Report

Although the record-long government shutdown recently ended, the Bureau of Labor Statistics (BLS) monthly jobs report was postponed to mid-December. As a result, the ADP private sector employment report is currently serving as the primary gauge for the labor market.

The November ADP employment report showed the private sector unexpectedly shed 32,000 jobs last month, the largest loss since March 2023. This figure was below the projected addition of 5,000 jobs and marks a sharp decline from the 47,000 jobs added in October. The latest data reinforces the narrative of a softening labor market, as it was the fourth month of private sector job losses within the last six.

The losses were most notable among small businesses (those with fewer than 50 employees), which combined to shed 120,000 jobs. In contrast, mid-sized and large businesses collectively added 90,000 jobs in November.

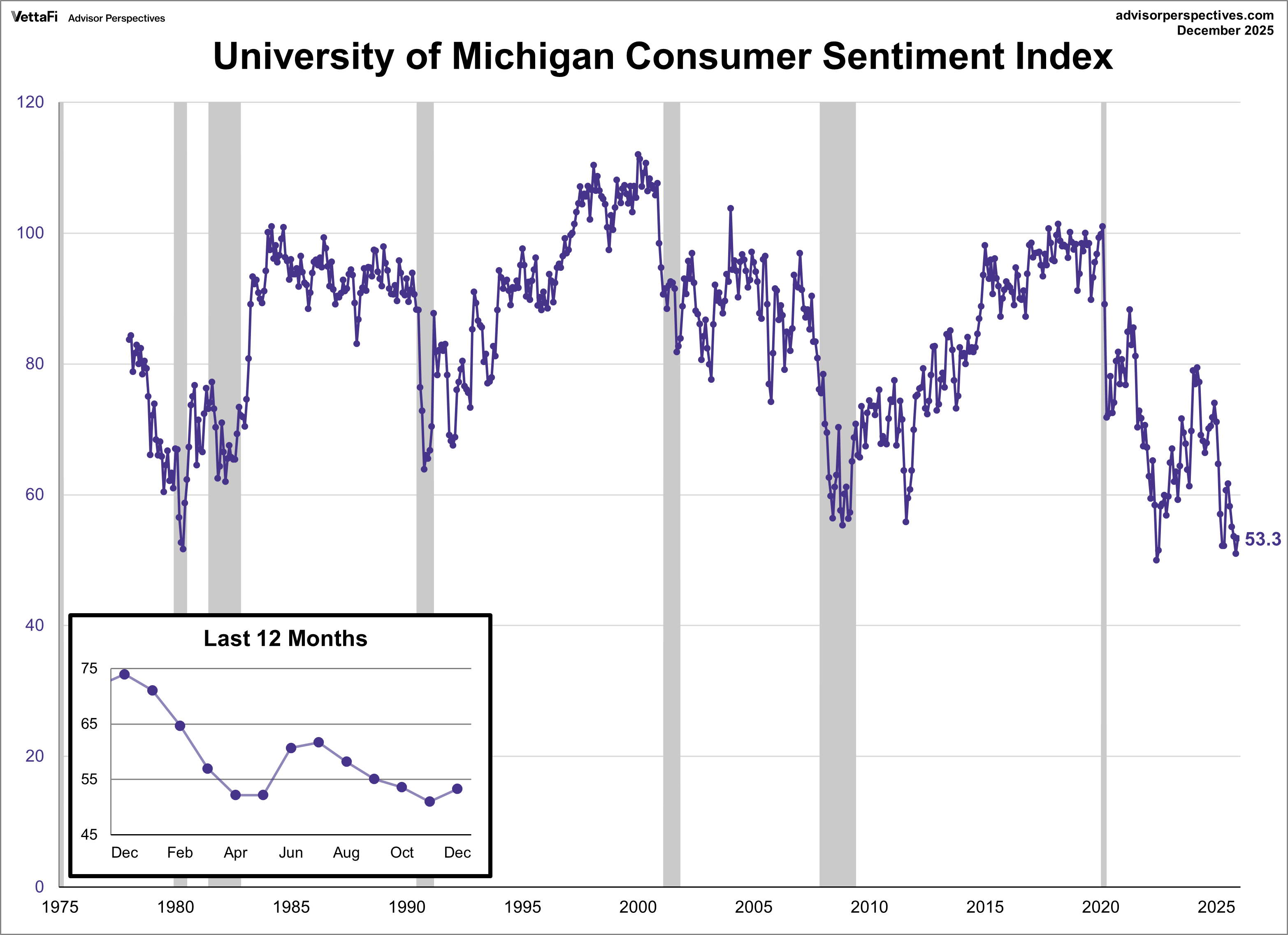

Michigan Consumer Sentiment

Consumer sentiment improved for the first time in five months, though the overall mood remains somber. The University of Michigan Consumer Sentiment Index rose nearly 5% to 53.3 this month, keeping the index near a historically low level. The latest reading reflects a nearly 30% decline in sentiment compared to a year ago.

The index's increase can largely be attributed to improvements in consumers’ perceptions of expected personal finances, with optimism evident across nearly all demographics. However, consumers’ views of current conditions continued to worsen, falling to a new record low.

On the inflation front, near-term expectations cooled for a fourth straight month, dropping from 4.5% in November to 4.1% in December. Similarly, long-term expectations cooled for a second straight month, falling from 3.4% to 3.2% for the five-year outlook. Despite these declines, which brought both series hitting their lowest levels since earlier this year, consumers continued to cite high prices as a top concern.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

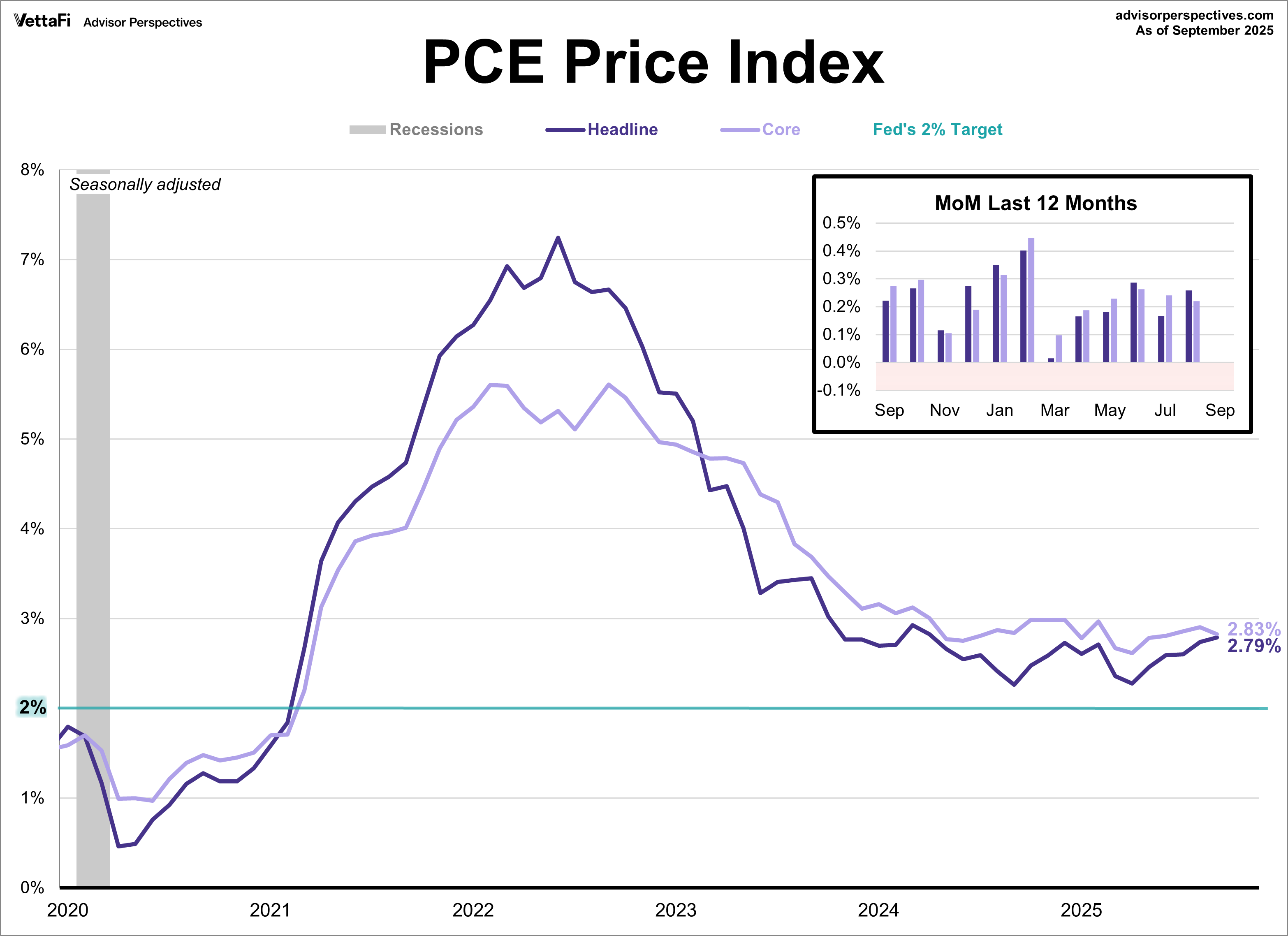

PCE Price Index

The Federal Reserve’s preferred inflation gauge unexpectedly cooled for the first time in five months, but remains well above the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.8% year-over-year in September. This was lower than the forecast of 2.8% and marked a slight slowdown from August. Meanwhile, the headline index remained at its highest level since April 2024, rising 2.8%, as expected. On a monthly basis, core prices rose by 0.2% and headline prices rose by 0.3%, both as expected.

Market Reactions

The S&P 500 came off its best week since May with another solid performance. The index closed the week out on a four day win streak, putting it within inches of a new record high. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.3% last week. Meanwhile, the S&P Equal Weight Index was up 0.2% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.2%.

The 10-year Treasury yield finished the week at 4.14%, while the 2-year note finished at 3.56%.

The CME FedWatch Tool currently shows an 87% likelihood that the Fed will cut rates by 25 basis points at their meeting this week. Markets are also pricing in two additional 25 basis point cuts in 2026.

Economic Data in the Week Ahead

The main event this week is the Federal Reserve's final meeting of the year. Policymakers will determine the path of interest rates heading into the new year, but yet again, they will be forced to do so with limited data, as the lingering effects of the government shutdown continue to shuffle the economic calendar. While the data flow is improving, key reports like the September Job Openings and Labor Turnover Survey (JOLTS) are still releasing later than their typical spot at the beginning of the month. Other updates throughout the week will include the NFIB Small Business Optimism Index, weekly unemployment claims and the trade balance.