Weekly Economic Snapshot: High Leverage, Low Sentiment

There is currently a stark contrast between everyday consumer confidence and financial market behavior. On one hand, persistent inflation and elevated living costs have driven consumer sentiment to historic lows. On the other hand, financial market participants are exhibiting aggressive risk appetite, with margin debt surging to an all-time high record on the heels of major equity market gains.

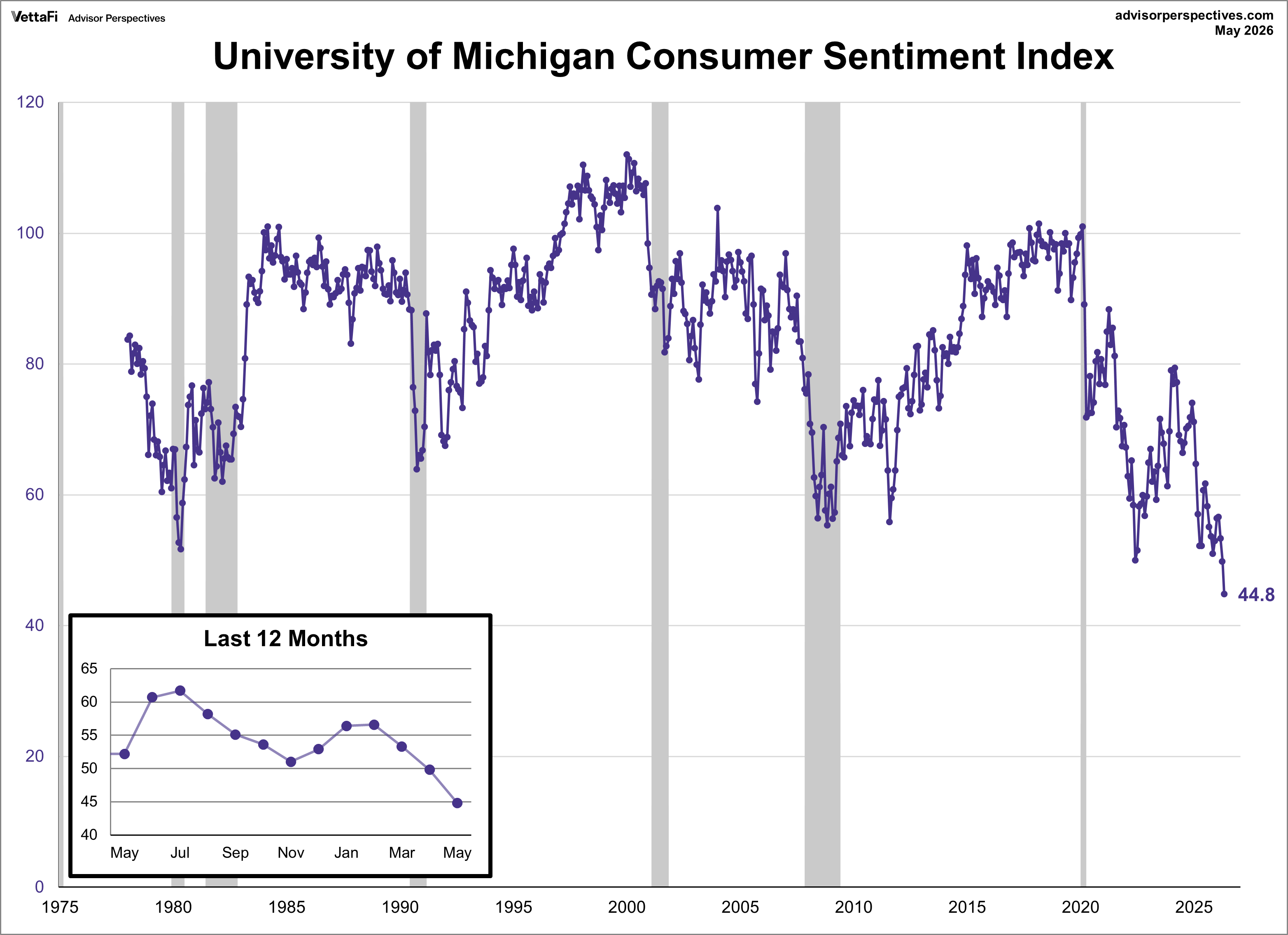

Consumer Sentiment Hits Historic Low Amid Inflation Concerns

Consumer sentiment hit another record low in May, largely driven by high prices and cost of living concerns. The final reading of the Michigan Consumer Sentiment Index came in at 44.8, falling well below the initial forecast of 48.2 and marking a 10% decline from April. The decline in sentiment was widespread across all political affiliations, with the most significant impact observed among lower-income households and individuals without a college education, who are typically more vulnerable to rising costs for fuel and basic necessities.

Record lows were reached in both the current conditions and future expectations subindexes, as both short-term and long-term inflation outlooks worsened. One-year inflation projections edged up from 4.7% in April to 4.8%, the highest level since August, while five-year projections surged from 3.5% to 3.9%, hitting their highest mark since October.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

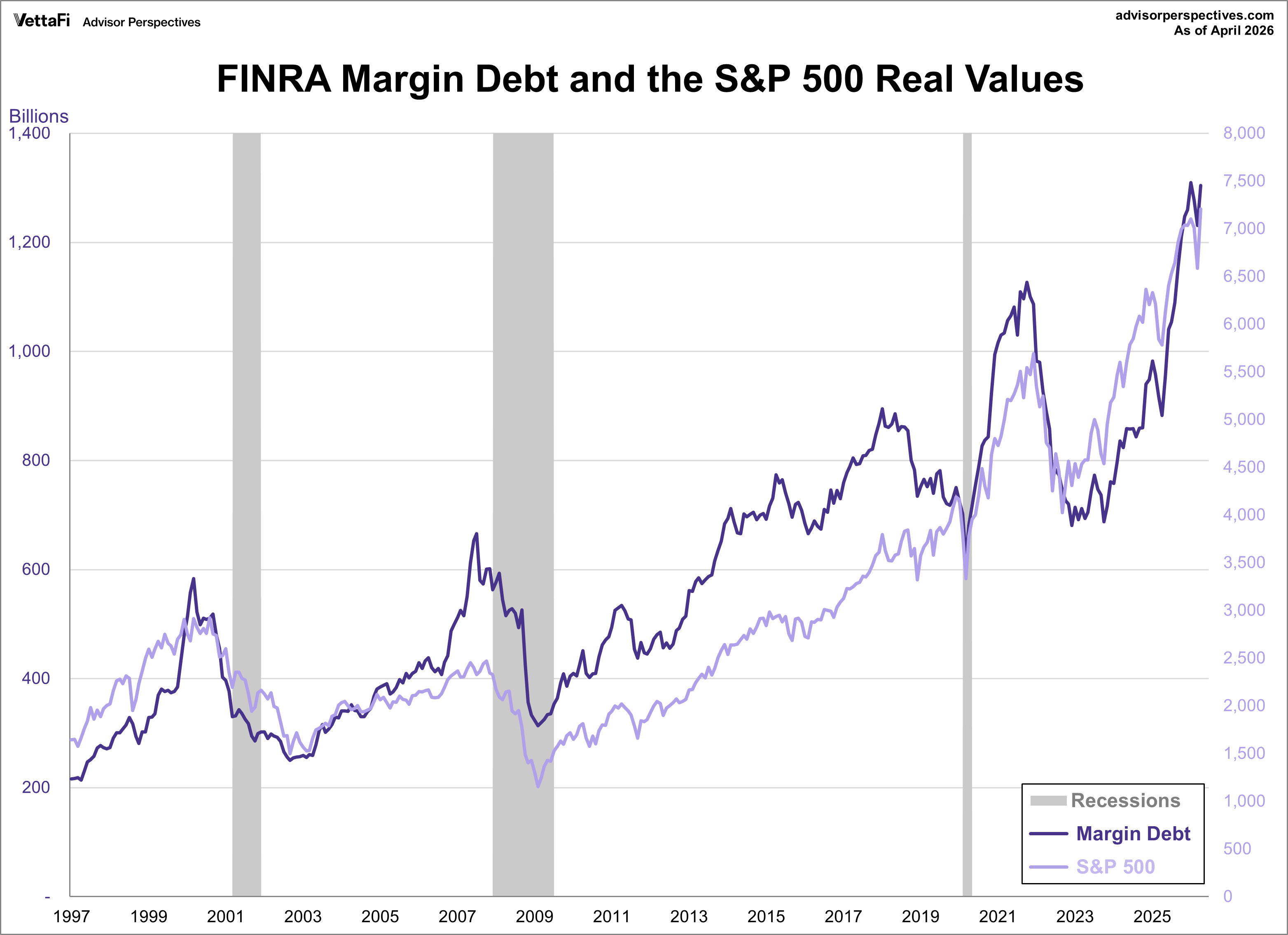

Speculative Borrowing Surges as Margin Debt Hits All-Time High

Margin debt, a significant indicator of investor sentiment and risk appetite, rose 7% in April to $1.30 trillion, its highest level in history. This marks the first increase in three months and suggests a resurgence in speculative borrowing, a move aggressively fueled by the S&P 500’s 10.4% jump in April. Margin debt has now grown over 50% over the past year.

Historically, margin debt and the stock market share a near-parallel relationship. High levels of debt often coincide with market peaks, while troughs tend to precede market bottoms. Although the current record high could reflect strong investor confidence, it also suggests unparalleled risk-taking and increased market volatility.

Market Reactions

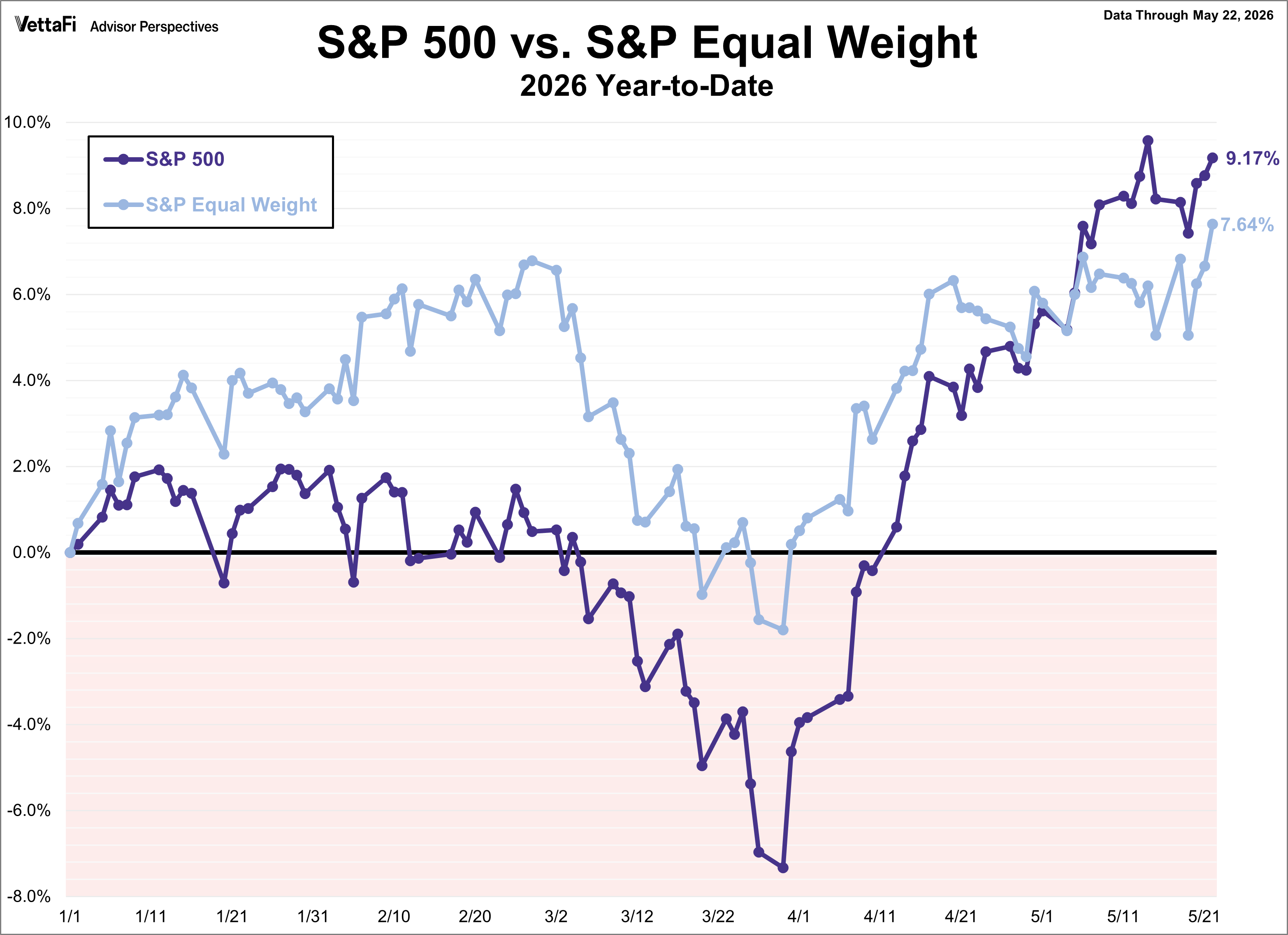

Despite a rough start to the week, the S&P 500 rallied in the back half to post its eighth consecutive weekly gain, its longest streak since 2023. Ultimately rising 0.9%, the index is now inches away from its all-time high. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.9% last week. Meanwhile, the S&P Equal Weight Index was up/down 2.5% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 2.5%.

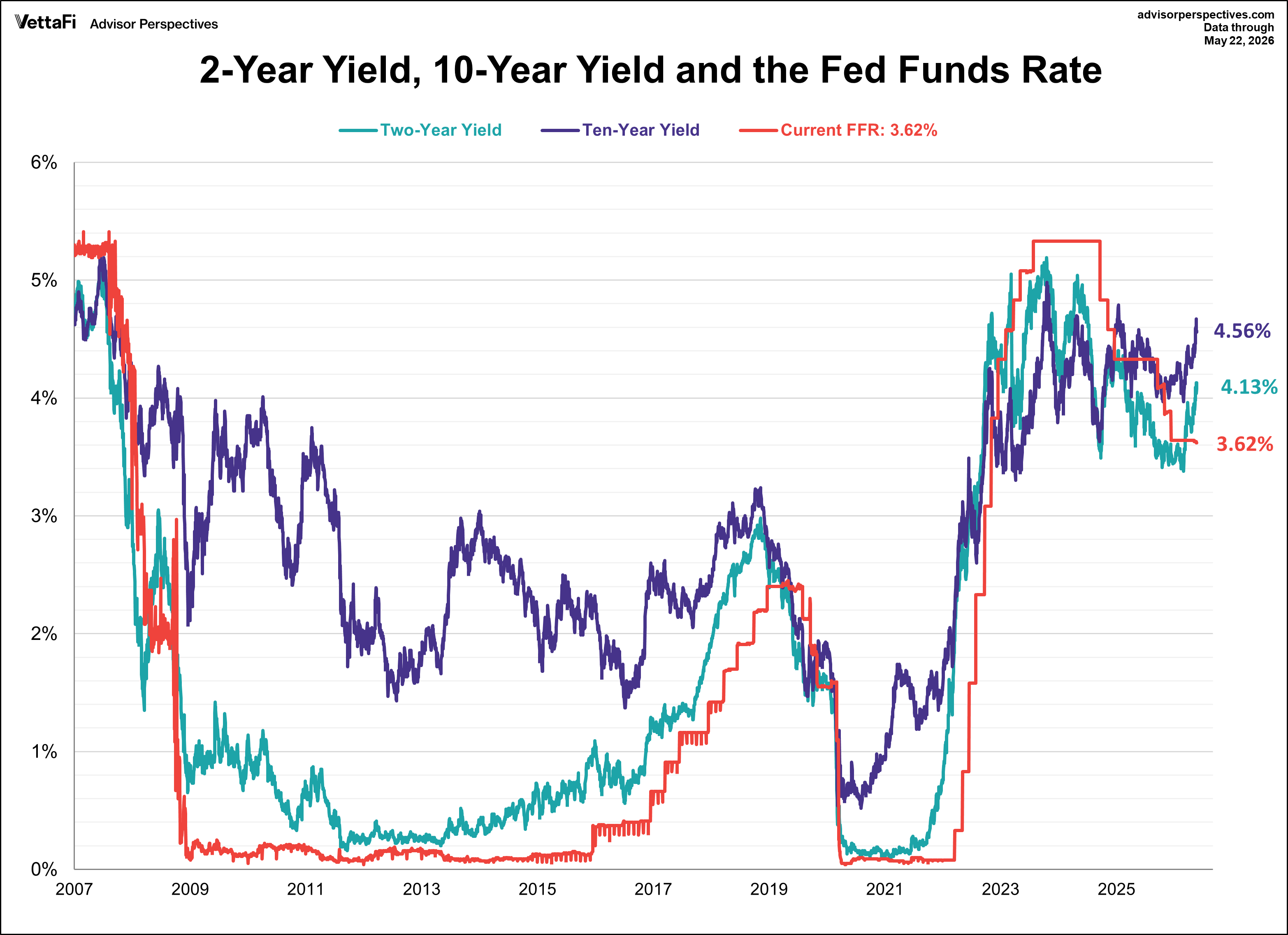

The 10-year Treasury yield finished the week at 4.56%, while the 2-year note finished at 4.13%.

The CMEFedWatch Tool currently shows a 96% likelihood that the Federal Reserve will maintain current rates during next month's meeting, compared to a 4% chance of an increase. Markets are currently pricing in a 25 basis point hike by year-end, potentially arriving as soon as October, followed by no further movement in 2027.

Looking Ahead: Economic Data for the Week of May 26, 2026

- Monday: Holiday

- Tuesday: Chicago Fed National Activity Index (Apr), S&P Cotality Case-Shiller Home Price Index (Mar), FHFA House Price Index (Mar), Conference Board Consumer Confidence Index May), Dallas Fed Manufacturing Index (May)

- Wednesday: Richmond Fed Manufacturing Index (May)

- Thursday: Weekly Jobless Claims, PCE Price Index (Apr), GDP (Q1 Second Estimate), Durable Goods (Apr), Personal Spending (Apr), New Home Sales (Apr)

- Friday: Chicago PMI (May)