As the second half of January begins, the U.S. economy presents a picture of cooling inflation and resilient consumer activity. While consumer price growth hit a six-month low in December and retail sales rebounded to start the holiday season, investor sentiment has reached a fever pitch. Record-high margin debt levels now suggest a significant increase in market risk-taking. This report analyzes shifting inflation dynamics, consumer strength, and the implications of heightened financial leverage.

Inflation: A Tale of Two Indexes

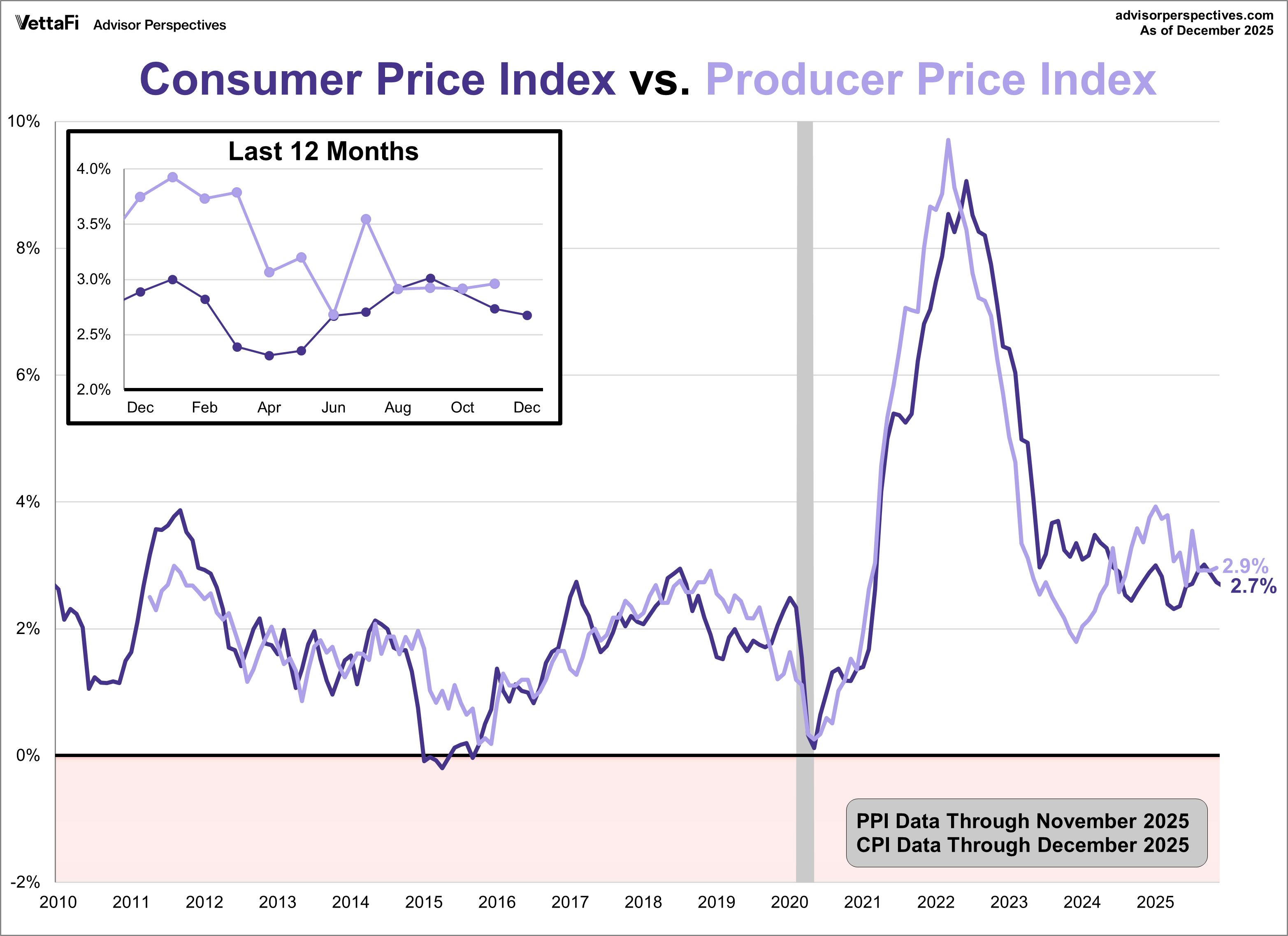

Consumer inflation cooled for a second straight month in December, hitting its lowest level in six months. The Consumer Price Index (CPI) came in at 2.68% last month, down from 2.74% in November and in line with expectations. On a monthly basis, prices were up 0.3%, as expected. Core inflation, which excludes volatile food and energy, inched slightly higher from 2.63% in November to 2.64% in December. Additionally, core prices were up 0.2% from the previous month. Both readings were lower than their respective forecasts.

However, business-side inflation told a different story, as the Producer Price Index (PPI) unexpectedly ticked higher in November. The index came in at 2.95%, up from 2.80% in October and higher than the forecast of 2.7%. On a monthly basis, wholesale prices were up 0.2% in November, a pickup from October 0.1% growth and in line with expectations. The PPI is considered a leading indicator of consumer inflation, as falling costs for producers often precede a slowdown in consumer prices.

Retail Sales: Consumers Keep Spending

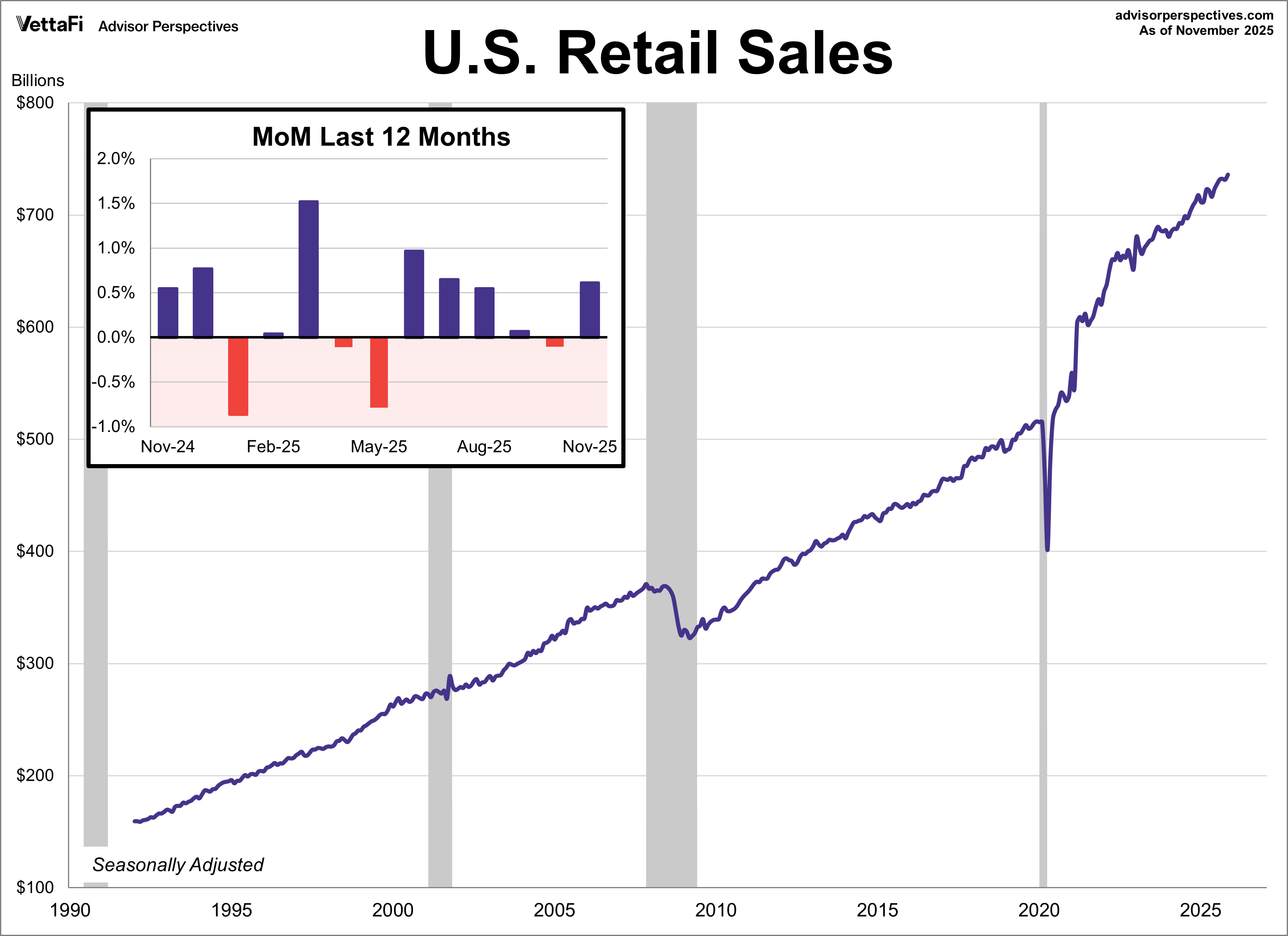

Consumer spending saw a healthy rebound in November as the holiday shopping season kicked off. Retail sales climbed 0.6%, outperforming the 0.5% forecast and marking a sharp recovery from October’s revised decline of -0.1%.

The increase was broad-based, with strong gains at sporting goods, hobby, musical instrument, and book stores as well as building material and garden stores. However, spending was down slightly at furniture stores.

Core sales, which exclude autos, were also higher than expected, rising 0.5% against the projected 0.4% growth. However, control purchases, a crucial GDP input and an even more “core” view of retail sales, came in below expectations with a 0.3% rise, falling short of the 0.4% forecast.

Retail sales could impact the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

Margin Debt: Record Breaking Risk

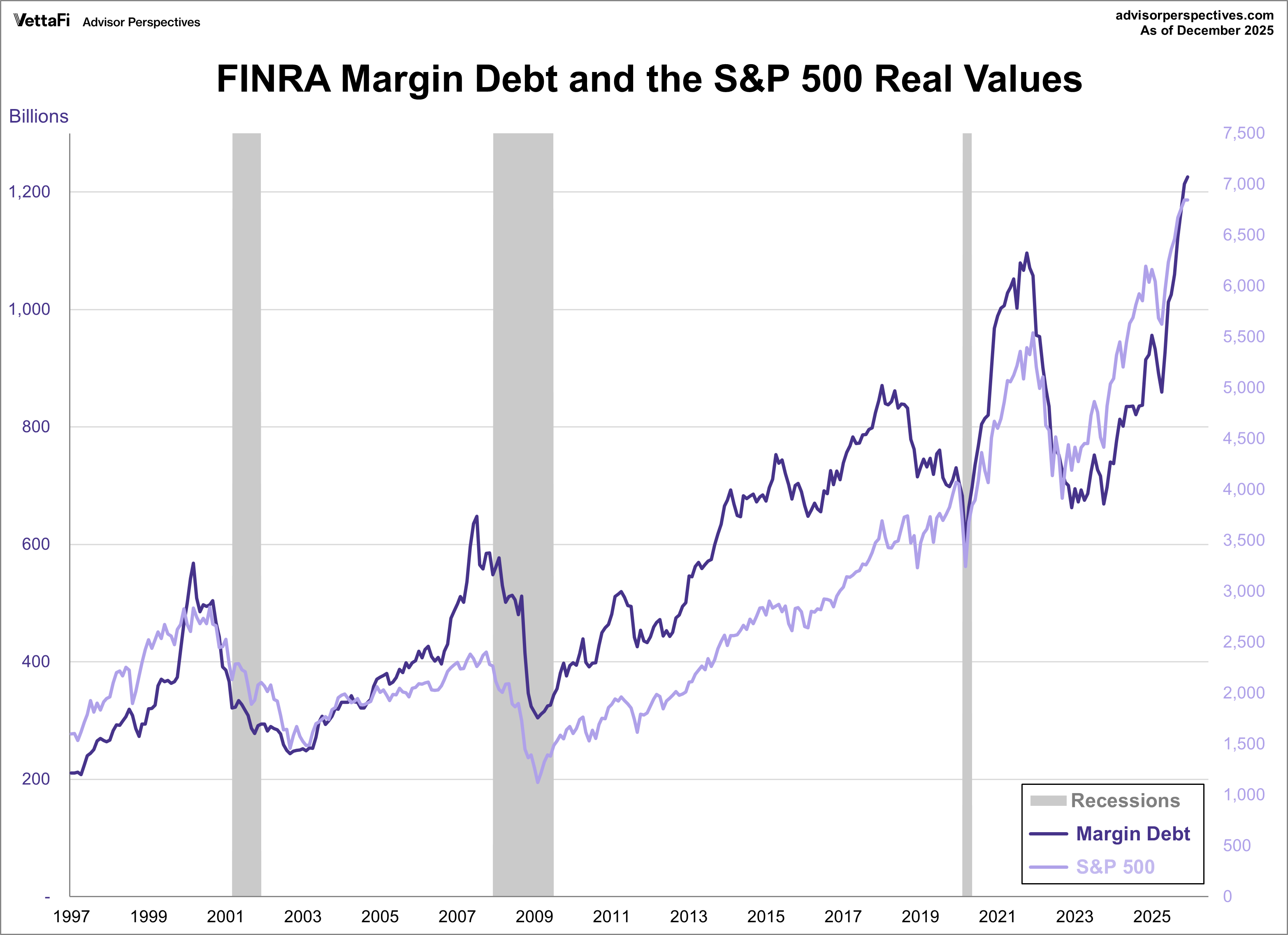

Margin debt reached a new high of $1.23 trillion in December, marking the eighth consecutive monthly increase and its sixth straight record. More significantly, when adjusted for inflation, the real debt level is also at its highest level in history, sitting just above the prior 2021 peak. This historic climb represents more than a 30% surge over the past year.

Margin Debt is a key indicator of investor sentiment and risk appetite. There is a near-parallel relationship between debt levels and the stock market, as significant increases in borrowing, often correlate with market peaks, while troughs in debt tend to precede market bottoms. While high levels of margin debt can signal strong investor confidence, it also means a higher risk appetite which can increase market volatility. The scale of borrowing over the past several months suggests unparalleled levels of risk-taking in the current stock market environment.

Market Reactions

The S&P 500 reached a record high on Monday before retreating to end the week with a 0.4% loss. As a result, the SPDR S&P 500 ETF Trust (SPY) fell -0.3% last week. Meanwhile, the S&P Equal Weight Index was up 0.7% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.7%.

The 10-year Treasury yield finished the week at 4.24%, while the 2-year note finished at 3.59%.

The CME FedWatch Tool currently shows a 95% chance the Fed will hold rates steady at their meeting at the end of the month. Markets are currently pricing in two 25 basis point cuts in 2026, coming at the June and December meetings, and none for 2027.

Economic Data in the Week Ahead

-

Monday: Holiday - no data

-

Tuesday: No notable data

-

Wednesday: Pending Home Sales

-

Thursday: Q3 GDP updated estimate, November PCE Price Index, Weekly Jobless Claims

-

Friday: University of Michigan Consumer Sentiment Index

Read more commentaries by VettaFi | Advisor Perspectives