The artificial intelligence (AI) boom has transitioned from an equity market narrative to a defining force in fixed income. Hyperscalers (Amazon (AMZN), Alphabet (GOOG/L), Meta (META), Microsoft (MSFT), and Oracle (ORCL)) are shifting from internal cash flows to substantial bond issuance to fund massive data center, graphics processing unit (GPU), and power infrastructure buildouts. This marks a structural change in investment-grade (IG) credit supply, with important implications for duration, spreads, sector composition, and portfolio construction.

In 2025, the five major hyperscalers issued approximately $121 billion in U.S. corporate bonds, more than four times their 2020–2024 annual average of $28 billion. Early 2026 data show continued momentum, with projections for hyperscaler net supply rising 30–50% to $130–150 billion. Overall U.S. IG gross issuance is forecast to hit record levels between $1.8 trillion and $2.25 trillion, with AI-related deals representing a material share. Tech’s weighting in major IG benchmarks has already increased and now accounts for around 10% of the Bloomberg Corporate Bond Index, which is up from 9% in 2024.

This issuance is notably long dated, reflecting the multi-decade useful life of data centers and associated infrastructure. Wall Street estimates center on $300 billion in AI-related IG supply for 2026, potentially delivering $360 billion in 10-year duration equivalents. The result is incremental duration added to portfolios at a time when many investors already grapple with term premium dynamics and a potentially steepening yield curve.

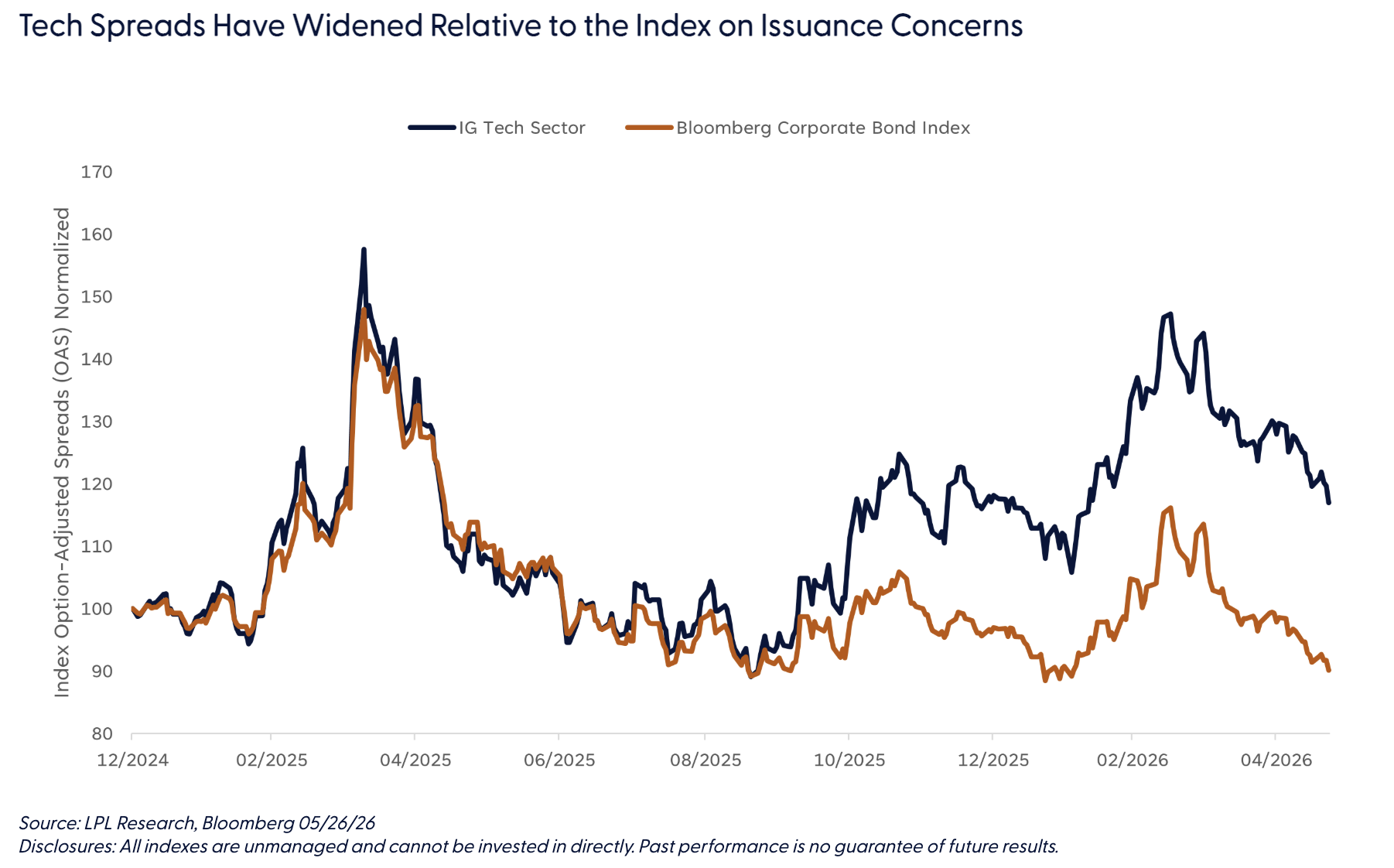

From a credit perspective, the story remains fundamentally constructive. Hyperscalers maintain solid balance sheets, with post-issuance leverage often in the 0.4–0.7x range versus the IG average of near 3x. New-issue concessions have averaged around 12 basis points — wider than the broader market’s ~2.5 basis points — yet deals remain heavily oversubscribed, often 4x or more (meaning for every $1 of debt issuance, there has been $4 of demand). However, despite steady demand, credit spreads (the additional compensation above Treasury securities) have widened for the tech sector relative to the broader IG corporate bond index on issuance concerns. After largely trading in concert with the index, the tech sector has underperformed lately right as issuance started to pick up.

That said, technical pressures are evident. Surging supply amid tight spreads risks modest widening, particularly if merger and acquisition (M&A) activity rebounds or refinancing waves coincide. Concentration risk is rising — the broader tech sector could exceed 12% of benchmarks (currently 10%), introducing greater equity-like correlation during periods of AI hype cycles or regulatory scrutiny.

Read more: How AI May Increase Jobs, Not Replace Them

The AI debt wave underscores a broader truth: innovation-driven capital expenditures (capex) are no longer confined to equity balance sheets. It is actively reshaping the IG universe, creating both challenges and compelling opportunities for those equipped to navigate the dispersion. While tech sector concentration within the broader corporate bond market will likely continue to rise, it is important to note that corporate bonds still represent only 24% of the Bloomberg Aggregate Bond Index. As such, tech concentration risk remains relatively modest within the broader fixed income market (less than 2.5%). And, with spreads still at historically low levels and total yields above long-term averages, the current environment favors income-oriented investors who can largely buy and hold bonds while harvesting coupon payments.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1114528

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial