Weekly Economic Snapshot: Jobs Data Softens While Consumer Sentiment Rises

The U.S. labor market showed further signs of cooling last week as private sector hiring slowed and job openings reached their lowest levels in over five years. While a brief government shutdown delayed official federal employment data, private reports and turnover summaries reinforced a narrative of diminishing demand for workers. Despite these softening conditions, consumer sentiment provided a modest bright spot, inching to its highest point since last summer. As the S&P 500 continues to hover near record highs, investors are now looking toward a packed data week, including the delayed BLS jobs report and fresh inflation figures, to gauge the Federal Reserve’s next move.

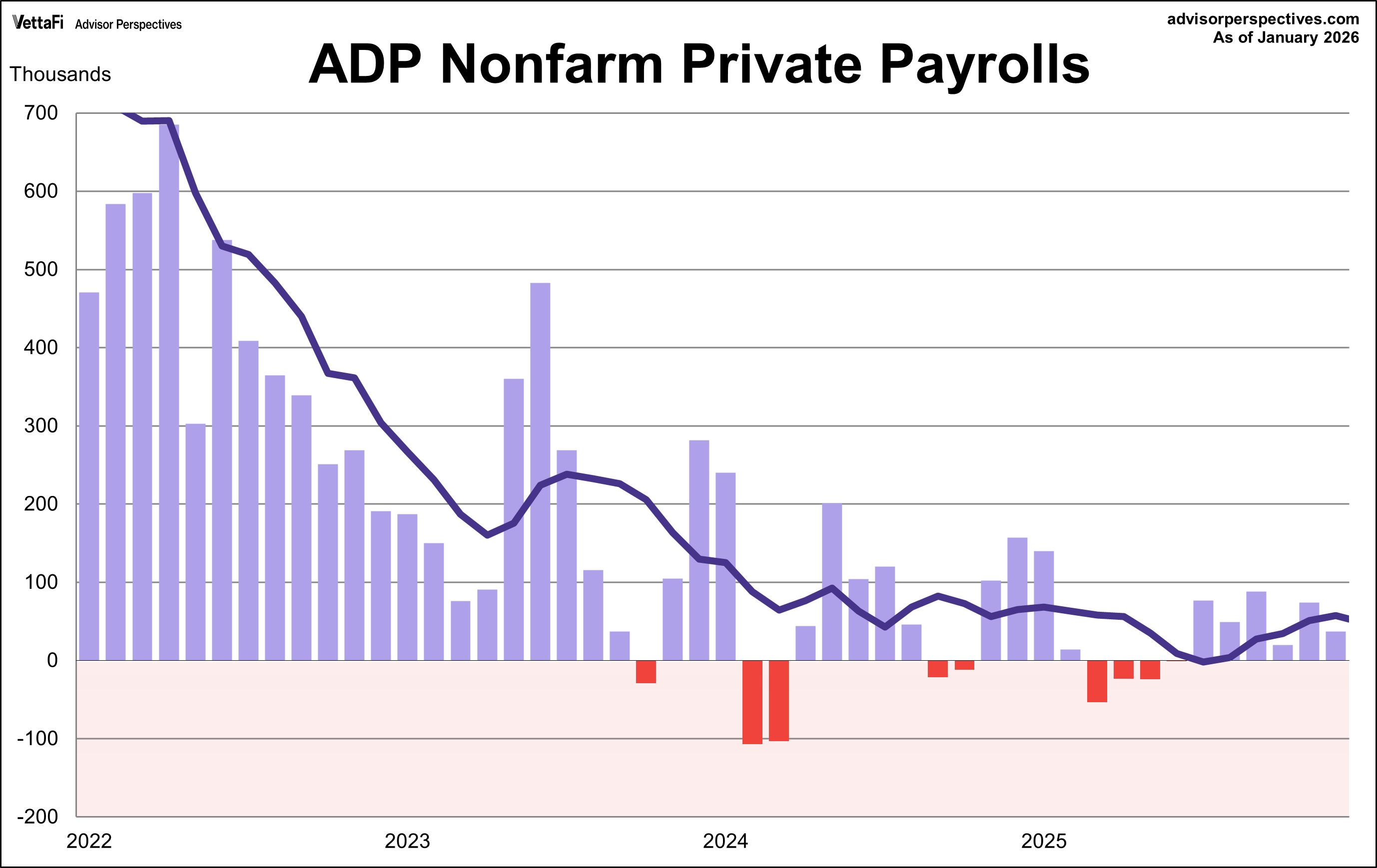

ADP Employment Report

Due to a brief partial government shutdown last week, the Bureau of Labor Statistics' (BLS) monthly jobs report was postponed until this coming Wednesday. Consequently, the ADP private sector employment report took center stage in assessing the current labor market.

The January ADP employment report showed the private sector added 22,000 jobs last month, missing the projected 46,000 by more than half. This represents a significant decline from the 37,000 jobs added in December, signaling a continued slowdown in private sector hiring.

The job gains were most notable among mid-size businesses (those with 50-249 employees), which added 37,000 jobs. In contrast, small businesses with 20-49 employees experienced the largest loss, shedding 30,000 jobs.

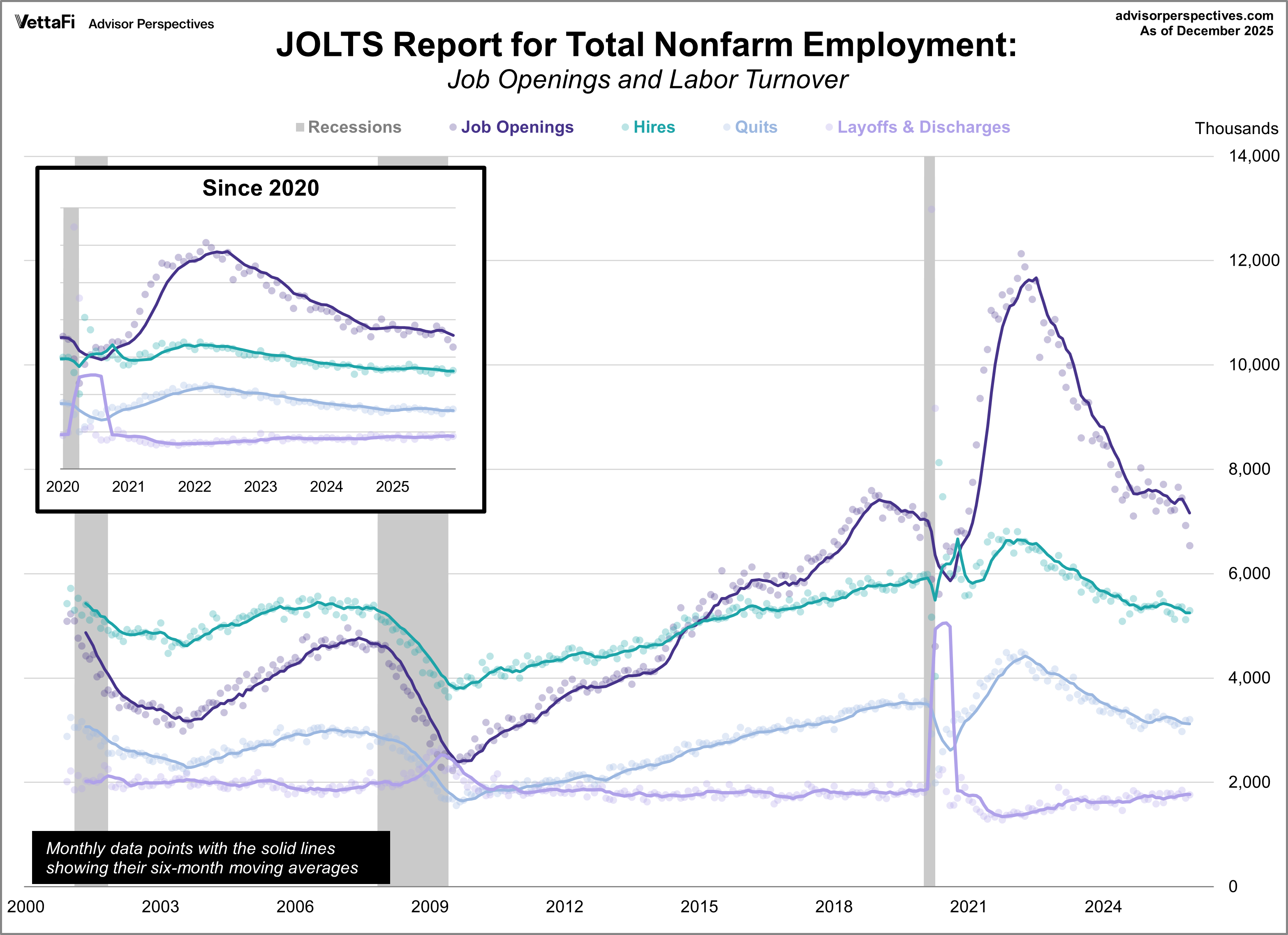

Job Openings and Labor Turnover Summary (JOLTS)

The cooling narrative was further supported by the latest JOLTS report, which showed job openings falling for a third consecutive month in December. Openings dropped to 6.542 million, the lowest level since September 2020 and significantly below the expected 7.200 million vacancies.

Crucially, the job openings-to-unemployed-workers ratio fell to 0.87, its lowest point in nearly four years. This shift indicates that there are now more unemployed individuals seeking work than there are available job openings.

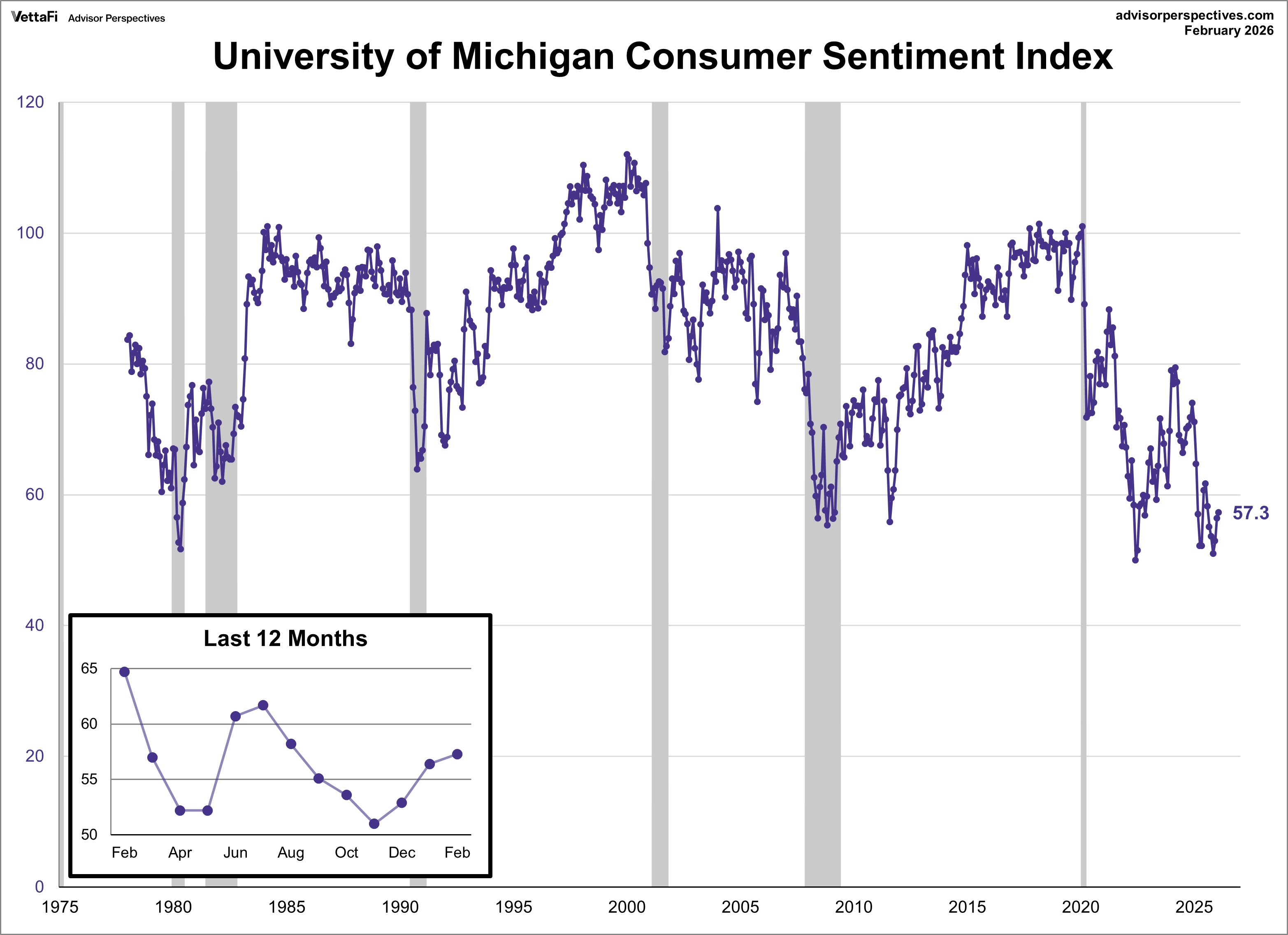

Michigan Consumer Sentiment

In a slight reversal of the labor market’s gloom, consumer sentiment rose for a third straight month in February. The University of Michigan Consumer Sentiment Index inched up 0.9 points to 57.3, outperforming the forecasted 55.0. However, this six-month peak offers little relief as sentiment remains historically low, currently sitting in the 3rd percentile of the series’ history.

The “current conditions” subcomponent rose for a second straight month, while the “expectations” subcomponent fell for the first time in four months. However, optimism is still tempered by ongoing price pressures and a perceived weakening in labor markets. On the inflation front, near-term expectations cooled for a sixth straight month, dropping from 4.0% in January to 3.5% in February. Long-term expectations rose for a second straight month, inching up from 3.3% to 3.4% for the five-year outlook.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Market Reactions

The S&P 500 experienced a mid-week slump before rebounding on Friday with its strongest single-day gain since May. The index ended the week down -0.1% but remains within reach of a new record high. As a result, the SPDR S&P 500 ETF Trust (SPY) fell -0.2% last week. Meanwhile, the S&P Equal Weight Index was up 2.1% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 2.1%.

The 10-year Treasury yield finished the week at 4.22%, while the 2-year note finished at 3.50%.

The CME FedWatch Tool currently indicates an 82% likelihood that the Fed will hold rates steady at their next meeting, compared to a 18% likelihood of a 25 basis point cut. Markets are currently projecting two 25 basis point cuts for 2026, coming at the June and September meetings, and none in 2027.

Economic Data in the Week Ahead

- Monday: No notable data

- Tuesday: Retail Sales (Dec), NFIB Small Business Optimism Index (Jan)

- Wednesday: BLS Employment Report (Jan)

- Thursday: Weekly Jobless Claims, Existing Home Sales (Jan)

- Friday: Consumer Price Index (Jan)