Weekly Economic Snapshot: Fed Shifts to “Wait-and-See” as Confidence Plummets

The final week of January saw a stark divergence between official policy and the American consumer's outlook. While the Federal Reserve maintained a "solid" view of economic growth, the public’s mood plummeted to a decade-low as sticky amid sticky wholesale inflation. This tension culminated in a wild week for the stock market, where the S&P 500's historic climb past 7,000 was abruptly reversed by the announcement of a new Fed Chair.

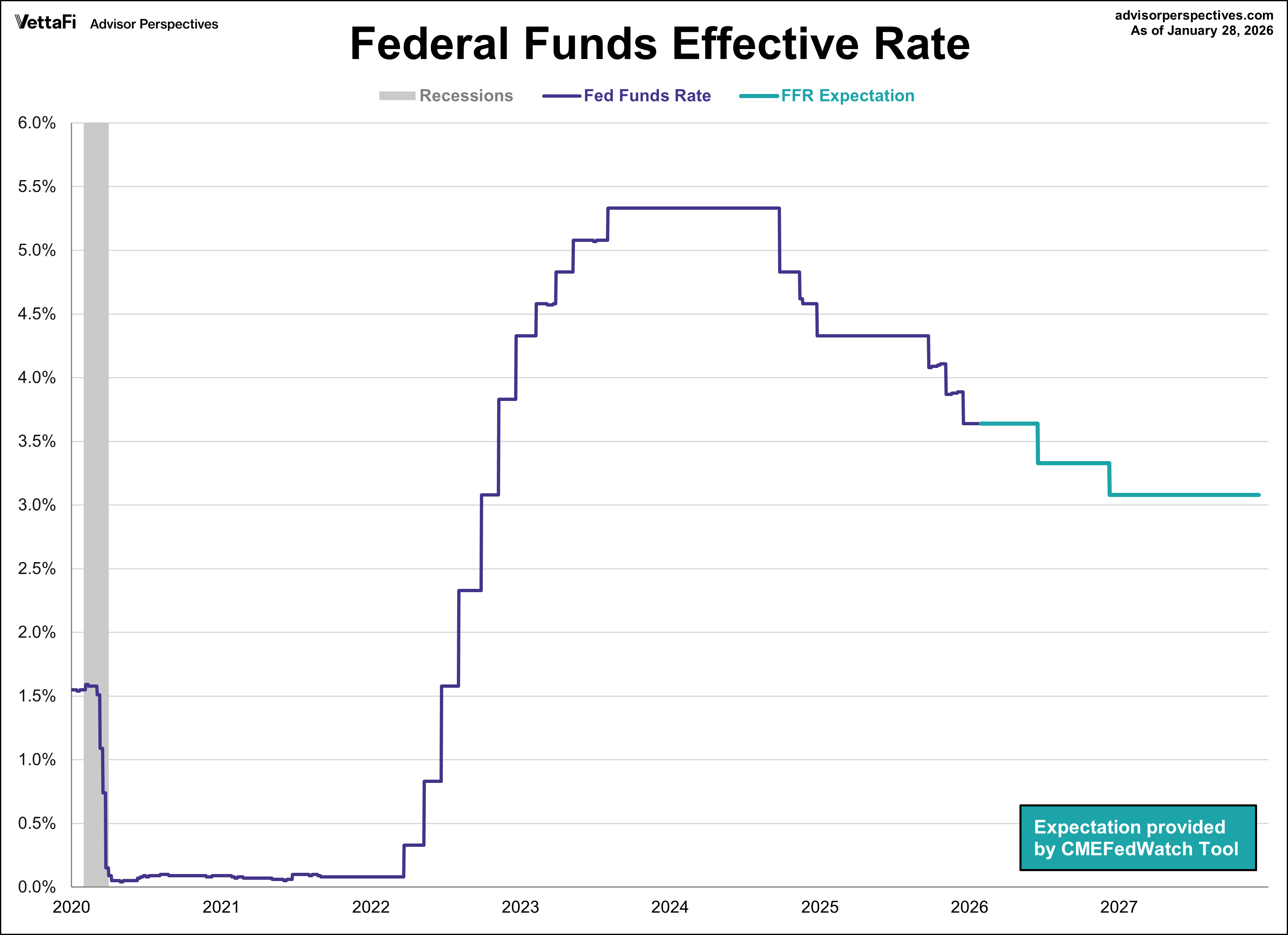

Federal Reserve Meeting: January 28, 2026

The Federal Reserve concluded its first meeting of the year by holding the federal funds rate in the range of 3.50%-3.75%. This pause follows a series of three consecutive rate cuts of 25-basis-points cuts and keeps the central bank’s range at its lowest level since November 2022.

While the move was widely anticipated, the Fed’s press release featured notable changes compared to previous ones. The Fed removed mentions of "downside risks to employment," instead describing the unemployment rate as "showing signs of stabilization”. Additionally, economic activity is now characterized as expanding at a "solid" pace, an upgrade from the "moderate" pace cited in previous meetings. Essentially, the Fed has entered back into wait-and-see mode as they continue to balance a somewhat cooling labor market against persistent price pressures.

The CME FedWatch Tool currently indicates an 87% likelihood that the Fed will hold rates steady at their next meeting, compared to a 13% likelihood of a 25 basis point cut. Markets are currently projecting two 25 basis point cuts for 2026, coming at the June and December meetings, and none in 2027.

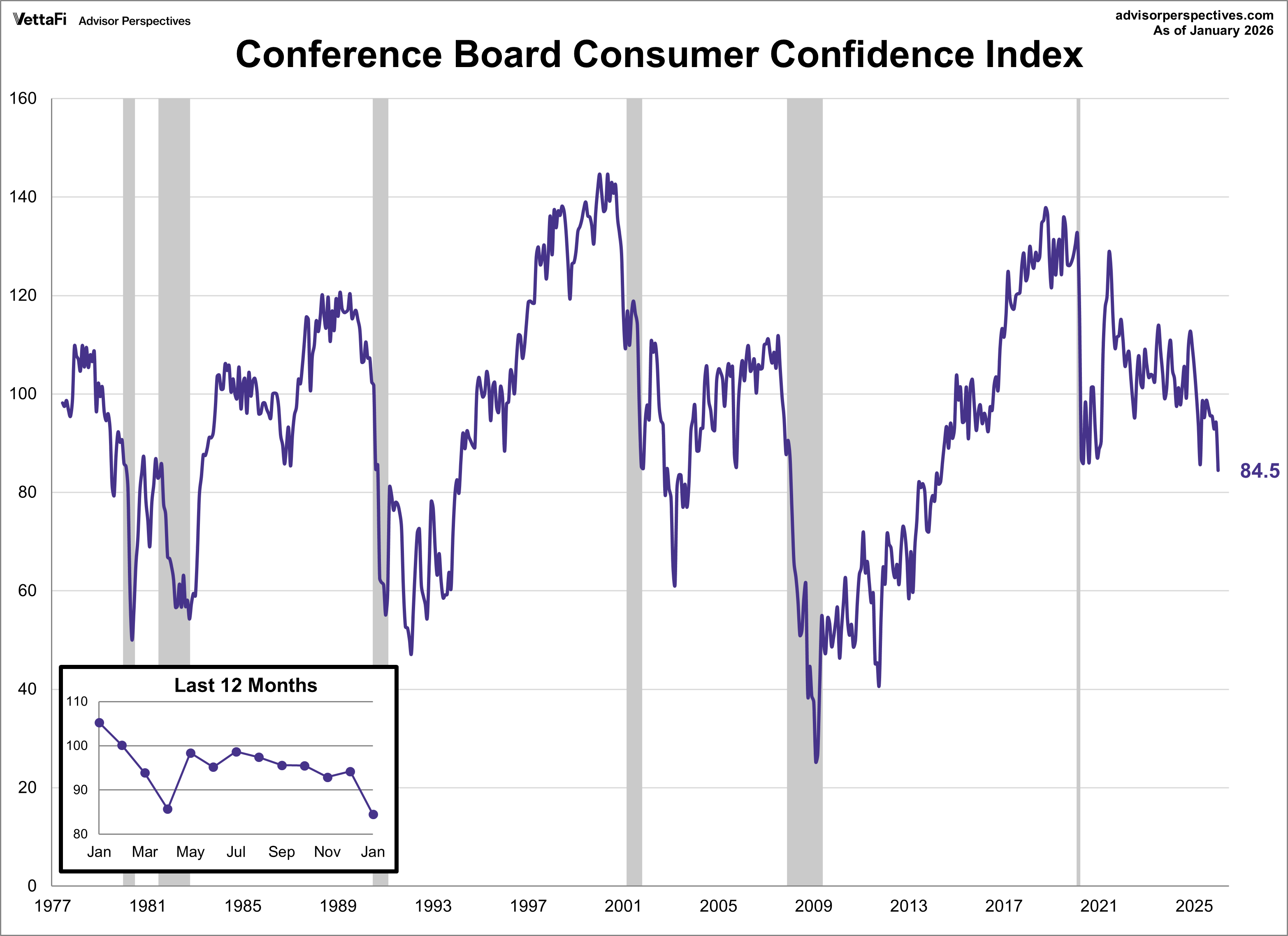

Conference Board Consumer Confidence Index

In sharp contrast to the Fed's "solid" economic outlook, the Conference Board Consumer Confidence Index® plummeted in January. The index dropped 9.7 points to 84.5, its lowest level since 2014. This represents the steepest decline in over four years, driven by deepening pessimism across all five index components, including future business and labor market conditions. Consumers remain primarily concerned with high prices, as 12-month inflation expectations edged higher once again.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

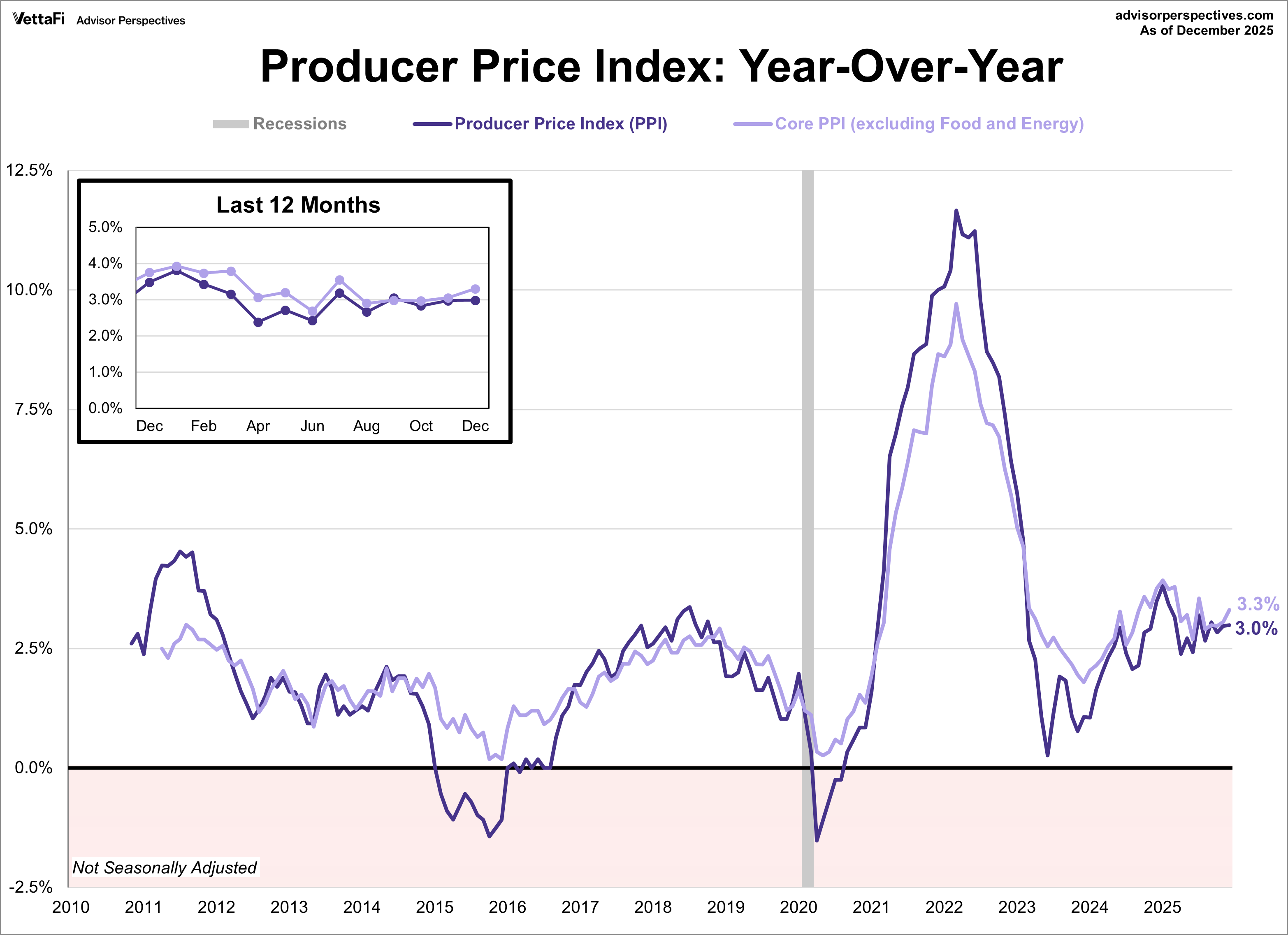

Producer Price Index

Adding to the Fed’s cautious stance, wholesale inflation rose more than anticipated in December. The Producer Price Index (PPI) increased 0.5% month-over-month, outpacing the 0.2% forecast. On an annual basis, the PPI remained at 3.0%, higher than the 2.7% expected by analysts.

Core PPI (excluding food and energy) also showed heat, rising 0.7% for the month and 3.3% annually. Because the PPI is often a leading indicator of consumer inflation, these rising costs for producers may signal a future pickup in prices for everyday consumers.

Market Reactions

The S&P 500 reached a new record high this week, even momentarily surpassing 7,000 for the first time. Despite these early advances, the index declined through the latter half of the week, wiping out most of its initial gains. Ultimately, the index concluded the week with a modest gain of 0.3%. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.4% last week. Meanwhile, the S&P Equal Weight Index was down -0.4% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell -0.4%.

The 10-year Treasury yield finished the week at 4.26%, while the 2-year note finished at 3.52%.

Economic Data in the Week Ahead

- Monday: S&P Global Manufacturing PMI (Jan), ISM Manufacturing PMI (Jan)

- Tuesday: JOLTS (Dec)

- Wednesday: ADP Employment (Jan), S&P Global Services PMI (Jan), ISM Services PMI (Jan)

- Thursday: Weekly Jobless Claims

- Friday: BLS Employment (Jan), University of Michigan Consumer Sentiment Index (Feb prelim)