Weekly Economic Snapshot: Inflation Heat Meets a Cooling Economy

The U.S. economy sent conflicting signals last week as a sharp deceleration in growth collided with unexpectedly stubborn inflation. While the S&P 500 managed to break its recent losing streak, the Federal Reserve’s primary inflation gauge hit its highest level since early 2024, complicating the outlook for potential interest rate cuts later this year. As investors weigh a fragile uptick in consumer sentiment against a cooling GDP, the focus shifts to whether the economy can maintain its footing in the face of persistent price pressures.

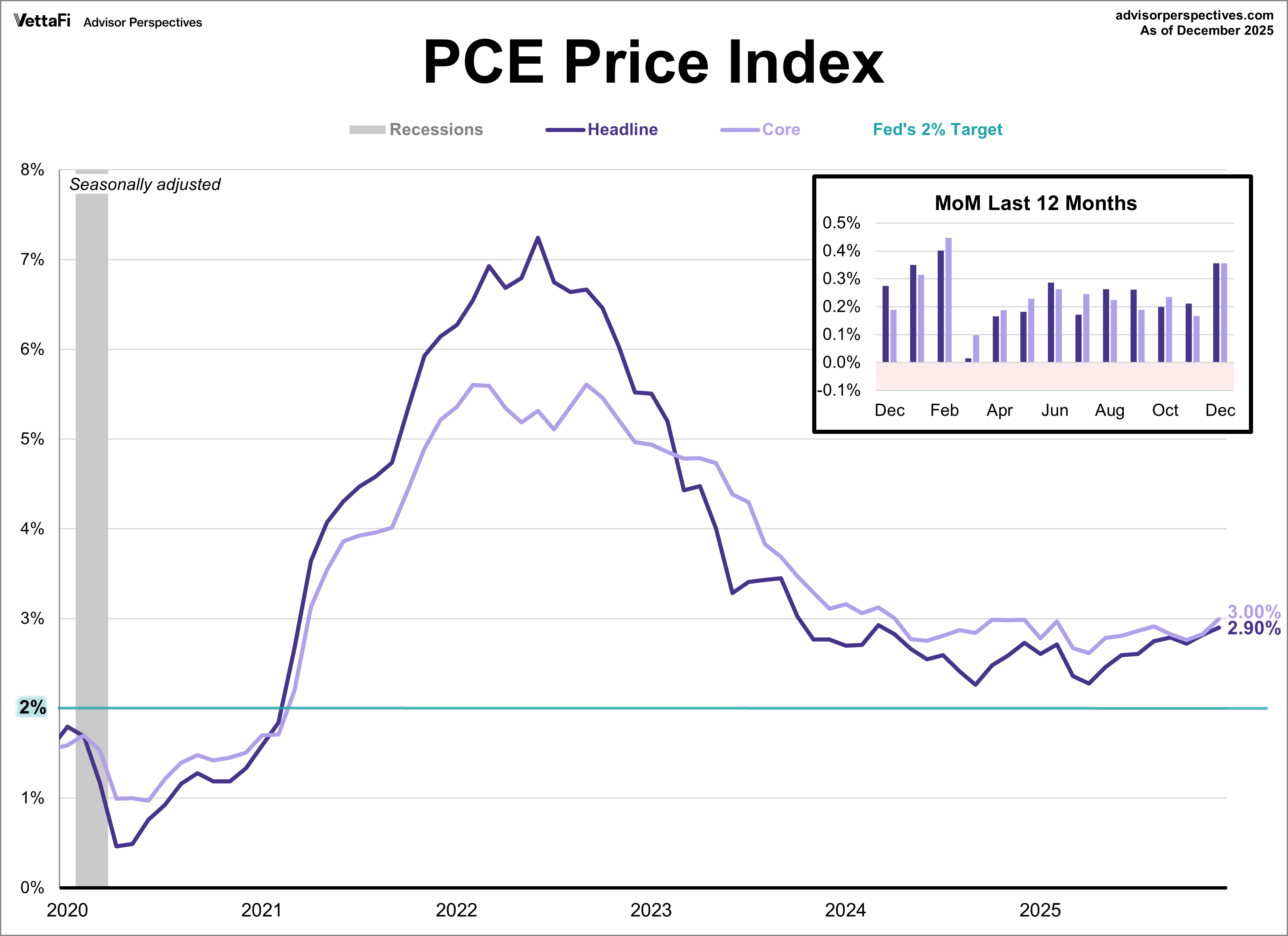

PCE Price Index: Inflation Pressures Intensify

The Federal Reserve’s preferred inflation gauge came in hotter than expected, with the Core Personal Consumption Expenditures (PCE) Price Index climbing to 3.0% year-over-year. This figure, which excludes volatile food and energy costs, exceeded the 2.9% forecast and marked an acceleration from November’s 2.8% reading. The headline index followed a similar path, rising 2.9% annually, to surpass both the previous month’s data and forecast. On a monthly basis, both core and headline prices increased by 0.4%, topping expectations and marking the sharpest monthly growth since February.

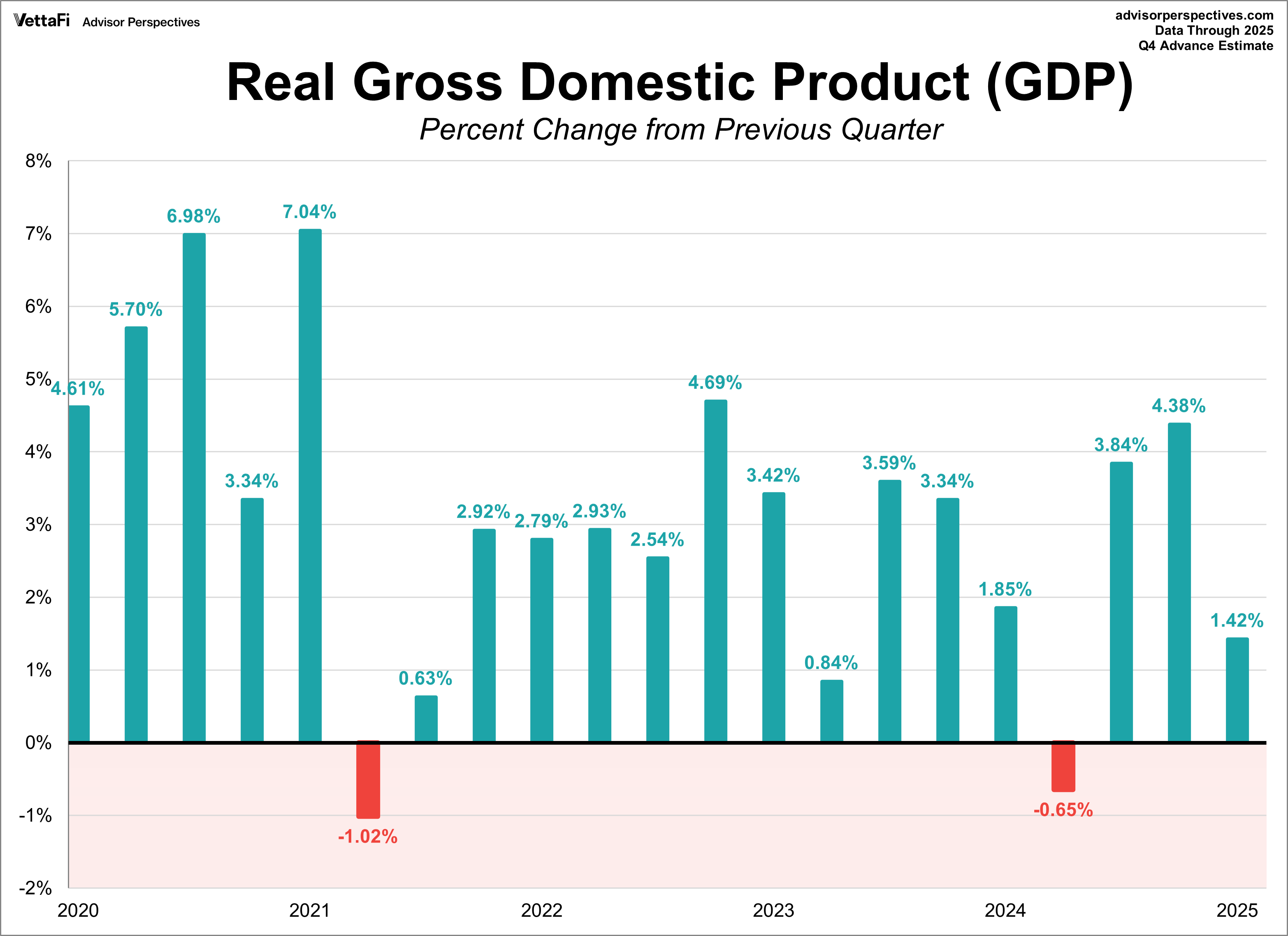

Gross Domestic Product (GDP): Growth Loses Momentum

The U.S. economy lost significant momentum in the final months of 2025, according to the BEA’s advance estimate. Real GDP expanded at an annual rate of 1.4% in the fourth quarter, a sharp declaration from the robust 4.4% growth recorded in the third quarter and only half of the 2.8% forecast. While the expansion was primarily driven by increases in consumer spending and business investment, these gains were partially offset by notable declines in exports and government spending.

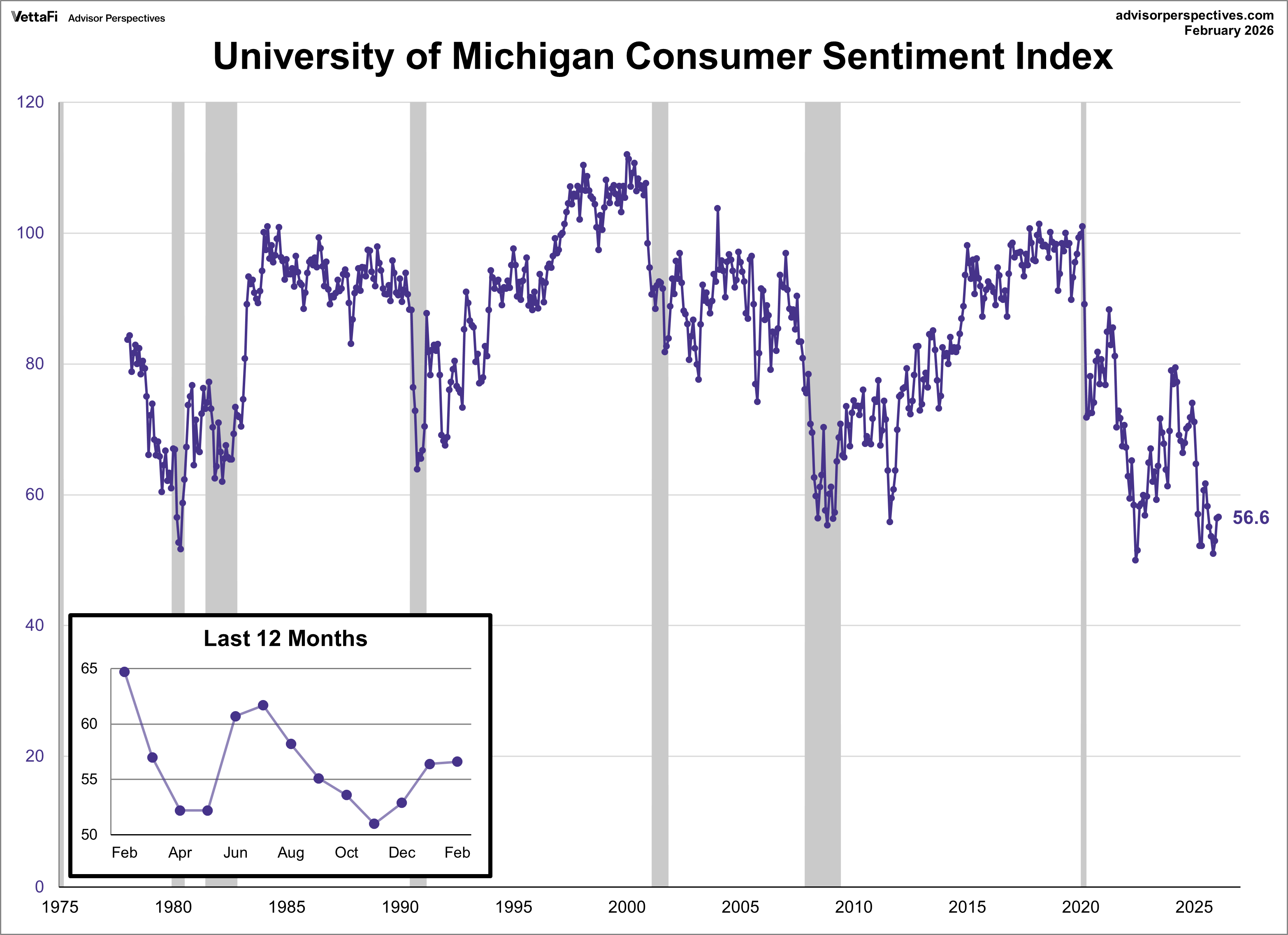

Consumer Sentiment: A Fragile Six-Month High

Consumer sentiment rose for a third consecutive month in February, reaching a six-month peak as the University of Michigan Consumer Sentiment Index inched up to 56.6. Despite this improvement, the index fell short of the 57.3 forecast and remains historically low, currently sitting in only the 3rd percentile of the series’ history.

While the "current conditions" subcomponent rose for a second month, the "expectations" subcomponent fell for the first time in four months as ongoing price pressures continued to temper optimism regarding personal finances. Interestingly, sentiment varied by demographic, with higher optimism reported by consumers with large stockholdings and higher education levels. On the inflation front, near-term expectations cooled to 3.4%, the lowest level in over a year, while long-term five-year expectations remained unchanged at 3.3%.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Market Reactions

The S&P 500 posted its first weekly gain since January, rising 1.1% after spending the majority of last week in positive territory. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.1% last week. Meanwhile, the S&P Equal Weight Index was up 0.6% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.6%.

The 10-year Treasury yield finished the week at 4.08%, while the 2-year note finished at 3.48%.

The CME FedWatch Tool currently shows a 96% chance the Fed will hold rates steady at their meeting next month. Markets are currently pricing in two 25 basis point cuts in 2026 coming at the July and October meetings, with one additional cut for 2027.

Economic Data in the Week Ahead

- Monday: Chicago Fed National Activity Index (Jan), Dallas Fed Manufacturing Index (Feb)

- Tuesday: S&P/Case-Shiller Home Price Index (Dec), FHFA Home Price Index (Dec), Conference Board Consumer Confidence Index (Feb), Richmond Fed Manufacturing Index (Feb)

- Wednesday: No notable data

- Thursday: Weekly Jobless Claims, Kansas City Fed Manufacturing Index (Feb)

- Friday: Producer Price index (Jan), Chicago PMI (Feb)